The Statement on the Conduct of Monetary Policy (the Statement) has recorded the common understanding of the Governor, as Chair of the Reserve Bank Board, and the Government on key aspects of Australia’s monetary and central banking policy framework since 1996.

The Statement seeks to foster a sound understanding of the nature of the relationship between the Reserve Bank and the Government, the objectives of monetary policy, the mechanisms for ensuring transparency and accountability in the way policy is conducted, and the independence of the Reserve Bank.

The centrepiece of the Statement is the inflation targeting framework, which has formed the basis of Australia’s monetary policy framework since the early 1990s.

The Statement has also been updated over time to reflect enhanced transparency of the Reserve Bank’s policy decisions and to record the Bank’s longstanding responsibility for financial system stability.

Building on this foundation, the current Statement reiterates the core understandings that allow the Bank to best discharge its duty to direct monetary policy and protect financial system stability for the betterment of the people of Australia.

Relationship between the Reserve Bank and the Government

The Reserve Bank Governor, its Board and its employees have a duty to serve the people of Australia to the best of their ability. In the carrying out of their statutory obligations, through public discourse and in domestic and international forums, representatives of the Bank will continue to serve the best interests of the people of Australia with honesty and integrity.

The Governor and the members of the Reserve Bank Board are appointed by the Government of the day, but are afforded substantial independence under the Reserve Bank Act 1959 (the Act) to conduct the monetary and banking policies of the Bank, so as to best achieve the objectives of the Bank as set out in the Act.

The Government recognises and will continue to respect the Reserve Bank’s independence, as provided by the Act.

The Government also recognises the importance of the Reserve Bank having a strong balance sheet and the Treasurer will pay due regard to that when deciding each year on the distribution of the Reserve Bank’s earnings under the Act.

New appointments to the Reserve Bank Board will be made by the Treasurer from a register of eminent candidates of the highest integrity maintained by the Secretary to the Treasury and the Governor. This procedure ensures only the best qualified candidates are appointed to the Reserve Bank Board.

Objectives of Monetary Policy

The goals of monetary policy are set out in the Act, which requires the Reserve Bank Board to conduct monetary policy in a way that, in the Reserve Bank Board’s opinion, will best contribute to:

- the stability of the currency of Australia;

- the maintenance of full employment in Australia; and

- the economic prosperity and welfare of the people of Australia.

These objectives allow the Reserve Bank Board to focus on price (currency) stability, which is a crucial precondition for long-term economic growth and employment, while taking account of the implications of monetary policy for activity and levels of employment in the short term.

Both the Reserve Bank and the Government agree on the importance of low and stable inflation.

Effective management of inflation to provide greater certainty and to guide expectations assists businesses and households in making sound investment decisions. Low and stable inflation underpins the creation of jobs, protects the savings of Australians and preserves the value of the currency.

Both the Reserve Bank and the Government agree that a flexible medium-term inflation target is the appropriate framework for achieving medium-term price stability. They agree that an appropriate goal is to keep consumer price inflation between 2 and 3 per cent, on average, over time. This formulation allows for the natural short-run variation in inflation over the economic cycle and the medium-term focus provides the flexibility for the Reserve Bank to set its policy so as best to achieve its broad objectives, including financial stability. The 2-3 per cent medium-term goal provides a clearly identifiable performance benchmark over time.

The Governor expresses his continuing commitment to the inflation objective, consistent with his duties under the Act. For its part the Government endorses the inflation objective and emphasises the role that disciplined fiscal policy must play in achieving medium-term price stability.

Consistent with its responsibilities for economic policy as a whole, the Government reserves the right to comment on monetary policy from time to time.

Transparency and Accountability

Transparency in the Reserve Bank’s views on economic developments and their implications for policy are crucial to shaping inflation expectations.

The Reserve Bank takes a number of steps to ensure the conduct of monetary policy is transparent. These steps include statements announcing and explaining each monetary policy decision, the release of minutes providing background to the Board’s policy deliberations, and commentary and analysis on the economic outlook provided through public addresses and regular publications such as its quarterly Statement on Monetary Policy and Bulletin. The Reserve Bank will continue to promote public understanding in this way.

In addition, the Governor will continue to be available to report twice a year to the House of Representatives Standing Committee on Economics, and to other Parliamentary committees as appropriate.

