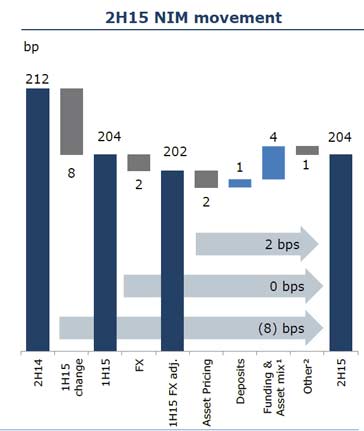

ANZ has announced a statutory profit after tax of $7.5 billion up 3% and a cash profit of $7.2 billion up 1%. The second half profit was down on expectations. On a cash profit basis, income was $14.6 bn, up 4.8% on FY14, and expenses were $9,4bn, up 6.8% on FY14. In the second half of the year, revenue grew only 1.5% whilst expenses lifted 3.8%, and 2H provisions were also higher. Customer deposits grew 10% with net loans and advances up 9%. Return on Equity (RoE) was 14.0%. Overall net interest income grew 5.9%, (a mix of rising volumes +9.3%, and falling NIM -4.2%). Group net interest margin fell 2H14 of 212 basis points to 204 basis points, thanks to loan discounting and FX impacts, despite higher returns from deposits and improved funding mix. However, NIM was more stable in the second half.

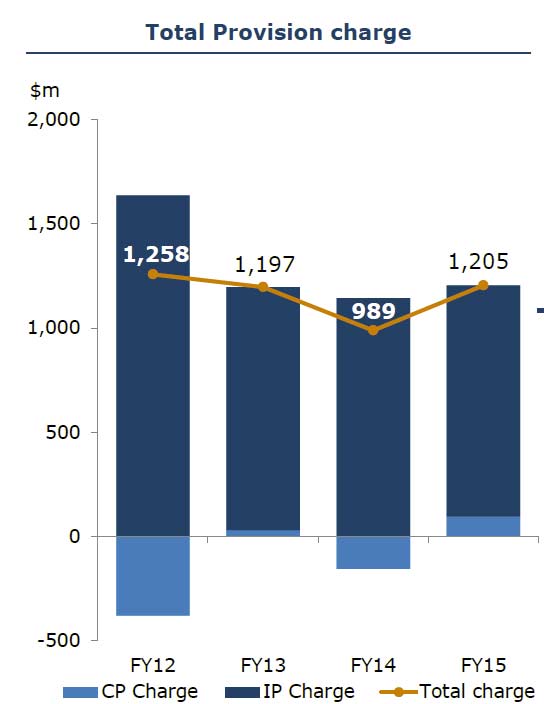

Gross impaired assets decreased 6% over the course of the year. While the total provision charge increased to $1.2 billion or 22 bps, loss rates remain well under the long term average having risen from their historically low levels. However, second half provisions were higher. The individual provision charge declined $34 million and while the collective provision charge increased it remained low in absolute terms at $95 million compared to a net release the prior year. During FY15 the movement in the risk profile component of the charge reflected moderating economic activity with a lower number of credit downgrades being recorded whereas the prior year saw a higher level of upgrades.

Gross impaired assets decreased 6% over the course of the year. While the total provision charge increased to $1.2 billion or 22 bps, loss rates remain well under the long term average having risen from their historically low levels. However, second half provisions were higher. The individual provision charge declined $34 million and while the collective provision charge increased it remained low in absolute terms at $95 million compared to a net release the prior year. During FY15 the movement in the risk profile component of the charge reflected moderating economic activity with a lower number of credit downgrades being recorded whereas the prior year saw a higher level of upgrades.

Final Dividend 95 cents per share (cps) fully franked. Total Dividend for the year 181 cps up 2%. Earnings per share was flat at 260.3 cents, reflecting increased shares on issue following the capital raising in the second half.

Final Dividend 95 cents per share (cps) fully franked. Total Dividend for the year 181 cps up 2%. Earnings per share was flat at 260.3 cents, reflecting increased shares on issue following the capital raising in the second half.

