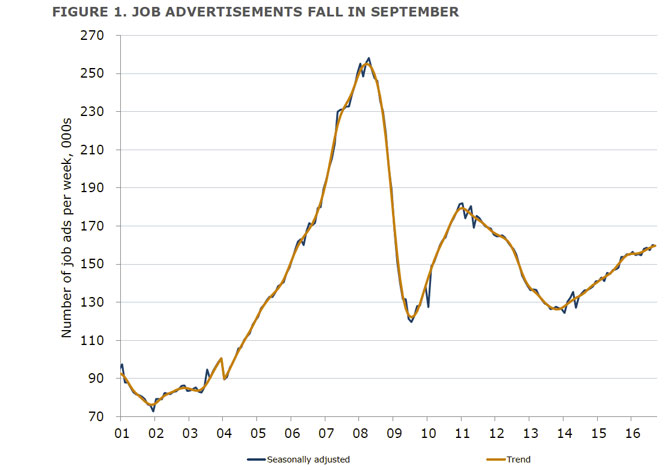

ANZ says after posting a solid gain in August, ANZ job ads edged lower in September.

Job advertisements fell 0.3% m/m in September after a 1.7% rise in August. Annual growth in job ads slowed to 3.7% from 8.0% in the previous month. In trend terms, job ads rose 0.3% m/m and 5.2% y/y. While trend annual growth in job advertisements has slowed, it remains consistent with a gradual improvement in the labour market.

The fall is consistent with some loss of momentum in labour markets this year, and more recently, in surveyed business conditions. It is also consistent with the RBA’s business liaison which reported that some firms had taken a more cautious approach towards hiring.

That said, job ads and still-elevated business conditions continue to suggest that the labour market remains in good shape. Indeed, the rise in job ads over the past three months is consistent with moderate annual employment growth, which should be sufficient to underpin a further decline in the unemployment rate, albeit at a gradual pace

CoreLogic confirms what we saw already, that there was a substantial drop in auction numbers this week due to the grand finals and the Labour Day long weekend.

853 properties were taken to auction last week, with a preliminary clearance rate of 77.5 per cent, compared to the same time last year when there were 865 auctions were held, with a clearance rate of 68.2 per cent. In comparison, over the week before last a total of 2,480 auctions were held with a clearance rate of 75.4 per cent.

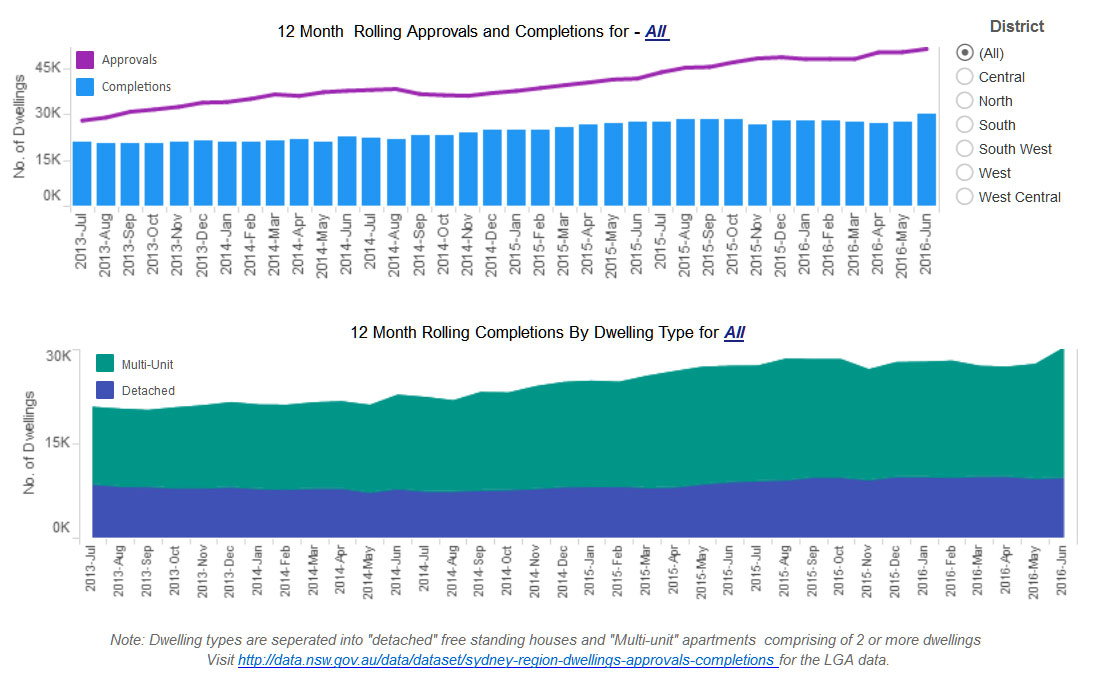

According to data to June 2016 from the NSW Department of Planning & Environment, more than 30,000 new homes have been built in Sydney in the last financial year, the highest figure since the building boom in the lead-up to the Sydney Olympic Games.

