The news has been full of stories about how companies such as Amazon, Apple, Google, Microsoft, Starbucks and others are able to shift their profits to low or no-tax jurisdictions by using novel, legally permitted corporate structures and complex internal transactions (known as transfer pricing schemes). Companies are able to do so because they are generally taxed at the place of their residence rather than where the underlying economic activity takes place.

The European Union is estimated to be losing about one trillion euros each year due to a combination of tax avoidance, evasion and arrears. This is bigger than the combined gross domestic product (GDP) of Norway and Sweden and requires political action.

Against the above background, in 2013, the governments of G20 nations asked the Organisation for Economic Cooperation and Development (OECD) to develop proposals for dealing with Base Erosion and Profit Shifting (BEPS).

As part of the BEPS project, the OECD has now completed the first phase consisting of 15 possible actions. These form part of its final reports which exceed 1,000 pages and a summary is available here. There is much to digest and the OECD does offer some ways of tackling BEPS, but ultimately the project is unlikely to make a significant dent in organised corporate tax avoidance.

Profit Shifting

Transnational corporate groups have been very adept at engineering inter-group loans. Under this, one subsidiary borrows from another and pays interest. No cash effectively leaves the group and the interest paid by the paying subsidiary attracts tax relief while the receiving company, often located in low or no-tax jurisdiction, pays no tax on its income. So the OECD suggestion that the tax relief on such interest payments be restricted may dissuade some from opting to adopt these ingenious and complex financial arrangements.

Where does a company like Starbucks make its money?Reuters/Chris Helgren

The OECD has supported calls for country-by-country reporting (CBCR). This requires companies to show the profit they make in each country together with sales, employment and other relevant information. This information can help to illustrate the mismatch between economic activity and profits booked in each country.

But the OECD only recommends that this disclosure be made by each multinational corporation to the tax authority in its home country. To secure this information, governments of other countries will need to enter into numerous treaties. Poorer countries will hardly be in a position to leverage negotiations with more powerful countries. A more efficient solution would be for companies to publish the required information as part of their annual accounts – something the European Parliament has called for.

Out of date

The current corporate tax system was designed nearly a century ago when the contemporary form of transnational corporation, direct corporate investment in foreign operations and the internet did not exist. The OECD has failed to address the three biggest fault lines in the current system. First, under various international treaties, companies are taxed at their place of residence rather than the place of their economic activity. The OECD reforms do not make any significant change.

Second, modern corporations, such as Starbucks and Google, are integrated entities. They coordinate the economic activities of hundreds of subsidiaries to achieve economies of scale, market domination and profits, but for tax purposes are assumed to be separate economic activities. So a single group of companies with 500 subsidiaries is assumed to consist of 500 independent taxable entities in diverse locations. This leaves plenty of scope of profit shifting and tax games.

Third, the profits of a group of companies are allocated to each country by using a system known as transfer pricing. This requires arm’s-length or independent market prices to calculate the price of intra-group inputs and value of outputs to estimate taxable profits. In the era of global corporations, independent prices can’t easily be estimated. For example, as I found in an investigation in 2011, just ten corporations control 55% of the global trade in pharmaceuticals, 67% of the trade in seeds and fertilisers and 66% of the global biotechnology industry.

The way forward

The OECD recognises the problem but does not offer any way forward. Instead, it seeks to repair the current broken system through improved documentation for transfer pricing and international treaties. An alternative approach known as unitary taxation can address the above shortcomings. It treats each group of companies as a single unified economic entity. It recognises that there can be no sale, cost or profit until the company transacts with an external party. Thus, all intragroup profit shifting is negated.

The global profit of an entity is allocated to each country in accordance with key variables, such as sales, employees and assets – and each country can then tax the resulting profit at any rate that it wishes. A system of unitary taxation has been operated within the US since the 1930s to negate the impact of domestic tax havens (for example Delaware) and profit shifting. The OECD could have studied this but chose not to.

The BEPS project is unlikely to be the last word on corporate tax avoidance.

Author: Prem Sikka, Professor of Accounting, Essex Business School, University of Essex

A weakening outlook for the global economy and jittery financial markets do not portend well for the Australian economy. With latest estimates of inflation at 1.5%, below the Reserve Bank of Australia’s target band of 2-3%, and delayed action in raising interest rates by the US Federal Reserve, the CAMA RBA Shadow Board on balance prefers to keep the cash rate on hold, attaching a 72% probability to this being the appropriate policy setting. The confidence attached to a required rate cut equals 14%, up five percentage points from the previous month, while the confidence in a required rate hike is unchanged at 14%.

Australia’s unemployment rate edged down to 6.2% in August, according to the Australian Bureau of Statistics, although the increase in monthly employment fell by more than half compared to July and the participation rate fell to a modest 65%. No new data on wage growth was released.

The Australian dollar’s decline continued to just below US70¢, making Australia’s exports even more competitive. Yields on Australian 10-year government bonds have fallen further to 2.62%, which is very low by historical standards.

The Australian property market is still looking strong, with the construction PMI surging to 53.8 in August, from 47.1 in July. However, in the same month building permits have fallen by nearly 7%. The local stock market has been suffering considerable losses, the S&P/ASX200 closing below 5000 earlier this week. With heightened uncertainty affecting global capital markets, it is unlikely domestic share prices will rebound significantly.

