According to CoreLogic RP Data, the preliminary auction clearance rate nudged higher over the first week of winter, however the number of auctions dipped compared with the previous week. There were 1,953 auctions held over the week, down from 2,480 last week, however higher than one year ago when 1,201 auctions were held and auction volumes were low due to the Queen’s birthday public holiday in all cities with the exclusion of Perth. Preliminary results show that 70.4 per cent of capital city auctions held this week were successful, rising from a final result of 67.7 per cent last week. One year ago, across the lower number of auctions, 78.5 per cent sold. Melbourne and Sydney, the two largest auction markets have maintained strength this week, while across the remaining, significantly smaller auction markets, results have been more varied.

The mix of monetary and fiscal policies in an economy has important implications for debt levels and financial stability over the medium term, Bank of Canada Governor Stephen S. Poloz said.

In the Doug Purvis Memorial Lecture given at the Canadian Economics Association’s annual conference, Governor Poloz used the Bank’s main policy model to construct three “counterfactual” scenarios of events from the past 30 years that show how different policy mixes can influence the amount of debt taken on by the private and public sectors.

Tight monetary policy with easy fiscal policy may lead to the same growth and inflation results as easy monetary policy paired with tight fiscal policy in a given situation, the Governor explained. However, the consequences for government and private sector debt levels would be quite different.

Recent experience in Canada and elsewhere shows that debt levels—whether public or private—can provoke financial stability concerns, said Governor Poloz. The insight about policy mix is important as authorities worldwide work to incorporate financial stability issues into the conduct of monetary policy, he added.

The Governor stressed that the counterfactuals are intended to illustrate the impact of the policy mix on debt levels; they aren’t meant to be taken as an opinion about what the best policy mix was in the past or is now.

“Hindsight is always 20:20 and such a discussion would have little meaning,” Governor Poloz said. “The best mix of monetary and fiscal policy will depend on the economic situation.”

There should be a degree of coordination between the monetary and fiscal authorities that allows both to be adequately informed of each other’s policies and consider their implications on debt levels over the medium term, the Governor said. In Canada’s case, the central bank operates under an explicit inflation-targeting agreement with the federal government that enshrines its operational independence, while allowing for both parties to share information and judgment, Poloz said. This framework represents “a simple yet elegant form” of policy coordination, he noted.

The lecture honours Doug Purvis, a Canadian macroeconomist and Queen’s University professor. In 1985, Purvis delivered the Harold Innis Lecture, in which he argued that rising government debt levels would eventually compromise the ability of authorities to implement stabilization policies. Governor Poloz said his lecture today is meant to build on Purvis’ initial insights by bringing more advanced macroeconomic models to bear on the topic, and linking them to the topical issue of financial stability.

A number of politicians have struggled this week to explain the Turnbull Government’s proposed changes to superannuation. Given the complexity of the area, that’s not surprising. And this complexity explains why intergenerational “theft” through superannuation has continued for so long.

Transition to retirement (TTR) provisions, introduced by the Howard Government in 2005, were supposed to encourage people to keep working part-time rather than stopping work entirely. Yet most people using a TTR pension have continued to work full time. In practice the provisions have simply been a gift enabling older people to pay less tax than younger people on similar incomes.

No-one has ever explained why we should have an age-based tax system, beyond the politically cynical observation that these provisions were introduced when demographics produced an unusually large number of voters aged 55 to 64. Some of these voters are now objecting vociferously to losing their privileges – but they were never justified in the first place.

The tax breaks of TTR pensions

Transition-to-retirement (TTR) pensions, as they stand today, have three features. They allow people to withdraw money from superannuation from the age of 60 without tax penalties. They allow older people to continue to contribute to superannuation while they withdraw funds. And they bring forward the age at which earnings on accumulated superannuation balances cease to be taxed (the superannuation earnings of younger people are taxed at 15%).

These provisions are a boon to older taxpayers. One benefit is the opportunity for “super recycling”, in which a person continues to work full-time and to consume their wage income, but pays around $5000 a year less income tax. People over 60 can put the maximum amount into superannuation from their pre-tax income, and then withdraw the money immediately. They pay much less income tax because their contributions to super are only taxed at 15%, whereas ordinary earnings are taxed at their marginal tax rate.

