Many older Australians are living in larger dwellings than they need after their adult children leave the family home. The 2011-12 ABS Survey of Income and Housing shows households aged 55 and over are more than twice as likely to have three or more spare bedrooms in their home than those aged under 55.

However a report released by the Productivity Commission today found most people are happy staying in their family home, despite a common perception that such homes are too big for them.

For some older home owners, this may well represent a positive choice driven by lifestyle reasons or because of an attachment to the family home. But for others, the decision to remain in place may be forced by barriers that prevent them from downsizing into a smaller or cheaper property.

The Productivity Commission says there is a general lack of affordable downsizing options for older Australians, due in large part to the red tape and inconsistencies within state and territory land planning regimes. Older people who wish to downsize also face financial barriers inherent in the tax-transfer system.

There is an opportunity to promote more efficient use of housing stock by relaxing the disincentives to downsizing among seniors, and to reap something of a “double dividend” from so doing. This would free up housing space for younger families. And older home owners would be able to release some equity from their home by downsizing into a cheaper property. This would in turn help supplement incomes in retirement.

A recent report on population ageing by the Bankwest Curtin Economics Centre found downsizing activity to be quite limited among older Australian home owners. During 2001-13, the incidence of moves among home owners aged 45 and over was just 5%. Among those who did sell their family home only to buy a new one, less than half moved into cheaper dwellings.

Financial barriers to downsizing

There is general consensus that the tax-transfer treatment of downsizing proceeds blunts incentives for seniors to downsize. Firstly, net proceeds from downsizing are subject to means tests. Secondly, stamp duty has to be paid on new home purchases.

A comparison across the five most populous states in Australia show the impact stamp duty has on the decision to downsize.

From 2001 to 2013, downsizing accounted for 28% of all property moves in Western Australia by homeowners aged 45 and over. Equivalent downsizing rates were substantially higher in other states – 36% in Victoria and more than 40% in NSW. At the same time, the average incidence of stamp duty on housing equity released through downsizing was highest in WA at 25%. This compares to just 15% in Victoria and 12% in NSW.

Median stamp duty as a percentage of median housing equity released through downsizing by owners aged 45 years and over, by State, 2001-2013

However, a closer look reveals that jurisdictional differences in stamp duty parameters are not the cause of the relatively high stamp duty burden in WA. The fact is that older West Australians tend to downsize into homes of higher value than older home owners in other states. This finding is not surprising given the year-on-year spike in house prices that occurred in WA during the last decade’s resource boom. A growing lack of affordability in local housing markets is eating into expected returns from downsizing.

From piecemeal to meaningful tax reforms

Some recent attempts have been made to improve downsizing incentives, but the measures have been rather piecemeal. For instance, the 2013 downsizing pilot program proposed by the Federal government attracted criticism for its restrictive eligibility conditions. Stamp duty concessions for downsizing have been implemented in some states and territories. But they simply do not go far enough to overcome the combined financial and emotional costs of moving out of a home in which families have been raised, and memories built.

Economists have long argued for the total abolition of stamp duty. It is often recommended that this should be accompanied by the levying of a broad-based land tax. This two-pronged reform would not only cushion revenue incomes for the State but also promote affordability as land tax is capitalised into lower land prices. Such reform measures are of course feasible. But they are conditional on both tiers of government being willing to share the cost of transitional arrangements for existing home owners.

However, what is often overlooked are the structural problems inherent in the general tax-transfer treatment of housing assets. The exclusion of the primary home from welfare means tests has encouraged extensive accumulation of wealth in housing assets by home owners. Not only is the entire value of the family home exempt from assets testing, home owners enjoy a wider range and higher levels of housing subsidies than renters, including but not limited to the First Home Owner Grant, land tax exemption, capital gains tax exemption and non-taxation of imputed rent. Put bluntly, current tax-transfer settings simply do not offer any financial incentives for seniors to divest their housing wealth through downsizing or any other means.

The preferential tax-transfer treatment of home ownership has also helped fuel house prices to historically high levels, making it difficult for seniors to find affordable properties to downsize into in their local area. If tax reform is to be successful in encouraging downsizing among seniors, it will have to deal with an entrenched structural problem that has contributed to a long-run inflationary bias in housing markets.

Fitch Rating. says that after its latest stress tests, the Bank of England’s (BoE) assessment is that the UK banking sector is adequately capitalised and the results will not force any capital planning revisions. Further sector-wide capital step-ups are unlikely in future.

Capital ratios are likely to remain stable, held up by the BoE’s increased use of countercyclical buffers. These will be built up as lending growth accelerates and will be released when the cycle turns. The BoE’s intention is that banks’ capital planning should become more efficient and flexible. The BoE’s Financial Policy Committee indicated that it considers a Tier 1 capital adequacy ratio of 11% to be appropriate for the sector. Fitch expect banks to set their internal buffers relative to this level and plan their capital needs relative to the level of sensitivity to stress test inputs.

Results from yesterday’s stress test show that, under the baseline scenario, the seven participating banks are improving their capital positions. But the Royal Bank of Scotland Group (RBS; BBB+/Stable) and Standard Chartered (A+/Negative) did not meet the BoE’s capital requirements under the stress scenario. Both banks have taken, or are taking steps this year to address capitalisation.