The latest figures from the Metropolitan Housing Monitor showed 30,191 new homes and apartments had been finished in the greater Sydney region.

This is the highest number of completions since the 1999-2000 financial year, when 30,520 completions were recorded.

Planning Minister Rob Stokes said the completion numbers were due to the strong local economy, a solid rate of development approvals and the NSW Government’s efforts to release land and build infrastructure to support housing supply.

“More houses being built means more opportunity for Sydneysiders to buy homes across our city,” Mr Stokes said.

“Unprecedented spending on new public transport and roads is helping to address a housing undersupply backlog of up to 100,000 homes. At the same time we’re creating a simpler, more efficient planning system to make it easier to build the homes we need.”

New home completions have increased by ten per cent in greater Sydney over the past financial year. Forty per cent of completed homes are within six local government areas: City of Sydney, Blacktown, Camden, Parramatta, Liverpool and The Hills.

An amusing snip-it. On the day the banks are starting to appear before the economics committee, I noticed the APRA web site was down. Yes, the ADI regulator had disappeared! I wanted to grab some information for analysis I was running. Normal service was resumed just before 11:00 this morning.

Thinking it might be my end, I tried this. Nope, the site was down.

At 8:55am, local time it came back, then went again. At 9:34, we are getting an HTTP Error 503 from APRA. A quick lookup says of 503:

HTTP Error 503 – Service unavailable

Introduction

The Web server (running the Web site) is currently unable to handle the HTTP request due to a temporary overloading or maintenance of the server. The implication is that this is a temporary condition which will be alleviated after some delay. Some servers in this state may also simply refuse the socket connection, in which case a different error may be generated because the socket creation timed out.

Fixing 503 errors

The Web server is effectively ‘closed for repair’. It is still functioning minimally because it can at least respond with a 503 status code, but full service is impossible i.e. the Web site is simply unavailable. There are a myriad possible reasons for this, but generally it is because of some human intervention by the operators of the Web server machine. You can usually expect that someone is working on the problem, and normal service will resume as soon as possible.

It is surely time for governments around the world, including Australia’s, to remember the first law of holes: if you’re in one, stop digging. Governments have been digging madly since the global financial crisis, injecting massive amounts of monetary and fiscal stimulus. It hasn’t worked.

We don’t have much to show for it in Australia – an interest bill of $16 billion on government debt compared with zero before the crisis, and a growth rate and unemployment rate that are struggling to meet long term averages.

The International Monetary Fund (IMF) has repeatedly downgraded its global growth forecasts over the past decade and is about to release another downbeat global growth forecast.

The world economy is in its 6th year of below average growth since 1990. Japan has not grown at all – its GDP in 2016 is exactly at the level it was in 2008 – despite massive amounts of monetary and fiscal stimulus over a decade.

Growth in Europe has remained below 1% every year since 2008, well below its pre-crisis levels, despite the United States Federal Reserve relentlessly pumping new money into the banking system with interest rates already zero. And the US also remains in a funk with growth at 1.5%, less than the 2.5% long run average, having also pumped new money into its banking system and running budget deficits every year that have seen government debt steadily grow as a share of the economy.

Incredibly, the IMF and some governments have not given up. They now accept that perhaps cheap money and plenty of it hasn’t worked, but they still cling to fiscal stimulus as the last great hope as long as it’s the right kind.

According to the IMF, debt-financed government infrastructure spending is the answer – think roads, ports, power and communication networks. They have constructed a mathematical model showing that such infrastructure spending, funded by borrowing, actually reduces the government debt to GDP ratio in a world of low interest rates. This is because it boosts GDP by more than it raises debt, and boosts overall economic wellbeing.

This will be music to the ears of those politicians who want to spend big on infrastructure. It is however a pipedream.

