The sharing economy has the potential to disrupt current business models, whether its taxis, banking, accommodation or a range of other areas. It also has the potential to be stopped dead in its tracks, if incumbents, or regulation get to dictate too much too soon. This note offers a few observations about the potential of sharing and highlights some of the open but important issues. It is especially relevant given Labor’s announcement on the sharing economy this past week.

First, a few basic points. In December 2014 the Institute of Public Affairs published an excellent report – “The Sharing Economy – How over-regulation could destroy an economic revolution“. It provides an excellent summary of the key issues which need to be considered.

The sharing economy describes a rise of new business models (‘platforms’) that uproot traditional markets, break down industry categories, and maximise the use of scarce resources. The best known services are the ridesharing system Uber and the accommodation service Airbnb. However, the sharing economy extends much further into finance, home tools, investment, and everyday tasks. The ‘sharing economy’ emerged from dramatically falling transaction costs that had prevented certain markets from developing. The sharing economy coordinates exchanges between individuals in much the same way as a traditional market, but does so in a flexible, self-governing, and potentially revolutionary way. These burgeoning benefits are profound: more sustainable use of idle and underutilised resources; flexible employment options for contractors; bottom-up self-regulating mechanisms; lower overheads leading to lower prices for consumers; and more closely tailored and customised products for users.

These sharing economy platforms are only in their embryonic stage of development. The benefits to the Australian economy as the market becomes more efficient are likely to expand. This expansion will only occur if Australia’s entrepreneurs are left to experiment and innovate. The real threat to the sharing economy is government regulation driven by the incumbent industries that are challenged. The danger of excessive legislation and regulation will absorb the gains yielded by technology improvements, preventing mutually beneficial trade and stifling economic growth. This paper recommends new approaches to regulatory design that would encourage the growth of the sharing economy:

- regulators should encourage bottom-up, organic, self-regulating institutions prior to introducing top-down government control;

- occupational licensing needs to be reduced to allow private certification schemes and reputation mechanisms to evolve;

- industry specific regulatory frameworks need to be avoided;

- regulations making it harder for start-ups to compete for labour need to be reduced; and

- the status of individual contractors needs to remain separate from highly restrictive employment law.

Whilst it is hard to keep track of all the new businesses springing up, there is a useful web resource which lists at least sixty locally. From this list we immediately see the breadth of industries which may be impacted. Everyone knows about Uber, the lift sharing service, Airbnb, for accommodation, Open Shed for neighbourhood services and tools, Zopa for finance, Kickstarter for funding for new ideas, and Airtasker for services. It is important to understand how wide-ranging the potential impact may be. Bloomberg Finance recently suggested that finance was potentially the area of largest potential disruption, followed by accommodation and transport.

These businesses only exist because mobile devices, and the internet make real-time collaboration and data sharing possible. The core proposition is peer-to-peer, where a platform facilitates someone with an asset to share that with someone looking for just that thing. As a result, underutilised assets can be better used, and the platform providing both matching, and payments. Users can also rate the product or service, so providers can be scored, to assist future prospective purchasers.

Technology reduces the transaction costs, makes pricing potentially more dynamic, and creates win-wins for seller and purchaser, and it fosters market based transactions. But will the market be sufficient to ensure services are of expected quality and ensure potential consumers are not ripped off? Do some of these models create unacceptable disruptions to existing businesses. If consumers get better outcomes when they use these services will they flourish at the expense of existing operators?

The core question is how and if they should be regulated. Should the sharing economy be allowed to self-regulate? If traditional “top down” forms of regulation are imposed will they simply kill off the business?

Andrew Leigh, Shadow Assistant Treasurer and Member for Fraser has highlighted the regulatory conundrum which needs to be addressed in “Sharing the benefits of the sharing economy“.

Initially, many governments have simply attempted to shut these services down. But forward-thinking regulators are increasingly realising that the sharing economy can deliver big benefits for consumers, while also creating new economic opportunities for the people who provide services through it. So how do we strike a balance between protecting public safety and supporting innovation? How can we ensure providers pay their taxes but don’t end up wrapped in red tape? And how do we open industries up to new competition without inadvertently dismantling important worker and consumer protections? We are just at the beginning of this conversation in Australia, as services like Uber and AirBNB have only been operating here for a short time. Internationally, however, local and state governments have now been grappling with these issues for several years. Exploring how they have responded to the rise of the sharing economy provides a useful starting point in thinking about the kind of regulatory structures we might build here at home.

Uber – restriction or rapprochement?

Ride-sharing app Uber has been perhaps the most controversial of all the new sharing economy services. No small part of the kerfuffle can be sheeted home to the company’s somewhat aggressive business strategies and PR missteps. But it also stems from its success in opening previously locked-up taxi markets to real competition. The regulatory issues surrounding Uber are varied and complex. They include the need to ensure public safety both for those in the car and on surrounding public streets, and the lack of transparency about the company’s pricing model and relationship with its drivers. Then there’s the question of insurance for mixed private and commercial use of a car, and the challenge of ensuring that drivers pay tax on what they earn.