The precise benefit of super recycling varies depending on income, as our recent Super Tax Targeting report shows. For workers aged between 60 and 64 who earn between $65,000 and $150,000, super recycling reduces the amount of tax paid by about $5000 a year. To put this in context, a 60-year old earning $75,000 then pays as much income tax as a 40-year old earning $57,000.

There are also big benefits for an older worker who takes a TTR pension and stops paying tax on the earnings of their superannuation well before they retire. Take someone with a superannuation balance of $500,000 – a larger balance than seven in eight Australian taxpayers of that age – and earning a 6% return. A TTR pension reduces the annual tax paid by around $4,500. If they take a TTR pension at age 56, they will save around $40,000 in tax by the time they stop working at 65. If their superannuation balance is higher, the tax benefit is proportionately larger.

Not a transition to retirement scheme at all

All the evidence suggests the TTR pensions are mainly used by high-wealth individuals to reduce their tax bills while they continue to work full-time. In a study published last year the Productivity Commission concluded that:

…the tax concessions embodied in transition to retirement pensions — designed to ease workers to part-time work prior to retirement — appear to be used almost exclusively by people working full-time and as a means to reduce tax liabilities among wealthier Australians.

The misuse of TTR pensions is reflected in the confusion about how many people will be affected by the Government’s changes. The Government estimates that some 115,000 people will be affected by the change.

Critics counter that the changes could affect more than 500,000 super accounts classified as TTR pensions. But many of these almost certainly belong to people who have in fact fully retired, but haven’t bothered to tell their super fund to change the classification of their pension. They have little incentive to get their paperwork up to date, because the TTR pension already provides all the benefits of tax-free super earnings to which retirees are entitled.

However many people are affected, these arrangements bear little resemblance to the now explicit objective for superannuation – “to provide income in retirement to substitute or supplement the Age Pension”. They don’t encourage additional saving. They do little in practice to delay retirement. Instead they are part of an age-based tax system that allows older Australians to pay less income tax than younger Australians with similar incomes.

Reducing the rorts

So the Government’s announcement in the May Budget that it would reduce the extent of these benefits should be no surprise.

The Government proposed to reduce the amount that can be contributed to super from pre-tax income from $35,000 to $25,000. As a result, a 60-year old earning a wage of $75,000 a year would only save $3,700 per year through super recycling rather than $5,800 per year.

However, there may be little change in practice because the Government also proposed yet another complexity that future politicians will also struggle to explain. People will be able to make additional pre-tax contributions if they contributed less than the limit of $25,000 in the previous five years. Although this is supposed to help women with broken work histories catch up on building their super funds, past practice shows that such provisions are primarily used by older men to minimise their tax.

The government also proposed to tax super earnings at 15% unless a person retires (and so forfeits the ability to make additional contributions to superannuation). Those withdrawing money from their superannuation, but also working and contributing to superannuation, will then pay 15% tax on the earnings of their super fund, just like everyone else still working.

Why the Government should stick to its guns

The Government has been attacked over the last week as it emerges that these changes will affect some people “only” earning $80,000 a year, who might be in the top 20% of income earners, but are not in the top 4%. Coalition backbenchers are reportedly concerned that some of their supporters will pay more tax. Financial planners are nervous that they will have less tax planning to offer.

But the outrage misses the vital question: why do such generous tax breaks exist at all? They lead to individuals with above average incomes paying less tax than younger Australians on similar incomes. They do almost nothing to contribute to the ostensible purpose of superannuation.

For more than a decade, superannuation tax concessions have been absurdly generous to older people on high incomes. They are one of the major reasons why older households pay less income tax in real terms today than they did 20 years ago, even though their workforce participation rates and real wages have jumped.

Superannuation tax breaks cost more than $25 billion in foregone revenue, or well over 10% of income tax collections, and the cost is growing fast. Lower-income earners and younger people have to pay more in other taxes – now and in the future – to pay for the tax-lite status of so many older Australians. The proposed changes are just the beginning of much needed reforms to superannuation to end intergenerational theft from the young.

