Westpac today announced a reduction in interest rates across a range of variable lending products for home owners and small businesses, while increasing a range of term deposit rates for savings customers.

Variable home loan (owner occupier) rate reduced by 0.14% to 5.29% per annum for customers with principal and interest repayments;

Variable residential investment property loan rate reduced by 0.14% to 5.56% per annum for customers with principal and interest repayments;

Variable home loan (owner occupier) rate reduced by 0.10% to 5.33% per annum for customers with interest only repayments;

Variable residential investment property loan rate reduced by 0.10% to 5.60% per annum for customers with interest only repayments;

Variable cash rate business loans will be reduced by 0.10%; and

One year term deposit rate increased by 0.55% to 3.00% per annum, two year term deposit rates increased by 0.45% to 3.10% per annum, and three year term deposit rates increased by 0.55% to 3.20% per annum.

The majority of Westpac customers are on the Premier Advantage Package, and receive up to 0.70% discount on their home loan.

George Frazis, Chief Executive of Westpac Consumer Bank, said while home loan rates are at historical lows, today’s decision reflects the complex domestic and international environment banks are facing.

“We take a number of factors into account when making interest rate decisions and, in an environment where the cost of funding and deposits are increasing, we have had to balance higher costs, while keeping rates as low as possible for home owners.

“In this low interest rate environment we have changed how we price interest only home loans compared to principal and interest home loans. As a result, we will now offer lower interest rates to customers who make principal and interest repayments to encourage them to pay down their debt and own their home sooner,” Mr Frazis said.

Customers with interest only home loans who wish to move to principal and interest repayments can do so without paying a switching fee until 30 September 2016.

Westpac offers competitive fixed rate home loan offers in the market, with 2 and 3 year owner occupier fixed rates in Premier Advantage package at 3.75% per annum and 3.85% per annum respectively, effective this Friday 5 August 2016.

ANZ today announced the Standard Variable Rate Indices for Residential Home Loan products will decrease by 0.12%pa, while increasing the rate on its one and two-year term deposits by up to 0.75%pa.

All Standard Variable Rate Indices for Residential Home Loan products to decrease by 0.12%pa. For Owner Occupiers this reduces the Index Rate to 5.25%pa; Residential Investor Index Rate reduces to 5.52%pa. All business lending variable rate indices will decrease by 0.10%pa. Deposit rate special for popular one-year Advanced Notice Term Deposit to increase by 0.60%pa to 3.00%pa; two-year term deposit to increase 0.75%pa to 3.20%pa with both effective 5 August.

ANZ Group Executive Australia Fred Ohlsson said: “This was a considered decision that balances the expectations of our home loan customers to keep lending rates as low as possible, while also supporting our savings customers who help fund our lending.

“Regulatory and funding costs have continued to rise and we need to remain attractive to depositors. We are pleased however that home loan customers can still benefit from these historically low interest rates and that we have maintained a competitive rate for both owner occupiers and investors.

“Customers concerned about the long-term direction of rates are able to take advantage of our highly competitive fixed rates that are now at historical lows, including our rate of 3.75%pa* fixed for two years,” Mr Ohlsson said.

Commonwealth Bank has responded to the Reserve Bank of Australia’s (RBA) cash rate decision by reducing interest rates for home owners and small business while increasing term deposit rates.

Standard Variable Rate (SVR) mortgages reduced by 0.13%; owner occupiers to receive record low rate of 5.22%. Business customers to benefit from 0.13% reduction to variable cash rate products, One year term deposit rate increased to 3.00%, a rise of 0.55%, Two and three year term deposit rates to lift by 0.50% to 3.10% and 3.20% respectively. All offers available to new and existing customers.

The CBA standard variable rate (SVR) mortgages will reduce by 0.13%, taking the rate for owner occupiers to a record low 5.22%. The SVR for investor loans will fall to 5.49%. While this decrease delivers benefits to mortgage holders, Commonwealth Bank will also support savers by increasing the return on several products, some by as much as 0.55%.

“While the circumstances of each RBA rate decision will always vary, we’ve carefully considered the current environment and the needs of both borrowers and savers,” said Matt Comyn, Group Executive Retail Banking Services.

“Today we’ve reduced our mortgage rates to a record low while increasing term deposit rates to provide an opportunity to the millions of Australians who rely on savings.”

To meet the needs of savers, Commonwealth Bank will increase one, two and three year term deposits with all rates set to rise to 3.0% or greater.