In 2014, Spain sidestepped all of these tough policy challenges by issuing a total injunction against Uber operating in that country. Unlike other attempts at banning the service however, the Spanish authorities went so far as to place associated restrictions on banks and internet firms supporting the Uber app. This detail may well be what lets the Spanish government succeed where others have failed in blocking Uber. That’s because the company might be happy to pay its drivers’ fines from local government authorities, but it simply can’t operate without the payment and communications infrastructure provided by those third parties. At the other end of the spectrum, several US states have now legalised Uber after working with them to come up with tailored regulations. In California for example, local legislators created new rules for ‘Transport Network Companies’, a category which covers Uber, Lyft, Sidecar and any other app offering pre-booked transport in return for a fare. Amongst other things, the rules require these companies to get an operating licence from the California Public Utilities Commission, carry out criminal background checks on their drivers, hold commercial liability insurance worth a minimum of US$1 million, and conduct a 19-point car inspection on every vehicle in their network. Other places, including Pennsylvania and Detroit, have classified these companies as ‘experimental’ service providers, in recognition of the fact that both their long-term impact and viability is unknown. These jurisdictions have given the companies temporary, two-year approval to operate while they decide on a more permanent response. The United States examples may not be exactly right for Australia, but they show that it is possible to regulate sharing economy services without squeezing the life out of them. As for the Spanish approach, it remains to be seen whether an injunction is enough to protect an existing monopoly indefinitely.

AirBNB – no place at home?

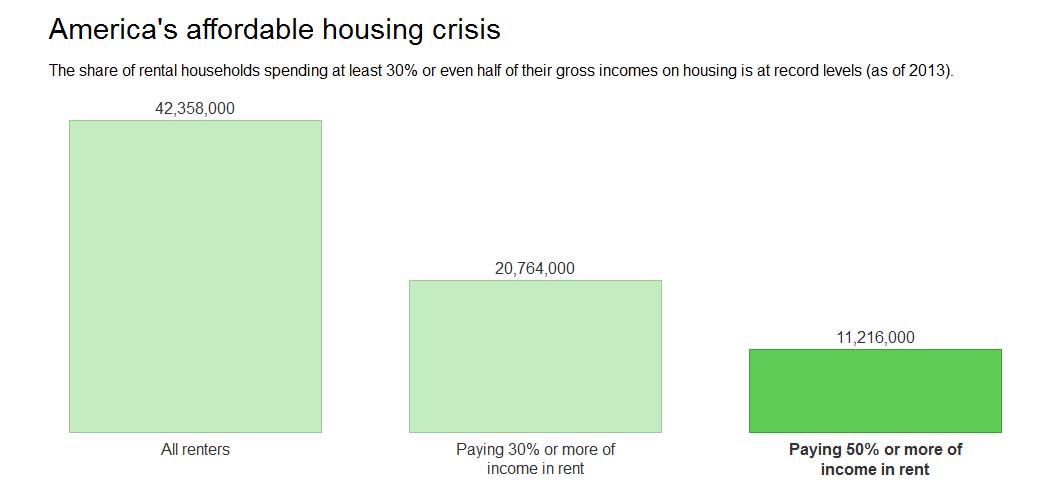

AirBNB’s accommodation service has attracted much less political heat than Uber, perhaps in part because it is not competing so directly with established players. The app lets people rent out a room or two – or their whole property – for short stays, with prices that are often well below hotel rates. Because of this, it has tended to attract intrepid adventurers and people on tight travel budgets, rather than the high-end business travellers who are the hotel industry’s bread and butter. As with Uber, AirBNB raises a host of questions about safety, insurance and tax, as well as public amenity for people who live in surrounding homes or apartments. The service has recently been the focus of major protests in New York, but other cities have reached an accord by acknowledging people’s right to do what they please with their own properties.

For example, Portland now allows its residents to rent out properties through AirBNB as long as they get a licence from the city and have a basic pest and safety inspection done. AirBNB has agreed to collect tax on behalf of the homeowners and pay this directly to the City of Portland. As an incentive for people to do the right thing, the city then channels this into a dedicated rental housing affordability fund. Questions have been raised about the transparency of this approach because AirBNB currently lodges a single tax return, rather than letting authorities know which renters earned what. But it’s a big step up from the unregulated way the company still operates in many other cities around the world. Amsterdam and Paris have similarly legalised AirBNB, but both cities only allow people to rent out their primary residences. This means landlords cannot switch their long-term rental properties to short-stay accommodation, as is often the concern of affordable-housing advocates. It also ensures that people living in apartment buildings don’t have to deal with a constant stream of strangers coming and going year-round. The Dutch have gone so far as the mandate that Amsterdammers may only rent out their homes for up to two months a year, with up to four guests allowed at a time. The Parisians, on the other hand, seem satisfied that the primary residence requirement acts as enough of a natural limit.

Rules like these seem to preserve what’s good about a new service such as AirBNB while limiting some of its negative externalities. That’s a balance Australian lawmakers should also be working towards as we move to clarify our local rules for the sharing economy. It’s unlikely that any government around the world will get sharing economy regulation right on the first go. These services are unprecedented in recent policymaking terms, and how they’ll develop in the long term is largely unknown. But if the benefits are real and the risks are manageable, then there’s a good argument for legalising these services now so that they have a real chance to grow.

