ABC Lateline carried a segment featuring BrickX, which can either be seen as an innovative way to facilitate housing affordability, or the ultimate in the financialisation of property. You decide!

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

ABC Lateline carried a segment featuring BrickX, which can either be seen as an innovative way to facilitate housing affordability, or the ultimate in the financialisation of property. You decide!

The RBA left the cash rate unchanged again today.

At its meeting today, the Board decided to leave the cash rate unchanged at 1.50 per cent.

There has been a broad-based pick-up in the global economy since last year. Labour markets have tightened further in many countries and forecasts for global growth have been revised up. Above-trend growth is expected in a number of advanced economies, although uncertainties remain. In China, growth is being supported by increased spending on infrastructure and property construction, with the high level of debt continuing to present a medium-term risk. The improvement in the global economy has contributed to higher commodity prices, which are providing a significant boost to Australia’s national income. Australia’s terms of trade have increased, although some reversal of this is occurring.

Headline inflation rates have moved higher in most countries, partly reflecting the higher commodity prices. Core inflation remains low. Long-term bond yields are higher than last year, although in a historical context they remain low. Interest rates have increased in the United States and there is no longer an expectation of additional monetary easing in other major economies. Financial markets have been functioning effectively.

The Bank’s forecasts for the Australian economy are little changed. Growth is expected to increase gradually over the next couple of years to a little above 3 per cent. The economy is continuing its transition following the end of the mining investment boom, with the drag from the decline in mining investment coming to an end and exports of resources picking up. Growth in consumption is expected to remain moderate and broadly in line with incomes. Non-mining investment remains low as a share of GDP and a stronger pick-up would be welcome.

Indicators of the labour market remain mixed. The unemployment rate has moved a little higher over recent months, but employment growth has been a little stronger. The various forward-looking indicators still point to continued growth in employment over the period ahead. The unemployment rate is expected to decline gradually over time. Wage growth remains slow and this is likely to remain the case for a while yet.

The outlook continues to be supported by the low level of interest rates. Lenders have announced increases in mortgage rates, particularly those paid by investors and on interest-only loans. The depreciation of the exchange rate since 2013 has also assisted the economy in its transition following the mining investment boom. An appreciating exchange rate would complicate this adjustment.

Inflation picked up to above 2 per cent in the March quarter in line with the Bank’s expectations. In underlying terms, inflation is running at around 1¾ per cent, a little higher than last year. A gradual further increase in underlying inflation is expected as the economy strengthens.

Conditions in the housing market continue to vary considerably around the country. Prices have been rising briskly in some markets and declining in others. In the eastern capital cities, a considerable additional supply of apartments is scheduled to come on stream over the next couple of years. Rent increases are the slowest for two decades. Growth in housing debt has outpaced the slow growth in household incomes. The recently announced supervisory measures should help address the risks associated with high and rising levels of indebtedness.

Taking account of the available information, the Board judged that holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time.