“Given increased funding costs and capital requirements, today’s announced changes seek to balance the needs of both customers and shareholders,” Mr Comyn said.

Business customers with variable rate products will also benefit from a 0.13% rate reduction.

Over the past two years, the official cash rate has decreased three times, and during this period Commonwealth Bank home loan customers who are owner occupiers have had cumulative savings of about $939 a year on the average loan of $350,000.

CBA fixed mortgage rates are unchanged and all new rate offers announced today will be effective from Friday, 19 August.

NAB has announced it will reduce its variable rate on all new and existing variable rate home loans by 0.10% per annum, effective from Friday 19 August 2016. This means NAB’s Variable Rate for Home Loans (Standard Variable Rate) will reduce to 5.25% p.a.

NAB Chief Operating Officer, Antony Cahill, said NAB had carefully considered the needs of customers and shareholders and the current economic and regulatory environment in making this decision.

“We have had to strike the right balance between providing customers with competitive mortgage rates and continuing to generate attractive returns for our 584,000 shareholders, while recognising that NAB’s funding costs have been steadily increasing due to a range of factors, including the need to strengthen our balance sheet,” Mr Cahill said.

“We also need to be able to continue investing in the products and services our customers want.”

As a result of today’s announcement, NAB customers with a standard variable rate home loan will save $18 each month on their home loan principal and interest repayments, or $216 every year (based on a $300,000 loan over a 30-year term).

At 5.25% p.a., NAB’s new Standard Variable Rate will be the lowest it has been for more than 40 years. In November 2010, the average standard variable interest rate across Australian banks was 7.80% per annum*, compared with NAB’s new Standard Variable Rate of 5.25% p.a. and under 4.00% p.a. for some fixed rate products.

Mr Cahill said NAB is committed to providing customers with great value and service. As at March this year, NAB home loan accounts are, on average, almost 15 months ahead on their repayments, and Mr Cahill said NAB has a range of home loan products available to suit customers’ needs.

“We understand some customers want to have certainty about their monthly repayments and that’s why we offer a number of highly competitive fixed-rate terms which allow customers to lock in interest rates for all or part of their home loan,” Mr Cahill said.

NAB is currently offering a suite of “4-under-4” fixed rate home loan offers. For owner-occupier principal and interest borrowers, interest rates ranging from 3.75% p.a. to 3.99% p.a. are now available across 1, 2, 3 and 4 year terms. Competitive offers are also available to those borrowing for investment purposes.

Also, from Monday 8 August, NAB will increase its interest rate on 8-month Term Deposits by 0.85% p.a., introducing a Blackboard Special of 2.90% p.a. (interest paid at maturity).

NAB will also reduce its rate for standard variable business rate lending products by 0.10% per annum, effective from Friday 19 August 2016.

I had the opportunity to catch up with the joint CEO’s of the SME digital market place, Proquo – Carl Spurling, from NAB and Ricky Lam from Telstra, to discuss the development of the platform and their future plans.

Proquo was formally launched a couple of months ago, following research in 2015 with SME’s from NAB’s SME Village and Telstra’s Gurrowa Labs. It uses a custom built software platform to enable SME’s to build a network of contacts and to trade with each other, for cash or in kind. Proquo say they are well on their way to acquiring their target of 2,000 customers in the first six months, from across the country.

We discussed the motivation for the launch of the business. Both NAB and Telstra have strong interest in the SME sector, and recognise the importance of getting SME’s digitally enabled. They cited research showing that 40% of SME’s were not online at all. They said they had identified a real need to provide an onramp for SME’s, and so spotted the opportunity to create the marketplace.

Now Proquo offers small business owners and accounting experts access to a range of services from other providers. Users can create briefs for the work they need, provide quotes, manage payments and publish reviews, all on the one platform. Micro and small business owners, as well as experts in the accounting industry are invited to register for free to take advantage of this tool to aid networking and help their business thrive. The services offered under the accounting umbrella include: Budgeting, Book keeping, Xero, tax and many more.

They want to focus, rightly, on getting the core platform running smoothly, and acquiring new customers. However, we discussed some of the potential extension strategies which might be considered later.

First, the data which is being captured in the system has the potential to be used for many purposes. For example, individual SME’s could be rated, just like other digital marketplaces, as part of building a network of trusted contacts. They have no firm plans to offer loans, but with the NAB connection, it is certainly an option for later.