The regulator will use future stress test results to assess individual banks’ capital requirements. Fitch expects the tests to become more sophisticated and more qualitative in nature. This is already the case in the US where the Federal Reserve’s annual Comprehensive Capital Analysis and Review plays an important role in how the country’s leading banks assess their capital planning exercises.

In the UK, annual cyclical tests will be run to capture risks from financial cycles, with the severity of scenarios increasing as risks build up. This should produce more rounded stressed results. Latent risks not captured by the annual cyclical scenario will be introduced every other year when the BoE will run a biannual stress test. Fitch thinks the banks should, over time, be able to anticipate broad movements in the annual cyclical scenario, making it easier for them to set internal buffers above minimum regulatory requirements, based on their expected sensitivity to the regulatory stress test.

The 2015 stress test hurdles – a 4.5% common equity tier 1 (CET1) ratio and a 3% leverage ratio – were not particularly onerous. All participating banks met these. But hurdle rates will evolve and banks will need to meet their Pillar 1 minimum CET1 ratios under stressed scenarios, plus any additional requirements set by the regulators under Pillar 2A and buffers for systemically important banks.

The prospect that the central banks of the US and the eurozone will soon make opposing moves on policy rates has allowed financial markets once again to demonstrate their neuroses. Some market participants are expecting exchange rate turmoil – but while this may always make good copy, it does not always follow from good analysis.

We saw this kind of frenzied response over the summer, when a couple of small changes in the Chinese renminbi exchange rate and continuing problems in Greece (an economy accounting for less than 2% of eurozone GDP), seemed to be capable of stopping rational analysis in its tracks.

The raison d’etre for financial markets is rather simple: they price the ongoing story of risk and ensure that assets consequently give an appropriate pay-off. Now, if markets cannot manage to price risk very well, then they tend to claim that uncertainty – by which we mean things we do not understand very well – has beaten them. For highly paid, intelligent individuals that is not a very good answer, particularly when it is used as an excuse to ask for extensions of the ultra-low interest rates that have made the whole tiresome business of capitalism so much simpler. More worryingly, of course, it means that something quite fundamental has gone wrong.

Accounting for changes

Indeed, the prospect that the US Federal Reserve will raise rates, as might the Bank of England next year, should be a clear signal for rejoicing rather than dread. The normalisation of interest rates is a sign that we are returning to normal times and is not a problem per se.

Equally, normalisation does not mean that the crisis is over or that there may not be troubles ahead. But it does indicate that we are probably past the worst of the ills stemming from the crisis of 2007-8. That is surely a good thing.

So why is the European Central Bank expected to cut rates again, or even extend the scale of QE, when its American equivalent is heading in the other direction?

Well, in the UK and the US, rates have been in the doldrums since 2008-9 when extensive quantitative easing (QE) policies were also started. However, in the eurozone, even though there has been extensive provision of liquidity, peripheral countries such as Portugal, Spain, Ireland and Greece suffered from the twin reinforcing problems of sovereign debt crises and bank fragility.

Eurozone QE was only started in January this year, rather late, and in a monetary union that lacks an appropriate degree of cross country fiscal insurance. Look, for example, at the extent to which the rest of the UK has been able to support Scotland following the collapse in oil prices. And so, given lacklustre average growth in the eurozone, it is hardly surprising that interest rate policy is not quite ready to normalise and indeed may need to be somewhat more supportive.

Same journey, different car

The key to understanding central banks is that they do not wish to jeopardise hard-won reputations for price stability. This means that they will use policy rates, and whatever influence they have on other market interest rates, to ensure that domestic inflation and longer term expectations for inflation continue to be consistent with price stability. Any divergence in policy rates between the US and Europe is simply like saying they are in different places on the map but still are trying to get to the same point.

Let me illustrate with a simple example. If Country A and Country B both suffer a common shock and have a similar economic structure, then policy rates will tend to move together and the economies will plot a similar path back to full employment.

But if Country A is booming and Country B is undergoing retrenchment, then the common aims will imply quite different responses. Country A will raise rates. This makes borrowing more expensive and saving more lucrative which will bear down on aggregate demand through the usual channels of consumption and investment. Country B will cut rates or, if they are already close to zero, increase quantitative easing in the hope of stimulating activity.

A key part of the transmission mechanism of these interest rates changes will be the exchange rate. The expectations of a higher interest rate in Country A, will lead to an appreciation in its exchange rate relative to Country B and this will further act to suppress demand in Country A. Also, rather handily, it will stimulate exports from Country B which will now be cheaper. The jump in the exchange rate is exactly what both countries need to help them get to their destination. The exchange rate thus allows risk to be shared, thankfully.

Off the charts

Euro-Dollar Swap Spread and Spot Exchange Rate 2000-2015.Source: Macrobond

So does divergence matter at all? Not if it simply promotes an orderly adjustment in the exchange rate. The chart above shows a plot of the daily euro-dollar exchange rate (blue) against the euro-US spread in two-year swap rates (red). The difference in short term market interest rates such as swaps sounds complicated but is simply a measure of market participant’s expected costs of borrowing in euros as opposed to dollars. If the swap rate spread is high, it means that we expect US rates to be higher than European rates on average over two years.