Data on the international economy has weakened. The US Federal Reserve has delayed the highly anticipated increase in the federal funds rate, citing low inflationary pressure and fragile capital markets. Delayed action by the Federal Reserve is likely to reduce the pressure to increase the domestic cash rate. In Europe, attention has shifted from the Greek debt crisis to the unabating refugee crisis. China’s economy continues to slow, with its manufacturing sector contracting for the second month in a row.

Many experts are now expecting China’s GDP growth to fall to 6%. Global capital markets continue to pose threats. According to the Institute for International Finance, net capital outflows for the world’s emerging markets will be negative this year, the first time since 1988, pointing to weak growth in the region. Commodity prices remain subdued.

Consumer and producer sentiment measures paint a motley picture. The Westpac/Melbourne Institute Consumer Sentiment Index fell back to 93.9 in September, from 99.5 in August. Business confidence, according to the NAB business survey slid further, from 10 in July to 4 in August and now 1, at the same time as the AIG manufacturing and services indices, both considered leading economic indicators, continued to improve slightly.

What the CAMA Shadow Board believes

The Shadow Board’s confidence that the cash rate should remain at its current level of 2% equals 72% (down from 77% in September). The confidence that a rate cut is appropriate has edged up a further five percentage points from the previous month, to 14%; conversely, the confidence that a rate increase, to 2.25% or higher, is called for is unchanged at 14%.

The probabilities at longer horizons are as follows: six months out, the estimated probability that the cash rate should remain at 2% equals 25% (27% in September). The estimated need for an interest rate increase lies at 62% (65% in September), while the need for a rate decrease is estimated at 13% (8% in September). A year out, the Shadow Board members’ confidence in a required cash rate increase equals 68% (six percentage points down from September), in a required cash rate decrease 14% (9% in September) and in a required hold of the cash rate 18% (unchanged).

Author providedAuthor providedAuthor provided

Comments from Shadow Reserve bank members

Paul Bloxham, Professor of Economics at Australian National University:

“Economic activity is gaining momentum.”

Author providedAuthor providedAuthor provided

The fall in the Australian dollar in recent months means that financial conditions have loosened noticeably. There is increasing evidence that the lower currency is working to support growth. Services exports are picking up, which combined with the ongoing upswing in housing activity, is lifting business conditions and jobs growth. Although GDP is growing at a below trend pace, the broader collection of activity indicators suggests that economic activity is gaining momentum, supported by very loose financial conditions. I recommend that the cash rate is left unchanged this month and expect that the cash rate is more likely to need to rise from here than fall, although not for some time yet.

Mark Crosby, Associate Professor, Melbourne Business School:

“Address weak economic fundamentals through reform rather than monetary policy.”

Author providedAuthor providedAuthor provided

Despite recent suggestions that the RBA should cut, it would appear unwise to do so in a world where the Fed is now very likely to raise at its next meeting. While Australia’s economic fundamentals are weak, issues are more properly addressed through tax, competitiveness and other reforms than through further loosening already loose monetary policy. Issues with excessive debt remain significant in many economies, and Australia ought not to exacerbate potential problems on that front through cutting rates. The medium term question is still how rates become normalised as at least some other advanced economies raise rates.

James Morley, Professor of Economics and Associate Dean (Research) at UNSW Australia Business School:

“The RBA can probably wait until US liftoff.”

Author providedAuthor providedAuthor provided

Despite the collapse of commodity prices and the effects of this on the stock market, the Australian economy has adjusted to the post-mining boom era reasonably well. This has been helped by the previous cuts in the policy rate and will continue to be supported by a weak Australian dollar. But the low interest rates also have risks in terms of large price swings in the housing market and excessive credit growth. Given all of this, the RBA should not lower the policy rate further. At the same time, the RBA can probably wait until US liftoff and more solid indications of inflationary pressures to start raising rates.

Jeffrey Sheen, Professor and Head of Department of Economics, Macquarie University, Editor, The Economic Record, CAMA:

“There is a significant risk of escalating market pessimism.”

Author providedAuthor providedAuthor provided

The US Federal Reserve did not change the target federal funds rate in September, given the sluggish world economy and fragile financial markets. These concerns will remain probably through to 2016. With input prices falling, inflation is unlikely to be an issue anywhere in the rich world for the forseeable future, and so there is no reason to act pre-emptively. Many central banks have cut interest rates in the last year including Australia, Canada, China, Denmark, Euro area, India, Israel, New Zealand, Norway, Russia, South Korea, Sweden and Switzerland. The time to change course is a way off, and in particular for Australia.

There are few indications of how potential GDP growth in Australia might go above the current 2%. A surge in China’s imports from Australia is unlikely. The new treasurer Scott Morrison appears likely to consolidate government expenditure. Business investment is still in retreat.

While some worry about a possible bubble in property prices, the September 2015 RBA Bulletin shows that there has been and remains significant structural excess demand for housing services in Australia, which is even more pronounced in NSW. The recent APRA-induced credit market tightening may have little effect on this structural excess demand, and may well dim one of the few bright lights in the economy – dwelling construction.

There is a significant risk of escalating market pessimism, which would be stoked by tightening monetary policy. For all these reasons, my recommendation has an increased weight on an interest rate cut, though no change still dominates for the October meeting.