Another angle could be the consolidation of purchases, via ecommerce, thus enabling individual businesses to gain group discounts. Again, for now, group buying is not enabled, but could be in the future.

We also discussed the thorny tax issues around offering services in kind. The ATO of course says that barter transactions will have a tax implication. So it will be important to track and manage this aspect. Whilst Proquo can generate a range of documents, they will not be offering tax advice. That said, within the network there could be Accountants who could help. We think there is an opportunity for Proquo to embed this type of tax reporting in the system.

Finally, today the platform is web based, and optimised for mobile, tablet and PC. Down the track, they may well consider a dedicated app, but only once the core functionality has been bedded down.

For now, Proquo is focussing on getting established with a high-quality portfolio of businesses. They will measure success by how successful customers on the platform will be, and how much value SME’s gain from it. Whilst it is a for-profit business in the long term, their initial focus is on building momentum and value for their customers.

We think this is an excellent example of digital innovation, and has the potential to assist many SME’s, who in the early years especially find building a network of customer’s hard work, and funding difficult. In fact, half will fail in their first five years in business. Proquo looks like a good catalyst and the SME sector should welcome the innovation it represents.

At its meeting today, the Board decided to lower the cash rate by 25 basis points to 1.50 per cent, effective 3 August 2016.

The global economy is continuing to grow, at a lower than average pace. Several advanced economies have recorded improved conditions over the past year, but conditions have become more difficult for a number of emerging market economies. Actions by Chinese policymakers are supporting the near-term growth outlook, but the underlying pace of China’s growth appears to be moderating.

Commodity prices are above recent lows, but this follows very substantial declines over the past couple of years. Australia’s terms of trade remain much lower than they had been in recent years.

Financial markets have continued to function effectively. Funding costs for high-quality borrowers remain low and, globally, monetary policy remains remarkably accommodative.

In Australia, recent data suggest that overall growth is continuing at a moderate pace, despite a very large decline in business investment. Other areas of domestic demand, as well as exports, have been expanding at a pace at or above trend. Labour market indicators continue to be somewhat mixed, but are consistent with a modest pace of expansion in employment in the near term.

Recent data confirm that inflation remains quite low. Given very subdued growth in labour costs and very low cost pressures elsewhere in the world, this is expected to remain the case for some time.

Low interest rates have been supporting domestic demand and the lower exchange rate since 2013 is helping the traded sector. Financial institutions are in a position to lend for worthwhile purposes. These factors are all assisting the economy to make the necessary economic adjustments, though an appreciating exchange rate could complicate this.

Supervisory measures have strengthened lending standards in the housing market. Separately, a number of lenders are also taking a more cautious attitude to lending in certain segments. The most recent information suggests that dwelling prices have been rising only moderately over the course of this year, with considerable supply of apartments scheduled to come on stream over the next couple of years, particularly in the eastern capital cities. Growth in lending for housing purposes has slowed a little this year. All this suggests that the likelihood of lower interest rates exacerbating risks in the housing market has diminished.

Taking all these considerations into account, the Board judged that prospects for sustainable growth in the economy, with inflation returning to target over time, would be improved by easing monetary policy at this meeting.

SuperConcepts has announced the acquisition of Reckon’s Desktop Super platform, which will see the transition of approximately 16,000 SMSF software clients to the SuperConcepts business.

The acquisition continues SuperConcepts’ growth as a provider of SMSF software services to accountants and specialist SMSF advisers, increasing its market share across both administration and software services from 6.8 to 9.7 per cent.

SuperConcepts and Reckon have also formed a strategic alliance to leverage each other’s expertise and industry relationships to provide customers with a leading SMSF software service.

Natasha Fenech, CEO SuperConcepts said the acquisition and strategic alliance is another step forward ingrowing the SuperConcepts business as a leading end-to-end service provider in the SMSF market.

“Reckon is a highly-regarded provider of accounting software services. We’re excited to form an alliance that will help us to enhance the level of service and technology available to SMSF trustees and their advisers.

“SMSF software continues to be a key part of our strategy and we will continue to invest in the technology as we expand our service to become a market leader in SMSF software solutions and partner of choice forthe SMSF industry,” she said.

In-line with its strategy, SuperConcepts has continued to build scale in the SMSF market as an end-to-end provider of administration, software and education services to SMSF trustees, accountants and financial advisers.