And as we might reasonably expect, the exchange rate, to a significant degree, reflects changes in these relative interest rates, particularly since 2008. And so it is simply a function of the relative stance of monetary policy and part of the expected adjustment mechanism.

For example, we can see that in both 2008-2009 and also in 2010-2011 the rise in the dollar was associated with a fall in the euro-dollar swap rate spread. Moreover, the two-year appreciation in the dollar since 2013 has been associated with a 100 basis point fall in the euro two-year swap rate versus the dollar two-year swap rate. To the extent that monetary policy divergence simply promotes these kinds of stabilising changes in the euro-dollar exchange rate, then bring it on; it is precisely what both economies need.

Author: Jagjit Chadha, Professor of Economics, University of Kent

If digital disruptors like crowd-sourced equity funding and peer-to-peer lending platforms are going to transform the finance sector, they need to be regulated. If they are going to create permanent positive change, they need to be regulated intelligently.

But so far, the ability of regulators and industry to agree on the rules has been hampered by a significant knowledge gap: there is no accurate, up-to-date information about the size, scale and scope of the rapidly growing online alternative finance sector in our region.

The University of Sydney Business School has joined forces with the United Kingdom’s University of Cambridge and Tsinghua University in China, to conduct the first comprehensive survey of the rapidly expanding alternative finance sector in China and across the rest of the Asia-Pacific.

Building on a successful 2015 benchmarking survey of the UK and Europe, the Asia-Pacific survey will run through to mid December 2015. By early 2016, we will have aggregate information about the various types of online platforms, the overall size and recent growth of the alternative finance sectors in Australia, New Zealand, Singapore, China and other Asia-Pacific neighbours.

Why is aggregate data on crowd-sourced and peer-to-peer finance so critical? Uninformed regulation can indeed be harmful — so why regulate at all? Direct connection between lenders and borrowers, or donors and causes, is part of the attraction of alternative finance, and that’s all between consenting adults after all. But it’s the “peer-to-peer” feature of these markets that calls for intelligent regulation.

Naïve ideology sees all regulation as anathema to free markets. In reality, most markets can’t function without it. Efficient markets depend on reliable information about product quality being shared between buyers and sellers, as Nobel prize winner George Akerlof demonstrated in his analysis of the used car market – his famous work on the “market for lemons”.

If buyers can’t tell whether they are buying a good car or a lemon they will never pay what a good car is worth. Owners of good cars will not offer their cars for sale and eventually only lemons will be left. Markets with this unequal information problem are likely to collapse without minimum quality guarantees.

In crowd-funded and peer-to-peer finance markets, the borrower knows much more about their ability to repay than the lender does. Minimum credit worthiness standards for borrowers, some limitations on risk exposure for unsophisticated lenders, and effective disclosures are needed for the survival of these platforms.

Take peer-to-peer lending for example. In conventional lending markets an intermediary like a bank transforms the deposits of lenders into loans for borrowers. Intermediation turns one person’s bank deposit into another person’s loan but no individual depositor cops a direct hit if a particular borrower defaults; the intermediary bears this risk. Of course, banks charge for the service of disconnecting lenders from the risk of individual borrowers.

This charge partly accounts for the (at least 10 percentage points) difference between term deposit rates and personal loan rates.

Peer-to-peer lending uses a direct connection between lenders and borrowers. This allows the platform to shrink the difference between lending and borrowing rates. Someone wanting a $5,000 loan for a holiday might register with a peer to peer platform. If they default on their repayments, whoever lent them the money bears the loss. While the average default rate across all loans on a peer-to-peer lending platform in normal times might be low – say less than 3% – the actual outcome for each lender depends on the specific borrowers they lend to and economic conditions at the time.

Without some minimum guarantees and lender protections, interest rates and charges are likely to rise as poor quality borrowers (lemons) drive out good quality borrowers, and the market will collapse. Similarly, the crowd-sourced equity platforms that can enable brilliant and highly profitable new ideas (so-called “unicorns”) to find capital depend on regulatory protection for unsophisticated investors. Stability, sustainability and trust are needed so we can all benefit from the accessibility and efficiency of this digital disruption.

Most alternative finance providers now operating in Australia are well aware of the need for sustainable business practice. Peer-to-peer lenders, for example, check the credit worthiness of borrowers in conventional ways, using credit history, capacity to pay, and sometimes secured assets. The platforms usually spread lenders’ funds across a range of borrowers, and facilitate payments and repayments.

However minimum regulatory guidelines ensuring good practice will protect the sector from “fly-by-night” entrants with lower standards. Setting those minimum standards well can only be done with comprehensive data on the alternative finance sector.

We don’t want to lose or delay the benefits of digital disruption in finance simply because not enough is known about the structures and participants.