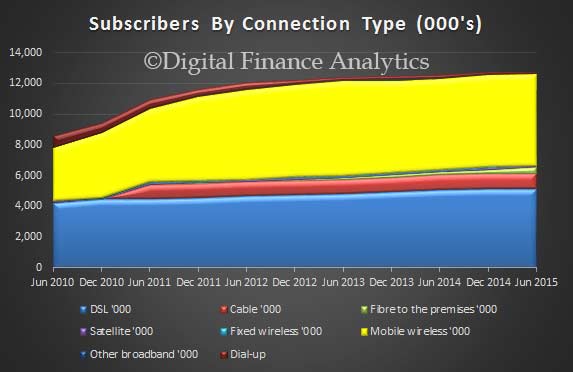

The latest internet usage statistics from the ABS, released today, to June 2015 shows there were approximately 12.8 million internet subscribers in Australia at the end of June 2015. This is an increase of 2% from the end of June 2014. Our own surveys show that many households enjoy multiple internet connections, including a fixed line ADSL service, and mobile services, so subscriptions should not be equated with individual households (there are about 9 million separate households). This again highlights the digital disruption underway, which creates both opportunity and risk. The trends in our Quite Revolution Report on digital channels, if anything, understated the speed of change.

As at 30 June 2015, almost all (99%) internet connections were broadband. Fibre continues to be the fastest growing type of internet connection in both percentage terms and subscriber numbers. Internet subscriptions to a fibre connection increased by 107% (or 217,000 subscribers) from the end of June 2014 to the end of June 2015.

There are more mobile subscriptions than fixed subscriptions now, with 47% of subscriptions being for mobile services and 40% on ADSL services.

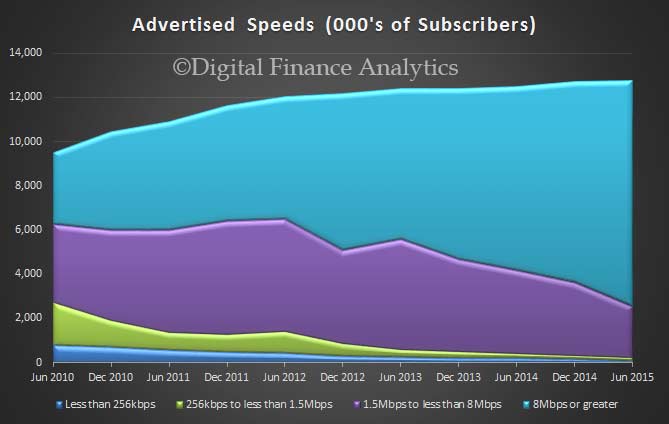

The average speeds are increasing significantly, with more than 80% of subscribers now enjoying download rates of 8 Mbps more higher.

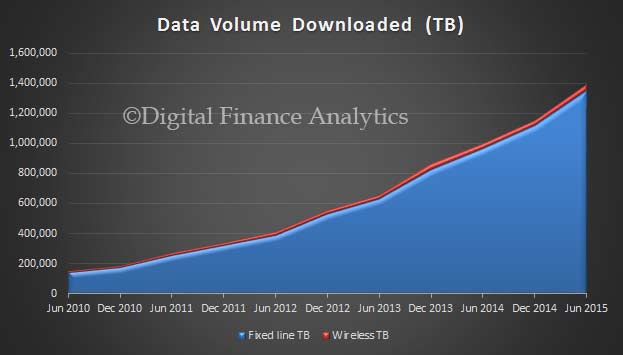

The volume of data being downloaded has risen significantly, especially via fixed line networks. Total volumes have more than doubled since 2012.

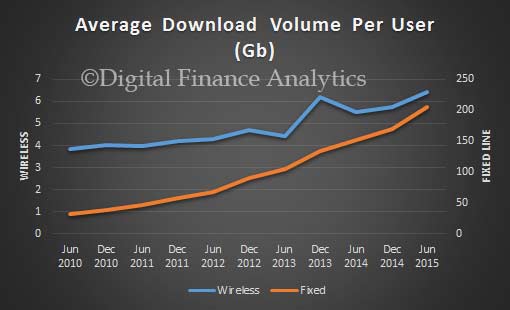

The average user on a mobile subscription downloads about 6 Gb of data, up from 4 Gb in 2010 per month. However the real growth has been in fixed line services, where the average user is now close to 200 Gb a month, compared with 45 Gb in 2010.

At its meeting today, the Board decided to leave the cash rate unchanged at 2.0 per cent.

The global economy is expanding at a moderate pace, with some further softening in conditions in China and east Asia of late, but stronger US growth. Key commodity prices are much lower than a year ago, in part reflecting increased supply, including from Australia. Australia’s terms of trade are falling.

The Federal Reserve is expected to start increasing its policy rate over the period ahead, but some other major central banks are continuing to ease policy. Equity market volatility has continued, but the functioning of financial markets generally has not, to date, been impaired. Long-term borrowing rates for most sovereigns and creditworthy private borrowers remain remarkably low. Overall, global financial conditions remain very accommodative.

In Australia, the available information suggests that moderate expansion in the economy continues. While growth has been somewhat below longer-term averages for some time, it has been accompanied with somewhat stronger growth of employment and a steady rate of unemployment over the past year. Overall, the economy is likely to be operating with a degree of spare capacity for some time yet, with domestic inflationary pressures contained. Inflation is thus forecast to remain consistent with the target over the next one to two years, even with a lower exchange rate.

