By Viktor Shvets of Macquarie via Zero Hedge.

Investors are currently residing in a surreal world of low volatilities and spreads, ignoring potentially radical shifts in monetary and fiscal policies and unwinding of extraordinary measures of the last decade. Even as Central Banks (CBs) are worried about lack of volatility and excessive risk-taking, investors seem convinced that either strength of economic recovery, or return to liquidity and cost of capital supports, will ensure that volatilities are kept under control. Thus, either way, investors seem to expect that spreads would stay low and elevated valuations of various asset classes remain a permanent feature of an investment landscape.

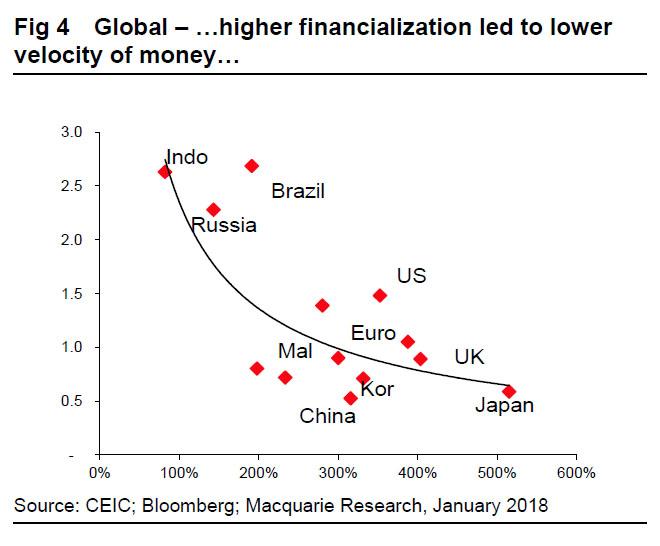

Do we agree? In our view, financial markets have been for years drifting away from real economies. Not only is the value of financial assets at least five-to-ten times larger than the underlying economies, but also this ‘financial cloud’ is now managed by computer trading, algorithms, AI and passive investments.

This is potentially a highly destabilizing mix.

CBs are aware of dangers; hence the warnings by IMF and BIS to be ‘mindful’ of gaps between economic growth and asset bubbles. In our view, CBs and financial supervisory bodies have essentially morphed from masters of the universe into slaves of grotesquely swollen financial markets.

The key to monetary policy is no longer to guide real economies, but to avoid a collapse of the financial cloud, out of fear of what a return to traditional price discovery and volatilities might imply for wealth creation and asset prices. Over the last three decades, real economies (everything from personal savings to fixed-asset investment) have become far more tightly intertwined with asset values than with wages or productivity.

In this surreal world of complete dominance of financial assets, conventional economic rules break down and financialization and avoidance of sharp asset price contractions becomes the paramount policy objective. In our view, this implies that liquidity supports cannot be withdrawn and cost of capital (holistically defined) can never rise.

Only a return to private sector dominance and accelerating productivity (rather than recoveries driven by liquidity and/or stimulus) can ensure ‘beautiful deleveraging’. We maintain that this remains a low-probability event.

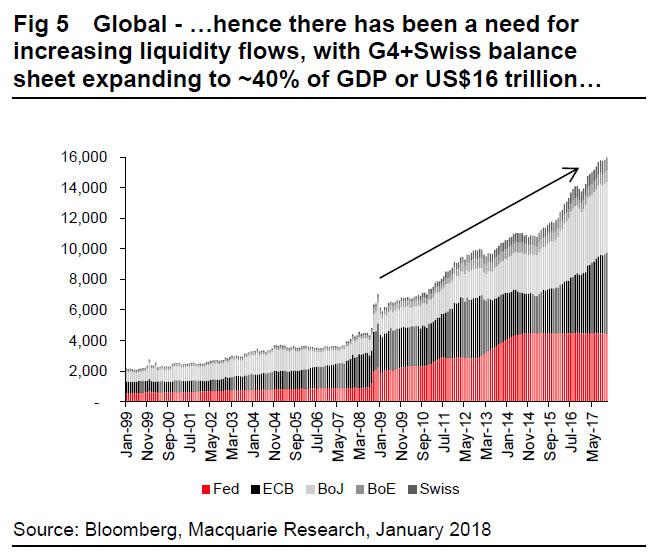

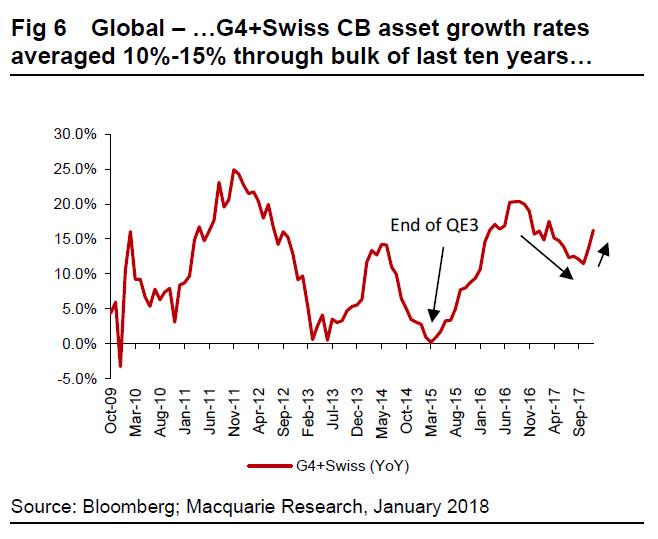

Far more likely is that the latest two-year-old recovery was due to a mix of unique and to some extent unsustainable factors, such as massive liquidity injections by key CBs (US$3.5 trillion – Mar’16 and Dec’17), coordinated monetary policies (since Feb’16) and as always, China’s stimulus.

The question therefore is what would happen to values and volatilities, if these three supports are gradually withdrawn. For example, CBs’ liquidity injection in ’18 is likely to be only ~US$0.7 trillion (turning negative in ’19) or growth of ~5%, barely enough to cover global nominal GDP (~6%).

Similarly, CBs are likely to make repeated attempts to raise cost of capital, despite likely inability to do so while China is tightening, and if history is any guide, it would more than likely over-tighten. This should raise volatilities. Even if assume that recovery is indeed more sustainable, CBs (uncomfortable as they are with current excessive valuations and low volatilities) would be happy to see volatilities rise and return to some form of price discovery. The 64-dollar dollar question is whether ‘patient is sufficiently healthy to withstand pressure’.

Thus, one way or another, it seems volatilities are likely to rise at some point in ’18, and as always ‘canary’ in the coalmine would be high yield, FX and EM markets.