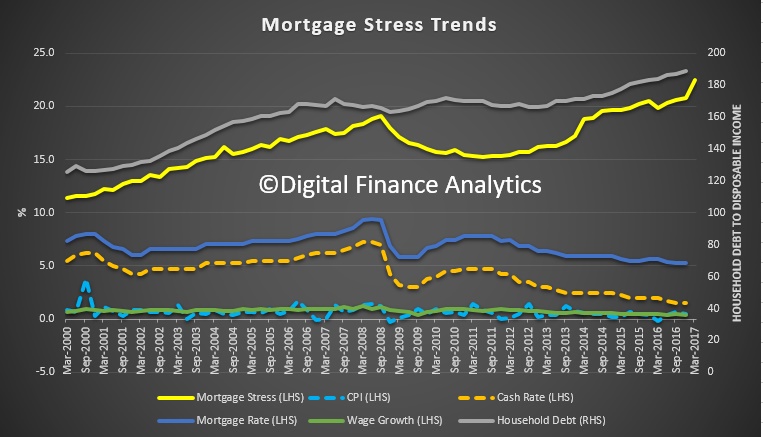

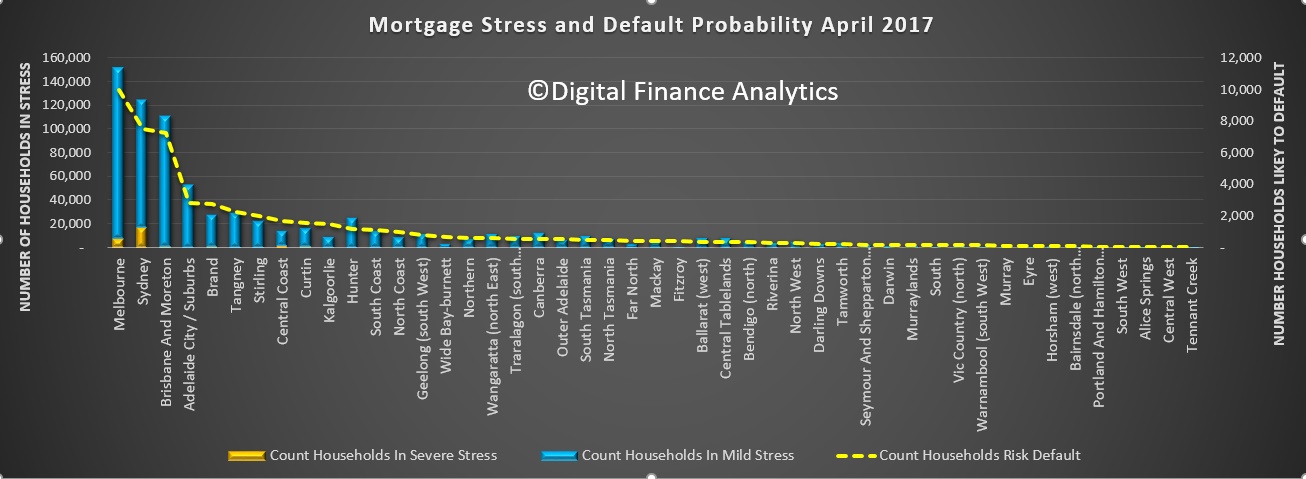

Following the initial release yesterday, and the coverage in the AFR, today we drill down further into the latest mortgage stress results.

By way of background, we have been tracking stress for years, and in 2014 we set out the approach we use. Other than increasing the sample, and getting more granular on household finance, the method remains the same, and consistent. We can plot the movement of stress over time.

Remember that the recent RBA Financial Stability review revealed that 30% of households were under pressure with no mortgage buffer, and a recent Finder.com.au piece suggested more than 50% were unable to cope with a $100 a month rise. So we are not alone in suggesting households are under greater financial pressure.

Remember that the recent RBA Financial Stability review revealed that 30% of households were under pressure with no mortgage buffer, and a recent Finder.com.au piece suggested more than 50% were unable to cope with a $100 a month rise. So we are not alone in suggesting households are under greater financial pressure.