In such circumstances, monetary policy needs to be accommodative. Low interest rates are acting to support borrowing and spending. Credit is recording moderate growth overall, with growth in lending to the housing market broadly steady over recent months. Dwelling prices continue to rise strongly in Sydney and Melbourne, though trends have been more varied in a number of other cities. Regulatory measures are helping to contain risks that may arise from the housing market. In other asset markets, prices for commercial property have been supported by lower long-term interest rates, while equity prices have moved lower and been more volatile recently, in parallel with developments in global markets. The Australian dollar is adjusting to the significant declines in key commodity prices.

The Board today judged that leaving the cash rate unchanged was appropriate at this meeting. Further information on economic and financial conditions to be received over the period ahead will inform the Board’s ongoing assessment of the outlook and hence whether the current stance of policy will most effectively foster sustainable growth and inflation consistent with the target.

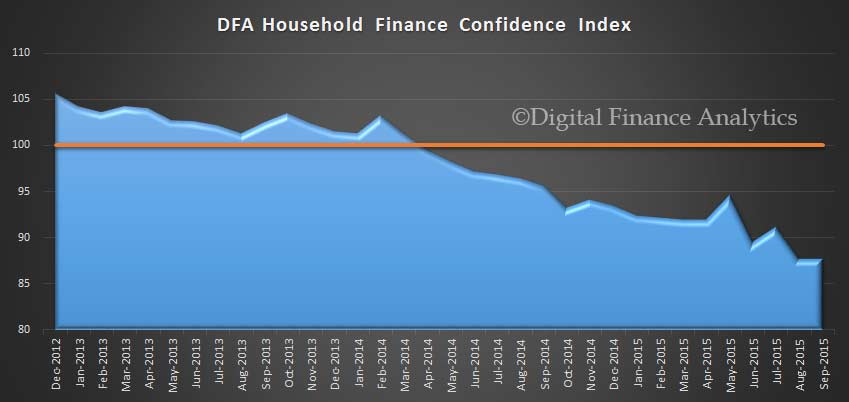

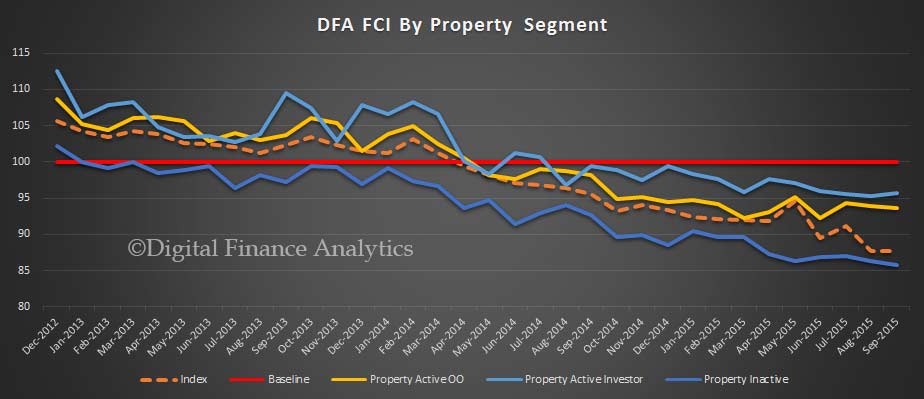

The negative household confidence sentiment continued in September according to the latest results from our household surveys, released today. The overall score was 87.73, compared with 87.69 last month. These are levels well below 100 which is a neutral result, and still in the lowest region since 2012 when the DFA FCI started. The instability in the financial markets, flat real income growth, and rising costs swamped any positive impact on the change of Prime Minister overall. Households with property investments remain significantly more confident than those who are property inactive.

The results are derived from our household surveys, averaged across Australia. We have 26,000 households in our sample at any one time. We include detailed questions covering various aspects of a household’s financial footprint. The index measures how households are feeling about their financial health.

To calculate the index we ask questions which cover a number of different dimensions. We start by asking households how confident they are feeling about their job security, whether their real income has risen or fallen in the past year, their view on their costs of living over the same period, whether they have increased their loans and other outstanding debts including credit cards and whether they are saving more than last year. Finally we ask about their overall change in net worth over the past 12 months – by net worth we mean net assets less outstanding debts.

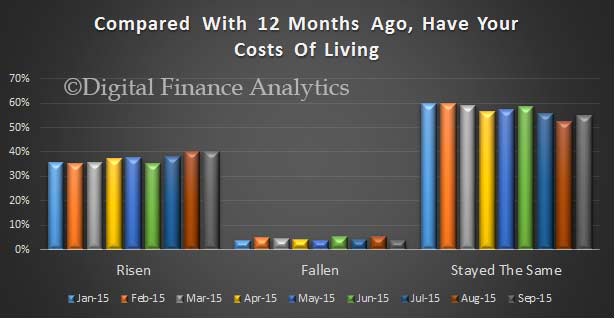

Looking in detail at the elements which drive the survey, 40% of households said their costs of living had risen in the past 12 months, a rise of 0.17% from last month. Only 3.6% of households said their costs had fallen, down 2% on last month. Major movements were driven by the rising costs of some supermarket goods, as well as child care and school fees. 55% of households said their costs of living had not changed in the part year, a rise of 2.5% from last month. The majority of younger households were significantly worse off.

