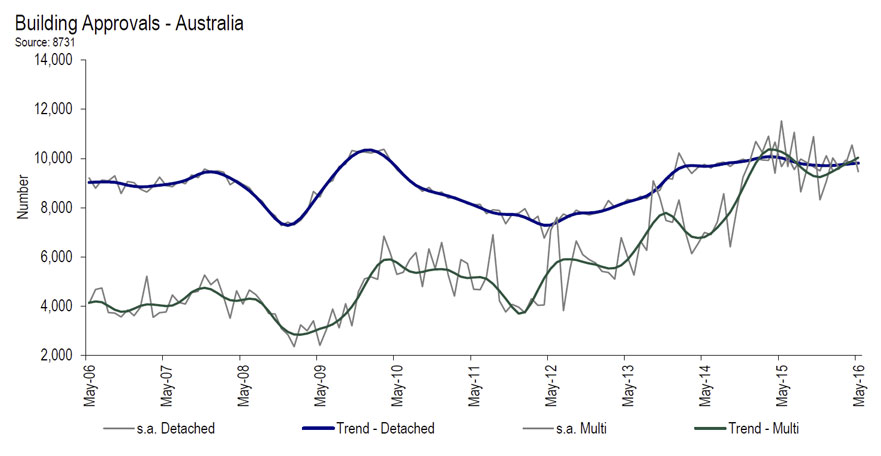

The number of dwellings approved rose 0.9 per cent in May 2016, in trend terms, and has risen for six months, according to data released by the Australian Bureau of Statistics (ABS) today.

Dwelling approvals increased in May in the Northern Territory (18.7 per cent), Australian Capital Territory (8.2 per cent), New South Wales (2.0 per cent), South Australia (1.9 per cent) and Victoria (1.8 per cent), but decreased in Western Australia (2.6 per cent), Queensland (1.8 per cent) and Tasmania (1.2 per cent) in trend terms.

In trend terms, approvals for private sector houses rose 0.2 per cent in May. Private sector house approvals rose in South Australia (1.9 per cent), New South Wales (1.5 per cent) and Victoria (0.2 per cent), but fell in Western Australia (2.2 per cent) and Queensland (0.5 per cent).

In seasonally adjusted terms, dwelling approvals decreased 5.2 per cent, driven by private sector dwellings excluding houses, which fell 11.3 per cent. Private sector house approvals rose 0.1 per cent in seasonally adjusted terms.

The value of total building approved rose 1.0 per cent in May, in trend terms, and has risen for five months. The value of residential building rose 1.5 per cent while non-residential building fell 0.2 per cent.

The value of total building approved rose 1.0 per cent in May, in trend terms, and has risen for five months. The value of residential building rose 1.5 per cent while non-residential building fell 0.2 per cent.

Commenting on the results, HIA Senior Economist, Shane Garrett said

Multi-unit approvals tend to bounce around a lot from one month to the next, but it’s been clear for some time that activity on this side of the market has peaked. Interestingly, the RBA cut interest rates during May and today’s result indicate that this move may have helped contribute to steadier conditions for detached house approvals. The decline in approvals during May was quite widespread in geographic terms, with Victoria being the only major state to experience an increase during the month. Today’s figures fit closely with our view that new home building activity is in the process of declining from last year’s record peak to more modest levels as the end of the decade approaches. The contraction in activity is predicted to be concentrated on the multi-unit side, with a more measured reduction in detached house building.