If we can get the rules right, this new part of the economy may well bring benefits that everyone can share in.

So back to Labor’s sharing economy principles:

1. Primary property is yours to share The sharing economy has come about through people making better use of their spare rooms, the empty seats in their cars and their unused tools. So when Australians use this primary personal property to deliver services, rules and regulations specific to the sharing economy should be applied. These should involve light-touch regulation which protects consumers without creating undue regulatory burden. But when additional property is being used to deliver services, this does not fall within the scope of the sharing economy. Standard commercial regulations and requirements should apply when an apartment is being rented year-round or someone has a fleet of cars on the road. When applying sharing economy-specific rules and regulation, compliance responsibility should rest with sharing economy platform operators wherever possible. This recognises that these platforms are better-equipped to understand and meet regulatory requirements than the individual Australians providing services through them.

2. New services must support good wages and working conditions Sharing economy services must not undercut the wages and conditions of Australian workers. Companies that facilitate labour hire should ensure their pricing and contracting arrangements allow Australians to achieve work outcomes at least equivalent to the prevailing industry standard. Australians delivering services through sharing economy apps are generally not employees. But it must be recognised that they are not entirely independent contractors either. This is because they do not have the bargaining power to meaningfully negotiate prices or conditions on individual jobs. The Federal Government should look at ways the Fair Work Act, Independent Contractors Act and Competition and Consumer Act could allow collective bargaining by sharing economy workers over issues like pricing, service charges and network access. Commonwealth and State governments should also investigate options for bringing sharing economy workers into insurance and workers’ compensation schemes – as is currently the case for certain independent contractors in states such as New South Wales – and explore reforms to support compulsory superannuation saving through the tax system.

3. Everyone must pay their fair share of tax Everyone doing business in the sharing economy must pay a fair share of tax. Sharing economy companies must pay company tax at the standard corporate rate on all revenue generated in Australia. Australians delivering services in the sharing economy must pay income tax at the standard marginal tax rate relevant to their annual income. They are also required to collect GST when their annual activity exceeds the current GST-exemption threshold. Since all its transactions take place online, the sharing economy has the potential to improve tax collection and simplify taxpaying. To facilitate the payment of tax, sharing economy companies should collect Tax File Numbers or Australian Business Numbers from the Australians operating on their networks and report annual earnings data to the ATO for pre-filling in tax returns.

4. Proper protection for public safety Sharing economy companies and those delivering services through them must have appropriate insurance policies to cover customer and third party risk. Sharing economy companies should work with the insurance sector to develop products which accommodate mixed personal and sharing economy use of property such as cars and homes. These companies should also act as an ‘insurer of last resort’, where doing so does not create unreasonable barriers to entry for new competitors. Compliance responsibility for meeting insurance requirements should rest with the sharing economy companies. They should cite and hold on file relevant insurance documentation for the Australians delivering services through their platforms. Sharing economy services should be subject to the provisions of Australian Consumer Law. This means that Australians are entitled to all standard protections relating to consumer rights, honest conduct and product safety when using these services. State and local governments should develop licensing and inspection codes specific to sharing economy services. For example, in some international jurisdictions governments have opted to take a light-touch approach based on minimum standards and streamlined vetting. These codes should recognise the lower level of risk posed by these services relative to commercial operations, rather than seeking to directly replicate existing regulatory structures. In determining whether sharing economy-specific or standard commercial regulations should apply to a particular activity, the personal property rule should be applied.

5. Access for all Sharing economy services should be required to meet agreed accessibility standards. Not every service will be fully accessible for people with disabilities, but sharing economy companies should negotiate appropriate service levels through binding accessibility agreements with disability advocates. The Australian Human Rights Commission should have jurisdiction under the Disability Discrimination Act to intervene where agreement cannot be reached or negotiated standards are not observed. Sharing economy services should be encouraged to offer platforms that cater specifically to people with disabilities. For example, Uber Assist offers disability-accessible cars and vans.

6. Playing by the rules In a context where tailored, light-touch rules exist for the sharing economy, there should be zero tolerance for companies that continue to flout Australian laws. Sharing economy companies should be subject to heavy penalties if they are found be operating in contravention of laws applying this flexible and responsive framework. Where platform operators repeatedly violate Australian laws, governments should take action to disable their operations.

To me, these seem on one level quite sensible, although it puts the acid on the platform providers to track, trace and report transactions. Such an obligation should be tailored to the size of the business, because if the full obligations are placed on nascent businesses too soon it will kill them, and it will potentially create a concentration of a small number of large scale players, whereas we should be encouraging a thousand flowers to bloom.

I suggest we should bias the regulatory framework to encourage new businesses to develop. Tender plants need carefully husbandry. Legislators must take the time to get the rules right, but with a bias towards facilitating disruption, not stopping it. In Australia, our track record on this is frankly poor, and incumbents often have such strong influence (at a market, and political level) that as a result new sharing economy businesses are likely to get crushed.