Another day, another tax headline. This week, it’s Apple, which faces a €13 billion (£11bn) tax bill in Ireland from the EU. Everyone says there must be a better way to make business pay its way. I support boosting the tax take, too, though not by punishing companies. Earlier this year, I argued in The Conversation that it was time for progressives to think the unthinkable and get rid of corporation tax.

UK politicians remain to be convinced, alas. The All Party Parliamentary Group’s recent report on the global tax system stated:

Some experts have argued that we should stop trying to tax the profits of global companies. We disagree. Governments need a range of taxes to fund public services and corporate profits form one part of that range.

They haven’t recognised that you could bring in much the same revenue for the state by shifting the burden to shareholders. How? By fully taxing company dividends – and reaping the tax proceeds of people selling UK shares that have risen because of companies becoming more profitable after being freed from corporation tax.

But here I want to propose another carrot: charge companies an annual fee to be registered in the UK.

Ever-decreasing corporation tax

Corporation tax brings in around 6% (net of dividend allowance) of UK tax revenues. Former chancellor George Osborne intended in the wake of Brexit to cut UK rates from the current 20% to 15% of companies’ pre-tax profits. Philip Hammond, his replacement, has yet to announce a policy but has signalled he may move in the same direction.

Coupled with further erosions to the corporate tax base due to internet trading and the relocation of intellectual property to more favourable tax regimes, the day is soon likely to arrive when the UK struggles to raise 4% of its tax revenues from corporation tax. What’s this in money terms? Say £20bn (compared to £30bn, net of tax credits, in 2015-16).

So how much corporation tax would be raised on average from UK companies each year if tax revenues fell to £20bn? There are 3.5m limited companies in the UK. But 2m are dormant, so only 1.5m are actively trading. This means that each company would be paying just over £13,000 each year to HMRC on average.

I don’t know the average cost of a company complying with corporation tax each year, but it won’t be far removed from £13,000 (much higher for multinationals, much lower for small companies). And while companies only pay taxes when they make profits, they must make tax returns either way. It’s also worth remembering that many companies are subject to investigations, make appeals and sometimes end up in court – more costs.

Now suppose we charged an annual fee for the privilege of being a UK company, using a fee scale based on company size. While companies would now be paying to be UK-registered, most would save more by not having to comply with corporation tax.

You could set the fee levels to bring in roughly what the government lost in corporation tax. In addition, the government would still have the revenue from the higher dividends and capital gains I mentioned earlier. In total, the income for the state would have risen substantially.

Collection of this fee would be simple. Companies would pay it when they deliver their confirmation statement (the replacement for the annual return). Penalties and interest would apply if payments were late – another source of money for government.

More information would be required to determine the number of fee bands and the charge per band for these new company fees, but below is a possible structure. Though the rates would of course be much higher for big companies, these are probably still comparable to what they spend on dealing with their tax affairs.

I’ve spoken to a few people who run or are involved with companies about how they would react to a system like this. What was their reaction? They’d bite your hand off to sign up, basically.

And a final thought. If the UK abolished corporation tax, where do you think Apple, Google and others would consider relocating given the problems the EU has created for Ireland?

Author: Grahame Steven, Lecturer in Accounting, Edinburgh Napier University

Access to a roaming service would enable mobile service providers to provide coverage for their customers in areas where they don’t have their own network.

The ACCC is aware that mobile coverage is an increasingly important issue in Australia, with a greater impact on those living in regional areas.

“Consumers are increasingly relying on mobile services and the issue of coverage and a lack of choice in some regional areas is a particular issue that has been raised by a number of groups,” ACCC Chairman Rod Sims said.

“There has been significant interest in the questions around access to mobile networks and mobile roaming, including from representatives from regional Australia, the Regional Telecommunications Review Committee, Infrastructure Australia and the House of Representatives Agriculture Committee.”

The ACCC says a declaration inquiry would focus on a number of key issues, including:

how consumer demands for mobile services are evolving, and whether there are differences in regional areas to urban areas

the likely investment plans of each of the mobile network operators to extend coverage and upgrade technology, absent a declaration

whether there are any significant barriers to expanding the reach of mobile networks

any lessons from similar experience with domestic mobile roaming in other countries.

The ACCC has previously considered mobile roaming in regional areas in inquiries held in 1998 and 2005 respectively. On both occasions it decided not to regulate an access service as it was satisfied roaming agreements were being commercially negotiated.

“Network coverage is clearly a key feature of a mobile service, and each of the mobile network operators has extended its networks since we last looked at this issue in detail,” Mr Sims said.