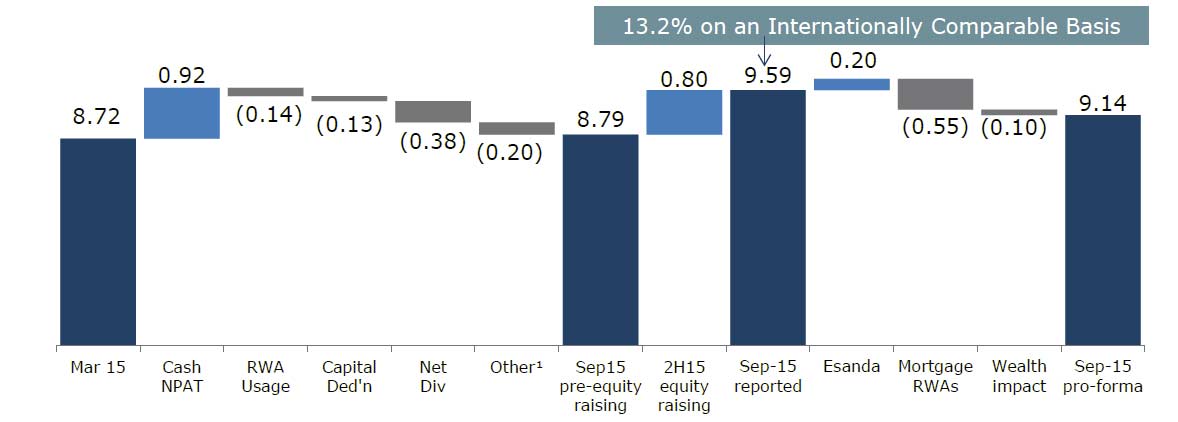

At the end of FY15 the Group’s APRA CET1 ratio was 9.6%, up 87 basis points (bps) from March 2015. On an Internationally Comparable basis the CET1 ratio was 13.2%, placing ANZ within the top quartile of international peer banks. The completion of the sale of the Esanda Dealer Finance portfolio will deliver a further 20 bps of CET1.

ANZ raised a total of $4.4 billion of new equity throughout the past year, including $3.2 billion in response to APRA’s increased capital requirement for Australian residential mortgages which applies from July 2016. ANZ expects the APRA CET1 ratio to remain around 9% post implementing the mortgage RWA change next year. The Group continues to retain significant capital management flexibility to progressively adjust to further changes in regulatory capital requirements if required.

ANZ raised a total of $4.4 billion of new equity throughout the past year, including $3.2 billion in response to APRA’s increased capital requirement for Australian residential mortgages which applies from July 2016. ANZ expects the APRA CET1 ratio to remain around 9% post implementing the mortgage RWA change next year. The Group continues to retain significant capital management flexibility to progressively adjust to further changes in regulatory capital requirements if required.

Segmentals

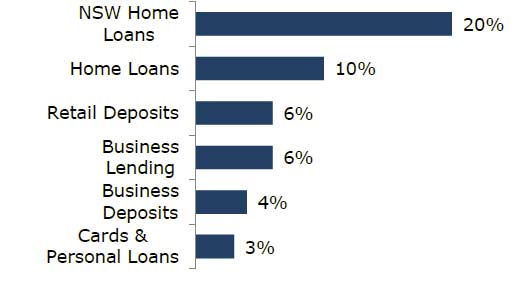

The Australia Division continued its trend of cash profit improvement with profit and PBP growth of 7%. The result was driven by growth in customer numbers (to 5.3 million) along with increased product sales and market share. Cash profit rose 7.2% and impaired assets fell from 0.43% in 2014 to 0.38% in 2015. However NIM fell 2 basis points. Investment focused on digital platform enhancement, increasing distribution sales capacity and capability, growing presence in particular in New South Wales (NSW), a high growth market where ANZ has historically been underweight, and building out specialist propositions in key sectors of Corporate and Commercial Banking (C&CB). Lending grew 9% with deposits up 5%. Sales performance has been strong, particularly in Home Lending, Credit Cards and Small Business Banking. ANZ has grown home lending market share consistently now for six years driven by capability and capacity improvements in branches, online, in ANZ’s mobile lender team and improved broker servicing. Home loans went from $209bn in 2014 to $231 in 2015.

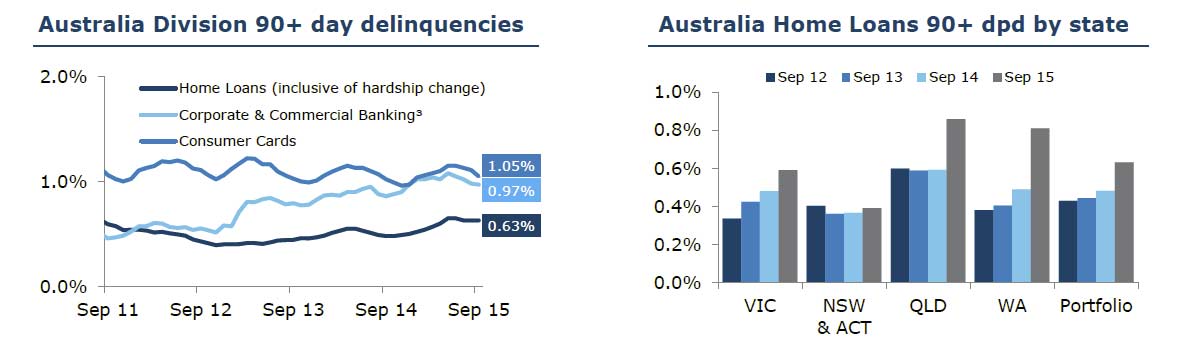

Excluding non=performing loans, home loan delinquencies 90day+ sit at 0.63%, with higher rates in QLD and WA.