Turning to income, after inflation, 4.8% of households said their incomes had risen, up 0.6% on last month, whilst 40% said their real incomes had fallen, down 2% on last month. 55% said there had been no change in the part 12 months. Those relying on income from savings continue to be hit by low deposit account interest rates, and recent stock market falls. We saw a number of households report a fall in overtime, especially in WA and SA, whilst in NSW and VIC additional work was a little easier to find.

Next we look at debt. 11% of households were more comfortable than 12 months ago, little changed from last month. Many of these continue to pay ahead on their mortgage, and are reducing credit card debt. 27.7% of households were more uncomfortable than a year ago, up 0.38% on last month. Those younger households with a owner occupied mortgage were most concerned, and in addition, we noted the rise of concern among those using credit cards to balance their spending. The ongoing low mortgage rates on owner occupied mortgages provides a buffer, and so far, the higher rates on investment loans have not worked through to dent confidence. 58% of households were as comfortable with the debts they service, very similar to last month.

Looking specifically at savings, 13.2% were more comfortable, down 0.4% on last month. 31.1% were less comfortable, up 1% on last month, thanks to stock market volatility and ultra low bank deposit rates. There was a higher concern now that the Government may impose more tax on superannuation following the change of leadership. 54% of households were still as comfortable compared with 12 months ago, little changed on the month.

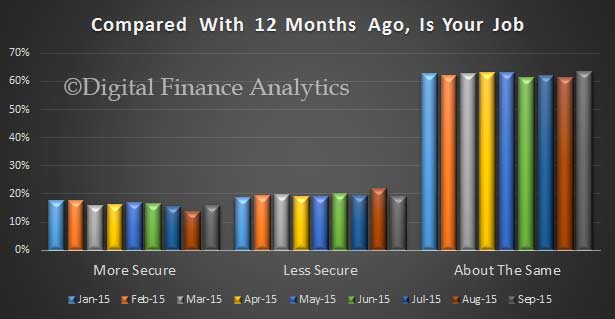

The state variations in job security are becoming more pronounced, with WA, SA and NT all showing greater concerns, whilst NSW and VIC continued to improve. We noted those currently working in the construction sector were more concerned this month, thanks to an expected development slow-down. Those more secure than last year rose 2.1% to 15.9%, thanks to the NSW and VIC effect. 63% of households were as confident as 12 months ago, up 2%, whilst those less confident overall fell by 2% to 19%. However, there are a number of moving parts which are working in different directions, and which are averaged away in the national summary.

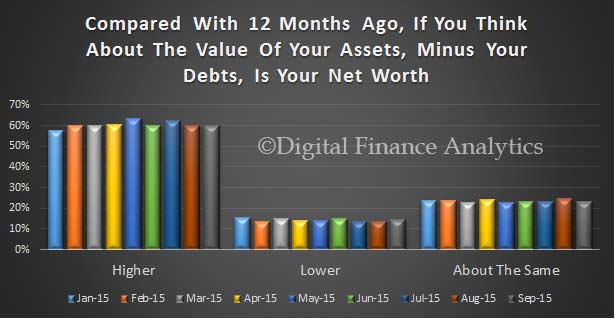

Finally, we look at net worth, a measure of overall value held, net of debt by households. Overall, those with higher net worth than a year ago remained at 60%, whilst those with lower net worth rose 1% to 14.5%. 23.5% of households said they had no overall change, up 2.6% on last month. There are again offsetting forces at work in these results, with sustained house price growth in NSW and VIC more than offsetting falls in the stock market. On the other hand, states where house prices were weaker, were more likely to see net worth fall, because mortgage debt is still high.

If we look at the overall index by property segment (as defined by DFA), those who are property inactive (either renting, living with friends, at home, or in public housing) had a lower confidence score, because they had all the pressures created by rising costs, static or falling incomes, and no upside from property. Investment property investors were the more confident (though still well below the 100 neutral level), and owner occupied home owners are between the other two segments.

Overall then household financial confidence continues to languish, despite record low interest rates. Because of this we believe many households will continue to spend carefully, and be careful not to extend their high personal debt further. We also see how property is supporting the confidence levels significantly, and of course if this changed for any reason (for example, static or falling capital growth, or rising rates) confidence would be significantly dented further. The future of housing has become the key to confidence.

St George Bank ruined a lot of bank holiday plans this weekend when their online banking systems stopped working.

The bank’s Internet systems appear to have stopped working on Sunday evening and were still unavailable almost 24 hours later on Monday afternoon. ATMs were working but, as it was a bank holiday, branches were closed meaning that people who rely on the Internet for account transfers and overseas credit card transactions were out of luck.

Apart from a short message acknowledging the outage on their website, St George has not yet given details of the causes of the problem.

But this was not the only recent Internet banking outage at a major bank.

On the 11th and 12th September, the Commonwealth Bank (CBA) suffered a prolonged disruption to its IT services in particular its ‘industry leading’ banking platform – NetBank. And this was not the only prolonged outage at CBA this year. There were IT service disruptions earlier this year, with failures to transfer money into and out of accounts, thus racking up late and overdraft fees for customers. And also last year, and before that …….

For those who would like to see the impact of such outages on CBA customers, the excellent website Aussieoutages has a whole section devoted to CBA and a blog on which customers can register their frustration, with many of the comments NSFW – as social media terms bad language.

So what has the Commonwealth Bank to say for itself about the latest outages? Nothing!

Where are the banking regulators when banking customers are inconvenienced by the banks that they are paying records fees to?

