Great cities and neighbourhoods always have a particular kind of urban intensity – what we might call the “character”, “buzz” or “atmosphere” that emerges over time. While unique in many ways, great cities also have certain things in common. One way to understand these properties is to think about a city’s “urban DMA” – its density, mix and access.

We’re still in the early days of understanding how cities work. But we do know that creative, healthy, low-carbon and productive cities all depend on intensive synergies of density, mix and access.

When we talk about “urban DMA”, we’re talking about the density of a city’s buildings, the way people and activities are mixed together, and the access, or transport networks that we use to navigate through them.

Like biological DNA, urban DMA doesn’t determine outcomes, but establishes what is possible. A low density, largely mono-functional cul-de-sac (such as a shopping mall or a gated enclave) is an anti-urban form. Minimum levels of concentration, co-functioning and connectivity are necessary for any kind of urban life.

The concept of urban DMA can be traced to the work of the late Jane Jacobs, whose book “The Death and Life of Great American Cities” was written in the mid-20th century, when many great cities were being surrendered to cars and poor urban design.

Jacobs wrote of the need for “concentration”, “mixed primary uses”, “old buildings” and “short blocks”. We recognise this as urban DMA – “concentration” is density; “mixed use” and “old buildings” are the conditions for a formal, functional and social mix; and “short blocks” means “walkability” at a neighbourhood scale.

Jacobs’ key contribution was to focus on the city as a set of interconnections and synergies rather than things in themselves – a focus on the city as an assemblage, rather than a set of parts. While the language has evolved, our understanding of these vital synergies needs to be taken much further.

Access

Access is about how we get around in the city. How do we make connections between where we are and where we want or need to be? What are the access routes – are they organised in closed or open networks? How fast are they at different scales and for different modes of transport? How far can we get with a given time frame and with what mix of walking, cycling, car, bus, tram or train?

At a neighbourhood scale access is primarily about “walkability”; at larger scales we depend on a mix of cars, cycling and public transport. But access means nothing if there is nowhere to go – the synergy with density and mix is everything.

Kim Dovey, Author provided

Mix

Mix is about the differences and juxtapositions between activities, attractions and people. It’s not about diversity as spectacle, but a means of enabling encounters and flows between different categories of people, buildings and functions. Mix is about the alliances and synergies between home, work and play; between production, exchange and consumption.

Like density, mix can be uncomfortable; it means proximity to different kinds of people and practices. It means a layering of old and new buildings, of large and small buildings, and of large and small organisations.

Mix is not an unmitigated benefit. Urban planning was largely invented to stop mixing – to prevent living with noise, smells and activities we don’t like. It means keeping where we live away from where we work and shop.

But that separation ceases to be helpful when the result is people living in suburbs with no shops, or working in suburbs with no transport. Great cities will have many different kinds of mix – a “mix of mixes” – each geared in turn to density and access.

There are dangers in an excess of some kinds of density, like the overcrowding of populations and the loss of light and air that comes with excessive building. There are many different kinds of densities – of residents, jobs, buildings, houses and street life. They interconnect, and they all matter.

The big question about density is: how much activity, how many people and how many buildings can be concentrated into one urban area? How close can we live to where we work or need to be? How many urban amenities, places and jobs can we walk or commute to?

Density is not one thing but many and it is the mix that matters.Elek Pafka, Author provided

Urbanity

What is at stake here is the future of this great cauldron of productivity and creativity we call urban life. The 19th century British economist Alfred Marshall famously suggested that there was “something in the air” of a city that made it more economically productive – a phrase that is suggestive of an “atmosphere” and a “buzz” of urban intensity.

Much more than a simple clustering of people and buildings, urbanity is a concentration of intensive encounters and interconnections. And its benefits are much more than economic – they’re social, environmental and aesthetic.

If we want to build great cities, we shouldn’t develop formulae or copies of “best practice” from other cities. We should turn to our existing cities and ask three simple questions:

How dense can we get yet remain liveable?

How mixed can we get while remaining safe and civil? And,

How easily can we get around in a healthy and sustainable way?

Urban planning enables and constrains these dimensions of urban life. And unlike human DNA, urban DMA can be redesigned. If we want a healthy, creative, productive and low-carbon city – if we want “the buzz” – we need to reshape the urban DMA.