Authors: Brendan Coates, Fellow, Grattan Institute; John Daley, Chief Executive Officer, Grattan Institute

Young Australians are getting serious about saving and plan to increase their levels of investment in the coming months, the latest MLC Wealth Sentiment Survey shows.

The quarterly survey of over 2,000 Australians found that 42 per cent of 18 – 29 year olds added to their savings in the last three months, compared to 29 per cent of people aged 30-49, and 21 per cent of the over 50’s. Younger investors are also more likely than any other age group to invest more in the next quarter.

While young investors are demonstrating optimism, older people are taking a more conservative approach – with debt consolidation and superannuation the main priorities. On balance, Australians added more to their superannuation (+2 per cent) and paid down more of their debts (+6 per cent) in the last quarter.

The survey found that the retirement savings gap is still a looming concern for many Australians, who now expect to retire with just over $450,000 on average – down from $501,000 last quarter. Men, on average, expect to retire with $192,000 more than women.

MLC General Manager Corporate Super Lara Bourguignon believes the focus on building super and reducing debt is a positive sign.

”We can see that Australians are taking action to contribute more to their super to address their concerns about how much money they will retire with.

”While we are moving in the right direction, it’s also important for people to consider long-term investment options to help maximise their retirement savings.

”Our research found that over 40 per cent of Australians have never used a financial planner and don’t have a financial plan, so there is more work to be done to ensure that Australians are adequately prepared for their later years,” said Bourguignon.

The survey includes results from MLC’s Investment Intentions Index, which measures whether Australians are planning to invest more or less in the next three months.

While overall investment intentions improved this quarter, rising three points to -5 points, the number of investors who are planning to cut back the amount they invest still outweighs those planning to invest more.

Additional findings include:

In the past three months, one in four Australians have added to their savings and deposits, whilst one in five have elected to pay off debt.

Almost one in three women believe they’ll have ”far from enough” to retire on, compared to one in five men.

Fifty-six per cent of women don’t think they will have enough to retire on and live to their desired standard, compared to 46 per cent of men.

One in five of us expect to have less than $100,000 in savings when we retire – which may explain why almost one in five of us also plan to keep working into our 70’s.

One in five young Australians expect to retire before 60, compared to less than one in ten of those over the age of 50.

Significantly more men (43 per cent) believe they are holding more super than their partners. Just 14 per cent of women believe they hold more super than their partners.

Around one in five ”don’t know” how much they’ll have in retirement

The latest World Economic Outlook includes country specific observations. Of note is their view of the Australian housing market. “Domestically, the unwinding of housing-market tensions to date may presage dramatic and destabilising developments, rather than herald a soft landing”.

We think the risks are centred on the high-rise apartment sectors, especially in the east coast urban centres. In our worst case scenario, prices may fall up to 38%, in Melbourne but not immediately.

They also echo the latest GDP scenario, as reported, GDP was up thanks to LNG exports, but of course household income growth continues to languish.

Output growth will gradually strengthen towards 3% in 2017. Adjustment to declining resource-sector investment will continue. Growth in the non-resource sector will pick up, aided by dollar depreciation and a steady increase in household consumption. Further falls in the rate of unemployment are not expected to generate strong inflationary pressures and will help reduce inequality.

With receding risks from the housing boom, there is leeway for further monetary policy easing in the event of a new downturn. Close vigilance on housing-market developments is still required. Fiscal consolidation should be back-loaded in light of economic uncertainties. Tax reform should be a core element of structural policy.

Boosting productivity in Australia requires a focus on innovation. Targeted R&D policy, university-business linkages and effectiveness and efficiency of financial support for research are important. Ensuring strong competition, regulation that accommodates new internet-platform-based businesses, sound ICT infrastructure and continuing education reform are also key for productivity performance. In addition, education reform will boost inclusiveness through stronger low-end skills and better ICT infrastructure can reduce gaps in economic opportunity by improving access in rural areas.