Unfortunately, APRA and ASIC continue to play pass the parcel on banking regulation.

OK, but which regulator should be wielding the big stick?

In 2011, DBS Bank, the largest bank in Singapore, suffered a computer outage that deprived its customers of access to banking services for about seven hours (half of that experienced by St George customers).

After an investigation, the local banking regulator, the Monetary Authority of Singapore (MAS) hit DBS with a stern rebuke and a set of new regulatory requirements. The bank was also ordered to “redesign its online and branch banking systems platform to reduce concentration risk and allow greater flexibility and resiliency in operation and recovery capability”. In other words – fix your IT systems, or else.

Importantly, the regulator ordered DBS to increase the capital held in reserve for ‘operational risks’ by 20 per cent, or around $180 million. Under the Basel II banking regulations, banks are required to maintain a capital buffer against operational losses, in particular ‘systems risks’.

Because the failure of Internet systems is clearly an operational risk problem, APRA should be considering at least a 20% addition to the operational risk capital charge on Commbank and Westpac (which owns St George and the other banks like BankSA which went offline at the same time). According to Commbank’s latest Risk (so-called Pillar 3) report, which incidentally has pictures of happy Internet users on the front page, a 20% increase would have CBA having to raise just over an additional $500 million of capital. On the same basis, Westpac would require just under $500 million extra capital. Good luck with that, when banks are scrambling to raise capital to cover upcoming regulatory changes.

But has APRA moved to get the IT systems of the country’s biggest banks under control? No sign so far.

So what of ASIC?

ASIC has recently released its regulatory stance on so-called Conduct Risk, or “the risk of inappropriate, unethical or unlawful behaviour on the part of an organisation’s management or employees”. Conduct Risk is the very latest in regulatory fashion and is an attempt to get banks to treat their customers more fairly.

One would have thought that, in return for account fees, providing access to customers’ own money might be a start for banks?

But a quick look at the ASIC web-site shows the usual list of fines and suspensions on financial institutions so tiny that small fry seem huge. But not a whale or even a barramundi in their nets. ASIC does not go after the big fish.

So which regulator should be going into bat for the costumers of the big banks?

Both!

APRA to ensure that IT systems in banks are robust, by using capital tools. And ASIC to ensure that banks treat customers fairly. Demanding return of fees for non-performance might be start?

Author: Pat McConnell, Honorary Fellow, Macquarie University Applied Finance Centre, Macquarie University

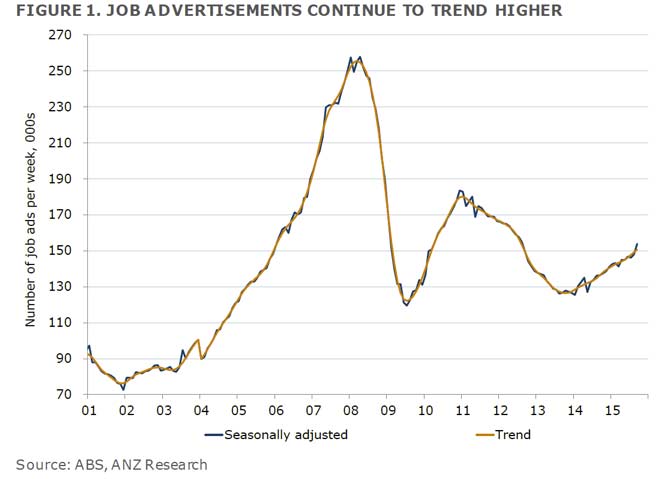

Further more postive economic indicators. According to ANZ Research, Job advertisements jumped 3.9% m/m in September in seasonally adjusted terms after rising by a solid 1.3% m/m in August. In trend terms, job ads were up 1.0% m/m and growth since mid year now appears a little stronger than previously. The number of internet job ads grew 4.0% m/m in September following an increase of 1.3% m/m in August. Internet job ads were 13.7% higher than a year earlier. The number of newspaper job ads (2% of total job ads) declined 2.7% m/m in September, after rising for two consecutive months.

The OECD’s final package of proposals for reforming the international system for taxing companies brings to an end the two-year BEPS project led by the OECD and other G20 countries which also included participation by representatives of developing countries, business, academia and NGOs.

Developing the BEPS, or Base Erosion and Profit Shifting reform package has been a remarkable endeavour involving thousands of hours of work and meetings – and thousands of pages of background work, interim proposals and commentary. All this has been in response to the undoubted need to reform a dysfunctional and ailing system.

It seems likely that, irrespective of the actual outcome, politicians will hail the BEPS project a success. Despite not having yet seen the final proposals we are prepared to disagree. The BEPS project may lead to some improvement but it will not lead to an international tax system fit for the 21st century. It might appear churlish to reach this conclusion before the final proposals have been published, so let us explain why.

In the February 2013 report that kicked off the project, the OECD made it clear that its aim was to close loopholes and tighten and extend existing rules to shore up the current system. It was equally clear that the fundamental framework underpinning the system was to remain in place. Subsequent BEPS documentation confirmed this.

However, the major problems afflicting the international tax system ultimately stem from flaws in the framework underpinning it. If that same framework remains in place, those problems cannot ultimately be resolved.

Double trouble

There are two major flaws. First, the current framework relies at its heart on concepts and distinctions that are not suited to the realities of a contemporary multinational enterprise operating in a global business environment.

