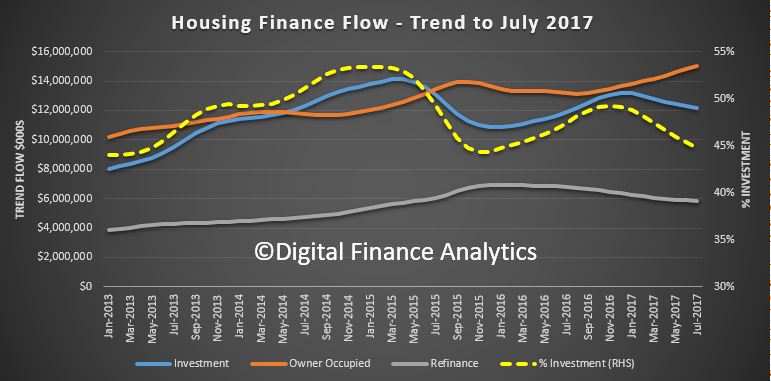

The latest data from the ABS, Housing Finance to July 2017, confirms what we knew. Owner occupied purchases are steaming ahead, while investment lending is stagnating. A clear reflection of the tightening in investor lending regulation, and the availability of new incentives and grants for first time buyers, alongside the attractor loan rates for new borrowers.

We saw first time buyers more active in NSW and VIC, two states where new concessions started in July.

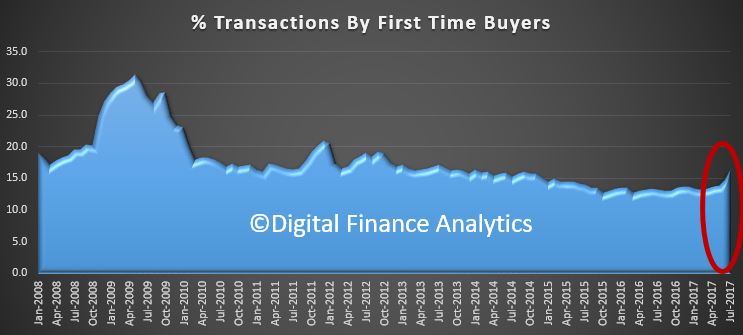

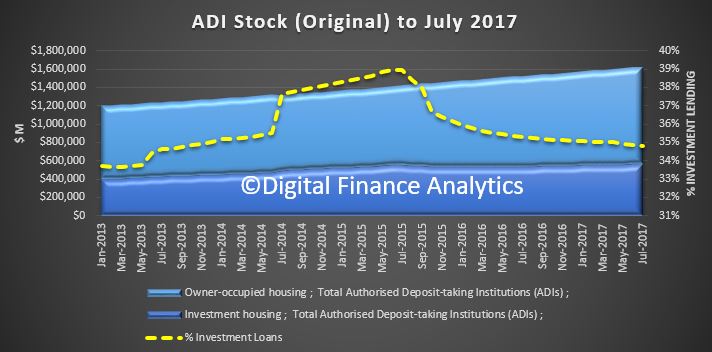

A small but important rise, which is still well below the pre-GFC peak of 30%.

A small but important rise, which is still well below the pre-GFC peak of 30%.