“A lot has changed since 2005. We do think it’s time we look at the issue again in detail, and examine some of these key matters, including consumer demand, network investment, and barriers to competition. We consider the most efficient way to do that is to consider all of the issues carefully through a declaration inquiry.”

Mr Sims stressed that, at this stage, the ACCC had not formed any views on whether declaration of a mobile roaming service would deliver benefits for consumers.

“A particular area of concern for us is whether consumers would, in fact, be disadvantaged if the incentives to invest in expanding the reach of mobile networks were reduced,” Mr Sims said.

“We considered whether we should examine mobile roaming issues as part of the market study. However, we decided that a more focused inquiry to deal with the issue more quickly will provide the market with greater certainty, sooner,” said Mr Sims.

The company formed by the payments industry to build and operate the New Payments Platform, NPP Australia Limited, has a new CEO, with the commencement today of Adrian Lovney as its inaugural Chief Executive Officer.

The New Payments Platform is a major industry initiative to develop new national infrastructure for fast, flexible, data rich payments in Australia. The Program proceeded to the fourth phase, “build and internal test” in August 2015. The NPP is on track to being operational in the second half of 2017.

The Program reached a historic milestone in December 2014 when 12 leading authorised deposit-taking institutions (ADIs) committed funding for the build and operation of the NPP. These institutions became the founding members of NPP Australia Limited.

NPP Australia also signed a 12-year contract with global provider of secure financial messaging services Society for Worldwide Interbank Financial Telecommunication (SWIFT) to design, build and operate the basic infrastructure. The establishment of NPP Australia and the appointment of SWIFT marked the launch of the Program’s “design and elaborate” stage, which was then successfully completed in July 2015. The current “build and internal test” stage is scheduled for completion in early-mid 2017.

In October 2015, NPP Australia reached agreement with Australia’s premier bill payment system provider -BPAY – to deliver the first overlay service to use the NPP once it is operational in the second half of 2017.

The NPP will be open access infrastructure for Australian payments. The intention is that all ADIs will connect to the NPP, either directly or indirectly through another member, so they can process a wide variety of fast data-rich payments for their account holders. ADIs can choose to join the NPP at any point in its development and operation.

Core members are Australia and New Zealand Banking Group Limited, Australian Settlements Limited, Bendigo and Adelaide Bank Limited, Citigroup Pty Ltd, Commonwealth Bank of Australia, Cuscal Limited, HSBC Bank Australia Limited, Indue Ltd, ING DIRECT, Macquarie Bank Limited, National Australia Bank Limited, Reserve Bank of Australia and Westpac Banking Corporation.

NPP Australia Chairman Paul Lahiff said in June, “Adrian is an energetic leader with a passion for leading large-scale transition programs and is well-equipped to head up the commercialisation of the NPP.”

“Adrian emerged as the outstanding candidate from an extensive domestic and global search process and the NPPA Board is delighted to have secured his services,” Mr Lahiff said.

Mr Lovney was the General Manager of Product & Service at Cuscal Ltd with responsibility for product, services, and customers across the business, including leading the organisation’s work in NPP. Previously, he was Cuscal’s General Manager Strategy & Communications, responsible for leading the evolution of Cuscal’s business over the last five years as well as the successful migration and transition of customers to a new and innovative payments platform.

Mr Lovney said in June , “I am honoured to be taking on this important role at this critical stage in the development of Australia’s New Payments Platform. The NPP is a uniquely Australian take on the real time payments infrastructure being implemented overseas. Its layered business architecture will deliver scale and efficiency, while supporting a diverse range of fast payments well into the future.

“These are exciting times and I am thrilled to be able to work with the NPP Australia Board and shareholders of NPP to help them realise the benefits of the investment they have made in this new payments system for Australia,” Mr Lovney said.