Author: Susan Thorp, Professor of Finance, University of Sydney

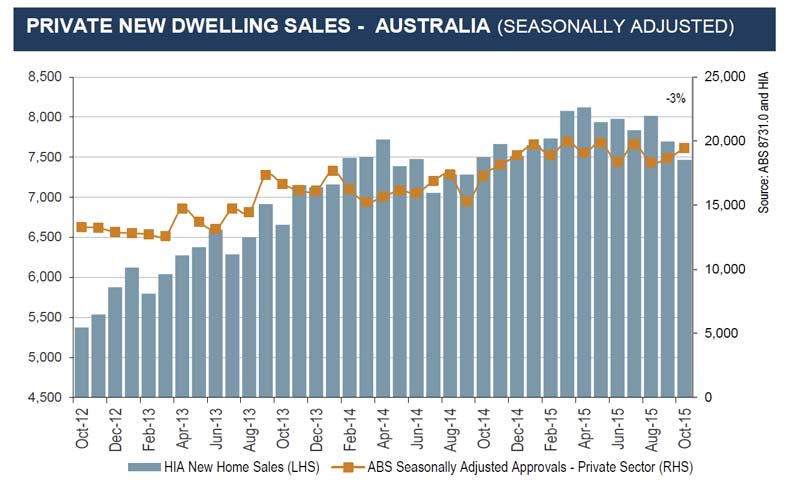

The HIA New Home Sales Report, a survey of Australia’s largest volume builders, reveals that while sales volumes are off their peak they are still holding up relatively well.

The latest update – for October 2015 – reveals a decline of 3.0 per cent in total seasonally adjusted new home sales. Detached house sales fell by 4.1 per cent while the sale of ‘multi-units’ notched up a 1.0 per cent gain.

In the month of October 2015 detached house sales declined in four out of the five the mainland states. Detached house sales fell by 9.3 per cent in Victoria, 5.4 per cent in Western Australia, 0.9 per cent in Queensland and 0.8 per cent in New South Wales. Detached house sales increased by 2.6 per cent in South Australia.

The Australian Competition and Consumer Commission has granted authorisation for five years to the Australian Retail Credit Association Ltd (ARCA) in relation to principles for exchanging comprehensive consumer credit data between signatory credit reporting bodies and lenders.

ARCA represents lenders and credit reporting bodies in Australia and has developed the principles in a process involving its members and industry since July 2013. This follows reforms to the Privacy Act which expand the type of consumer credit information that can now be shared.

The ACCC received a large number of submissions from industry in response to the application and its draft determination, with general support for the principles.

“Access to more consumer credit information will allow lenders to make better credit decisions, with resulting benefits for consumers in the form of greater financial inclusion for consumers and assisting to reduce consumer over-indebtedness,” ACCC Deputy Chair Delia Rickard said.

“This will lead to increased competition between credit reporting bodies and between lenders, and assist lenders to comply with their responsible lending obligations at less cost.”

The ACCC has considered a concern raised that some provisions are unduly prescriptive and will impose costs on smaller credit providers who wish to have an agreement with more than one credit reporting body. Also consumer advocacy bodies want to include provisions about recording repayments under financial hardship arrangements.

“The ACCC accepts that there are some potential public detriments arising from the costs imposed by the provisions. However, these costs appear to be relatively small and offset by the cost savings and other benefits of these provisions,” Ms Rickard said.

“Each credit provider will make a commercial decision whether or not to provide data and consume data from multiple credit reporting bodies.”

“ARCA is working to resolve the issues around reporting of financial hardship arrangements, and will need to involve industry and relevant regulators. The ACCC will be keen to see this matter resolved in assessing any application for re-authorisation.”

Authorisation provides statutory protection from court action for conduct that might otherwise raise concerns under the competition provisions of the Competition and Consumer Act 2010. Broadly, the ACCC may grant an authorisation when it is satisfied that the public benefit from the conduct outweighs any public detriment.

In March, the Reserve Bank commenced a review of the regulatory framework for card payments. As part of this process, the Bank released an Issues Paper that noted some developments in the payments system that raised concerns given the Bank’s mandate to promote competition and efficiency in the payments system. Bank staff have since consulted extensively with stakeholders on these matters.

At its meeting of 20 November, the Payments System Board agreed to consult on changes to the standards for card payment systems. The Bank has today released a Consultation Paper containing amended draft standards. A summary of the proposed reforms is provided below and in some Q&A on the Bank’s website. Stakeholders are invited to make submissions on the draft standards by 3 February.

The draft standards include changes to the regulation of surcharges on card payments and interchange payments in card systems. In preparing the draft changes to the surcharging standard, Reserve Bank staff have consulted with staff from the Treasury and the Australian Competition and Consumer Commission (ACCC) regarding the Government’s plans to ban excessive surcharging and give enforcement powers to the ACCC. The Government has today announced draft legislation that will insert a ban on surcharging in excess of merchant costs into the Competition and Consumer Act (2010).

Changes to the Bank’s Surcharging Standard

Merchants incur costs when they accept a payment from a customer, and different payment methods can have very different payment costs; cards that provide significant rewards to consumers are typically significantly more expensive for merchants. When merchants have the right to surcharge on more expensive payment methods they are able to provide price signals to consumers and encourage the use of less expensive payment methods. By helping to hold down payment costs, the right to surcharge helps to hold down the price of goods and services charged to all consumers and reduces the extent of subsidisation between those who pay with cheaper payment methods and those who use more expensive methods.