Essentially, the international tax system addresses the possible double taxation of income arising from cross-border activity by allocating primary taxing rights between “residence” and “source” countries. In a “1920s compromise” in the League of Nations, source countries were allocated primary taxing rights to the “active” income of the business and residence countries the primary taxing rights to “passive” income, such as dividends, royalties and interest.

This might have been a sensible system in the 1920s but it is ill-suited to dealing with modern multinationals operating in a truly global business environment. Modern multinationals have shareholders scattered across the world, a parent company resident in one country, a potentially large number of affiliates undertaking an array of activities, such as research and development, production, marketing and finance that are located in many different countries, and consumers that could also be scattered across the world.

In such a scenario, there is no clear conceptual basis for identifying where profit is earned; all those locations may be considered to have some claim to taxing part of the company’s profit.

Best intentions?Reuters/Pool

Conceptually, the residence/source and active/passive distinctions do not offer much help. In practice, applying these distinctions in the context of intra-group transactions, where affiliated entities in different jurisdictions are assigned the status of “source” or “residence”, gives rise to extensive and significant problems, not least those relating to pricing transfers within the multinational group. Overall, they lead to a system which is easily manipulated, distortive, often incoherent and unprincipled.

Unhealthy competition

Second, the system invites governments to destabilise it by competing with each other for economic activity, tax revenue and possibly to try to advantage their own domestic companies. For at least 30 years this has led to gradual reductions in effective rates of taxation of profit. Governments around the world compete in this way while also demanding that companies should pay their “fair share” of tax, whatever that may be. This tension is particularly evident in the UK, where the goal of having the most competitive corporation tax regime in the G20 is held concomitantly with an active role in pushing forward the BEPS project.

Competition is not only on rates, but also on many aspects of the tax base. Over the years countries have introduced rules that enhance their competitive position or seek to give an advantage to domestic companies, but in practice facilitate the erosion of the tax base of both domestic and foreign jurisdictions and thus further destabilise an already fragile system. For example, as well as reducing tax rates, countries have introduced patent boxes with lower rates of tax on royalty income, and relaxed anti-avoidance measures intended to prevent international profit shifting.

These two flaws will continue to afflict the international tax system even if the proposals resulting from the BEPS project were to be implemented adequately by all states. For this reason, we do not believe it will lead to an international corporate tax system fit for the 21st century.

Authors: Michael Devereu, Professor of Business Taxation, University of Oxford, John Vell, Associate professor and Senior Research Fellow at the Oxford University Centre for Business Taxation (CBT), University of Oxford

Data from the US Bureau of Labor Statistics for September suggest that the Fed may delay their much anticipated, and continually postponed, interest rate rise. This is a reaction to slowing world trade, China, and financial market uncertainty, as well as as series of downward revisions to earlier months data.

Their September data showed that total nonfarm payroll employment increased by 142,000 in September, and the unemployment rate was unchanged at 5.1 percent. Job gains occurred in health care and information, while mining employment fell. Wage growth was zero.

In September, the unemployment rate held at 5.1 percent, and the number of unemployed persons (7.9 million) changed little. Over the year, the unemployment rate and the number of unemployed persons were down by 0.8 percentage point and 1.3 million, respectively.

The number of persons unemployed for less than 5 weeks increased by 268,000 to 2.4 million in September, partially offsetting a decline in August. The number of long-term unemployed (those jobless for 27 weeks or more) was little changed at 2.1 million in September and accounted for 26.6 percent of the unemployed.

The civilian labor force participation rate declined to 62.4 percent in September; the rate had been 62.6 percent for the prior 3 months. This level of participation has not been seen since the 1970’s. The employment-population ratio edged down to 59.2 percent in September, after showing little movement for the first 8 months of the year.

The number of persons employed part time for economic reasons (sometimes referred to as involuntary part-time workers) declined by 447,000 to 6.0 million in September. These individuals, who would have preferred full-time employment, were working part time because their hours had been cut back or because they were unable to find a full-time job. Over the past 12 months, the number of persons employed part time for economic reasons declined by 1.0 million.

In September, average hourly earnings for all employees on private nonfarm payrolls, at $25.09, changed little (-1 cent), following a 9-cent gain in August. Hourly earnings have risen by 2.2 percent over the year. Average hourly earnings of private-sector production and nonsupervisory employees were unchanged at $21.08 in September.

Labour party leader Jeremy Corbyn this week unveiled his new team of economic advisers. He hopes they will help build a set of policies capable of countering the narrative of belt-tightening austerity which delivered David Cameron and George Osborne into Downing Street back in May.

Corbyn and shadow chancellor John McDonnell are scheduled to meet four times a year with the seven-strong group which includes people like Thomas Piketty and Mariana Mazzucato. Also on the panel is City University professor Anastasia Nesvetailova, an expert on the international financial sector and its role in the global financial crisis of 2007-09. We asked her to give her thoughts on four policy areas reportedly under consideration by Corbyn and his team:

Q: The new Labour leadership has indicated support for a financial transaction tax, but why does support for this ebb and flow so much?

The idea for the Tobin tax, so called after the economist James Tobin suggested it in the late 1960s to early 1970s, has been long debated. This concept of applying a relatively tiny tax to every financial transaction tends to be evoked in the midst of financial crises and instability, or whenever the costs of finance to society appear to outweigh the benefits of deregulated finance.