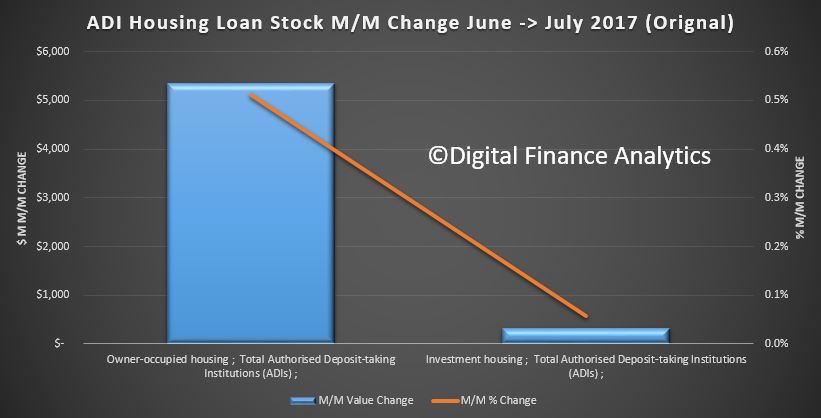

Importantly, owner occupied lending is still rising stronger than inflation or incomes, so the burden of household debt is set to rise further. Some revisions to earlier months data were made, and the RBA already highlighted that $1.4 billion of loans were reclassified between investment and owner occupied loans in the month.

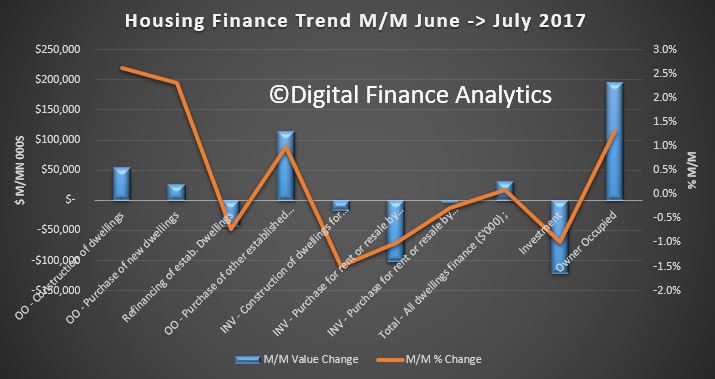

In July, the trend lending flows were $33 billion, up 0.1%, with owner occupied lending up $20.8 billion or 0.7%, and Investment lending down 1% to $12.1 billion. The number of owner occupied transaction rose 0.6%, construction of dwellings rose 2%, new dwellings, 2% and the purchase of established dwellings 0.3%.

In July, the trend lending flows were $33 billion, up 0.1%, with owner occupied lending up $20.8 billion or 0.7%, and Investment lending down 1% to $12.1 billion. The number of owner occupied transaction rose 0.6%, construction of dwellings rose 2%, new dwellings, 2% and the purchase of established dwellings 0.3%.

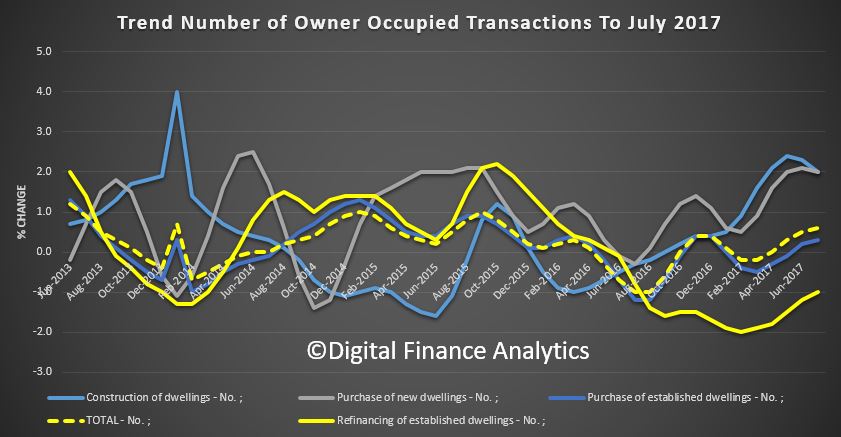

The owner occupied lending trends highlight the rise in loans for construction and new building, as well as a rise in refinanced loans.

The owner occupied lending trends highlight the rise in loans for construction and new building, as well as a rise in refinanced loans.