Authors: Kim Dove, Professor of Architecture and Urban Design, University of Melbourne; Elek Pafk, Lecturer in Urban Planning and Urban Design, University of Melbourne

Self-employment is on the rise in the UK. The latest government statistics put it at 4.79m, which represents 15% of all people in work. And, in recognition of this changing nature of employment, the prime minister has commissioned a review of workers’ rights. One of its chief tasks is to address concerns that millions are stuck in insecure and stressful work.

Flexible working and self-employment are inevitable solutions to the growing “gig economy”, in order to best manage projects and fluctuating work flows. A flexible lifestyle may be desirable for the highly paid IT consultant. But for the call centre worker on a zero-hours contract, it means a pension, mortgage and income protection are all illusory.

In Tim Ferriss’ book The 4-Hour Work Week, creative freelancers live the dream. They work anywhere, anytime, provided they deliver agreed outputs. And, as social scientist Richard Florida suggests in his view of the “Creative Class”, high-tech workers, artists and musicians typically gravitate to dynamic and open urban regions, with good schools, sporting and shopping facilities. These high-earning creative types then generate jobs for contingent workers whose rights must be protected from abuse. The challenge for urban planners is to attract such talent at both ends of the flexible working spectrum.

Creative class chill.shutterstock.com

Flexibility in self-employment, however, presents a quite different scenario for those with zero-hours contracts. These are increasingly common employment contracts where employers do not guarantee the individual any work and the individual is not obliged to accept any work offered. They are a hot topic for debate, with significant polarisation of views.

The recent investigation into Sports Direct’s use of zero-hours contracts showed them in a particularly negative light and there is talk of the company moving to fixed hours. New Zealand banned these types of contracts in April. And an employment tribunal in London recently ruled that Uber drivers should be classed as workers, rather than self-employed. Yet for some – students, for example – a zero-hours contract is better than no contract at all.

Despite the latest outrages over zero-hours contracts, theories of workplace flexibility have been around for many years. The academic John Atkinson put forward a well-known model for the “flexible firm” in 1984. It advocated that companies retain a core group of workers and use a flexible workforce that is determined by and responsive to business demand.

The model also distinguishes between functional and numerical flexibility. This has long been the operating model in the entertainment industry where the supply of staff is driven by business demand. It is a continuing theme in discussions about employment trends in the fourth industrial revolution.

A business staple

The high-profile coverage of zero-hours contracts might give the impression that they are one of the dominant forms of employment contract in the UK. But, government statistics show that 903,000 people were employed on them during April to June 2016 – this is just 2.9% of all people in employment. They are most likely to be young, part-time, women, or in full-time education. Typically they work 25-hours per week and a third say they would prefer more hours in their current jobs.

Zero-hours contracts, however, are actually less prevalent than other forms of flexible and non-standard employment such as shift work, annualised hours and temporary contracts. And they are only slightly more common than agency work.

In effect, they can be seen as equivalent to the long-established position of a casual contract, something which has been the staple of the business model in the leisure, entertainment and culture industry for years. When work is seasonal, margins are narrow and covering the minimum wage is a challenge for employers, many of whom simply cannot afford surplus staff.

Juggling act

One sector that experiences significant fluctuation in demand is the entertainment business. Blackpool, a seaside resort on the north-west English coast, whose main industry is tourism, is a good example of how difficult it is to get this right. There is a seasonal and school holiday cycle, which introduces one level of fluctuation. Then there are other unpredictable factors that affects the need for staff.

The famously variable British weather affects the relative popularity of indoor and outdoor attractions. And the city is host to a number of events, ranging from major darts competitions, musical acts and theatre productions, to small weddings and functions. The skills required varies significantly too. Whether it’s the annual British Homing Pigeon World Show (January), the world ballroom dancing championships (May), or the annual Rebellion punk reunion festival (August). Flexibility is a daily challenge for many businesses in similar situations.

So, in a world of increasing flexibility and insecurity, we will watch with interest to see the outcome of the government’s review of modern employment. Matthew Taylor who is running it has a wide remit that includes security, pay and rights; progression and training; finding the appropriate balance of rights and responsibilities for new models; representation; opportunities for under-represented groups; new business models. Taylor has said that “most part-time workers, and even most zero-hours workers, say they have chosen to work this way”. Let’s see whether the evidence really bears this out.

Authors: Julie Davies, HR Subject Group Leader, University of Huddersfield; Mark Horan, Senior Lecturer Human Resource Management, University of Huddersfield

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

The global economy is continuing to grow, at a lower than average pace. Labour market conditions in the advanced economies have improved over the past year, but growth in global industrial production and trade remains subdued. Economic conditions in China have steadied recently, supported by growth in infrastructure and property construction, although medium-term risks to growth remain. Inflation remains below most central banks’ targets.