Excluding non=performing loans, home loan delinquencies 90day+ sit at 0.63%, with higher rates in QLD and WA.

ANZ’s C&CB business grew lending by 6% despite patchy sentiment in the Commercial sector, with Small Business Banking performing particularly strongly, up 12%. Increased specialist capability saw lending to the Health sector up 16% in the second half. ANZ has seen strong commercial outcomes from its investment in digital capability with increased numbers of customers engaging with the business via digital channels. In FY15 sales via digital channels grew 30%, new to bank goMoney customers grew 89% and product purchases on mobile devices increased 121%.

International and Institutional Banking cash profit declined 1.6% from $2.7 bn in 2014 to $2.66 bn in 2015. NIM fell from 1.5% in 2014 to 1.34% in 2015. While it has been a challenging year for the business they continued to develop the customer franchises in Asia, New Zealand and Australia with particularly good outcomes in Asia. Customer sales in higher returning products demonstrated good growth with cash deposits up 11%, commodities sales up 44% and rates sales up 32%. Global Markets customer income continued a pattern of steady year on year (YOY) increases, up 7%. Despite a strong performance over the nine months to the end of the third quarter, changed financial market conditions in the last six weeks of the fourth quarter caused significant dislocation and a widening of credit spreads, which particularly impacted trading income as well as suppressing sales. This meant total Global Markets income finished the year down 2%. A multi-year investment in the high returning Transaction Banking Cash Management capability has seen Cash Management deposits up 48% over the past three years. Similarly investment in Global Markets product, technology and customer sales capability has driven good outcomes with Foreign Exchange income up 24% over the past three years to represent 42% of the book. IIB has been refining key business areas. Reduced exposure to some lower returning areas of the Trade business, while lowering Trade income slightly, has improved returns. In the Global Loans business, increased focus on RWA efficiency over the course of the second half saw profit decline but margins and returns on RWA begin to stabilise.

New Zealand Division cash profit grew 3% with PBP up 7%. NIM fell 1 basis point in the year. Ongoing business momentum is reflected in balance sheet growth which along with capital and cost discipline (costs +2%) has grown returns. While underlying credit quality remains robust and gross impaired assets continued to decline from 0.61% in 2014 to 0.35% in 2015, a lower level of provision write-backs YOY saw the provision charge normalising although remaining modest at $59 million. Lending grew 8% with deposits up 14%. Brand consideration remains the best of the top four banks, strengthening further. In turn, this is translating into lending demand with ANZ now the largest mortgage lender across all major cities. ANZ has grown market share in key categories during the year including mortgages, credit cards, household deposits, life insurance, KiwiSaver and business lending. The Commercial business grew strongly across all regions with lending up 8%. ANZ increased investment in digital and in sales capability. Sales revenue generated from digital channels increased 32%. A focus on delivering a great digital experience for customers has seen ANZ’s mobile banking app ‘goMoney’ consistently scoring above 98% in customer satisfaction and, with over half a million customers, it is the most downloaded banking app in New Zealand.

The Global Wealth Division increased profit by 11%. Positive performance was experienced across all business units. Insurance delivered growth in in-force premiums along with stable claims and lapse experience, which contributed to an 18% increase in both embedded value and in the value of new business. Private Wealth continued to deliver growth through customer focused investment solutions – with FUM increasing 22% and customer deposits 33% YOY. Global Wealth continues to reshape the customer experience through new digital solutions. Recent innovations include ‘Advice on Grow™’, new tools improving the advice experience, while ‘Insurance on Grow™’ will soon be released to the market. ANZ Smart Choice Super leads the industry in value for money and innovation. FUM now exceeds $4.3 billion and for the second year ANZ Smart Choice received the prestigious Super Ratings Fastest Mover award. ANZ KiwiSaver continues to build its market position with FUM growing 32% to A$7 billion. Global Wealth’s focus on improving customer experience is reflected in the increased sale of Wealth solutions through ANZ channels with growth of 8% YOY.

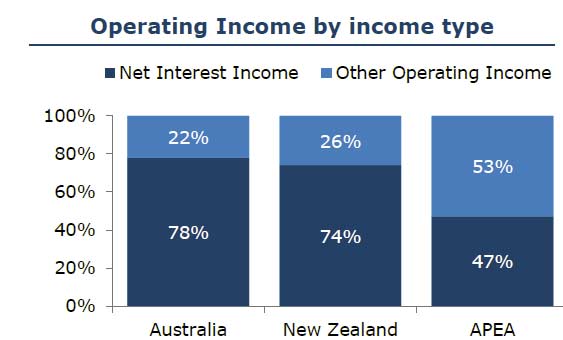

Overall contribution by region shows how reliant ANZ is on Australian net income.

Finally there was a clear emphasis on their strategy to drive digital channels, with considerable volume growth and focus, as well as efficiency. FTE declined 3%.

Finally there was a clear emphasis on their strategy to drive digital channels, with considerable volume growth and focus, as well as efficiency. FTE declined 3%.