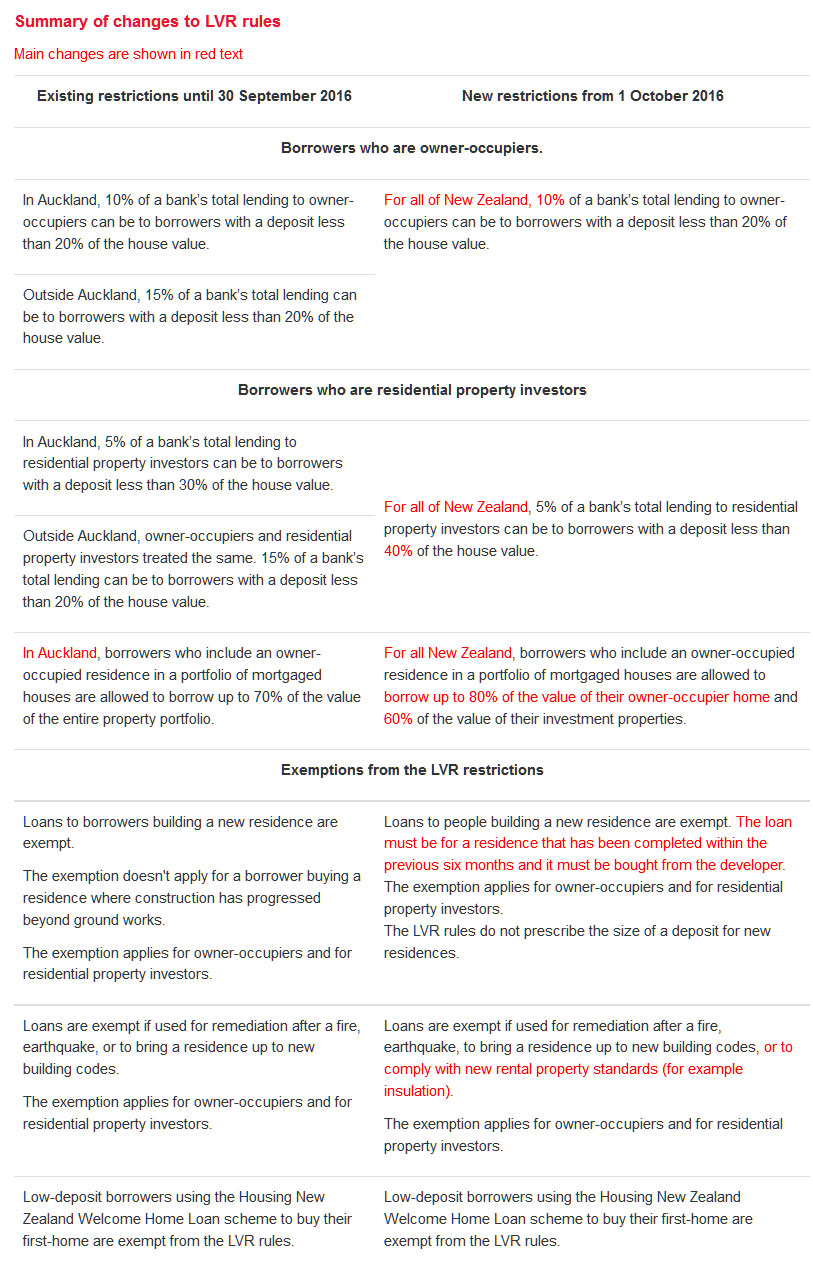

The NZ Reserve Bank today confirmed that new macroprudential rules tighten restrictions on bank lending to residential property buyers throughout New Zealand. Residential property investors will generally need a 40 percent deposit for a mortgage loan, and owner-occupiers will generally need a 20 percent deposit.

From 1 October, residential property investors will generally need a 40 percent deposit for a mortgage loan, and owner-occupiers will generally need a 20 percent deposit. In both cases, banks are still allowed to make a small proportion of their lending to borrowers with smaller deposits.

Confirmation of the new rules is in the Reserve Bank’s response to submissions to its public consultation about changes to Loan to Value Ratio (LVR) rules that was issued on 19 July.

The Reserve Bank is modifying its proposals in response to public consultation, and also through meetings and workshops with banks that are subject to the rules.

The new rules take effect on 1 October 2016, but banks have chosen to start following the new limits already.

Existing exemptions to LVR restrictions will continue to apply under the new rules and have been extended to include borrowing for a newly-built home, or to do work needed for a residence to comply with new building codes and rental-property standards.

The Federal Government’s plan to wind back superannuation tax breaks would create a fairer superannuation system more aligned to its purpose of providing income to supplement the Age Pension, according to new Grattan Institute analysis. It would also contribute to budget repair.

The analysis shows how either of the reform packages proposed by both major parties would be a big step in the right direction. It explores how the current system provides much larger benefits to those with such ample resources that they will never qualify for an Age Pension. And it shows how the proposed changes would affect them – and pretty much nobody else.

As they debate the Coalition government’s proposals to wind back tax breaks on superannuation, politicians on all sides can do three big things: create a better and fairer superannuation scheme; take an important step towards repairing the Commonwealth budget; and show that our political system still works.

Both main parties have laid out their preferred reforms to super tax concessions. While they agree on all but the details, they are yet to strike a deal. Our new research shows what is at stake.

A better, fairer, super system

First and foremost, the proposed reforms to superannuation announced in the 2016 budget are about making super better, and fairer.

Tax breaks should only be available when they serve a policy aim. The purpose of super identified in the budget and due to be defined in legislation is to provide income in retirement to substitute or supplement the Age Pension. Super tax breaks don’t fulfil this purpose when they benefit those who were never going to qualify for an Age Pension in the first place.