It is important, however that merchants do not impose surcharges in excess of their actual payment costs. The Bank has had concerns about excessive surcharging in some sectors for some time. Accordingly, and consistent with the Government’s draft legislation, the Board is proposing to change the Bank’s surcharging standard with the aim of ensuring that customers cannot be surcharged any more than the cost of accepting cards. The proposed standard preserves the right of merchants to surcharge for more expensive payment methods but includes changes to enhance transparency and improve enforcement in cases where merchants are surcharging excessively.

The draft standard envisages the following framework for surcharging of card payments:

Card schemes will not be permitted to make rules that prevent merchants from recovering part or all of the costs of accepting card payments.

However, card acceptance costs will be defined more narrowly than in the Bank’s current guidance note, as the merchant service fee and other fees paid to the merchant’s bank (or other payment service provider).

Statements provided by banks to merchants will be required to contain easy-to-understand information on the average cost of acceptance for each payment method, which will constitute the maximum permissible surcharge if the merchant chooses to surcharge.

These statements will express acceptance costs in percentage terms, except where a merchant’s cost of acceptance for a particular payment method is fixed across all transaction values. This should ensure that merchants – including in the airline industry – who wish to surcharge will typically do so in percentage terms rather than as a fixed dollar amount.

Reserve Bank staff will continue to consult with the ACCC and will be working with banks, other payment service providers and the merchant community to develop templates for providing information on payment costs to merchants. The Bank expects that the more specific definition of the cost of acceptance and the transparency measures that are being proposed will result in enhanced enforcement of the surcharging framework in cases where merchants may be surcharging excessively.

Changes to the Bank’s Interchange Standards

Interchange fees are fees set by card schemes such as MasterCard, Visa and eftpos that require payments from the merchant’s bank to the cardholder’s bank on every transaction. While there may be a useful role for interchange fees when a card network is first established, the case for significant interchange fees in mature card systems is much less clear. Where merchants do not feel able to decline cards, the incentive is for schemes to raise interchange rates to induce banks to issue their cards and for banks to then use these fees to pay rewards to consumers to take and use the cards. Evidence from a range of countries suggests that competition between well-established payment card networks can lead to the perverse result of increasing the price of payment services to merchants (and higher retail prices for consumers).

Accordingly, in 2003 the Bank introduced benchmarks intended to prevent the significant upward pressure on interchange rates seen in many markets. Contrary to predictions by the international schemes at the time of the initial regulations, the Australian cards market has continued to grow very strongly since then and innovation has thrived. The Bank’s reforms have been supported by the leading Australian consumer and merchant organisations. Following the Bank’s reforms, a number of other jurisdictions have also regulated interchange fees.

The Bank’s Issues Paper drew attention to a number of issues related to interchange fees:

the decline in transparency for some end users of the card systems, which is partly because interchange fees have become increasingly complicated and the range of interchange fee categories has widened

the question of whether there is scope for average interchange fees to fall further, consistent with falls in overall resource costs in the card systems and as was contemplated in both the conclusions to the Bank’s 2007–08 Review of Card Payment System Reforms and the Final Report of the Financial System Inquiry

the possibility that the growth of companion card arrangements may indicate that the current regulatory system is not fully competitively neutral.

Following consultation on these issues with a wide range of stakeholders, the Board is proposing some changes to the Bank’s interchange standards that will improve competition and efficiency in the card payments market and in the broader payments system.

The Bank is proposing to modify the credit card interchange standard so that issuance of American Express companion cards will be subject to the same interchange fee regulation that applies to the MasterCard and Visa systems. In particular, interchange fees will be defined to also include fees paid by schemes to card-issuing banks as incentives to issue cards. In addition, both companion card issuance and traditional ‘four-party’ card issuance will be subject to rules on ‘other net payments’ to issuers, so as to prevent any circumvention of the interchange standards.

The Bank is not proposing to replace the current system of weighted-average interchange benchmarks with hard caps. The weighted-average benchmark for credit cards will remain at 0.50 per cent. However, the Bank is proposing to reduce the weighted-average benchmark for debit cards from 12 cents to 8 cents, consistent with the fall in average transaction values since the debit benchmark was introduced.

The weighted-average benchmarks will be supplemented by caps on any individual interchange fee within a scheme’s schedule. It is proposed that no credit card interchange fee will be able to exceed 0.80 per cent and no debit interchange fee will be able to exceed 15 cents if levied as a fixed amount or 0.20 per cent if levied as a percentage amount. These changes are expected to significantly reduce the extent to which small and medium-sized merchants are disadvantaged relative to a group of preferred merchants in the MasterCard and Visa interchange systems.

There are some other proposed changes to the system of benchmarks including a shift from three-yearly compliance to quarterly compliance. In addition, it is proposed that all transactions at Australian merchants will be included in calculations for observance of the benchmarks, with transactions on foreign-issued cards treated equivalently to transactions on domestic cards. Transactions on prepaid cards will be included with debit cards in the observance of the debit benchmark.