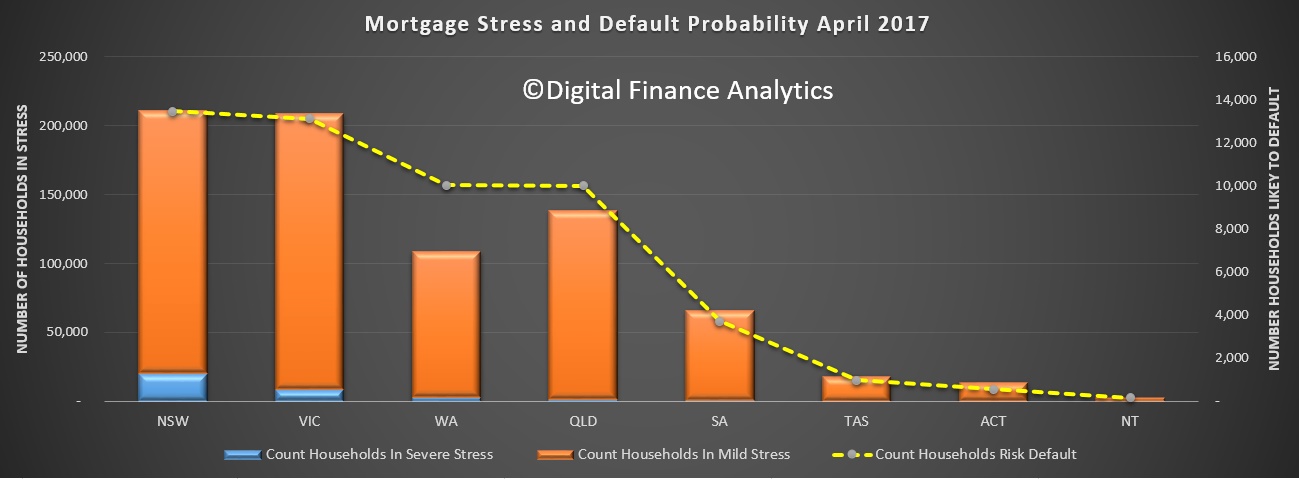

For this analysis we plot the number of households in mild stress (making mortgage repayments on time but tightening their belts so to do); severe stress (insufficient cash flow to pay the mortgage), and also an estimation of the number of households who may hit a 30-day default within the next 12 months. This is calculated by adding in a range of economic overlays into the stress data. This is all done in our core market model, which contains data from our rolling surveys, private data from lenders and other sources, and public data from the RBA, APRA and ABS. This model is unique in the Australian context because it runs at a post code and household segment level, allowing us to drill into the detail. This is important because averaging masks significant variations.

The analysis shows that there are more severely stressed households in NSW than other states, and that around 13,000 households risk default in the next year, a similar number to VIC. WA is third on this list, with the number of defaults lower elsewhere.

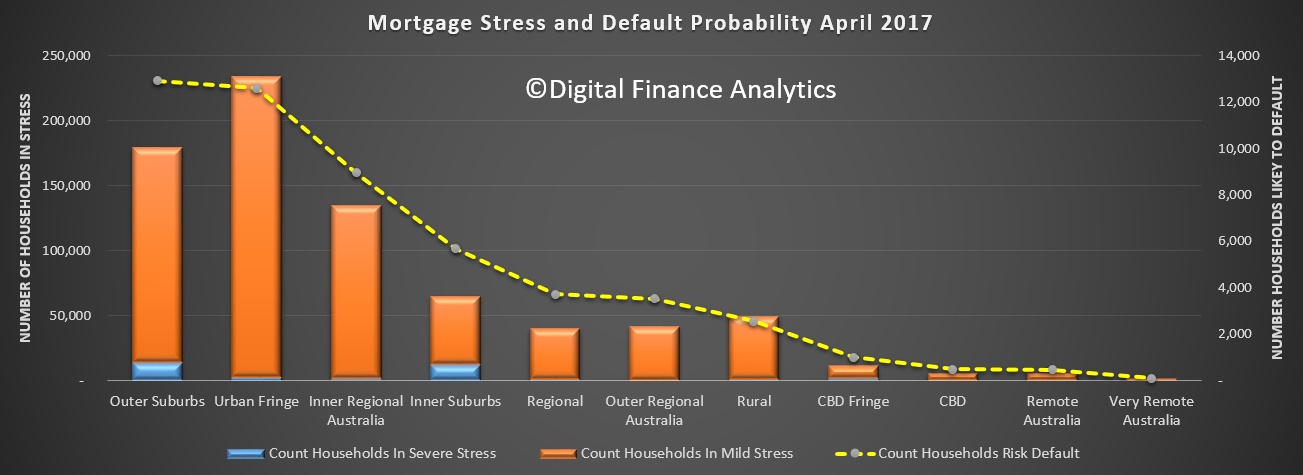

Another lens is by the locations of households, in the residential zones around our major cities. The highest risk of default resides in the our suburbs, where a higher proportion of households are in severe stress. Households in inner regional Australia are next, followed by the inner suburbs, where again more households are in severe stress.

Another lens is by the locations of households, in the residential zones around our major cities. The highest risk of default resides in the our suburbs, where a higher proportion of households are in severe stress. Households in inner regional Australia are next, followed by the inner suburbs, where again more households are in severe stress.