Sam Allert, Managing Director Reckon for Australia and New Zealand said: “Our strategic alliance with SuperConcepts ensures Reckon is providing the best value SMSF software solution to our clients going forward. We’re thrilled to be to working with a leading brand in the SMSF administration market and this is just the start of a powerful partnership.”

Desktop Super customers will not notice any immediate change to the way they access their funds.

About SuperConceptsSuperConcepts is a leading provider of self-managed superannuation fund (SMSF) administration, software and education services to SMSF trustees, accountants and financial advisers, servicing more than 40,000 funds.SuperConcepts comprises a number of sub-brands including AMP SMSF, Ascend, Cavendish, Multiport, Justsuper, SuperConcepts, SuperIQ, superMate, yourSMSF and a part ownership of Class Ltd. Find out more at www.superconcepts.com.au.

About ReckonReckon is an ASX listed and Australian owned company with over 25 years’ experience delivering market leading solutions to accountants and bookkeepers, legal professionals and small to medium sized businesses. Reckon’s software solutions are designed to make accounting faster, easier and more productive. Find out more at www.reckon.com.

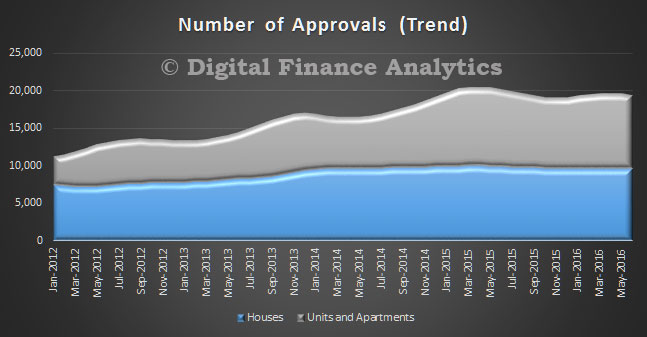

The number of dwellings approved fell 0.9 per cent in June 2016, in trend terms, according to data released by the Australian Bureau of Statistics (ABS) today. This is the second successive monthly fall.

Dwelling approvals decreased in June in Western Australia (5.2 per cent), Tasmania (3.7 per cent), Queensland (3.2 per cent), Australian Capital Territory (2.8 per cent) and Victoria (0.1 per cent), but increased in the Northern Territory (3.6 per cent), South Australia (1.6 per cent) and New South Wales (0.8 per cent) in trend terms.

In trend terms, approvals for private sector houses fell 0.6 per cent in June. Private sector house approvals fell in Western Australia (3.5 per cent), Victoria (0.6 per cent), Queensland (0.5 per cent) and South Australia (0.3 per cent). Private sector house approvals rose in New South Wales (0.9 per cent).

In seasonally adjusted terms, total dwelling approvals decreased 2.9 per cent, with both total other residential dwelling approvals (3.4 per cent) and total houses (2.4 per cent) recording falls.

The value of total building approved rose 1.2 per cent in June, in trend terms, and has risen for six months. The value of residential building rose 0.1 per cent while non-residential building rose 3.7 per cent.

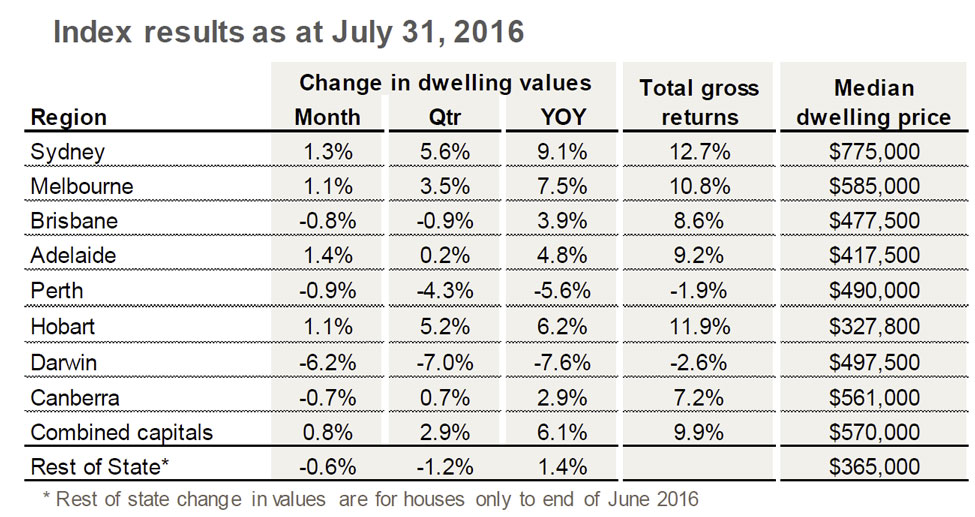

The latest Corelogic data shows that their hedonic eight capital city aggregate index rising 0.8 per cent over the month to reach a new record high. But the movements varied considerably across the capital cities and rental yields fell again.