Next Steps

The Board seeks views on the draft surcharging and interchange standards as well as on other issues discussed in the Consultation Paper. The Consultation Paper also seeks industry views on appropriate implementation dates for any revised standards. Formal written submissions on these issues are requested by 3 February 2016.

Given the complexity of issues involving interchange fees and companion cards, it is unlikely that the Board will take any formal decision on changes to the interchange standards before its May 2016 meeting. In the case of surcharging, depending on consultation responses, it is possible that the Board may be in a position to make an earlier decision on changes to its standards.

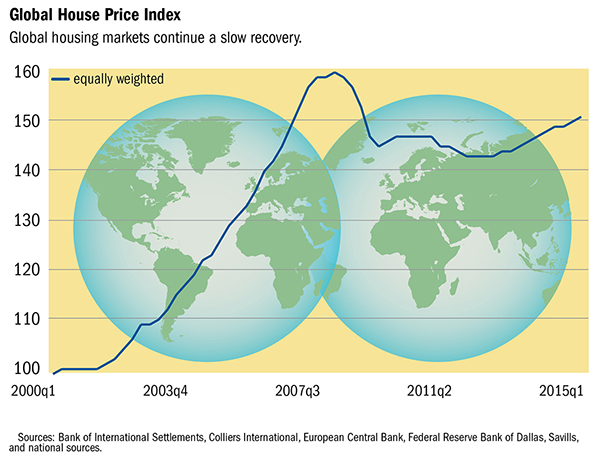

In the latest release, the IMF have provided data to October 2015, and also some specific analysis of the Australian housing market. We think they are overoptimistic about the local scene, and we explain why.

But first, according to the IMF, globally, house prices continue a slow recovery. The Global House Price Index, an equally weighted average of real house prices in nearly 60 countries, inched up slowly during the past two years but has not yet returned to pre-crisis levels.

As noted in previous quarterly reports, the overall index conceals divergent patterns: over the past year, house prices rose in two-thirds of the countries included in the index and fell in the other one-third.

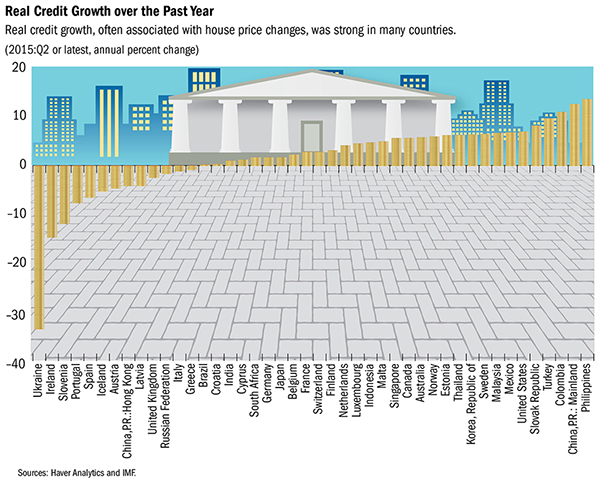

Credit growth has been strong in many countries. As noted in July’s quarterly report, house prices and credit growth have gone hand-in-hand over the past five years. However, credit growth is not the only predictor for the extent of house price growth; several other factors appear to be at play.

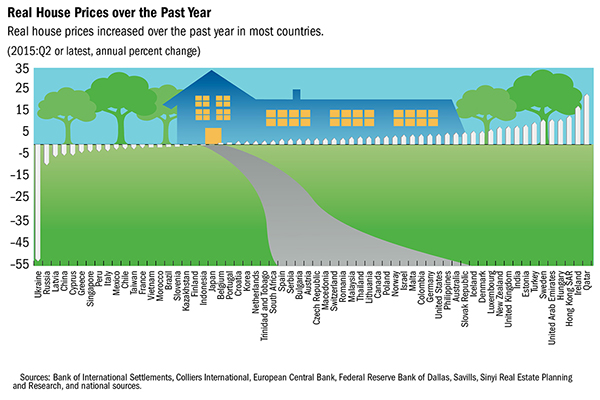

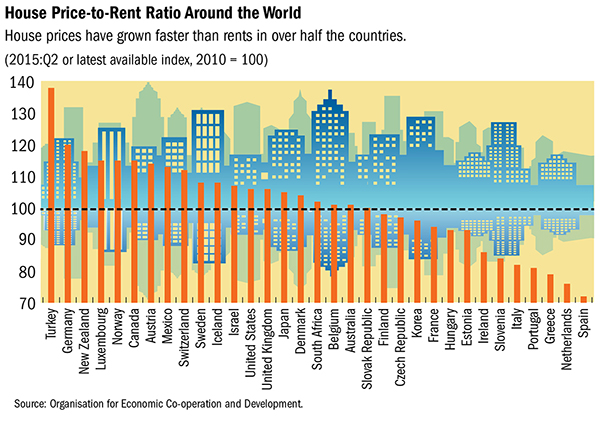

For OECD countries, house prices have grown faster than incomes and rents in almost half of the countries.