Commodity prices have risen over recent months, following the very substantial declines over the past few years. The higher commodity prices have supported a rise in Australia’s terms of trade, although they remain much lower than they have been in recent years.

Financial markets are functioning effectively. Funding costs for high-quality borrowers remain low and, globally, monetary policy remains remarkably accommodative. Government bond yields have risen, but are still low by historical standards.

In Australia, the economy is growing at a moderate rate. The large decline in mining investment is being offset by growth in other areas, including residential construction, public demand and exports. Household consumption has been growing at a reasonable pace, but appears to have slowed a little recently. Measures of household and business sentiment remain above average.

Labour market indicators continue to be somewhat mixed. The unemployment rate has declined this year, although there is considerable variation in employment growth across the country. Part-time employment has been growing strongly, but employment growth overall has slowed. The forward-looking indicators point to continued expansion in employment in the near term.

Inflation remains quite low. The September quarter inflation data were broadly as expected, with underlying inflation continuing to run at around 1½ per cent. Subdued growth in labour costs and very low cost pressures elsewhere in the world mean that inflation is expected to remain low for some time.

Low interest rates have been supporting domestic demand and the lower exchange rate since 2013 has been helping the traded sector. Financial institutions are in a position to lend for worthwhile purposes. These factors are assisting the economy to make the necessary adjustments, though an appreciating exchange rate could complicate this.

The Bank’s forecasts for output growth and inflation are little changed from those of three months ago. Over the next year, the economy is forecast to grow at close to its potential rate, before gradually strengthening. Inflation is expected to pick up gradually over the next two years.

In the housing market, supervisory measures have strengthened lending standards and some lenders are taking a more cautious attitude to lending in certain segments. Turnover in the housing market and growth in lending for housing have slowed over the past year. The rate of increase in housing prices is also lower than it was a year ago, although prices in some markets have been rising briskly over the past few months. Considerable supply of apartments is scheduled to come on stream over the next couple of years, particularly in the eastern capital cities. Growth in rents is the slowest for some decades.

Taking account of the available information, and having eased monetary policy at its May and August meetings, the Board judged that holding the stance of policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

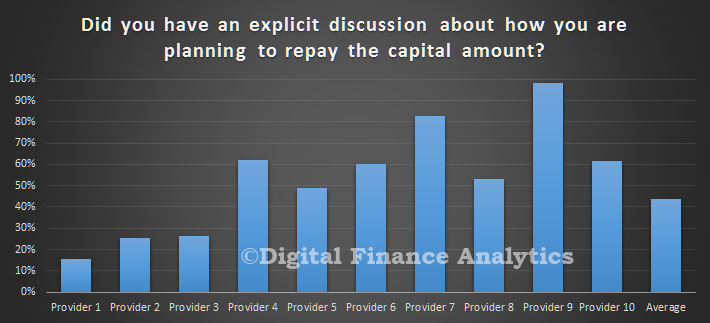

Building on yesterday’s post which discussed the interest-only loan debt trap, today we show that lenders are having quite varied conversations with their borrowers.

We took a cross section of households who have interest-only loans, and mapped their experience to a selection of specific lenders, looking at whether there was, as part of the purchase or refinance discussion, any explicit exploration of how the capital amount was to be repaid. Remember this is looking at the transaction from the perspective of the household, not the lender.

The average is that 43% of households with interest-only loans had an explicit discussion, but whilst some lenders achieved a score above 90%, others were much lower. A wide variation. The policy as set out by APRA is not being universally applied.

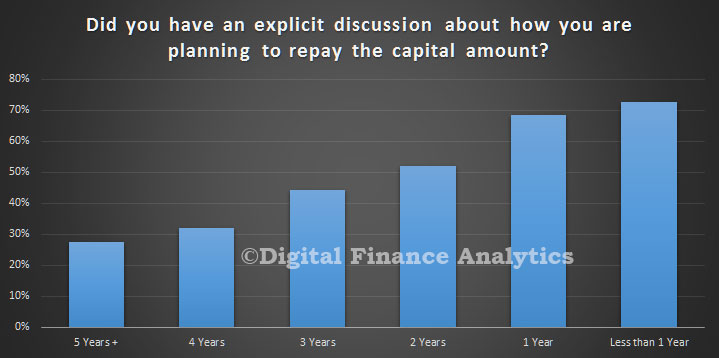

We also found that newer loans are more likely to be funded in the context of an explicit capital repayment discussion, whereas older loans were less likely to include such a discussion. This, we think, reflects lenders reacting the regulator guidance in the past couple of years. But there is clearly more to do.