The plans of both the government and the ALP would be big steps towards aligning super tax breaks more closely with their purpose. They would trim the generous super tax breaks enjoyed by the top 20% of income earners – people wealthy enough to be comfortable in retirement and unlikely to qualify for the Age Pension.

Retirees with large superannuation balances will start paying some tax on their superannuation savings, but still pay much less tax than wage earners on lower incomes. For a small proportion of women with higher incomes later in life, the changes will reduce their catch-up contributions. Yet the changes will reduce the tax breaks far more for wealthier old men.

Claims that the budget changes will affect many low and middle-income earners are wrong. Our research shows the changes will affect about 4% of superannuants, nearly all of them high-income earners who are unlikely to access the Age Pension. Nor are the proposed changes retrospective. Many reforms affect investments made in the past, and no-one suggests they are retrospective. Rather, the changes will affect taxes paid on future super earnings, and entitlements to make future contributions to super.

Any plausible combination of the packages on offer would make the super system fairer. At present, someone in the top 1% of income earners can expect to receive nearly three times as much in welfare and tax breaks from super in their lifetime as an average income earner. The government’s changes would trim some of these excesses: the top 1% would instead receive just twice as much as low or average income earners. And by targeting tax breaks that go to the top 20% of income earners, neither side’s plan would see much of an offsetting increase in Age Pension spending.

An unsustainable tax system for seniors

Decisions by the former Coalition Government to abolish taxes on superannuation withdrawals in 2007 and radically increase the amount senior Australians could earn before paying income tax have dramatically reduced the tax bills of older Australians.

These changes are one of the main reasons why households over the age of 65 (unlike households aged between 25 and 64) now pay less income tax in real terms today than they did 20 years ago. At the same time, the workforce participation rates and incomes of seniors have jumped. Generous super tax breaks have been funded by deficits. The accumulating debt burden will disproportionately fall on younger households.

Tax breaks to older Australians are also a major cause of the increase in the “taxed nots” identified by Treasurer Scott Morrison. The number of older Australians not paying any income tax has increased from three in four in 2000 to five in six today. The rise of these “taxed nots” coincides with the introduction of the Senior Australian Tax Offset in 2000, and tax-free super withdrawals in 2007.

Repairing the budget

The increased cost of services and reduced taxes per older household explain in large part why the Commonwealth budget is in trouble. For eight years, budget deficits have persisted at about 2 to 3% of GDP, and the future looks little better. The returned Turnbull government is putting a priority on budget repair, now described as a “massive moral challenge” by the Prime Minister. Winding back some of the tax breaks given to older Australians during the happier times of the mining boom is an obvious step.

The government’s super package would save the budget at least A$800 million a year. Alternative proposals by the ALP, which broadly supports the Coalition’s reforms, and then goes further, would save more than A$2 billion a year. Should Treasurer Morrison seek a deal with the ALP or the Greens, any “concessions” will mostly improve the budget position.

Nor is the Turnbull government likely to find more attractive opportunities for budget savings. Unlike most of the government’s savings measures, changes to super tax breaks are broadly popular. Electorates more likely to be adversely affected by the super changes – that is, those with more old and wealthy voters – tended to swing less to the ALP at the last election than other electorates. And a survey before the election showed that the proposals had more support amongst those most likely to be adversely affected.

A test for our political system

Even after the reforms, super tax breaks will still mostly flow to high-income earners who do not need them, and the budgetary costs of super tax breaks will remain unsustainable in the long term. Further changes to super tax breaks will be needed in future. But agreeing to the super package now before the Parliament would be progress in the right direction. And there is a broader issue at stake.

Super is only the first of a number of difficult choices that will come before the Parliament as government seeks to promote economic growth in a sluggish global economy, and bring the budget back under control. There is no easy road to these ends that will keep everyone happy all the time. Pragmatic compromise will be critical.

The proposed changes to super tax breaks are built on principle, supported by the electorate and largely supported by the three largest political parties. If we cannot get reform in this situation, then our political system is in deep trouble. In coming weeks, our MPs have the chance to show how government in Australia can still change the nation for the better.