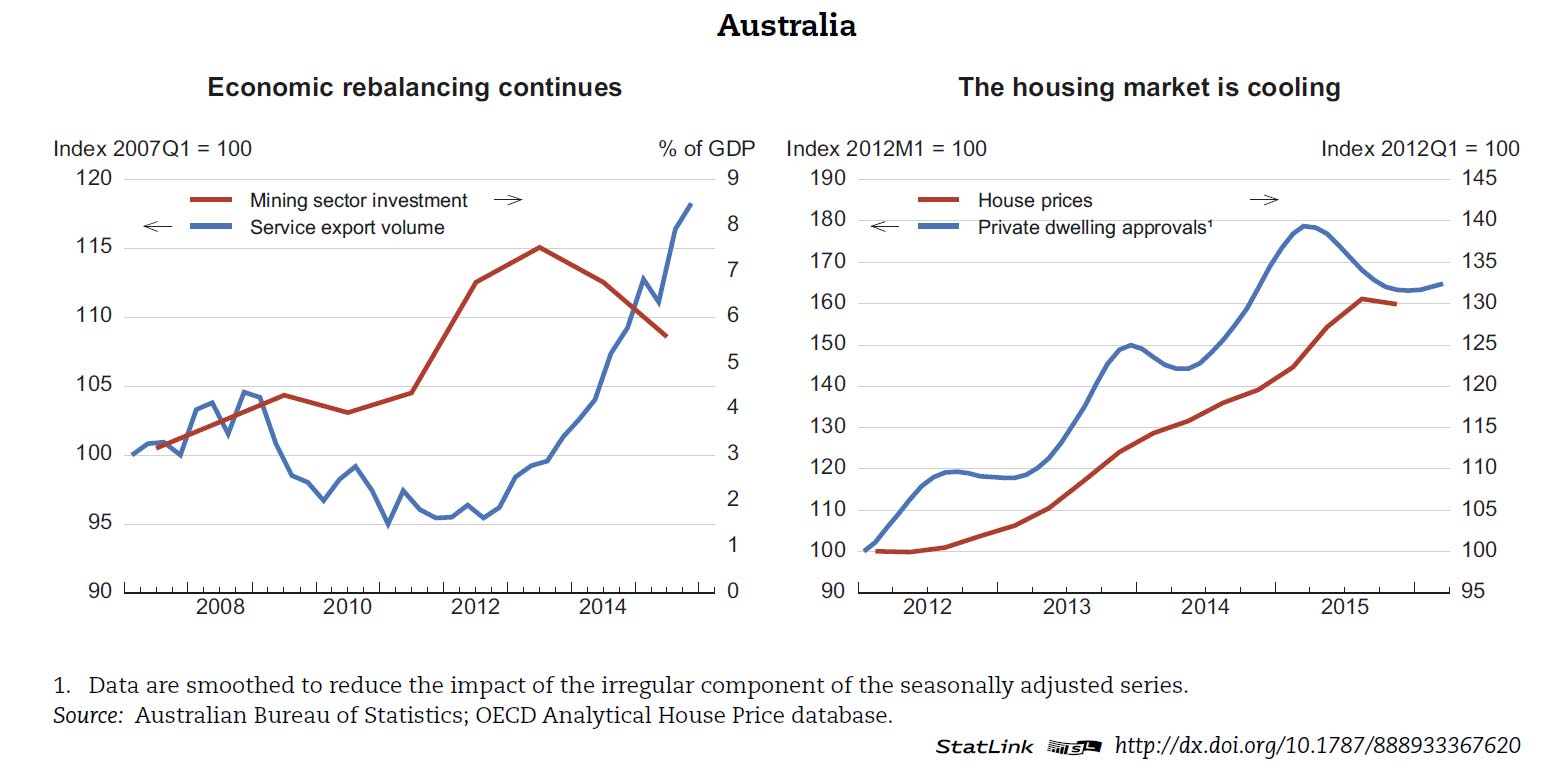

Rebalancing away from resource sectors continues

Resource-sector investment and employment face ongoing decline and commodity prices remain low, although new liquefied-natural-gas (LNG) production is boosting exports. Non-resource activity continues to pick up, especially in services exports, in part reflecting past depreciation of the currency. Non-resource activity is now driving employment growth. In addition, house-price and mortgage-credit growth are slowing, assisted by macro-prudential tightening. Consumer price inflation remains low. Also, uncertainty about global economic prospects is impacting Australia’s stock market and business sentiment.

