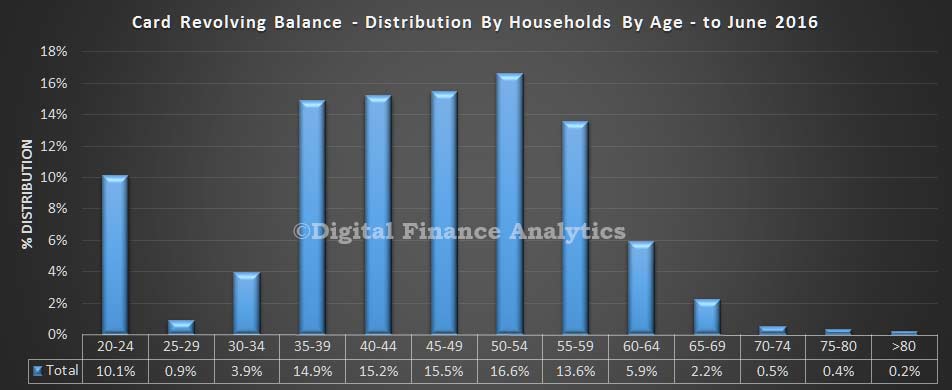

Following the US card data analysis we reported this morning, we have been looking at the situation among Australian households by using data from our household surveys. We extracted the average revolving balance data from our surveys, and mapped this first to household age bands. We find that the largest proportion of debt are found in households aged 50-54, and more generally, older households have more debt, similar to the US findings. The spike in the 20-24 age bands is explained by young households yet to own a property, and often living with parents, or in shared accommodation, with larger spending appetites.

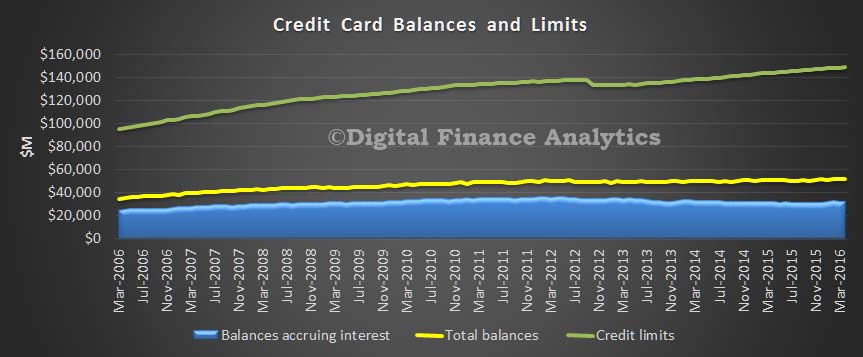

Data from the RBA also shows that nationally, whilst credit limits have steadily increased, the total balances accruing interest have not.

Data from the RBA also shows that nationally, whilst credit limits have steadily increased, the total balances accruing interest have not.

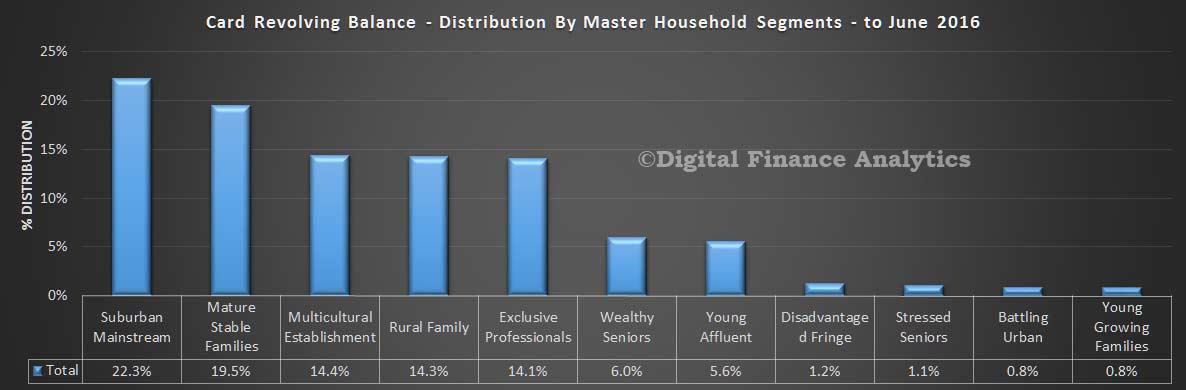

We also looked at households by our master segments, and found that most debt sits with our suburban households. These are relatively stable households, but not the most affluent. Stressed households, relatively, hold lower debt balances.