Authors: John Daley, Chief Executive Officer, Grattan Institute; Brendan Coates, Fellow, Grattan Institute; William Young, Associate, Grattan Institute

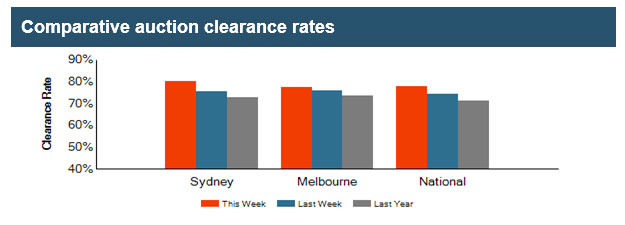

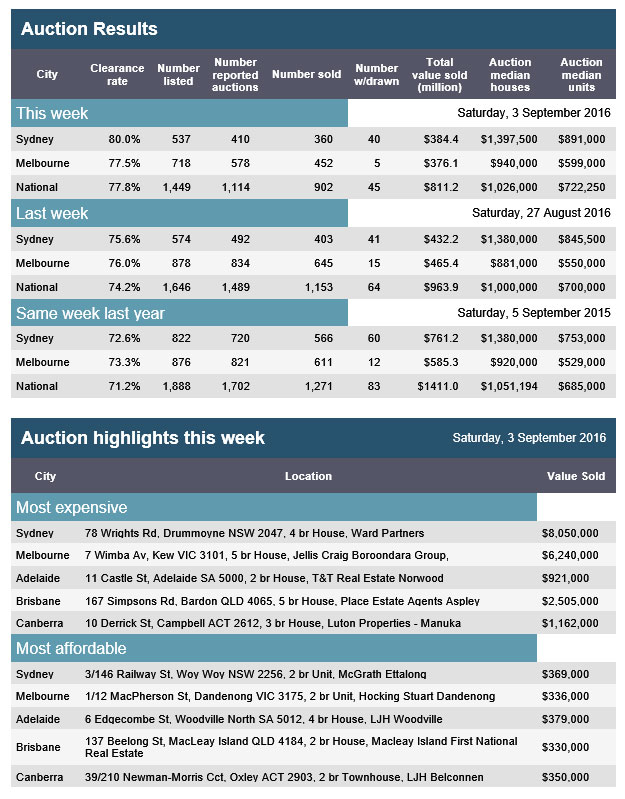

The provisional data from APM PriceFinder for today’s auction clearances shows that once again there is a high sale rate, though on lower listing volumes than this time last year. There is life in the property market still!

In Sydney, 80% of the 537 listings cleared, up from 75.6% last week, and 72.6% last year – though there were 822 on the market then. In Melbourne, 77.5% of the 718 properties sold, compared with 76% last week, and 73.3% last year. Brisbane cleared 55% of the 83 properties listed, Adelaide 74% of 59 properties and 82% of the 52 properties listed in Canberra.

Nationally, the result translates to 77.8% of 1,449 listings, compared with 74.2% of 1,646 last week and 71.2% of 1,888 last year.

As reported in the Globe and Mail, U.S. employment growth slowed more than expected in August after two straight months of robust gains and wage gains moderated, which could effectively rule out an interest rate increase from the Federal Reserve this month.

Nonfarm payrolls rose by 151,000 jobs last month after an upwardly revised 275,000 increase in July, with hiring in manufacturing and construction sectors declining, the Labor Department said on Friday. The unemployment rate was unchanged at 4.9 per cent as more people entered the labour market.

“This mixed jobs report puts the Fed in a tricky situation. It’s not all around strong enough to assure a September interest rate hike. But it’s solid enough to engender a heated policy discussion,” said Mohamed el-Erian, chief economic adviser at Allianz, in Newport Beach, California.

Economists polled by Reuters had forecast payrolls rising 180,000 last month and the unemployment rate slipping one-tenth of a percentage point to 4.8 per cent.

Last month’s jobs gains, however, could still be sufficient to push the Fed to raise interest rates in December. The rise in payrolls reinforces views that the economy has regained speed after almost stalling in the first half of the year.

The report comes more than two weeks before the U.S. central bank’s Sept. 20-21 policy meeting. Rate hike probabilities for both the September and December meetings rose after remarks last Friday by Fed Chair Janet Yellen that the case for raising rates had strengthened in recent months.

Following the report, financial markets were pricing in a 27 per cent chance of a rate hike this month and a 57.7 per cent probability in December, according to the CME Fedwatch tool.

The Fed lifted its benchmark overnight interest rate at the end of last year for the first time in nearly a decade, but has held it steady since amid concerns over low inflation.

The dollar fell against a basket of currencies after the report, while prices for U.S. government bonds rose. U.S. stock futures rose.

“As far as the Fed is concerned, I don’t think it’s a number that is a major setback for what they ultimately want to achieve, which is a slow and gradual pace for a rate normalization,” said Jason Celente, senior fixed income portfolio manager at Insight Investment in New York.