Continued policy support for economic adjustment and productivity growth is required

The Reserve Bank reduced the policy rate by 25 basis points in May to 1.75%, the first rate change in 12 months, prompting a depreciation of the exchange rate. The projection envisages no further easing and assumes that policy-rate increases begin in 2017. Nevertheless, room for further rate cuts remains in the event of below-par growth. Fiscal policy needs to let the automatic stabilisers operate while keeping a medium-term objective of reducing the public-debt burden.

In structural policy, the OECD has long emphasised the scope for improving Australia’s tax system, in particular through greater use of efficient tax bases, such as the Goods and Services Tax and land tax, and reforms in specific areas, such as the taxation of pensions (“superannuation”). Reform to the latter could lower inequality by narrowing differences across households and between women and men among older cohorts. Strengthening of consumer-protection regulation in banking would also benefit households. Australia’s greenhouse-gas reduction policy relies principally on the Emission Reduction Fund, which provides financial incentives for businesses to reduce emissions and as of July 2016 it will backed by a safeguard mechanism that discourages offsetting emissions.

Boosting productivity requires strengthening capacities for generating and absorbing innovation. Research collaboration between the university and business sectors remains a point of weakness. Also, ensuring value-for-money in financial incentives, such as R&D tax breaks, remains a challenge. Policy responses to “disruptive” internet-platform innovations have generally been positive. Australian product and labour market regulation is broadly conducive to resource re-allocation, thus helping innovation via “creative destruction”. However, ICT infrastructure and services require ongoing policy attention and there is scope for greater innovation in public services.

The pick-up in growth will be gradual, but risks and uncertainties remain sizeable

Output growth is projected to be just under 3% in 2017. Negative effects from shrinking mining investment are set to ease and new LNG production will boost exports. Exchange rate depreciation and supportive macroeconomic policy have helped rebalance activity towards non-mining sectors. Employment growth will drive a further decline in the rate of unemployment. Household consumption is expected to remain solid, helped by further erosion of the household savings ratio.The pick-up in activity will not generate significant inflationary pressure, due to remaining economic slack.

Australia’s exposure to commodity-market developments, particularly those linked to the Chinese economy remains an important source of uncertainty and risk. Domestically, the unwinding of housing-market tensions to date may presage dramatic and destabilising developments, rather than herald a soft landing. Uncertainties on future economic policy ahead of the Federal election, which is scheduled for 2nd July, are also adding a degree of risk.

National Australia Bank has entered the online SME lending market with the launch of the NAB QuickBiz Loan, which that allows customers to borrow up to $50,000 in unsecured funding via a new online application process.

Developed by NAB’s in-house innovation hub, NAB Labs, the online platform uses financial technology to assist with the loan application process and states that customers will have money in their account within three days of NAB receiving their signed loan document.

The QuickBiz Loan carries a fixed interest rate of 13.85% for terms of either one or two years. The loan is repaid by monthly principal and interest payments and there are no application or ongoing fees.

According to Angela Mentis, NAB group executive for business banking, “in the early days of business ownership, small businesses often only require small amounts of funding – and many owners don’t have a property or other significant assets to secure a loan against. We’re responding to these customer needs, placing more emphasis on the strength of the business rather than traditional physical bricks and mortar security.”

Jonathan Davey, executive general manager of NAB Labs added the NAB QuickBiz Loan is “another example of the bank’s agile approach to meet customer needs”.

Meanwhile, Canstar’s research manager Mitchell Watson says “from NAB’s point of view this is a move to help stem any loss of low-risk customers to smaller, more agile competitors.”

According to Watson, “the advertised 13.85 percent does seem to be a fair interest rate”, given it is lower than the 16% being charged by the Commonwealth Bank’s Simple Business Overdraft. However, it should be noted that an overdraft is a more flexible and expensive loan product than a principal and interest loan.

What this means for your business

QuickBiz Loans are unsecured, although borrowers should enquire about whether personal guarantees are required. They should also check to ensure the 13.85% rate is based on the outstanding balance rather than the original limit. Any discrepancy would have been evident had the NAB website quoted the interest rate on an APR (annualised percentage rate) basis. Borrowers should also be aware that they could be up for costs if for whatever reason they terminate the loan before the expiry date.