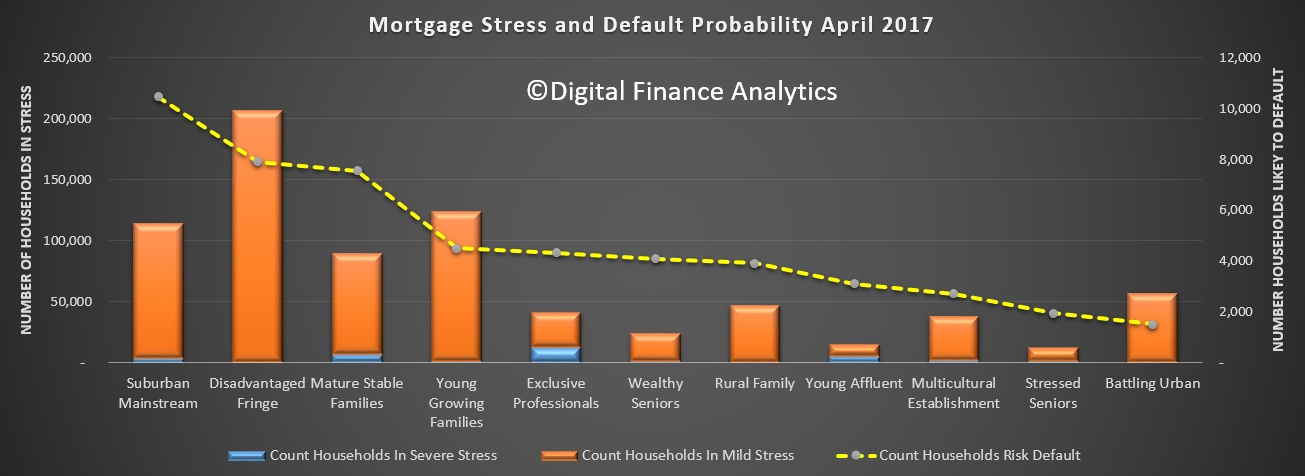

Our core household segmentation shows that the highest count of defaults are likely among the suburban mainstream, then the disadvantaged fringe, followed by mature stable families and young growing families. It is also worth noting that the young affluent and exclusive professional, the two most affluent segments contain a number of severe stressed households. This have larger mortgages and lifestyles, but not necessarily more available cash.

Our core household segmentation shows that the highest count of defaults are likely among the suburban mainstream, then the disadvantaged fringe, followed by mature stable families and young growing families. It is also worth noting that the young affluent and exclusive professional, the two most affluent segments contain a number of severe stressed households. This have larger mortgages and lifestyles, but not necessarily more available cash.

Finally, for today, here is the mapping across the regions. No surprise that the largest number of stressed households are in the main urban centres of Melbourne and Sydney.

Finally, for today, here is the mapping across the regions. No surprise that the largest number of stressed households are in the main urban centres of Melbourne and Sydney.

Next time we will look at post codes across the country.

Next time we will look at post codes across the country.

Yellow Brick Road released their quarterly update to end March 2017.

Operating cash surpluses have improved despite tougher lending market conditions. Higher margins and the benefits of the Company’s rationalised operating structure have delivered improved operating cash surpluses.

This improvement has been achieved despite an 8% decline in settlement volumes, vs Prior Comparable Period (PCP:Q3 FY2016).

The net operating cash result for the quarter was a $0.5m surplus, an improvement of 340% ($0.4m) from Q3FY2016 ($0.1m). Underlying cash trends are positive. Compared with Q3 FY2016, on an underlying basis these trends are:

- Receipts from customers improved 8%.

- Surplus of receipts over direct costs improved by 10%

- Underlying cash outflows increased by 4% due to increased marketing outflows.

Underlying, revenue generating, assets of the business are continuing to grow, for example:

- The Company’s wealth operations continue to gain scale FUM are up by 87% to $1.3b (vs PCP).

- The group book of loans under management grew 19% vs PCP to $42.5b

Recent initiatives by regulators seeking to limit the volume of certain types of lending, including investment loans and interest only loans, have affected the lending market.

The Company has seen lower than expected lending volumes as a result of the changes. To date the reduction has not been sufficient to materially affect the Company’s ability to continue to meet market expectations (a FY2017 full year profit). The medium-term impact of the changes on lending volume is unable to be quantified at this time.