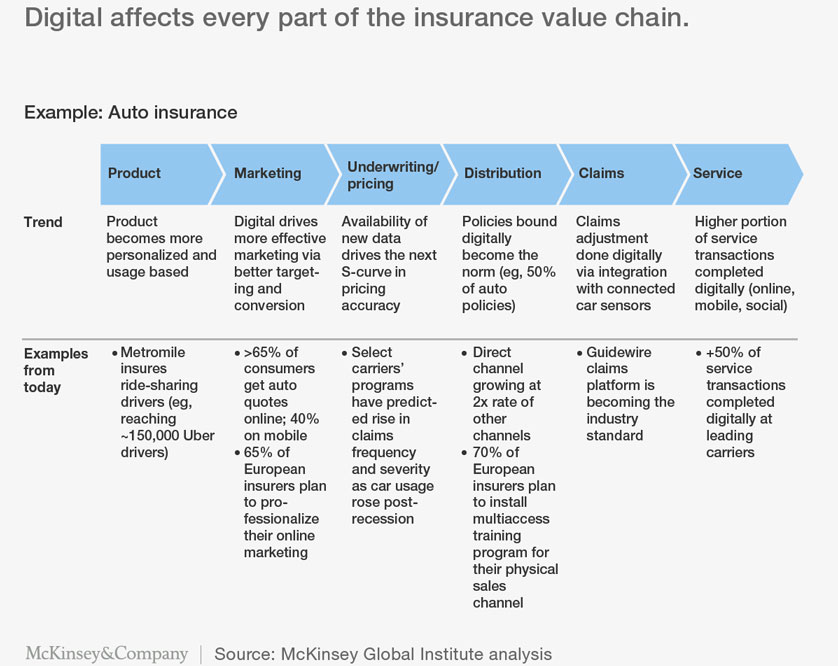

The General Insurance sector is one of the laggards across financial services when it comes to digital transformation. However, according to a new report from McKinsey, whilst the sector lags in digital sophistication and so examples of the full benefits of digital are scarce; they suggest that the top 20 or 30 processes can account for up to 40 percent of costs and 80 to 90 percent of customer activity. Digitizing these processes can take out 30 to 50 percent of the human service costs while delivering a much better customer experience. And the benefits do not end there.

The nature of competition in property and casualty (P&C) insurance is shifting as new entrants, changing consumer behaviors, and technological innovations threaten to disrupt established business models. Though the traditional insurance business model has proved remarkably resilient, digital has the power to reshape this industry as it has many others. Innovations from mobile banking to video and audio streaming to e-books have upended value chains and redistributed value pools in industries as diverse as financial services, travel, film, music, and publishing. As new opportunities emerge, those insurers that evolve fast enough to keep up with them will gain enormous value; the laggards will fall further behind. To succeed in this new landscape, insurers need to take a structured approach to digital strategy, capabilities, culture, talent, organization, and their transformation road map.

Though the P&C insurance business has long been insulated against disruption thanks to regulation, product complexity, in-force books, intermediated distribution networks, and large capital requirements, this is changing. Sources of disruption are emerging across the value chain to reshape:

Products. Semiautonomous and autonomous vehicles from Google, Tesla, Volvo, and other companies are altering the nature of auto insurance; connected homes could transform home insurance; new risks such as cybersecurity and drones will create demand for new forms of coverage; and Uber, Airbnb, and other leaders in the sharing economy are changing the underlying need for insurance.

Marketing. Evolving consumer behavior is threatening traditional growth levers such as TV advertising and necessitating a shift to personalized mobile and online channels.

Pricing. The combination of rich customer data, telematics, and enhanced computing power is opening the door to usage- and behavior-based pricing that could reduce barriers to entry for attackers that lack the loss experience formerly needed for accurate pricing.

Distribution. New consumer behaviors and entrants are threatening traditional distribution channels. Policyholders increasingly demand digital-first distribution models in personal and small commercial lines, while aggregators continue to pilot direct-to-consumer insurance sales. Armed with venture capital, start-ups like Lemonade—which raised $13 million in seed funding from well-known investors including Sequoia Capital—are exploring peer-to-peer insurance models.

Service. Consumers expect personalized, self-directed interactions with companies via any device at any hour, much as they do with online retail leaders like Amazon.

Claims. Automation, analytics, and consumer preferences are transforming claims processes, enabling insurers to improve fraud detection, cut loss-adjustment costs, and eliminate many human interactions. Connected technologies could allow policyholders and even smart cars and networked homes to diagnose their own problems and report incidents. Self-service claims reporting such as “estimate by photo” can create fast, seamless customer experiences. Drones can be used to assess damage quickly, safely, and cheaply after catastrophes. All these disruptions are being driven and enabled by digital advances, as illustrated with examples from auto insurance. No single competitor or innovation poses a threat across the entire value chain, but taken together, they could lead to the proverbial death by a thousand cuts: many small disruptions combining to fell a giant.

