The New York Fed has, for the last two years, been part of an international dialogue on the reform of culture in the financial services industry. Why culture? Let’s begin with the following hypothesis: environment drives conduct. What each of us learned from our parents governs some of our behavior, but not nearly as much as any of us who are parents would like to believe. Place ordinary people in a bad environment, and bad things tend to happen. That said, place someone in a good environment, and good things tend to happen. This is just part of being human. We observe and adapt.

Before continuing, I would like to clarify that the views I express today are my own and may not reflect the views of the Federal Reserve Bank of New York or the Federal Reserve System.

Part of any organization’s environment is its culture. Some have labored over a precise definition of the word “culture.” Bill Dudley, the President of the New York Fed, has offered the following description, which works for me: “Culture relates to the implicit norms that guide behavior in the absence of regulations or compliance rules – and sometimes despite those explicit restraints. Culture exists within every firm whether it is recognized or ignored, whether it is nurtured or neglected, and whether it is embraced or disavowed.”1

The New York Fed’s interest in reforming culture is a product of events since the Financial Crisis. Take, for example, the manipulation of LIBOR and foreign exchange rates, much of which was collusive. Each of those episodes involved misconduct affecting wholesale markets on which the real economy relies. Both cases shared an underlying, flawed outlook. Bankers failed to see beyond their immediate financial goals. They ignored the broader social consequences of their decisions on the firm and its customers, as well as on consumers, producers, savers and investors. The same flawed outlook may have contributed to the Financial Crisis.

There are many more examples. One bank was fined for doing business with Sudan despite economic sanctions imposed for engaging in genocide. Another bank manipulated electricity markets in California and Michigan. Other banks helped U.S. citizens evade taxes. I will not review the full litany. Notably, none of these recent episodes had anything to do with capital levels or liquidity ratios. The many post-Crisis reforms to bank balance sheets – including the Dodd-Frank Act and new standards developed by the Basel Committee on Bank Supervision and the Financial Stability Board-provided necessary bulwarks against systemic risks. Capital and liquidity requirements, and the enhanced testing surrounding them, have made banks and the financial system more resilient to stress. But those new laws, regulations, and standards have done little to curb banker misconduct. Each post-Crisis episode demonstrates a narrow cultural focus on short-term gain and disregard of broader social consequences.

Last year the New York Fed challenged the industry to consider many factors that have contributed to recent, widespread misconduct. There are no simple answers and that discussion is continuing. This year, by contrast, our focus has been more on solutions-what’s working, and what is not. In both years, we have offered three messages to the industry.

First, cultural problems are the industry’s responsibility to solve. The official sector can monitor progress and deliver feedback and recommendations. In fact, many individual supervisory findings are often symptoms of deeper cultural issues at a firm. But the banks themselves must actively reform and manage their cultures.

Second, a bank’s implicit norms-especially those reinforced through incentives-must align with the public purpose of banking. Gerald Corrigan, more than three decades ago, presented a theory of banking based on the principle of reciprocity. Banks receive operating benefits unavailable to other industries because they provide important services to the public. For example, financial intermediation is enhanced through deposit insurance and access to the discount window. Public benefits, though, are not a gift. They are part of a quid pro quo. In exchange for receiving valuable operating benefits, a bank’s implicit codes of conduct-that is, its culture-must reflect the public dimension of the services that banks provide.

Third, the reform of bank culture should aim to restore trust. The bedrock of the financial system is trust and the word credit derives from the Latin notion of believing or trusting. We saw seven years ago that the public’s trust is critical in a crisis. The repair of the financial system would not have been possible without public support. If another crisis were to happen tomorrow, would there be that support?

A lack of trust-or, more accurately, low trustworthiness-also imposes day-to-day costs.8 For starters, there are fines. Then there are the legal costs in investigating allegations and defending lawsuits. Internal monitoring also becomes more expensive as rules become more extensive. Some might say that the proliferation of rules since the Financial Crisis is inversely proportional to a decline in the industry’s perceived trustworthiness. The choice between rules and standards depends on the trustworthiness of the regulated. A more flexible, standards-based legal regime requires a degree of trustworthiness that, in recent years, banks have not demonstrated.

Those are the measurable costs of low trustworthiness. There may be other, longer-term costs that are more difficult to price. Let me raise just two. If employees perceive a firm as untrustworthy or disloyal, will they choose to work in that firm? And, if they do, how will they behave toward the firm and its stakeholders?

I am encouraged that the industry seems to understand the importance of reforming its culture. Consider for a moment the following data points. In September 2013, shareholders of a major U.S. bank requested that the bank prepare “a full report on what the bank has done to end [its] unethical activities, to rebuild [its] credibility and provide new strong, effective checks and balances within the [b]ank.” That request was forwarded, by the way, by a Catholic nun. The bank responded through its attorneys that the nun’s proposal was “materially false and misleading” and “impermissibly vague and indefinite.” Fast forward to May 2015. The Federal Advisory Council-a panel of bankers that advises the Federal Reserve System-reported that “Regulators and the banking industry have worked extensively to restore financial stability through a series of mechanisms and rules that establish appropriate levels of capital, liquidity, and leverage. . . . As often as not, however, the challenges faced in recent years have been behavioral and cultural; post-crisis episodes such as LIBOR and foreign exchange manipulation provide hard evidence that there remains work to be done.” This is clearly an encouraging difference in perspectives.

The public sector, too, has paid increasing attention to culture. The Group of Thirty, the Basel Committee, the European Systemic Risk Board, and the Financial Stability Board have issued papers on culture, governance, and misconduct risk. The Fair and Effective Markets Review-a joint project of the Bank of England, the Financial Conduct Authority, and Her Majesty’s Treasury-has called for heightened standards for market practice in matters affecting the public good. And in the last year, we have seen emerging approaches to supervision that aim to address culture, conduct, and governance. In particular, the central bank of the Netherlands-De Nederlandsche Bank-has pioneered new techniques for the supervision of corporate governance, especially for assessing the group dynamics of boards and senior management.

