The Australian Securities and Investments Commission (ASIC) inquiry into the way mortgage brokers are paid may uncover some isolated shady dealings but the system of remuneration for brokers is already regulated well enough by intense competition.

Assistant Treasurer Kelly O’Dwyer announced the inquiry last year in line with recommendations from the Financial System Inquiry and ASIC recently commenced the inquiry with a scoping paper. The focus is likely to be on whether the advice of brokers is in the best interests of the customers.

As always, there are questions about whether the remuneration incentives for brokers distort their advice. And, again as always, there are questions about whether the fact that big banks own some brokers leads these brokers to favour the products of their owners, and not necessarily to offer the products most appropriate to the customer.

In many ways, the inquiry is just part of the ongoing reviews of different parts of the finance sector. The same arguments are likely to be rehashed.

In announcing the review, ASIC Commissioner Peter Kell was clear that:

“We are focused on consumer protection issues in the context of personal credit products, ranging from small amount credit contracts through to home loans.”

There has been some discussion in the press that loans organised by brokers default at a higher rate than loans written by banks. The Australian Prudential Regulation Authority (APRA) might regard this as a concern for financial stability, but ASIC will be concerned with whether people are getting loans they really should not be. The focus will clearly be on consumer outcomes.

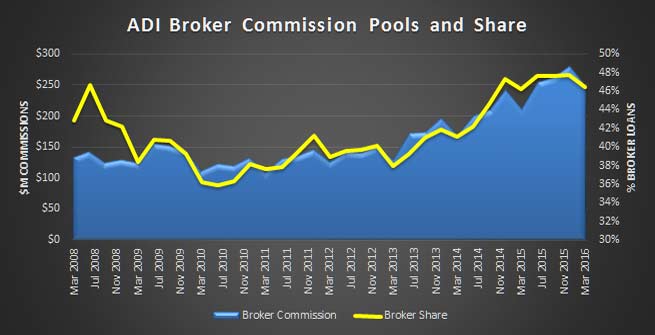

It’s worth looking at the mortgage broking sector mainly because it has been growing rapidly and is now quite big. About half of all mortgages are provided through brokers, up from 40% a decade ago. The upfront commissions for brokers are about 0.5%, which yields annual revenue of close to A$2 billion.

So it is a big and rapidly growing financial sector and ASIC has duly been charged to have a look around for problems. Australia already has laws addressing any concerns. The National Consumer Protection Act has, since 2011, put the onus on providers to act in the best interests of customers. ASIC is really just checking up that the law is being complied with.

While there may be some bad behaviour, it is hard to see what the concern is. People have a choice.

They can go to their own financial institution and buy a mortgage direct from the manufacturer. Alternatively, they can look around among financial institutions to find the mortgage that works for them.

Now they can also go to one of the dozens of mortgage brokers to see if one of them can find a better deal. From the customers’ point of view, there are hundreds of retail outlets (banks and mortgage brokers) offering mortgages.

The fact that mortgage brokers are taking market share away from the banks suggests that customers really appreciate the mortgage broker effectively cutting the buyer’s cost of searching.

There shouldn’t be a problem with the banks paying the broker for delivering the customer, as there is a clear cost saving to the bank. It does not need to have as many branches or as many staff.

Seen from the bank’s point of view, it can originate the mortgage through its own branch and incur some overhead and running costs, or initiate the loan through the broker channel and pay the broker for its overhead and running costs.

Ultimately, the client is buying a product, in this case a mortgage. The price the customer pays is transparent, as are the terms and conditions.

If brokers were not providing a good service, customers could easily swing back to searching for their own mortgage among the banks, or simply walk down the street to another broker. Smart customers will thus keep the providers honest and make sure competition works as it should.

There is a not a lot of academic research into the issues associated with remunerating mortgage brokers. What there is tends to be from the US, which has not had a good record in managing mortgages over recent years. The most relevant paper suggests that loan quality can be improved though requiring registration, higher education standards and continuing education and/or by requiring brokers to post bonds.

The ASIC inquiry will uncover more information about the sector. It may also find some people have behaved badly (as in any area of human endeavour), but it’s hard to see a significant structural problem in a very competitive market.

In other words, whilst we are exporting more volume – and this quarter liquid natural gas was a stand-out, this greater activity did not translate to national or household income. In fact, this continues to fall, as previously shown by the stagnant growth in real incomes. The Australian economy may be running fast, but is not creating more wealth for its residents. Not a pretty picture.

In other words, whilst we are exporting more volume – and this quarter liquid natural gas was a stand-out, this greater activity did not translate to national or household income. In fact, this continues to fall, as previously shown by the stagnant growth in real incomes. The Australian economy may be running fast, but is not creating more wealth for its residents. Not a pretty picture.