An interest rate of 13.85% is at the lower end of the rates charged by the new breed of online lenders. Banks will always be able to offer cheaper loans to customers because of their lower cost of funds but while it is important, price is not the only factor SMEs consider when it comes to borrowing.

The biggest attraction of the online lenders is the ease of doing business and although there is little doubt that banks can develop software and systems at least as good as the online SME lenders, none of them will survive in this increasingly crowded marketplace if they fail to deliver on the commitments made on their website.

NAB says the QuickBiz loan product is launching in early June, although the website has already been up for several days. In fact, four days ago I applied for a QuickBiz Loan and the experience has been insightful in that the process is not automated, as it is with true online lenders where your application is made totally online. Rather this was an online enquiry. In addition it has not been quick. Having submitted answers to several basic questions about my identity and existing relationship with NAB, I then received the following message in an automatically generated email:

“Thank you for your enquiry regarding the NAB QuickBiz Loan.

“We are currently reviewing the information you provided us and we’ll be in touch shortly to discuss your application further.”

Four days later there has been no response. Of course there are always teething problems in implementing new ways of doing business but this experience re-enforces the importance of good execution. Banks have lots of great products and ideas but too often their execution lets them down.

If the big banks really get their act together with online SME lending, it’s going to be tough for the new little guys to compete. But this remains a big “if” and in the meantime the new players are backing their ability to do better on product and service delivery.

However this unfolds, we are finally starting to see genuine competition in the SME lending market and that’s a great thing for those SMEs who for years have been missing out.

Author: Neil Slonim who is the founder of theBankDoctor.org, a not-for-profit online resource centre that helps business owners deal with the challenges of funding their business. Reproduced from SmartCompany with permission.

This follows a rise of 0.4 per cent in March 2016.

In seasonally adjusted terms, there were rises in cafes, restaurants and takeaway food services (1.0 per cent), household goods retailing (0.3 per cent), clothing, footwear and personal accessory retailing (0.5 per cent), other retailing (0.2 per cent) and department stores (0.4 per cent). Turnover in food retailing fell 0.3 per cent in April 2016.

In seasonally adjusted terms, there were rises in New South Wales (0.3 per cent), Western Australia (0.6 per cent), South Australia (0.5 per cent), Tasmania (1.0 per cent), the Australian Capital Territory (0.9 per cent) and the Northern Territory (0.7 per cent). There were falls in Victoria (-0.3 per cent) and Queensland (-0.1 per cent) in April 2016.

The trend estimate for Australian retail turnover rose 0.2 per cent in April 2016 following a 0.2 per cent rise in March 2016. Compared to April 2015, the trend estimate rose 3.4 per cent.

Online retail turnover contributed 3.0 per cent to total retail turnover in original terms.

Small businesses around Australia will soon be able to develop and grow through a new digital marketplace called Proquo; a start-up joint venture between NAB and Telstra.

Proquo will offer more than two million Australian small businesses an online platform to network, trade or swap services with each other.

Small businesses will be able source a range of services from other providers, create briefs for the work they need, exchange quotes, manage payments and publish reviews all on the one simple platform.

Proquo is a modern interpretation of the phrase quid pro quo (meaning ‘this for that’) and offers users the unique ability to swap or exchange their skills or services in addition to traditional monetary payments.

Proquo was developed by NAB’s innovation hub, NAB Labs and Telstra’s Gurrowa Innovation Lab. While it is a 50/50 joint venture, it will operate as an independent entity.

NAB Executive General Manager Micro and Small Business Leigh O’Neill said NAB was continually looking at ways to support Australian businesses and to make it easier for them to build their business.

“Small business is the backbone of the Australian economy; around 97% of all Australian businesses are small businesses and they provide a huge economic contribution to Australia’s current and future prosperity,” Ms O’Neill said.

“Small business owners tell us they are continually looking for new ways to do business and we think Proquo will provide them with a unique way to network and grow their business.

“Strategic partnerships like this one with Telstra, to combine the capabilities of two of Australia’s biggest companies, creates a really innovative business option for the small business community,” Ms O’Neill said.