Small to medium enterprises (SME) are increasingly relying on commercial credit cards to finance their operations, because payment terms for the businesses they supply are stretching out. But if the Reserve Bank of Australia (RBA) goes ahead with plans to include commercial cards in the new caps on interchange fees, SMEs will be even more hard pressed to make ends meet.

These interchange fees are a major component of the Merchant Service Fees that all Merchants pay on accepting payment cards. Commercial cards are however operated on a different business model to consumer credit cards. For example, commercial cards have much higher credit limits than consumer cards and the flow of interchange revenue from spending on these cards, to the card issuers (usually banks) enables them to take more credit risk and hence extend more credit to SME’s.

The Australian Small Business and Family Enterprise Ombudsman, Kate Carnell has said that, “the majority of small business failures are by far a result of poor cash flow, with slow payments from customers or clients, a leading factor”. She claimed that “the big end of town are delaying payments to those that can least afford it; small-to-medium sized enterprises”.

One example of this is major food businesses Fonterra and Kellogg’s stretching payment terms for suppliers from 90 days to 120 days. The consequences of this are twofold; firstly the large corporations will hold onto money for longer and get positive returns on that, while the SME’s are forced to use expensive overdrafts at banks to fund their ongoing business.

A survey by a UK company MarketInvoice earlier this year, found Australia was the worst offender for late payments, ranking even below countries such as Mexico. Some jurisdictions have however been moving in the other direction; since March 2013 the maximum payment terms in the European Union have been 30 days, unless an agreement is made in writing by both parties, in which case the maximum is 60 days.

To overcome the cash flow challenges that go on along with longer payment terms, many SME’s use commercial credit cards to pay their suppliers and hence take advantage of the up to 55 interest free days (all the major Australian banks issue commercial cards and the interest free periods are up to 55 days) on these cards. SME’s are using commercial credit cards for more than just their cash flow.

These cards can be used to partly finance payments to suppliers, particularly where an SME has struggled to get finance from a bank. SME’s are hence more likely to rely on commercial cards as a source of finance than are larger businesses, which typically can raise capital through a variety of means like bank loans, share issues or corporate bonds.

The reduction in interchange which the RBA is imposing may cause issuers, including banks, to cut costs by reducing credit risk, which would mean less credit extended to SME’s, via commercial cards. Issuers could also find this segment of the credit card market less attractive and hence be less willing to offer this type of credit card to SME’s.

The RBA’s reasoning for including commercial cards ín the proposed maximum 0.80% interchange cap, is there’s not enough evidence to suggest that issuers will stop providing these cards under the cap. The RBA however accepts that “this may involve the introduction of fees on these cards and/or the reduction of the interest free period”.

According to the Australian Bureau of Statistics, as of June 2015, the SME sector employed 68% of Australians and it generated 55% of total income from industry. As larger businesses look to increase the number of days before they settle their invoices from SME suppliers and these businesses face pressure to pay their employee’s wages and utility bills on time, the value of commercial payment cards is all the more obvious.

Less commercial payment cards; with less credit offered on them, at higher interest rates, could well be another unintended consequence of the RBA’s intervention into the payments system.

Author: Steve Worthington, Adjunct Professor, Swinburne University of Technology

It seems that the world has become unsafe for trade agreements. In particular, the Trans-Pacific Partnership (TPP), a major new trade deal among the United States and 11 other Pacific Rim nations, has become a political lightning rod for both the left and the right.

As if to highlight that fact once again, Senate Majority Leader Mitch McConnell said recently that he would not bring the TPP to a vote until after the new president takes office in January.

That’s bad news for the trade agreement – and for President Barack Obama, who sees its passage as the final plank in his foreign policy legacy and who is pushing hard for a vote during Congress’ post-election lame duck session.

But the controversial Asian pact is not the only trade agreement potentially on the chopping block. Last month, the European Union’s trade commissioner, Cecilia Malmström, decided not to fast-track the EU-Canada Comprehensive Economic and Trade Agreement (CETA) due to the anti-trade climate prevailing on the continent.

And France’s President François Hollande just declared that his country would not support moving forward with the gigantic Trans-Atlantic Trade and Investment Partnership (TTIP) being negotiated between the U.S. and the EU. His announcement came on the heels of a statement by Germany’s vice chancellor that TTIP “has failed.”

It seems that every time we get closer to the conclusion and ratification of a trade deal, a new barrier emerges to block any progress. What, then, are we to make of the tremendous obstacles confronting these three major agreements?