We also looked at households by our master segments, and found that most debt sits with our suburban households. These are relatively stable households, but not the most affluent. Stressed households, relatively, hold lower debt balances.

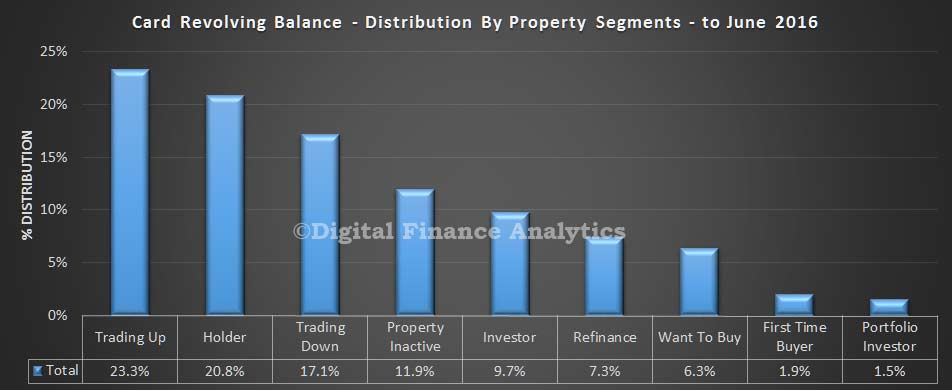

This is confirmed by looking at households by our property segmentation. The highest debt distribution is found in households looking to trade up, hold property, or trade down. These groups have significant assets behind them. Other groups, including first time buyers have lower debt balances.

This is confirmed by looking at households by our property segmentation. The highest debt distribution is found in households looking to trade up, hold property, or trade down. These groups have significant assets behind them. Other groups, including first time buyers have lower debt balances.

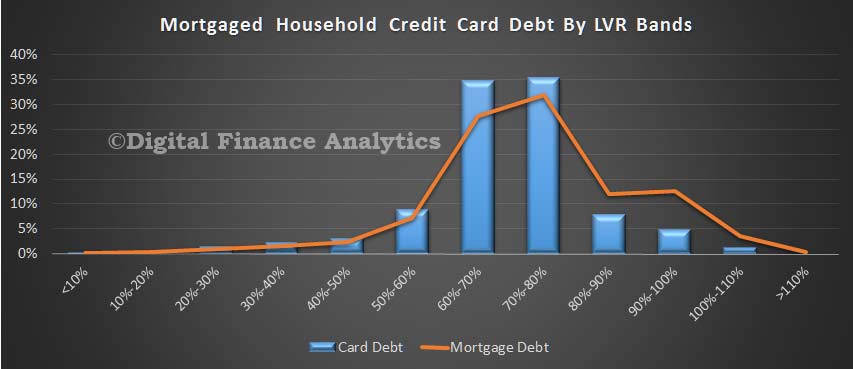

In our final piece of analysis, we looked are credit card debt distribution by the loan to value of those with mortgages. We found the largest debt levels reside in LVR bands between 60-80%, where the same is true of mortgage balances. So, we can see a correlation between LVR bands and credit card revolving debt.

In our final piece of analysis, we looked are credit card debt distribution by the loan to value of those with mortgages. We found the largest debt levels reside in LVR bands between 60-80%, where the same is true of mortgage balances. So, we can see a correlation between LVR bands and credit card revolving debt.

So, overall we conclude that older households, especially with a mortgage hold the highest card balances, and that card lending is intrinsically connected with home lending.

So, overall we conclude that older households, especially with a mortgage hold the highest card balances, and that card lending is intrinsically connected with home lending.