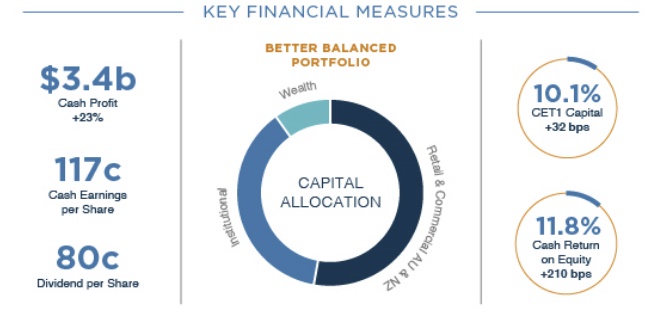

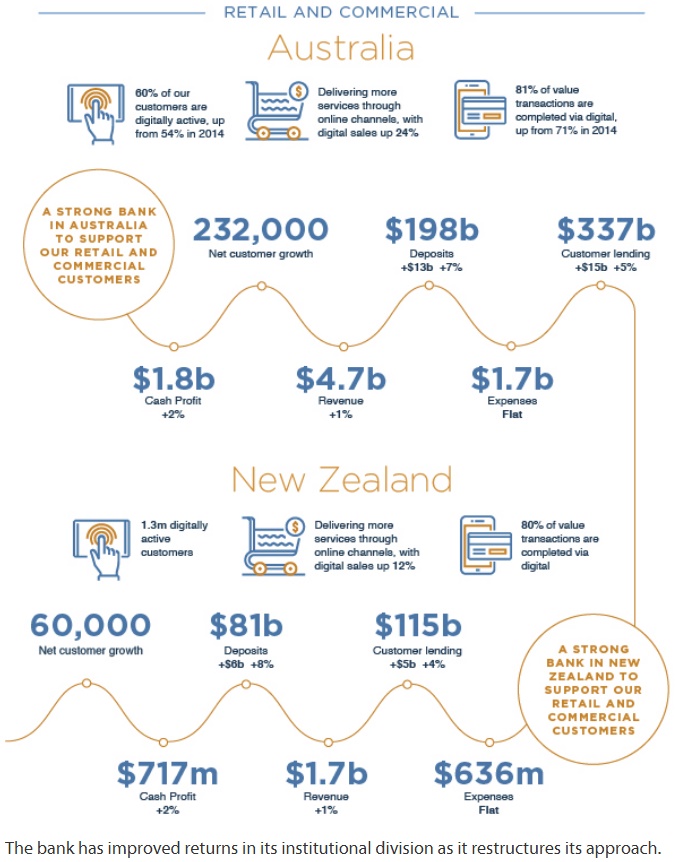

ANZ’s IH17 result, announced today shows the benefit of the consolidation of the business, with more focus on growth in Australia and New Zealand. Profit is up, despite a drop in Group Net Interest Margin, with support from loan and deposit growth, and lower provisions. All well and good so long as the local economy performs!

ANZ today announced a Statutory Profit after tax for the Half Year ended 31 March 2017 of $2.9 billion up 6% and a Cash Profit1 of $3.4 billion up 23% on the prior comparable period (PCP). Cash profit was up 23%.

Group net interest margin fell 7 basis points from 1H16 to 2%.

Group net interest margin fell 7 basis points from 1H16 to 2%.

ANZ’s Common Equity Tier 1 Capital Ratio was 10.1% at 31 March 2017 up 52 basis points (bps) from 30 September 2016. (15.2% on an

Internationally Comparable basis). Return on Equity increased

210 bps to 11.8%.

The total provision charge of $720 million ($787 million individual provision charge and a $67 million collective provision release) equates to

a loss rate of 25 bps, a decline of 11 bps from the end of 2H16. Gross

impaired assets over the same period decreased 7% to $2.94 billion with

new impaired assets down 3%.

Strong organic capital generation performance saw Australian Prudential Regulation Authority (APRA) Common Equity Tier 1 capital ratio above 10% for the first time and Return on Equity increased materially for the

first time since 2010.

The Group has a strong funding and liquidity position with the Net Stable

Funding Ratio at 113% up 5% from 30 September 2016. The improvement

was largely attributable to strong Retail deposit growth in Australia.