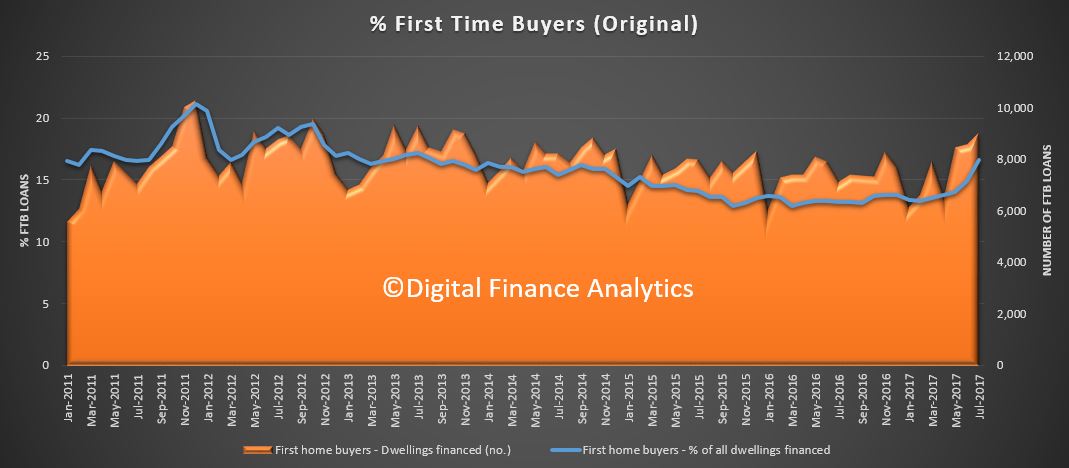

In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments rose to 16.6% in July 2017 from 14.9% in June 2017. The absolute number of loans also rose.

In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments rose to 16.6% in July 2017 from 14.9% in June 2017. The absolute number of loans also rose.

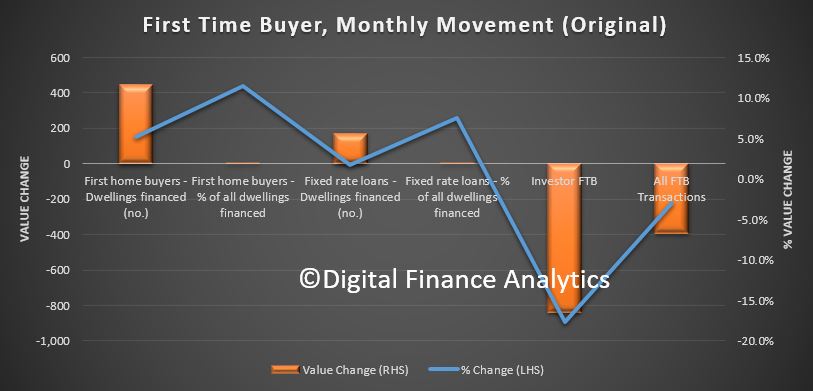

The number of first time buyer investors fell (using data from our surveys) showing a clear movement towards owner occupied first time buyer purchase.

The number of first time buyer investors fell (using data from our surveys) showing a clear movement towards owner occupied first time buyer purchase.

![]() The number, and proportion of first time buyers rose, and there was a rise in the proportion of loans on a fixed rate, reflecting attractive offers, and concerns about future rate rises.

The number, and proportion of first time buyers rose, and there was a rise in the proportion of loans on a fixed rate, reflecting attractive offers, and concerns about future rate rises.

As a result, in original terms, the total pool of loan stock rose more than $6 billion in the month, to another record of $1.61 trillion.

As a result, in original terms, the total pool of loan stock rose more than $6 billion in the month, to another record of $1.61 trillion.

The bulk of the rise was in the owner occupied sector.

The bulk of the rise was in the owner occupied sector.

So the good news for banks is their loan portfolios are still growing, and their margins are now quite healthy. The longer term social impact of households saddled with massive debt will work out over a generation, but it highlights how exposed the nation is to any potential rise in interest rates.

So the good news for banks is their loan portfolios are still growing, and their margins are now quite healthy. The longer term social impact of households saddled with massive debt will work out over a generation, but it highlights how exposed the nation is to any potential rise in interest rates.