The problem is not so much what the debt is used for, although that does matter, it is more the size of debt itself. Since 2008, government debt has increased in almost all advanced countries as a ratio to GDP.

In the US total government debt has increased from 92 to 125%, in the UK from 63 to 114%, in Japan from 184 to 246%, in Australia from 34 to 65%, and even in relatively austere Germany from 68 to 82%. The combination of rising government debt and booming asset prices (stocks and housing) financed by monetary stimulus is dangerous.

We have seen through the global financial crisis the devastating effects of a collapse in asset prices on the economy, especially on economies with debts whether held by the private or public sector. Indeed it’s this memory that is surely one of the factors currently holding back spending by households and firms.

In this environment, it would be reckless of governments to embark on major fiscal stimulus that raises their debt levels further. The IMF’s model does not take account of the risk of an asset price collapse in a world of high debt and the effect this has on private sector spending.

It needs to be said that the IMF’s model is essentially the same type of model that it uses to forecast GDP growth of countries and which The Economist found had an appalling record of inaccuracy. The Economist team took a sample of 220 instances from 1999 to 2014 where a country went from growth in one year to recession in the next, and found that the IMF had never once predicted the looming recession in its April forecasts of the previous year.

There is at least one prescription to the world’s low growth problem that governments have not yet tried. That is to do precisely nothing – stop digging. We may even discover things about the economy’s restorative powers that we didn’t know, or had forgotten.

A related idea is to actively unwind government intervention where evidence suggests it is not working. It is easy to dismiss such prescriptions as the old-hat 1990s deregulation agenda.

But that was a period of great prosperity in Australia and elsewhere. In any case it’s not about deregulation, but more like what David Cameron in the UK called “better regulation” which was enabled through the Deregulation Act 2015. It is worth noting that growth in the UK has been the strongest in Europe in recent years.

Back to home, the Reserve Bank of Australia should keep its power dry when it meets today and hold its official interest rate steady at 1.5%. And so it should for some time to come.

The Australian government should do the same and not be seduced by the siren call from the IMF and others to spend up big on infrastructure.

Author: Ross Guest, Professor of Economics and National Senior Teaching Fellow, Griffith University

When the chiefs of Australia’s largest banks appear before the Standing Committee on Economics this week it’s likely they’ll be asked about the current level of competition in retail banking.

One of the objectives of competition law in Australia “is to enhance the welfare of Australians through the promotion of competition”. Promoting competition means making sure there is vibrant competition. This means ensuring that competitiveness is enhanced once competition is established.

Reluctance to change

Existing market players generally resist the changes needed to make a sector more competitive. This resistance is driven by the rational fear that a more competitive sector will lead to lower margins and loss of market share.

It seems odd, but in the early days of text messaging it was only possible to send texts to people on the same network. Interconnection of networks was driven partly by commercial opportunity, but mainly by the prospect of regulatory intervention. In mobile telecommunications, mobile number portability was introduced in Australia and elsewhere as a result of similar pressures.

Competition regulators know that competitiveness is higher when it’s easier for a consumer to switch providers. Of course, that does not mean there will be mass switching. Consumers switch when there is a prompt. This might be the end of a contract, or poor (uncompetitive) service from a provider.

Switching banks

In Australia, in common with other parts of the world, switching between retail banks presents hurdles. It’s just a difficult process, even with the help of the bank to which you are switching. A mixture of direct credits, direct debits, mortgage or rent payments and links to credit cards means that switching banks is complex and hard.

One solution to this problem is bank account number portability. The idea is that you can switch your bank without changing your bank account number – just like switching mobile providers.

This could be implemented by having a single independent bank account number database (iBAND), which links account numbers with people. Each bank would then check the iBAND when making a payment as depicted below.

iBANDRob Nicholls

The UK experience

Even this might be a bit more complicated than is needed. The Australian Payment Clearing Association’s “New Payments Platform” offers a range of identifiers for people in addition to bank account numbers. This could also form the basis for portability and switching.

In the UK, the Current Account Switch Service (CASS) is a free-to-use service for consumers to simplify switching current accounts. This service is designed to increase competition, competitive entry and consumer choice.

The consumer education process that accompanied the introduction of CASS in the UK means more than three-quarters of all current account holders are aware of the service.