The FY17 interim result reflects further benefits from a significant reshaping of the business driven by ANZ’s strategic focus to create a simpler, better capitalised and more balanced bank producing better outcomes for customers and shareholders.

The Interim Dividend of 80 cents per share fully franked, is the same as the Interim Dividend in FY16, reflecting a payout ratio of 69% (Pro Forma 65%).

Highlights include:

Highlights include:

The adoption of Agile at scale continues, with planning is already underway to broaden its roll out in early 2018.

Solving the affordable housing crisis is a high priority for state governments around Australia.

This is understandable given the hyper-inflated property markets in many Australian capital cities. Rising concerns that interest rates will increase over coming years also fuel the unaffordability fires.

Proposed solutions to this crisis often focus on opening up new greenfield areas of land in the outer suburbs to develop lower-cost housing. Hence the solution to the affordable housing process is often thought to lie in creating housing with a low purchase price. This approach incentivises developers and housing suppliers to keep the price of new housing stock as low as possible.

This leads to houses that are more costly to own and maintain. Construction savings on features such as insulation, passive solar design, and heating and cooling systems mean such houses have high energy demands. That, in turn, means ongoing living costs such as the cost of air conditioning remain high for the life of the house.

Such houses are also constructed to the minimum standards dictated by the building codes. Poorer design and lower-quality materials can lead to large deferred maintenance costs and lower resilience to natural hazards.

In addition, housing in the outer suburbs has poorer prospects for capital growth, effectively trapping poorer households on the fringes of our cities. The residents of these suburbs also generally face higher transport costs to get to work and services.

Exposed to future risks

We are, in effect, encouraging new home owners to take on larger future risks and costs just so they can buy a house. This keeps government happy by increasing the number of new home owners – a proxy for affordable housing.

But this approach ignores the issue that home owners increasingly cannot afford to continue to own a home, not just buy one.

Increasingly, the first cost-saving action for struggling home owners is to be uninsured or underinsured. About 14% per cent of people have no home or contents insurance whatsoever.

Of those who are insured, many know they are not adequately covered. Back in 2012 it was identified that around one-quarter of home owners and renters had no insurance cover for house contents. Other estimates suggest that nearly one-third of households in Australia remain uninsured. Other studies more recently concluded that 41% of tenants do not have contents insurance.

Events like the recent Cyclone Debbie remind us just how exposed many families are to natural hazards, including physical damage to assets and the associated emotional hardship.

In many cases, families have been financially wiped out as a result of their lack of insurance coverage. These families then go back onto the long waiting list for affordable social housing.

Therefore, by defining affordable housing in terms of only purchase price of housing and number of new home owners, we are dramatically understating the problem of housing affordability.

By facilitating families to invest in houses that require high energy demands to be liveable, and which are located in areas increasingly exposed to natural hazards while households are uninsured or underinsured, we are simply mismanaging the affordable housing challenge.

Reframing affordability

A key action that can be taken is to frame housing affordability in terms of whole-of-ownership-life costs. This means we move away from defining affordable housing in terms of the initial capital cost and instead consider the total cost of owning a house over the term of ownership.

This approach explicitly encapsulates the risks of under-insurance and higher interest rates.

This is the approach used when funding infrastructure and major utilities assets. When planning major infrastructure, cost-benefit analyses must now consider the whole-of-life costs. This is to account for enthusiastic infrastructure advocates deferring costs through to increased maintenance obligations so the capital costs remains low, and hence the project becomes more attractive.

It’s the same for housing development. Therefore, the same approach needs to be adopted for home ownership.

Digital Finance Analytics has released new mortgage stress and default modelling for Australian mortgage borrowers, to end April 2017. Across the nation, more than 767,000 households are now in mortgage stress (last month 669,000) with 32,000 of these in severe stress. This equates to 23.4% of households, up from 21.8% last month. We also estimate that nearly 52,000 households risk default in the next 12 months.

![]() This analysis uses our core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end April 2017.

This analysis uses our core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end April 2017.

We analyse household cash flow based on real incomes, outgoings and mortgage repayments. Households are “stressed” when income does not cover ongoing costs, rather than identifying a set proportion of income, (such as 30%) going on the mortgage.

Those households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell.