Telstra Group Managing Director Telstra Business, Andy Ellis said Telstra supports more than 1 million businesses across the country with technology solutions so they can focus on running their business; and believes Proquo will offer them a new and innovative way to network and help their business thrive.

“Small businesses often struggle to get off the ground and our research shows that the exchanging of services will be a great advantage to many start-ups.

“We’re excited and proud to partner with NAB to offer this unique digital platform. This joint venture further highlights our commitment to small business so they can run, develop and grow their business,” said Mr Ellis.

Proquo will begin a pilot phase in June, with a full launch expected in July 2016.

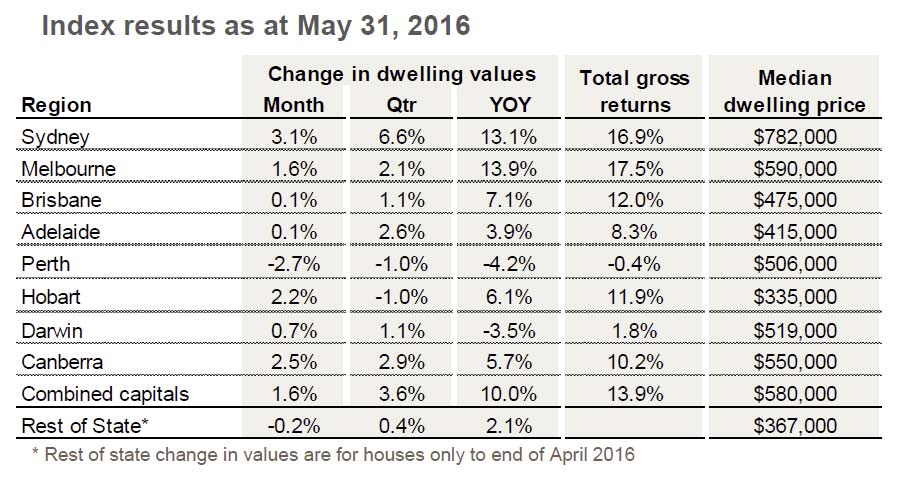

The latest home price data from CoreLogic RP Data shows that dwelling values across the combined capital cities of Australia rose by 1.6% in May with house values driving most of the capital gains, up 1.8% compared with a 0.1% rise in unit values. The strong May numbers were largely the result of a surge in Sydney dwelling values which were up 3.1% over the month. A rise of more than 1% month-on-month was also recorded in Melbourne (1.6%), Canberra (2.5%) and Hobart (2.2%). Perth was the only city to record a fall in dwelling values over the month, down 2.7%.

The CoreLogic combined capitals index has recorded a 5.0% increase since the beginning of January and as a result, has caused the annual trend in capital gains to rebound after conditions tapered since July last year. The annual rate of growth, which recorded a recent trough in December last year at 7.4%, has since rebounded back to 10.0% at the end of May.

After such a strong performance across the Sydney housing market, the annual rate of growth has moved substantially higher to reach 13.1% per annum after reaching a recent low point of 7.4% per annum growth over the 12 months ending March 2016. Despite Sydney’s bounce in the trend rate of growth, Melbourne’s housing market is still recording the highest annual rate of capital gain at 13.9%.

Perth and Darwin remain the only markets to record an annual decline in home values. Perth dwelling values are down 4.2% over the past year and have recorded a peak to current fall of 6.7%. Similarly, Darwin dwelling values fell by 3.5% over the past year and are down 5.5% since peaking two years ago.

The current growth cycle has been running for four years now. After capital city dwelling values fell by 7.4% between October 2010 and May 2012, values have since risen by 36.6% over the growth cycle to date. The largest capital gains over the cycle to date have been in Sydney where dwelling values are 57.5% higher followed by Melbourne with a 39.4% capital gain since values started rising. The third strongest performance has been in Brisbane at 18.5%. The rebound in the rate of capital gain during 2016 is supported by other measurements in the market. Auction clearance rates across the combined capital cities have remained stable and hovered around the high 60% to low 70% range since February this year. Sydney clearance rates remain firm, sitting at around the mid 70% mark over the past three weeks while Melbourne clearance rates now sit in the early 70% range.