The Treasurer expresses support for the continuation of these arrangements, which reflect international best practice and enhance the public’s confidence in the independence and integrity of the monetary policy process.

Financial Stability

Financial stability, which is critical to a stable macroeconomic environment, is a longstanding responsibility of the Reserve Bank and its Board.

The Reserve Bank promotes the stability of the Australian financial system through managing and providing liquidity to the system, and chairing the Council of Financial Regulators (comprising the Reserve Bank, Australian Prudential Regulation Authority, the Australian Securities and Investments Commission and the Treasury).

The Payments System Board has explicit regulatory authority for payments system stability. In fulfilling these obligations, the Reserve Bank will continue to publish its analysis of financial stability matters through its half-yearly Financial Stability Review.

In addition, the Governor and the Reserve Bank will continue to participate, where appropriate, in the development of financial system policy, including any substantial Government reviews, or international reviews, of the financial system itself.

The Reserve Bank’s mandate to uphold financial stability does not equate to a guarantee of solvency for financial institutions, and the Bank does not see its balance sheet as being available to support insolvent institutions. However, the Reserve Bank’s central position in the financial system, and its position as the ultimate provider of liquidity to the system, gives it a key role in financial crisis management. In fulfilling this role, the Reserve Bank will continue to coordinate closely with the Government and with the other Council agencies.

The Treasurer and the Governor express their support for these longstanding arrangements continuing.