Culture also features prominently in criminal enforcement. The U.S. Department of Justice requires its prosecutors to determine “the pervasiveness of wrongdoing” at a corporation before seeking an indictment. According to its prosecutors’ manual, “[T]he most important [factor in making this determination] is the role and conduct of management. Although acts of even low-level employees may result in criminal liability, a corporation is directed by its management and management is responsible for a corporate culture in which criminal conduct is either discouraged or tacitly encouraged.” Individuals, including senior managers, also face criminal liability for their conduct. Recent guidance from the U.S. Department of Justice places greater emphasis on individual culpability. And the recent convictions of two traders for rigging LIBOR, one of whom served as the Global Head of Liquidity and Finance at a major bank, may send a powerful message to bankers about the consequences of their misconduct.

The new acceptance of culture as an important area of focus was evident at a workshop that the Federal Reserve Bank of New York hosted on November 5. Christine Lagarde, Managing Director of the International Monetary Fund, and Stanley Fischer, Vice Chairman of the Board of Governors of the Federal Reserve System, headlined a contingent of over 20 public sector authorities from around the globe. They were joined by the CEOs, senior executives, and board members of global financial institutions. Together, they discussed methods of reforming culture and the continuing challenges in this effort. In my view, the workshop offered a number of useful insights, chiefly:

-

Culture is a soft concept that is hard to measure, and perhaps harder to manage and sustain. But it is as important as capital and liquidity, and should receive continuous and persistent attention.

-

A bank’s culture must be consistent with public expectations and promote behavior that considers the firm’s many stakeholders, including the public. Also, a positive, constructive culture can be an important pillar aligned with the execution of a firm’s business strategy.

-

Culture cannot be set by fiat. Leadership is indispensable, and requires more than a “tone from the top.” Managers of all levels must take action to promote a greater sense of personal responsibility and stewardship among employees. The next generation of financial leaders will reflect the expectations of leaders today.

-

Despite firm-wide statements about values and codes of conduct, banks may have several dissonant sub-cultures. “Silos” or “tribes” as they are sometimes called, appear in most if not all of the episodes I described earlier. By sharing best practices across the industry, firms might identify common warning signs of problems within sub-cultures and behaviors that are incompatible with the firm’s values.

-

Diversity of thought and background are valuable cultural assets because they generate better questions and decisions, contributing to effective challenge. A diversity of views, though, must be complemented by a sense of common purpose. Certain basic principles-fair treatment of customers and employees, for example-cannot be open to debate.

The Federal Reserve Bank of New York recently launched a webpage that collects resources on bank culture. We’ve included the papers by the Group of Thirty and other organizations that I have mentioned, and summaries of our two workshops on culture. I hope you’ll take a look.

To conclude, the Financial Crisis and subsequent scandals revealed deep and continuing flaws in the culture of banking. The responsibility to address these flaws rests with the banks themselves. Many industry leaders have initiated reform programs within their firms. It is important to keep the momentum going. Reform requires relentless and sustained effort: from the top of an institution to its most junior employees, and across all of the institution’s business activities. Reform must include the full scope of an employee’s career, beginning with recruiting and continuing with annual performance management, compensation and promotion decisions. We in the official sector will be looking to the industry to fulfill its end of the bargain-to act consistent with the public well-being, to value long-term stability over short-term gain, and to take account of all stakeholders in making decisions.

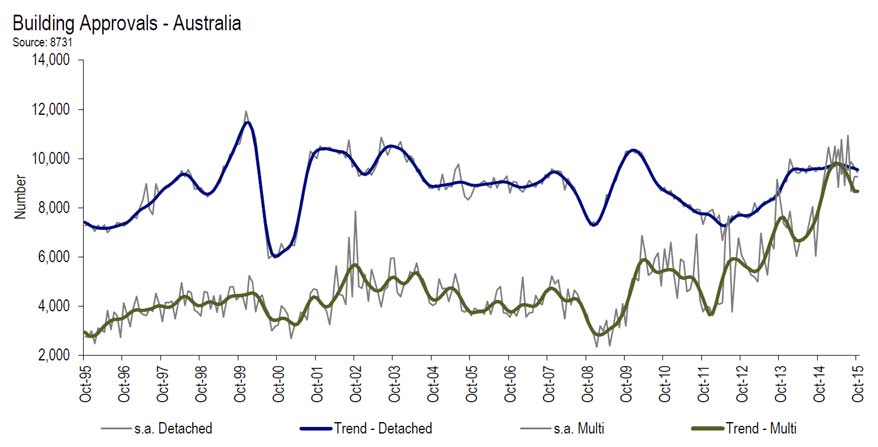

During October 2015, total seasonally adjusted new home building approvals saw the largest increase in South Australia (+23.4 per cent), followed by New South Wales (+22.0 per cent) and Victoria (+21.2 per cent). Approvals fell in Tasmania (-41.6 per cent), Queensland (-28.7 per cent) and Western Australia (-1.1 per cent). In trend terms, approvals saw a 7.1 per cent increase in the NT but declined by 10.8 percent in the Australian Capital Territory.

During October 2015, total seasonally adjusted new home building approvals saw the largest increase in South Australia (+23.4 per cent), followed by New South Wales (+22.0 per cent) and Victoria (+21.2 per cent). Approvals fell in Tasmania (-41.6 per cent), Queensland (-28.7 per cent) and Western Australia (-1.1 per cent). In trend terms, approvals saw a 7.1 per cent increase in the NT but declined by 10.8 percent in the Australian Capital Territory.