It also reinforces the point there is a cadre of loans shortly to come to reset and review, where householders suddenly find they are asked some hard questions about capital repayment – perhaps for the first time. If they do not pass muster, an interest-only loan may not be available, forcing them to move to another lender (if available), or different loan structure, where repayments to principle are included. This could get quite nasty.

Should, we ask, lenders be contacting borrowers, outside the review cycle, to preempt the problem? Unless they have a watertight record of an explicit capital repayment discussion, we think they should.

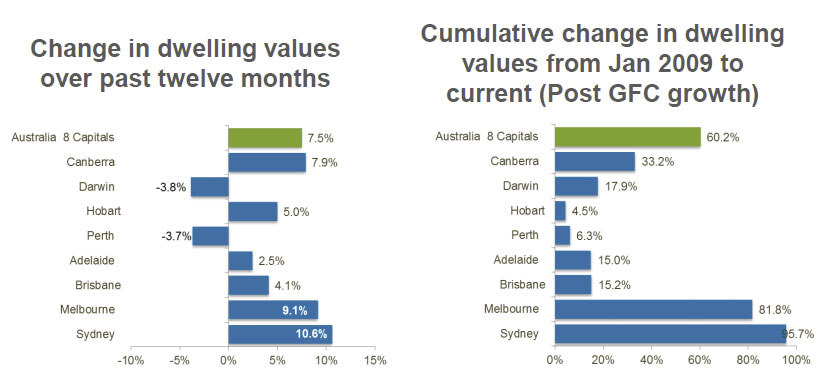

CoreLogic says that capital city dwelling values shift half a percent higher in October 2016 based on their Home Value Index. They have reached a new record high for the month, with values rising across six of the eight capitals.

Apart from Adelaide (-1.3%), Hobart (-2.8%) and Perth (-1.5%), every capital city recorded a rise in dwelling values over the past three months, with the Canberra housing market recording the largest increase in values after a 5.6% quarterly rise.

Sydney continued as the stand out based on annual capital gains, recording the largest year-on-year increase; dwelling values are now 10.6% higher over the past 12 months. Detached houses (+10.9%) are showing only a slightly higher rate of capital gain compared with units (+9.1%) across Sydney, highlighting the healthier supply/demand dynamic that exists across the Sydney region for higher density housing.

The divergence in performance between houses and units is most clearly evident in Melbourne and Brisbane. The annual rate of capital gains in Melbourne remains strong at 9.1%, however there is a substantial difference in growth rates between houses and units, with house values up 9.6% compared with a 5.2% increase in unit values over the past year. Brisbane’s housing market has shown a larger capital gain spread, with house values up 4.7% compared with a 1.4% fall in unit values over the year.

According to CoreLogic, another sign of market strength can be seen in auction results. In fact, over the past two months, clearance rates across Sydney have dipped below 80% only once. A year ago auction clearance rates were consistently trending around the mid 60% range, albeit on volumes that were about 20% lower than last year.

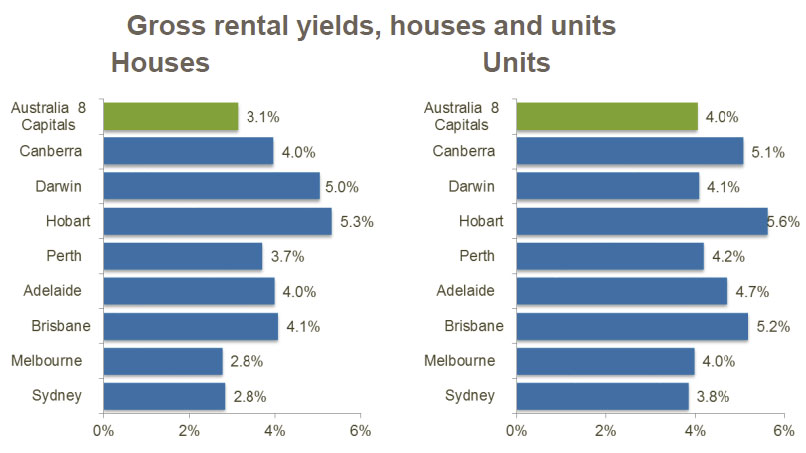

While dwelling values have broadly risen during October, rental yields in Sydney and Melbourne remain depressed, with gross yields at record lows. The typical Sydney and Melbourne house is now providing a gross rental return of just 2.8%. Taking into consideration holdings costs, expenses and vacancy, the net rental yield for houses is likely to be closer to 2% in these markets. Markets where value growth hasn’t been as strong are seeing healthier yield profiles, with Hobart demonstrating the highest gross rental yields of any capital city.