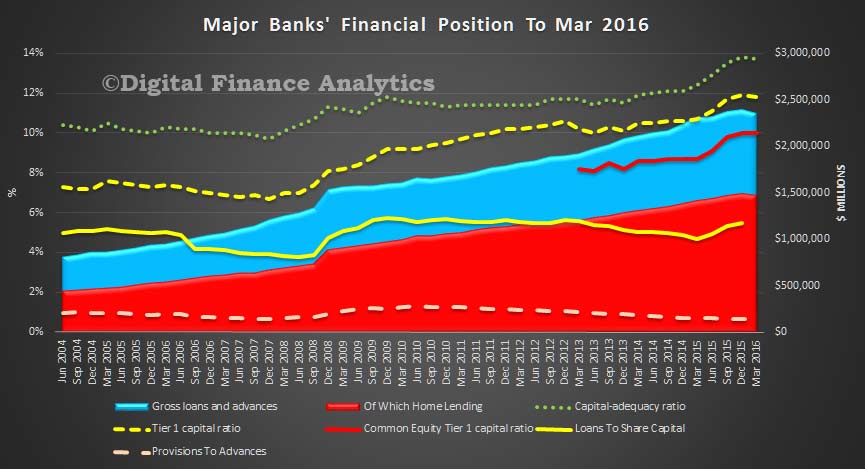

The latest data from APRA to March 2016 relating to the financial position of the banking sector, makes interesting reading. Net Profit after tax for the sector fell 12.5% to $30.8 billion, total assets rose 1.1% from March 2015 and the capital adequacy ratio rose 1.1% to 13.8%. Total provisions were down 13.9% compared with March 2015.

However, once again we have calculated some key ratios, and overlaid this over their loans and advances and there are a number of stresses revealed when we look at the four major banks. Their total provisions are lower despite a rise in consumer delinquency and specific commercial risks, capital adequacy is lower in the past quarter (despite all the raising), and the ratio of loans to share capital, while up slightly, is still lower than in 2010. The sector is under pressure and we think dividend payouts will have to fall and provisions will need to rise.

APRA says

on a consolidated group basis, there were 156 ADIs operating in Australia as at 31 March 2016, compared to 157 at 31 December 2015 and 165 at 31 March 2015.

The net profit after tax for all ADIs was $30.8 billion for the year ending 31 March 2016. This is a decrease of $4.4 billion (12.5 per cent) on the year ending 31 March 2015.

The cost-to-income ratio for all ADIs was 50.0 per cent for the year ending 31 March 2016, compared to 48.4 per cent for the year ending 31 March 2015.

The return on equity for all ADIs was 11.6 per cent for the year ending 31 March 2016, compared to 14.2 per cent for the year ending 31 March 2015.

The total assets for all ADIs was $4.53 trillion at 31 March 2016. This is an increase of $51.1 billion (1.1 per cent) on 31 March 2015.

The total gross loans and advances for all ADIs was $2.91 trillion as at 31 March 2016. This is an increase of $89.0 billion (3.2 per cent) on 31 March 2015.

The total capital ratio for all ADIs was 13.8 per cent at 31 March 2016, an increase from 12.7 per cent on 31 March 2015.

The common equity tier 1 ratio for all ADIs was 10.3 per cent at 31 March 2016, an increase from 9.2 per cent on

31 March 2015.

The risk-weighted assets (RWA) for all ADIs was $1.83 trillion at 31 March 2016, an increase of $25.9 billion (1.4 per cent) on 31 March 2015.

Impaired facilities were $14.4 billion as at 31 March 2016. This is a decrease of $0.8 billion (5.2 per cent) on 31 March 2015.

Past due items were $12.5 billion as at 31 March 2016. This is an increase of $18.1 million (0.1 per cent) on 31 March 2015; Impaired facilities and past due items as a proportion of gross loans and advances was 0.93 per cent at 31 March 2016, a decrease from 0.98 per cent at 31 March 2015.

Specific provisions were $6.9 billion at 31 March 2016. This is a decrease of $16.7 million (0.2 per cent) on 31 March 2015; and specific provisions as a proportion of gross loans and advances was 0.24 per cent at 31 March 2016, a decrease from 0.25 per cent at 31 March 2015.