The annual rate of growth, which hit a recent peak at 11.1 per cent across the combined capitals index in October last year, is now tracking at 6.1 per cent; the slowest annual rate of appreciation since September 2013.

Sydney and Melbourne have also seen the annual rate of growth slip back to below 10 per cent, with the July indices showing a respective 9.1 per cent and 7.5 per cent capital gain over the past twelve months. Darwin and Perth remain as the only two capital cities to record a negative movement in dwelling values over the past twelve months, with values in Darwin down 7.6 per cent and Perth values falling by 5.6 per cent.

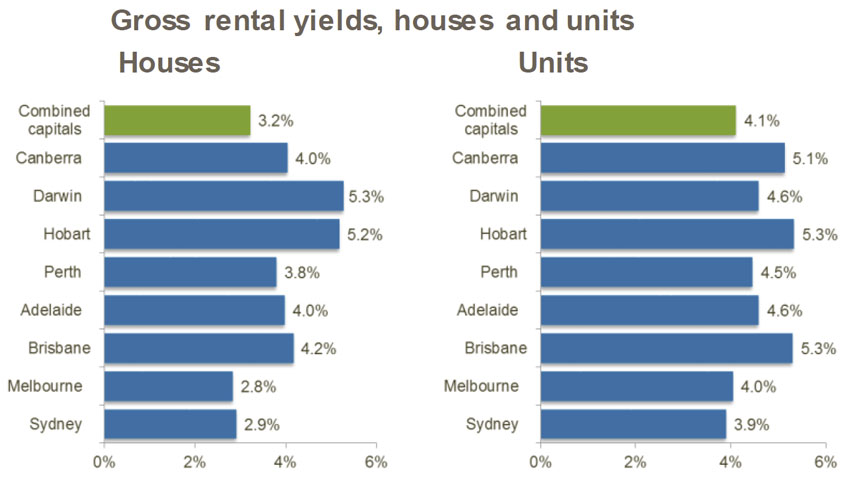

Capital city rental yields have fallen to a new low of 3.3 per cent, with Melbourne down to 2.6% and Sydney 3.9 per cent.

Kabbage is one of the most interesting platform lenders offering loans to SME’s in the US, and now Canada, Mexico and via white label platforms other countries, including Australia. Their analytic platform takes business activity data such as online sales and accounting information to facilitate fast underwriting in just a few minutes. Loans of up to $100,000 are available to businesses with a turnover of $50,000 or more.

The Kabbage platform has originated more than US$1.6 bn in loans, via Kabbage, the SME platform, Karrot, their consumer lending business and via white labeling to third party lenders. Kabbage is funded and backed by leading investors including Reverence Capital Partners, SoftBank Capital, Thomvest Ventures, Mohr Davidow Ventures, BlueRun Ventures, the UPS Strategic Enterprise Fund, ING, Santander InnoVentures, Scotiabank,and TCW/Craton.

In 2015 Kabbage announced plans to move into the Australian market with a white-label offering of its small business lending technology. The launch in Australia represents Kabbage’s first foray into the Asia-Pacific region, having already been in operation in both the U.K. and the U.S.

The service in Australia is operated by Kikka Capital, which licensed the platform and manages marketing, funding, and loan servicing. Kabbage handles underwriting and management of the loans.

Here is an interesting post where Kabbage discuss small business funding options. We have previously discussed the difficulty SME’s face in getting access to funding, and the role of fintechs have in changing the lending landscape. The latest Disruption Index measures the growth in momentum for SME lending in Australia.

Many small business owners might at some point find it difficult to get working capital or a small business loan from a traditional bank – and in that situation, it’s important to know about the various alternative loan options that are available.

According to a recent article in the Harvard Business School “Working Knowledge” blog, as of May 2014, only 13 percent of applicants for small business loans at big banks were getting approved. The SCORE organization has found that small business owners are less likely to get a bank loan if their business is young (less than 2 years in business), if they have less than perfect credit (credit score below 640) and if they are seeking a relatively small loan amount (less than $250,000). Big banks tend to prefer to issue larger loans than most small business owners need, because the banks’ costs of issuing loans are not much smaller for small loans than they are for big loans.