Martin North, Principal of Digital Finance Analytics said “Mortgage stress continues to rise as households experience rising living costs, higher mortgage rates and flat incomes. Risk of default is rising in areas of the country where underemployment, and unemployment are also rising. Expected future mortgage rate rises will add further pressure on households”.

“Stressed households are less likely to spend at the shops, which acts as a drag anchor on future growth. The number of households impacted are economically significant, especially as household debt continues to climb to new record levels. The latest housing debt to income ratio is at a record 188.7* so households will remain under pressure.”

“Analysis across our household segments highlights that stress is touching more affluent groups as well as those in traditional mortgage belts”.

Regional analysis shows that NSW has 211,000 households in stress, VIC 209,000, QLD 139,000 and WA 109,000. The probability of default has also risen, with more than 10,000 in WA, 10,000 in QLD, 13,000 in VIC and 14,000 in NSW. Probability of default extends the mortgage stress analysis by overlaying economic indicators such as employment, future wage growth and cpi changes.

We will look at the data in more detail over the next few days and then drill down to some of the worst hit post codes.

*RBA E2 Household Finances – Selected Ratios Dec 2016.

From The Australian Financial Review.

Record numbers of Australian households face mortgage stress as large loans and rising interest rates start to bite, according to detailed analysis of lending, repayments and household incomes.

![]()

Affluent suburban postcodes feature among an estimated 1000 households a week expected to face mortgage default over the next 12 months, the analysis reveals.

“Debt stress momentum is unprecedented,” according to Martin North, principal of research firm Digital Finance Analytics, who has been doing the survey for more than 15 years.

“This is not just about mortgage battlers. It is also hitting the households with bigger incomes and more leverage. It is worrisome,” Mr North said. Numbers of borrowers in severe distress has increased by about one-third to about 32,000 in the past 12 months, he said.

Concern that 767,000 households – or one-in-four across the nation – are facing financial distress follows last month’s warning by the Reserve Bank of Australia about increasing family “vulnerability” caused by soaring property prices, particularly in Melbourne and Sydney.

Reserve Bank assistant governor Michele Bullock said regulators may be forced to impose even heavier restraints on lenders to prevent the property market becoming the trigger for a disruptive financial crisis, said Reserve Bank assistant governor Michele Bullock.

Ms Bullock conceded that the effect of so-called macroprudential regulations imposed on the banks in 2015 to curb investor lending may be fading.

It also follows the Australian Securities and Investments Commission discovery that about 1.5 million recent loan applications matched minimum financial requirements, triggering concerns about lax lending standards.

Other prudential regulators are warning about the need to control interest-only lending because of concerns borrowers’ lack strategies for repaying principals, increasing vulnerability to financial stresses.

Digital Finance Analytics’ report is based on information from 52,000 household surveys and public data from the Reserve Bank of Australia, Australian Bureau of Statistics, Australian Prudential Regulation Authority and information from lenders and aggregators, which are companies that act as intermediaries between mortgage brokers and lenders.

Households are “stressed” when income does not cover ongoing costs, rather than identifying a percentage of income committed to mortgage repayments, such as 30 per cent of after-tax income.

Those in “severe distress” are unable to meet repayments from current income, which means they have to cut back on spending or rely on credit, refinancing, loan restructuring or selling their house.

Mortgage holders under “severe distress” are more likely to seeking hardship assistance and are often forced to sell.

“Stressed households are less likely to spend, which acts as a drag anchor on future economic growth,” said Mr North. “The number of households impacted are economically significant, especially as household debt continues to climb to new record levels.”

However lenders would be expected able to ride out a spike in arrears because they can foreclose on properties whose value has been inflated by unprecedented price growth.

State government budgets in the nation’s most populous states and territories have been boosted significantly by stamp duty charged on property transactions.

About 32,000 households are in severe distress, the analysis reveals. An additional 10,500 households in the suburban mainstream are in risk of default.

Other vulnerable community segments at risk of default include young growing families, the highly leveraged young ‘affluent’.

Most lenders are increasing rates for investors and toughening lending terms and conditions by increasing deposits and demanding more evidence that loans can be comfortably serviced by borrowers.