The Commonwealth Bank has long been active in the space of financial literacy – that is, educating young people about the importance of managing money effectively.

Just recently it announced an overhaul to its “Start Smart” financial literacy programs, which aim to teach children about money.

The catch phrase seems progressive but is loaded with assumptions about women, men, their relationships, and their financial choices. This downplays the economic and social reasons why women’s financial opportunities and experiences tend to differ from men’s.

Pay gap in the workplace

It’s a bold ambition when you consider the broader context. According to the Workplace Gender Equality Agency, the highest gender pay gap actually occurs in the financial and insurance services industry, where senior management positions continue to be male dominated and the difference between women’s and men’s earnings is 30.2%.

Further, when comparing Indigenous females to non-Indigenous male workers with median incomes, the reported superannuation gap is 39%.

Such programs, like the one Commonwealth Bank is offering, are based on the assumption that a combination of guest speakers visiting schools and downloadable resources hold the key to improving financial literacy teaching and learning.

Why are banks getting involved?

The federal government has invested millions of dollars and entrusted the Australian Securities and Investments Commission (ASIC) to lead initiatives intended to help children understand finance.

We also have consecutive National Financial Literacy Strategies led by ASIC, that are intended to drive improvements in the way financial literacy is taught and learned in schools.

Consumer and financial literacy has an elevated status across the Australian curriculum, signalling opportunities for interdisciplinary approaches, particularly in mathematics and economics and business.

Financial literacy projects are big business for consultancies. And for banks, manoeuvring under the guises of corporate social responsibility serves to position brands favourably.

The ANZ bank, for example, conducts its Survey of Adult Financial Literacy every three years. This is considered the leading measure of adult financial literacy in Australia.

These strategies are important to them since their houses are not in order. The recent parliamentary inquiry confirmed that the big four banks are troubled by bad behaviour and more effective regulation is needed.

How do children learn about money management?

Children tend to learn about money within their homes in different ways – and those teaching around this area need to be sensitively attuned to this learning.

Children become socialised and oriented to consumer, economic and financial issues through a series of conversations, observations, and experiences – consciously and unconsciously.

Even primary-aged students make surprising, insightful comments that show mature understandings about earning, spending, saving, and sharing money. This is particularly true in disadvantaged communities.

How is financial literacy taught?

Research into financial literacy education in schools – how it is taught and learned – is an emerging field, typically characterised by program trials and evaluations.

Program evaluations tell short term success stories – the rubber really hits the road when students need to apply their learning in the real world down the track.

In 2012, the OECD and Programme for International Student Assessment (PISA) included a Financial Literacy Assessment for 15-year-old students. Australia ranked fifth out of the 18 participating countries and economies.

The findings showed that students in city schools achieved higher scores than students in provincial and remote schools; and non-Indigenous students significantly outperformed their Indigenous counterparts.

Teaching kids about managing money is most effective when classroom tasks are tailored to meet students’ family backgrounds and interests, and occurs at the point of need.

Students enjoy financial problem solving and decision-making experiences that captivate their imagination, challenge them to think, and prepare them for the real world.

Devising financial literacy lessons that create connections between students’ financial literacy learning at home and at school is hard to do without really knowing the local context and students.

Because Australian classrooms are diverse, this stuff rarely comes together “off the shelf”.

Not reaching the most vulnerable communities

The uncomfortable truth is that workshops by so-called finance literacy experts and downloadable teaching and learning resources may not reach and resonate with Australia’s most vulnerable communities.

Planning for financial literacy learning requires an understanding of the school community, interdisciplinary navigation of the Australian Curriculum, and skilful inquiry approaches.

This is what teachers are trained to do, although they need and crave quality professional learning to hone their craft.

When it comes to meeting students’ academic, social and emotional needs on any issue, let’s invest in schools and trust teachers to do what they’re qualified to do.

Authors: Carly Sawatzki, Lecturer, Monash University; Levon Ellen Blue, Research fellow, Griffith University