Data can help

The other issue with switching is knowing whether the deal you will get with the new bank is better. What would be ideal is to have a way of comparing your existing bank or banks and credit card providers with other financial institutions. One way of doing this is by having a standardised form of metadata.

If you wanted to do a comparison, you could download a set of anonymised metadata that described your banking needs. This could then be compared on a platform with other providers.

The UK’s Competition and Markets Authority (CMA), in its final report into the UK retail banking system, suggests that the provision of open banking applications programming interfaces (API) would facilitate such an exchange of data. The broad approach is set out below.

CMA approachRob Nicholls derived from CMA report

The idea is that each bank would present a common interface to external systems through the API. This would allow the banks to create and use apps to enhance the consumer experience. However, it would also allow third parties to be intermediaries or to compare the banks’ offerings.

Switching, innovation and productivity

In its submissions to the Harper review of competition law and policy, CHOICE argued that such a scheme would encourage innovation. The ACCC put the case that “initiatives to allow consumers to effectively use their information … have the potential to assist consumers to make better choices and drive competition”.

The UK government has put consumer switching at the heart of its approach to increasing productivity. It regards this step as critical to open and competitive markets with the minimum of regulation.

Both the Harper review and the Murray inquiry into the financial system found that competition should be at the forefront of regulatory consideration. One way to improve competitiveness in banking is to facilitate both switching and consumer information.

But perhaps the best way to determine whether there is a need to promote competitiveness would be for the ACCC to commence a market inquiry on retail banking. This could have the aim of developing initiatives to stimulate additional competition.

National Australia Bank Limited today announced completion of the sale of 80% of its life insurance business to Nippon Life Insurance Company (Nippon Life) for $2.4 billion.

As previously advised, NAB will retain ownership of 20%of the new life insurance business, and retain full ownership of the existing investments business which includes superannuation, platforms, advice and asset management.

The financial details of the sale will be finalised and reported with the FY16 Full Year Results on 27 October 2016. The key details relating to the transaction are materially consistent with those outlined in the FY15 Full Year Results ASX announcement and Investor Presentation and include:

• Following completion, the transaction is expected to deliver an increase of approximately 50 basis points to NAB’s CET1 capital ratio.

• Goodwill for the Wealth business is expected to reduce by approximately $1.6-$1.7 billion.

• The transaction has resulted in a loss on sale, which is expected to be approximately $1.2-$1.3 billion.

• NAB will retain the MLC brand, although it will be licensed for use by MLC Life Insurance for 10 years and will continue to be used (as is currently the case) in NAB’s superannuation, investments and advice business.

As part of the sale, NAB is also today commencing a long term partnership with Nippon Life which includes a 20 year distribution agreement to provide life insurance products through NAB’s owned and aligned distribution networks.

NAB Group CEO Andrew Thorburn: “From today we move forward with a simpler, clearer wealth model designed to serve our customers better – with continued ability to offer leading life insurance products and services. “We have also streamlined our superannuation business, merging five super funds into one to create Australia’s largest retail super fund. This simplifies our superannuation business, which NAB will retain, and over time makes it easier for customers to access various products and features within the fund as their needs change. NAB has also committed additional investment of at least $300 million over the next four years in our superannuation, platform, advice and asset management business. The combination of these initiatives will allow us to deliver a better and more aligned customer experience”.

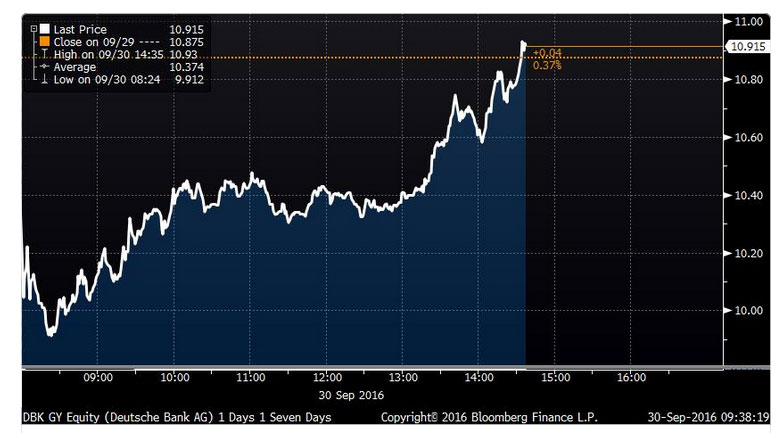

Deutsche Bank is in the news for all the wrong reasons. Some speculators believe that it will be the 2008 Lehman Brothers collapse all over again. Shares in the bank were briefly driven down to single digits. They seem to have stabilised around €10 but this remains well below the €30 just over a year ago and €100 a share in 2007. And the bank’s future is uncertain.