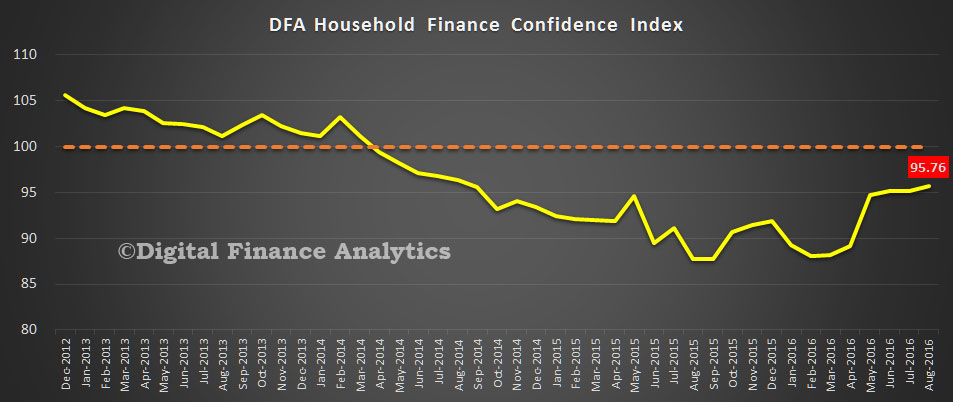

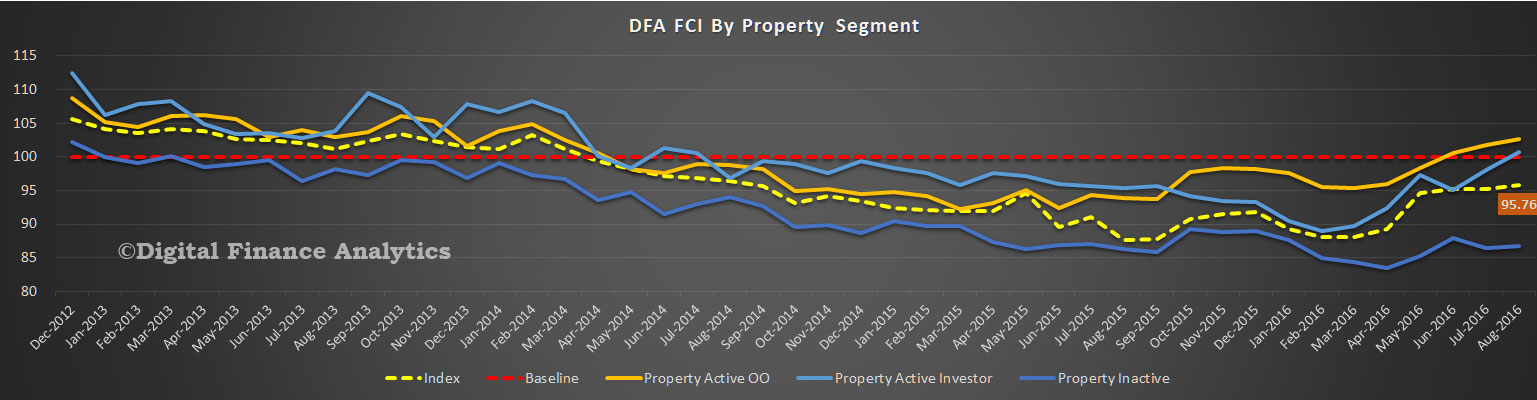

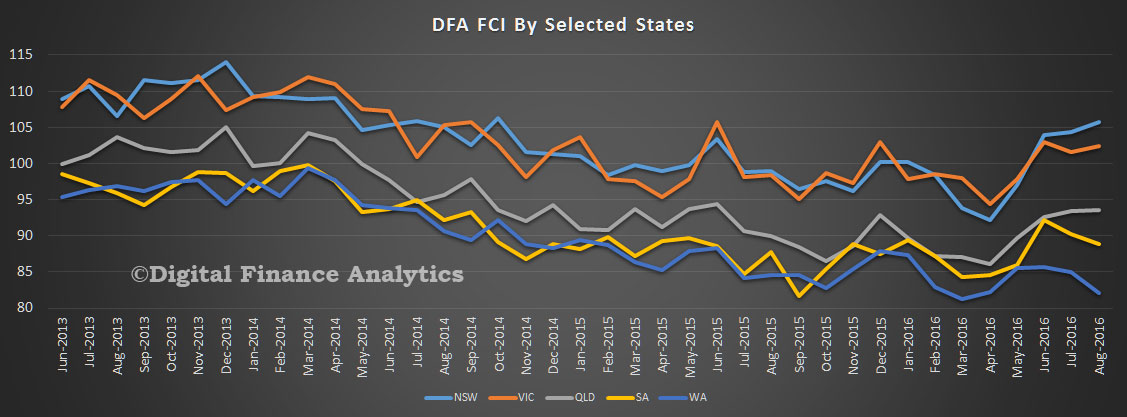

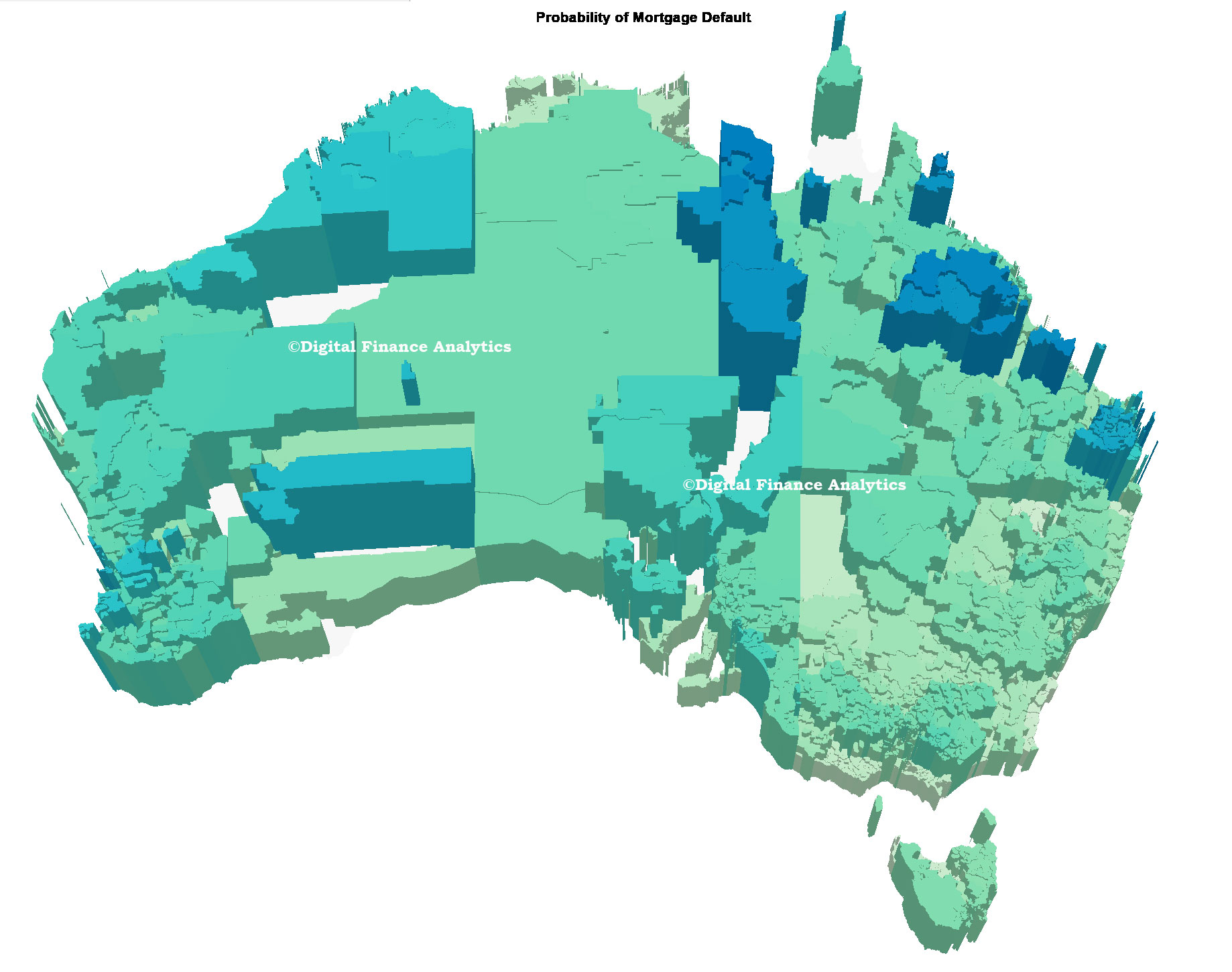

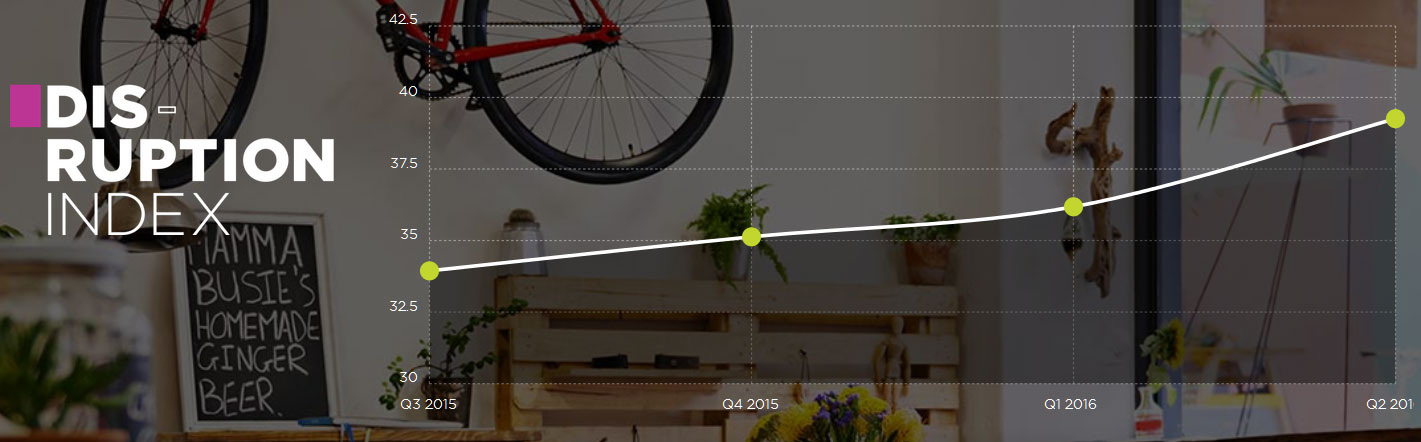

The Disruption Index tracks change in the small business lending sector, and more generally, across financial services. The Financial Services Disruption Index, which has been jointly developed by Moula, the lender to the small business sector; and research and consulting firm Digital Finance Analytics (DFA).

The Disruption Index tracks change in the small business lending sector, and more generally, across financial services. The Financial Services Disruption Index, which has been jointly developed by Moula, the lender to the small business sector; and research and consulting firm Digital Finance Analytics (DFA).