Commonwealth Bank of Australia, Westpac, National Australia Bank and Australian and New Zealand Banking Group have all raised investor rates in recent weeks.

Lenders are describing their strategy of slugging interest-only investors and easing pressure on principal and interest borrowers as the “new normal” because it differentiates between classes of borrowers as directed by regulators.

Sydney home values remained unchanged in April, adding to a string of a data that points to a slowdown in property prices in the Australia’s largest city.

The April results mark the weakest monthly change in dwelling values in Sydney since December 2015 had a 1.2% fall, data from research firm CoreLogic showed today.

Apartment values fell 1.2% in Sydney last month. Melbourne values inched up 0.5%, while the increase across all capital cities was a mere 0.1%, the slowest pace in 15 months, the data showed.

The latest figures add to tentative signs of easing in Sydney, where prices have more than doubled since January 2009, prompting the Reserve Bank of Australia to voice concerns of financial stability risks and the banking regulator to tighten lending norms.

While the weekend’s new figures will be released later today, auction clearance rates in Sydney slipped last week, while growth in investor home loans, the primary drivers of the market, climbed at the slowest pace in six months.

This table shows the changes in dwelling values

“The softer results should also be viewed against a backdrop of an ever evolving regulatory landscape s which is firmly aimed at slowing investment and interest-only mortgage lending,” Tim Lawless, head of research at CoreLogic said. “The higher cost of debt, as well as stricter lending and servicing criteria, has likely dented investment demand over recent months.”

And this one points to the housing boom in Sydney and Melbourne

The Australian Prudential Regulation Authority last month directed banks to limit the flow of new interest-only lending to 30% of total new residential mortgage lending, as well as placing strict internal limits on the volume of interest-only lending loan-to-value ratios. It also urged banks to to restrain lending growth in higher risk segments and apply prudent buffers in assessing loan eligibility.

The 30% limit on interest-only loans, which are favoured by investors, compares to about 40% of all new mortgages now, a level that APRA said was quite high by international and historical standards.

While tighter lending can dent demand in Sydney, where more than half the new mortgage demand is from investors, CoreLogic cautioned against calling a peak after just a month of “soft results.”

“April, in particular, coincides with seasonal factors including Easter, school holidays and ANZAC day long weekend,” Lawless said.

Any measures in the federal budget aimed at housing affordability will have little impact on getting more people owning their own homes, according to latest budget monitor report from Deloitte Access Economics.

The concept of home and all that it means will come into focus at the federal budget next week with treasurer Scott Morrison indicating he will take action to increase home ownership.

The key questions are why housing has become so expensive and what can be done to get young people back into the market, especially in Sydney and Melbourne where prices have skyrocketed.

Nationally, house prices have risen 12.9% over the last year, with hot spot Sydney jumping almost 20%, according to the latest numbers.

Deloitte Access Economics blames record low interest rates.

“Affordability is through the floor because interest rates are through the floor,” according to the budget monitor report, led by respected budget forecaster Chris Richardson.

Deloitte Access Economics says politicians are increasingly pretending “they” can do something about it.

“Housing affordability is stunningly important … today’s housing prices are dangerously dumb, especially so in Sydney,” says Deloitte Access Economics.

Among the measures the federal government could announce in the 2017 budget are cutting the capital gains tax discount and supporting capital raising for social housing.

“But the likely impact of any of these on affordability would require a microscope to observe,” says Deloitte.

“Yes, there’s good policy there and much that we’d support,” says Deloitte.

“But affordability is rotten because interest rates have never been lower.”

Deloitte says each percentage point increase in interest rates would strip some 7% off average housing prices.

Here’s how mortgage rates have fallen over the last three decades:

Source: Deloitte Access Economics

Source: Deloitte Access Economics“If politicians, state and federal, are leaving punters with the impression that they can solve housing affordability, then they’re leading us down the garden path,” says the budget monitor report.

“And that’s unfortunate, because the electorate is already incredibly disappointed in the ability of politicians to deliver anything.”

Shane Oliver, head of investment strategy and chief economist at AMP Capital, notes that the government is now playing down what it can deliver on housing affordability.

“Maybe a few fiddles to encourage downsizing but since the big issue is supply and that is a state issue there is not really much it can do,” he says.