Clearly investors are worried and there is an absence of people who believe even €10 would be a sensible investment. At €10 per share, an investor has a right to €48 of equity. But the problem is whether that €10 will ever be returned to you – let alone with gains. Like many other banks though, Deutsche Bank faces a number of headwinds, which have knocked its profits in recent years.

New regulation since the financial crisis requires that banks must accumulate their profits to create a greater cushion against the risks that became apparent in 2008. This means that the profits that Deutsche will earn over the next few years will be used to increase the size of that cushion rather than being returned to shareholders. Relief is unlikely, as the IMF has identified Deutsche as “the most important net contributor to systemic risks in the global financial system”.

Large well-established banks have a second problem. They have become fat with too many employees juggling outdated, disparate and often dysfunctional IT systems. Deutsche has more than 100,000 employees. Its retail branches – a number of which have been cut this year – are labour intensive and add to these problems.

Dealing with this problem requires reinvesting some of its profits in restructuring its activities – which again means less money for shareholders in the short-run. Failure to do so, however, will create opportunities for new entrants to the banking market such as alternative finance and new fintech operations.

The European Central Bank’s negative interest rate policy is compounding problems. Historically, banks benefited from retail depositor inertia – depositors that park their money in accounts and don’t act upon earning little or no interest. A healthy deposit base ensured a source of zero or low-cost funds that could be lent elsewhere. But the benefit of depositor inertia disappears when interest rates go negative as it costs money to service these customers with extensive retail networks. Imposing user fees is unpopular with customers.

Crisis catalyst and management

These structural issues are well known. The catalyst for the recent action is a US$14 billion fine from the US Department of Justice for mis-selling mortgage bonds a decade ago. Deutsche is looking to negotiate a smaller figure, but if the $14 billion fine sticks the bank could need to raise another €9 billion of equity. At current prices, hapless investors would need to subscribe an additional 60% of their investment to simply hang on to the share of future profits that they expected to receive prior to the fine.

While Deutsche talks confidently of lowering its fine, it is unlikely to attract buyers for its stock. Meanwhile, speculators betting on a decrease in the share price are pushing an open door. Plus, given the dysfunctional nature of eurozone financial regulation, the high political costs of German government intervention and risk of signalling that larger eurozone members play by a different set of rules – the German government will be slow to intervene.

Adding to this complexity, the fine from the US government comes just days after the US$13 billion fine the EU hit Apple with, making some suspicious that there is an element of revenge at play. True or not, the uncertain outcome during the lengthy appeals process will only increase the perceived risks of an investment in Deutsche Bank.

From the sidelines, one would be sympathetic to the CEO’s statement that Deutsche is a strong bank that is being targeted by “forces that want to weaken us”. The bank has assets of more than €1.8 trillion and equity of €67 billion.

As a large, complex entity, it is easy for outsiders to speculate that the bank may be weak, further eroding investor and customer confidence in both the bank and European bank regulation. The coming days will largely determine whether the negative feedback loop between confidence and the stock price can be broken. At worst, the outcome will be significant economic and political difficulties in the coming weeks. At best, it may create a sense of urgency within the eurozone to comprehensively address the banking sector issues that have festered for the past eight years.

Author: Eamonn Walsh, Professor of Accounting, University College Dublin

At the end of last week, shares in Deutsche Bank rebounded somewhat on the rumor that a settlement had been reached with the US Department of Justice. Stock markets followed. However, the rumour has not been substantiated. So how will the markets react now?

… the AFP “story” of a $5.4 billion revised settlement between DB and DOJ was indeed “sources” on Twitter, and had no basis in reality. The reason: not only has John Cryan barely started the negotiations with the DOJ, and is set to arrive in the US this week to beg for mercy, but as the WSJ, which broke the original settlement story more than two weeks ago just reported, Deutsche Bank’s settlement talks with the DOJ are continuing, “with no deal yet presented to senior decision makers for approval on either side.”

The talks are moving forward, but they have “not progressed to a degree that a proposed deal has reached senior-level review at the Justice Department or with Deutsche Bank’s supervisory board, people familiar with the matter said.”