Forex fight.REUTERS/Damir Sagolj

It may be comparatively mature as a concept then, but the Tobin tax has been difficult to implement in real policies. During its early life, the idea was eclipsed by the paradigm of monetarism and free markets of the 1970s and 1980s. And throughout there have remained unresolved technical issues about its implementation.

One major divisive issue has been the scope of a possible tax: should it be universal and global (to minimise regulatory arbitrage), or can it be implemented on a different scale by individual nation states? The Tobin tax was originally proposed to target the foreign exchange market – a segment of financial volatility, speculation and bubbles. Today though, we know that the foreign exchange market is only one part of the financial system – albeit a very large part at about a US$5 trillion daily trading volume.

Many other financial transactions today are multi-layered and multi-jurisdictional – very often they involve complex credit contracts. And so a tax designed when the realities of financial markets were quite different and less advanced may not be applicable to all financial transactions today uniformly.

Another issue is how to tailor such a measure to the complexity of today’s financial structures and not harm the needs of businesses and consumers who rely on the foreign exchange market for their daily business needs. Finance is famously prone to speculation and bubbles, but it is an organic and very central sphere of economic activity in advanced, highly financialised capitalism; we need to be cautious about tinkering with the inner workings.

Q: Is there a future for Britain free of the dominance of the financial sector?

This is a tricky question, because it presumes that the financial sector is counterpoised to the rest of economic activity. In reality, we are all part of finance today, and that includes the shadow banking system – a complex set of non-bank financial intermediaries, transactions and entities. Overall, the City of London financial sector plays a crucial role in providing market and funding opportunities for the economy. A better question would be to ask: how can the financial sector today work for society?

It is true that competition and financial innovation can and does spur economic growth and makes our daily lives much easier: it is convenient to rely on credit cards when you travel or to be able to take a mortgage. But financial innovation is also inherently very risky. Hyman Minsky, the theorist of financial fragility who did not live to see many of his predictions come true, said that in advanced capitalism there is always a trade-off between financial innovation and economic stability. Looking back at the unresolved legacy of the 2007-09 crisis, it is clear that the question about who should assume the risks incurred by the financial industry during the “good times”, has not been addressed by policy-makers fully.

Taxpayer funded. RBS.REUTERS/Luke MacGregor

Instead, society and the state, were made to work for finance: in 2007-08, the risks from financial innovation were socialised and austerity measures followed. This happened against the big gains from financial innovation that had been privatised by the finance industry. As a result, despite the progress on the financial reforms since 2008, we are ill-prepared for the next financial crisis, which according to Minsky, is certain to come.

Q: What should a new Bank of England mandate look like?

The Bank of England should remain independent, but it should have the power and the tools to continue to act as a stabiliser of the economy and be able to intervene with a diverse and flexible range of tools during a period of financial crisis or instability. It is important to understand that uncertainty about central banks’ mission and mandate today is not a unique problem of the UK.

During the crisis of 2007-09, the central banks on both sides of the Atlantic stepped in and played a role that they were not meant to. We are lucky that they did so. Against many economic dogmas, they were not simply lenders of last resort, they made the markets, as my colleague Perry Mehrling argues in his book New Lombard Street. They made the markets when liquidity vanished and when private participants, buyers and sellers, simply would not pick up the phone.

In the wake of Lehman, along with the governments, central banks saved the payment system from a collapse. And although it was meant as a temporary solution, there was no exit strategy from that role. Up to this day, central banks are de facto in charge of much more than simply price stability.

Notes and queries. How can the BoE be better put to use?natalie, CC BY-NC

The problem is that the formal mandate of the Bank of England is too narrow for what is required of the central bank in the advanced financialised context. The risk is that during the next financial crisis they may not have the tools to intervene. Central banks are major actors in financially advanced economies and in any plans for a major recovery they are likely to remain so. They will need new tools to deal with what will be an unavoidably a complex crisis.

Q: Is there a feasible place for public ownership in the banking sector?

Again, an interesting question because somehow it assumes that public ownership is alien to the banking system. In reality, public ownership is already present in finance: as a policy measure when banks are nationalised and a potential measure when a bank is identified as a systemically important institution and its failure threatens the economic stability.

One of the major triggers of the great transformation of banking in late 20th century was the move (in the US) to put investment banks into the hands of markets and the ownership of shareholders. The major consequence of that decision was that the risks that previously were theoretically containable in closed partnerships arrangement, were potentially socialised. Simply put, large bank holding companies trading in the markets have systemic consequences for the economy – and a collapse may trigger systemic risks beyond this particular institution.

This is exactly what happened in 2007-09, when the UK government had to nationalise several banks in order to save them from a collapse. Since banks are crucial systemic institutions in our economy, and since they perform many utility-like functions (payments, clearing) critical for the economic security of the country, it can be argued that public ownership is best suited to guard the public interest in utility banking. And in fact, given our experience in the financial crisis, it can be argued that they were, in effect already nationalised.

I can anticipate a counterpoint from the banking industry: public ownership is wasteful, it stifles innovation and competition. But while the benefits of privately-owned banking groups are difficult to quantify, data suggests that bank executives and managers were rewarded handsomely even as their institutions were making losses and were on a public liquidity drip and, further, that in finance, innovation takes the form of regulatory arbitrage and avoidance, rather than the benign pursuit of the public good.

Author: Anastasia Nesvetailova, Professor of International Politics, Director of the Global Political Economy MA, City University London