McConnell, second from right, has endorsed Trump, who has made anti-trade rhetoric a big part of his campaign.Jim Young/Reuters

The times they are a-changin’

First and foremost, opposition to trade is a sign of the times. The Great Recession, among other events, has generated strong pushback against globalization and liberal exchange, something that seems to have caught political elites around the world off guard.

The Doha Round of the World Trade Organization (WTO) had already come apart well before the recession. Its failure meant that a multilateral deal, one that would have committed nearly all of the world’s countries to the same trade agenda, was no longer possible.

At the heart of Doha’s collapse were the interests of the newly rising BRICS – Brazil, Russia, India, China and South Africa – which could not be reconciled with those of the U.S. and the EU. The failure of the WTO, in its turn, gave new impetus to regional agreements such as TTIP and TPP.

Initially, these regional agreements, along with their more modest bilateral cousins (deals between only two nations), were treated with suspicion by free traders, who feared that they would carve up the global trading system into inefficient blocs. But, in time, such agreements presented themselves as the best, and only, way forward in a more complex, multipolar economic environment.

Still, TTIP and TPP are more than just victims of the general skepticism for globalization that has arisen in the past few years. They are also the collateral damage from political events in the world’s major trading countries.

European Union Trade Commissioner Cecilia Malmström worries about the public opposition to CETA and TTIP.Jason Lee/Reuters

Illiberalism on the rise

First among these is the U.K.’s Brexit vote, which is likely to result in the country’s withdrawal from the EU. Brexit, which is itself the fruit of growing illiberalism in England and Wales, has distracted European leaders to such a degree that TTIP and CETA have moved onto the back burner.

Moreover, in the United States, the success of Donald Trump in mobilizing the anti-globalization working class has made Republicans in Congress, who typically support trade as good for business, wary of trade deals. It has also led Hillary Clinton to distance herself from previous statements supporting TPP made during her tenure at secretary of state.

Another problem facing TPP and TTIP is their unprecedented scope. Not only do these agreements create free trade blocs that encompass much of the world’s economic output, but they also touch on a variety of issues from internet freedom to generic drug prices to the right of private investors to sue states for compensation. Many of the most controversial elements of the agreements relate to these issues rather than to the traditional components of trade protection.

What happens next?

What would be the consequences if these agreements fail?

Economically, the U.S. is already tightly linked with both Asia and Europe. The TPP agreement would essentially expand the Pacific trade bloc beyond NAFTA to include nine additional countries, most significantly Japan. Similarly, TTIP would deepen the already significant economic interdependence that traverses the Atlantic.

The loss of these agreements would certainly have negative economic effects on all sides, as least in the aggregate (since some jobs would be saved by the reduced competition). Agreements this large cannot be jettisoned without consequences.

That said, given the deep connections that already exist among Asia, North America and Europe, the purely economic results of killing the agreements are likely to be important, but not enormous. More serious would be the geostrategic implications.

A rejection of TTIP by either side could signal a reduced U.S. presence in Europe, a particular concern in the face of increasing Russian assertiveness.

Meanwhile, an end to TPP could encourage a number of Asian countries, unsure of America’s future in the region, to move into China’s growing sphere of influence. It is no surprise that this last argument is the one being made most aggressively by the Obama administration.

Long live free trade?

If TTIP and TPP are not likely to be approved any time soon, does this mean that they are already dead?

A President Trump would certainly kill the agreements. If, however, Hillary Clinton becomes the next president, as the polls seem to indicate, their future is harder to predict. Clinton seems to be, at heart, a believer in open markets, but the current political situation makes it hard for her to say so directly.

If elected, Clinton’s statements during the campaign would make it difficult for her to support TPP out of the gate, especially with strong opposition from Bernie Sanders supporters. As envisioned by Cato trade analyst Simon Lester, she may well try to renegotiate a portion of the agreement as political cover and then resubmit it to Congress for approval.

By this point, if Trumpism has been defeated, Republicans may have a greater appetite for foreign trade. The question, of course, is whether the other TPP signatory countries will be willing to reopen portions of the agreement that have already been concluded.

Similarly, in Europe, it seems unlikely that much progress will be made until the Brexit issue is resolved and growth starts to pick up.

Despite all the obstacles, however, I believe that it is important to keep moving forward on free trade. The rejection of these important agreements could risk becoming merely the first step in a gradual erosion of support for the global economic architecture.

This architecture, so carefully created and maintained by the United States after 1945, has contributed mightily to international prosperity and peace. Maintaining it is of critical importance.

Author: Charles Hankla, Associate Professor of Political Science, Georgia State University

Profit-seeking missile. BoBaa22