House price-to income and house price-to-rent ratios are highly correlated, as documented in the previous quarterly report.

Turning to the Australia specific analysis, Adil Mohommad, Dan Nyberg, and Alex Pitt (all at the IMF) argue that house prices are moderately stronger than consistent with current economic fundamentals, but less than a comparison to historical or international averages would suggest. Here is just a summary of their arguments, the full report is available.

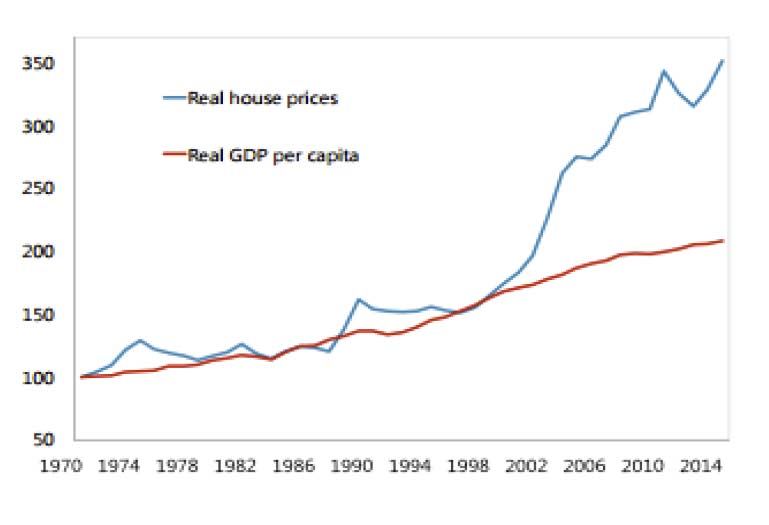

Argument: House prices have risen faster in Australia than in most other countries, suggesting, ceteris paribus, overvaluation.

Counter argument 1: House prices are in line on an absolute basis – Price-to-income ratios have risen in Australia and now near historic highs. However, international comparisons suggest that Australia is broadly in line with comparator countries, although significant data comparability issues make inference difficult.

Counter argument 2: The equilibrium level of house prices has also risen sharply – Lower nominal and real interest rates and financial liberalization are key contributors to the strong increases in house prices over the past two decades. The various house price modeling approaches indicate that house prices are moderately stronger (in the range of 4-19 percent) than economic fundamentals would suggest.

Counter argument 3: High prices reflect low supply – Housing supply does indeed seem to have grown significantly slower than demand, reducing (but not eliminating) concerns about overvaluation.

Counter argument 4: It is just a Sydney problem, not a national one – The two most populous cities, Sydney and Melbourne, have seen strong house price increases, including in the investor segment. A sharp downturn in the housing market in these cities could be expected to have real sector spillovers, pointing to the need for targeted measures—including investor lending—to reduce risks from a housing downturn.

Counter argument 5: There are no signs of weakening lending standards or speculation – While lending standards overall seem not to have loosened, the growing share of investor and interest-only loans in the highly-buoyant Sydney market, is a pocket of concern.

Counter argument 6: Even if they are overvalued, it doesn’t matter as banks can withstand a big fall – While bank capital levels are likely sufficient to keep them solvent in the event of a major fall in house prices, they are not enough to prevent banks making an already extremely difficult macroeconomic situation worse.

Second, we agree, in the main centres, house prices are about 20% over fundamentals, and in some pockets up to 30%, so yes this is a problem, especially at a time of flat income growth.

Third, supply has been increasing, but this has stoked investment housing speculation, and is not equally strong in all areas and price brackets. We still have a massive under-supply of affordable housing, just ask prospective first time buyers – and many are having to reach for the skies just to buy something, so we thing prices are still hiked because of supply problems.

Fifth, underwriting standards had declined, refer to recent APRA. ASIC and RBA comments. Guidelines on assessment of income, and baseline interest rate assumptions have been tightened. Speculation is also rife, especially in the investment sector (refer our surveys).

Thus, DFA concludes the IMF initial statement is correct, and despite their detailed analysis, their counterarguments are not convincing. We do have a problem.

Launched today, the Financial Services Disruption Index, which has been jointly developed by Moula, the lender to the small business sector; and research and consulting firm Digital Finance Analytics (DFA) shows that Financial Services are undergoing disruptive change, thanks to customers moving to digital channels, the emergence of new business models, and changing competitive landscapes. Combing data from both organisations, we are able to track the waves of disruption, initially in the small business lending sector, and more widely across financial services later.

The index tracks a number of dimensions. From the DFA Small business surveys (26,000 each year), we measure SME service expectations for unsecured lending, their awareness of non-traditional funding options, their use of smart devices, their willingness to share electronic data in return for credit, and overall business confidence of those who are borrowing relative to those who are not.

Moula data includes SME conversion data, the type of data SMEs share, the average loan amount approved, application credit enquiries, and speed of application processing.