According to a survey published in an article in the Wall Street Journal, 19 percent of small business owners have postponed investments in their businesses because of lack of loan funding, and only 18 percent could get a bank loan – faced with a lack of funding from traditional sources, 17 percent of business owners borrowed money via credit cards, and 13 percent asked their friends and family for loans. Small business owners are starting to get more creative in looking for alternative loan options when they cannot get what they need from the traditional bank lenders.

One of the biggest new trends in helping business owners find alternative loan options is the rise of platform lending. With platform lending, borrowers can get the money they need without relying on the traditional bank system. A study from Harvard Business School found that in 2014, although the total loan volume of small business bank loans decreased by 3.1 percent, overall online lending to small businesses grew by 175 percent. This is a sure sign that platform lending is on the rise and is taking the place of traditional lenders.

With so many business owners seeking loans and finding it more difficult to get approved by traditional bank lenders, it’s no wonder that new options like platform lending are starting to fill the gap. Platform lending is an innovative new way to get loans, where people can sign up online, go through a faster, efficient approval process and get the funds they need more quickly than a typical bank loan.

If you’re looking for a small business loan and wondering how to navigate the alternative loan options such as platform lending, here are a few guidelines on how to evaluate each of your options:

Loan from Family and Friends

Borrowing from family and friends is often a first-resort loan for many small business owners. After all, the people who know and love you best are often eager to support you in your business endeavors. If you want to let your family and loved ones in on a great investment opportunity, selling equity in your business or asking for a small business loan could be one way to get the cash you need.

Advantages: Friends and family typically know you best, and they will believe in you and support your vision of success, even if a traditional bank lender cannot offer you a loan. It’s natural to want to turn to your inner circle first. And your family might be willing to give you more favorable payment terms – lower interest rate, longer time to pay off the loan, etc. – than a typical bank would.

Drawbacks: First of all, it can be hard to raise enough money just by asking your family and friends. Unless your family are a bunch of angel investors, they might not have enough money to spare to be able to fund a significant business investment. And even if you can get enough money from them, borrowing from friends and family can be risky – not only in a financial sense, but also emotionally risky. After all, what if your business idea doesn’t work out? What if you lose your family’s money? What if your business becomes a source of hurt feelings and damaged relationships with the people you love most? It’s often better to keep business and family concerns separate from each other.

Crowdfunding

Other small business owners look for alternative loan options by using crowdfunding. By setting up an online crowdfunding campaign, your business can ask your social media followers, friends and fans to contribute money to help fund your business’ next phase of growth.

Advantages: Online crowdfunding platforms like Kickstarter, GoFundMe and others give you the power to raise money to support your business, whether it’s funding for new product development or for any other specific purpose. By giving away prizes and using other participation strategies, you can motivate people to give more money – for example, by giving donors a special behind-the-scenes experience or an early-stage sample of your new product.

Drawbacks: Crowdfunding is flexible and adaptable, but that same flexibility can also make the results unpredictable: according this Kabbage article, the typical crowdfunding campaign takes about 9 weeks and raises an average of $7,000. Depending on how much time you have and how much money you need, crowdfunding might not be the best fit for your goals.

Platform Lending

With banks making it more difficult for small business owners to get loans, a variety of online services known as “platform lending” services have come onto the market. Kabbage is one of these online platform lenders where business owners can get loans more quickly and often more effectively than they could from a traditional lender.

Advantages: Platform lending is often a good option for people who have less-than-perfect credit. Also the loan amounts offered by platform lending services are often a better fit with what small business owners are seeking – for example, $40,000 to $100,000. Another advantage of platform lending is that the approval process is more flexible and relevant to small businesses than the traditional bank loan process; for example, platform lenders tend to look at a business’ online sales and social media following and other metrics to show the creditworthiness of the business that are separate from the traditional approach of looking at credit scores.

Drawbacks: Platform lending tends to charge a slightly higher interest rate than a typical bank small business loan. Make sure to do your research and understand the fine print of any platform lending agreement before you sign – just like you would if you were signing up for a new credit card or other financial product.

If your business is struggling to get approved for a bank loan, don’t get discouraged – get money! There are more alternative loan options than ever before, especially if you are able to be creative and flexible and pursue some new services like platform lending.