While there is much more information one could hope for in what is now the most important litigation in capital markets, we will gladly take what the WSJ reports over the market-manipulating garbage spewed by AFP with the sole intent of getting both DB and the market to close higher.

Some more details from the WSJ: “People familiar with the continuing settlement talks say details remain in flux. Justice Department lawyers have floated the possibility of also reaching accords with other European banks who have yet to resolve similar investigations and announce them at once, but no such move is certain, the people say.”

The WSJ also adds that CEO John Cryan plans to be in Washington, D.C. this week for meetings of the International Monetary Fund and World Bank. The visit has stoked speculation that he could delve in person into ongoing talks with the Justice Department. The Deutsche Bank spokesman declined to comment on any matters related to talks with Justice Department.

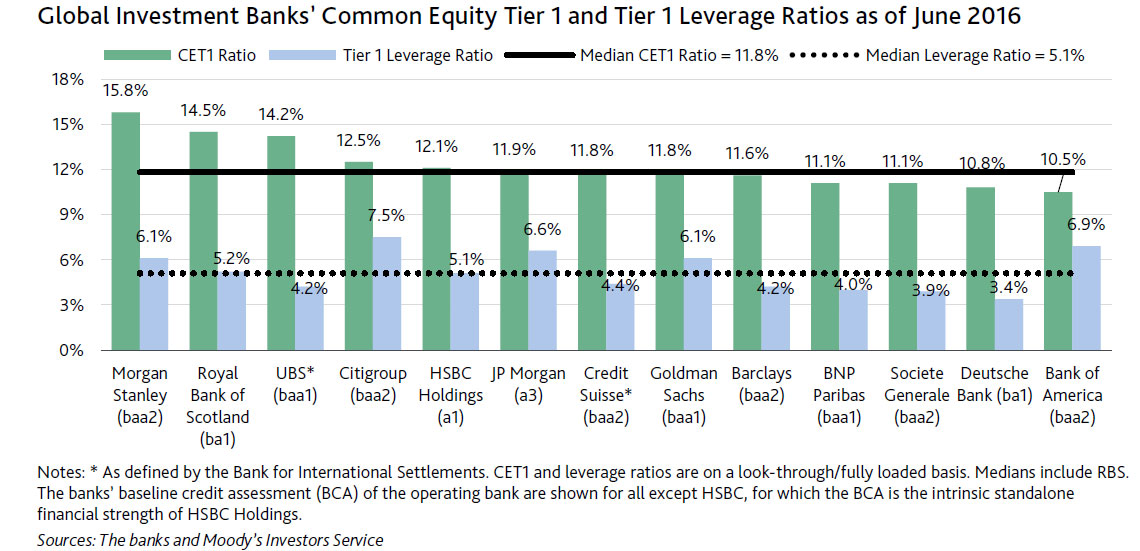

In addition it is worth remembering that DB capital ratios are below many other comparable banks, as this data from Moody’s shows. DB is 3.4% tier 1.

A new off-the-plan property sale platform has been launched to cater for foreign investors who are looking to on-sell their investment via nomination before the settlement date.

Aofun.com.au has launched an online platform that will allow property buyers, who have made down payments on off-the-plan properties, the opportunity to on-sell their investment via nomination before settlement.

The platform is primarily targeted at foreign investors who have been ‘caught out’ by the major Australian banks’ decision to tighten their lending to foreign investors.

Aofun founder and chief executive Jason Zhu said many potential sellers who bought an off-the-plan property in the past few years now have “little or no” chance of securing finance.

He said some of these sellers may be willing to forgo the full 10 per cent deposit.

“There is a real opportunity for first home buyers who may not have sufficient savings for their first home to register on the website and acquire their first home with the deposit paid,” Mr Zhu said.

He added that the Aofun platform allows the original buyers to list their property, and hopeful buyers can make an offer.

“Buyers and sellers can then negotiate the final sale price on the property via the online portal. The sale will then proceed through all the normal legal processes.”

Many original buyers may be willing to sell below the original contract amount to avoid a potential lawsuit from the property developer or to avoid receiving a bad credit rating – factors that “may have negative implications for any future immigration application to Australia or investment in Australia,” according to Mr Zhu.

“The reality facing the market is that many of the overseas buyers of these properties, for various reasons, are not going to able to complete their purchases, leading to an oversupply that will inevitably place a sizable burden on the property and construction industries.”