The index stood at 33.02 from May to July 2015, and rose to 33.94 in the August to October period. The higher the score, the greater the disruption. Of note SMEs are becoming more aware of non-traditional unsecured lending options, are becoming more demanding in terms of application processing times, are more willing to share data and are more likely to apply using a smart device. In addition, the loan values being written are rising, more businesses are willing to share richer data, and the confidence levels among borrowing SMEs is on the rise.

Overall, unsecured lending to the SME sector is being disrupted significantly, and we expect the index will continue to trend higher, as awareness of alternatives to traditional banking continues to rise, and more firms apply for credit.

The average expectation duration was down from 9.2 days in Q3 2015 to 7.5 days this quarter. SMEs continue to expect better service standards when applying for credit. Whilst they accept it may take a few days for an application to be processed, the survey data shows that many think a week should be enough to complete an unsecured loan and get money into their account, and they expect to receive regular progress reports and updates on the way through.

We see a rise in awareness among SMEs of the availability of alternative credit solutions and greater familiarly with the tag “Fintech”. This month 3.75% of businesses recognised the concept, up from 2.74% last month, and momentum is increasing.

More business owners are using smart devices to run their business. They expect access to a wider range of services this way, and more immediate responses. Last quarter 42.6% of businesses used a smart device, this time it was 44.6%, and the rate of adoption is increasing.

According to the Galaxy research commissioned by MasterCard, Australians of all ages continue to embrace contactless payments, with 66% preferring to use tap and go for small transactions under a $100 instead of entering their PIN, and 64% favoring it as a payment method over cash. The study was conducted online during October 2015 using a sample of 1,005 Australians aged between 18-64 years old, who have a credit or debit card.

Results from the survey showed that speed and convenience continue to generate increased adoption of the technology by Aussies (77%), and safety benefits available through contactless cards are also contributing to its growing popularity over cash; the majority of Australians (82%) believe they are more likely to be reimbursed for unauthorised contactless payments made with a stolen credit or debit card than they are likely to get stolen cash back.

First introduced into Australia in 2007, contactless payments have been one of the fastest-adopted payment technologies globally, and despite recent reports, MasterCard data in addition to industry data, reveals no increase in fraud specifically relating to contactless payments. Australian Card Data* has found that fraud relating to contactless payments makes up less than 2% of all total card fraud. This is despite huge growth in the category, where contactless MasterCard transactions have grown 148% based on card data compiled by MasterCard and Visa showing that number of Contactless MasterCard transactions grew 148% between July 2013 and 2014.

MasterCard SVP and Country Manager, Andrew Cartwright said “This research indicates not only a shift in the preferred methods in which consumers like to pay, but also suggests that they are beginning to understand and trust the safety benefits associated with paying by card. As contactless payments continue to rise, cash is increasingly become unnecessary real estate in wallets.

“I’ll take a card any day of the week – it is safer than cash. With a card I’m protected against unauthorised purchases, whereas, if my wallet is stolen, the cash is as good as gone”, said Cartwright.

Shoppers in West Australia have the highest preference for contactless payments in the country (72%), followed by shoppers in NSW (67%), VIC and TAS (66%).

In the month of October 2015 detached house sales declined in four out of the five the mainland states. Detached house sales fell by 9.3 per cent in Victoria, 5.4 per cent in Western Australia, 0.9 per cent in Queensland and 0.8 per cent in New South Wales. Detached house sales increased by 2.6 per cent in South Australia.

In the month of October 2015 detached house sales declined in four out of the five the mainland states. Detached house sales fell by 9.3 per cent in Victoria, 5.4 per cent in Western Australia, 0.9 per cent in Queensland and 0.8 per cent in New South Wales. Detached house sales increased by 2.6 per cent in South Australia. As noted in previous quarterly reports, the overall index conceals divergent patterns: over the past year, house prices rose in two-thirds of the countries included in the index and fell in the other one-third.

As noted in previous quarterly reports, the overall index conceals divergent patterns: over the past year, house prices rose in two-thirds of the countries included in the index and fell in the other one-third. Credit growth has been strong in many countries. As noted in July’s quarterly report, house prices and credit growth have gone hand-in-hand over the past five years. However, credit growth is not the only predictor for the extent of house price growth; several other factors appear to be at play.

Credit growth has been strong in many countries. As noted in July’s quarterly report, house prices and credit growth have gone hand-in-hand over the past five years. However, credit growth is not the only predictor for the extent of house price growth; several other factors appear to be at play. For OECD countries, house prices have grown faster than incomes and rents in almost half of the countries.

For OECD countries, house prices have grown faster than incomes and rents in almost half of the countries. House price-to income and house price-to-rent ratios are highly correlated, as documented in the previous quarterly report.

House price-to income and house price-to-rent ratios are highly correlated, as documented in the previous quarterly report. Counter argument 1: House prices are in line on an absolute basis – Price-to-income ratios have risen in Australia and now near historic highs. However, international comparisons suggest that Australia is broadly in line with comparator countries, although significant data comparability issues make inference difficult.

Counter argument 1: House prices are in line on an absolute basis – Price-to-income ratios have risen in Australia and now near historic highs. However, international comparisons suggest that Australia is broadly in line with comparator countries, although significant data comparability issues make inference difficult.