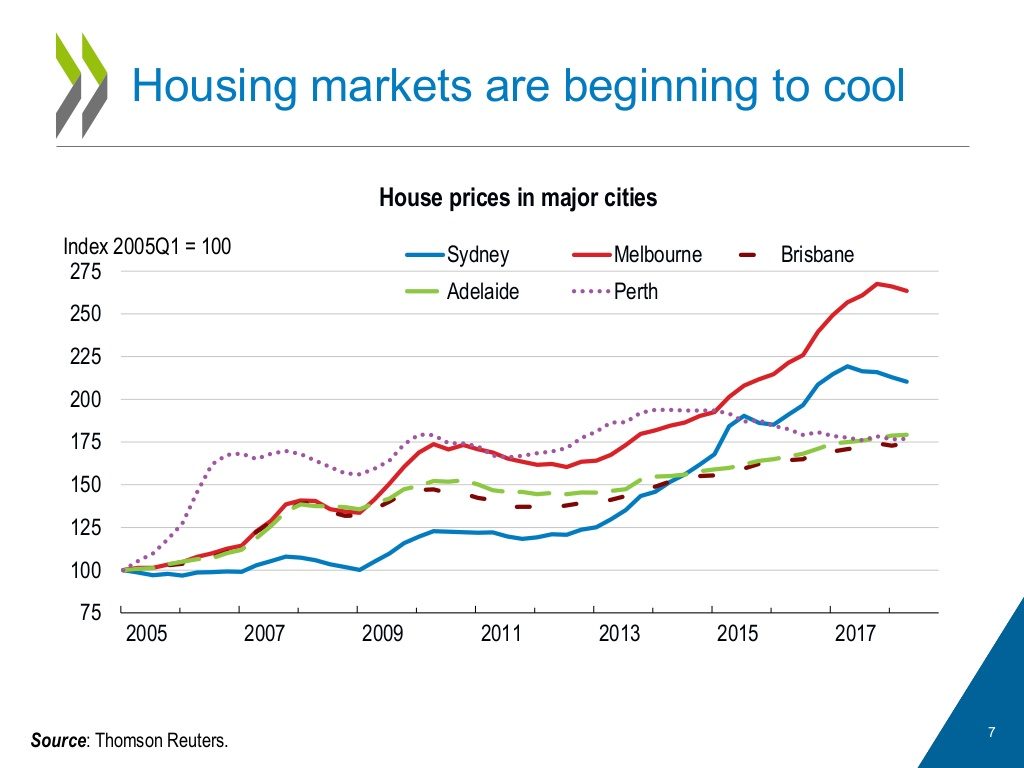

The OECD says Australia’s housing market is a source of vulnerability. Prices have more than doubled in real terms since the early 2000s and household debt has surged. The market has started to cool over the last year, with prices falling most notably in Melbourne and Sydney. So far, data point to a soft landing without substantial consequence for the overall economy. Nevertheless, risk of a hard landing remains.

To date the decrease in house prices has been gradual. Prudential measures taken by the Australian authorities restricting certain types of housing credit have played a role. So too has a pick-up in new housing supply and construction activity remains elevated. Furthermore, some evidence suggests that Australia’s house prices have not been hugely overvalued; the IMF has estimated that as of Q3 2017 prices were above equilibrium by only between 5 and 15% (Heilbling andLi, 2018).

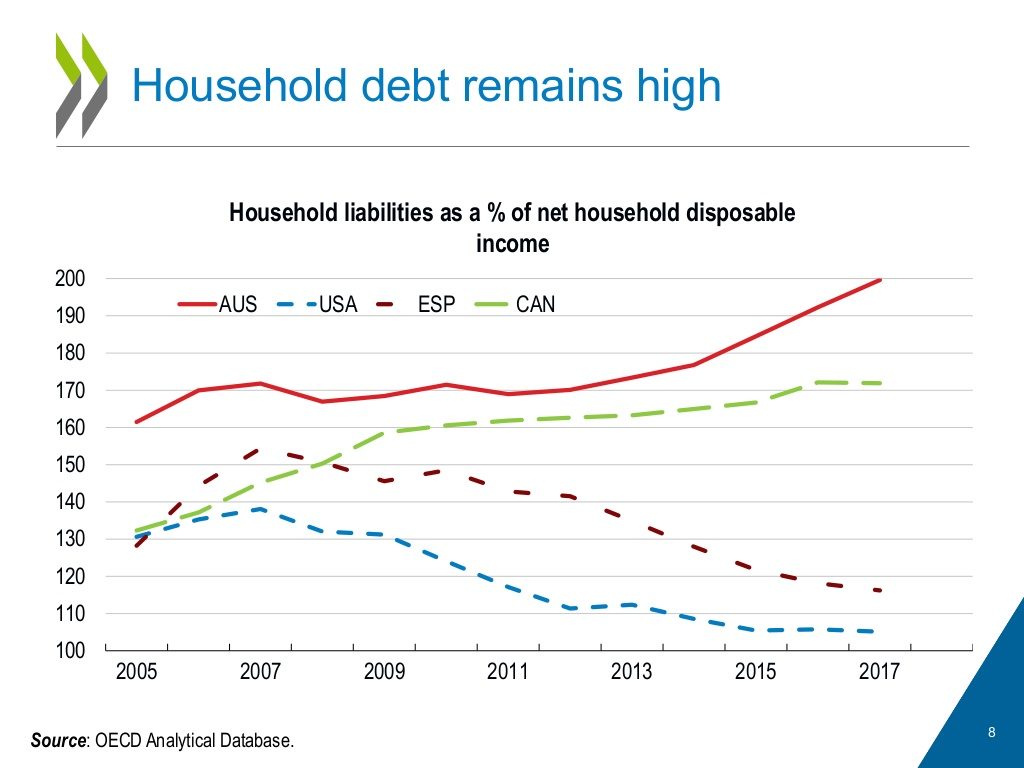

Several features of Australian financing limit the risk of financial fall-out from a house-price correction. Banks are well capitalised and their liquidity position is sound. Indebtedness is concentrated in middle- and high-income households, and data indicate declining financial stress in recent years, despite rising mortgage debt. Moreover,many mortgage holders have accumulated substantial buffers of advance payments(“mortgage prepayments”).

Nevertheless, risk of a macroeconomic downturn from the cooling housing market remains. Not withstanding the estimates that Australia’s market is not greatly overvalued, house prices could fall more substantially. Should this happen, household consumption could weaken. Households would cut their spending due to lower housing wealth and due to increased economic uncertainty generated by downturn. Households would also reduce expenditures related to the purchase, sale and maintenance of housing (such as spending on renovation and interior decoration). Sustained decreases in house prices would also weaken construction activity. Weakened aggregate demand could in turn lead to losses on loans to businesses, putting stress on the financial sector.

The OECD’s 2018 Economic Survey of Australia recommends authorities prepare contingency plans for a severe collapse in the housing market. These should include the possibility of a crisis situation in one or more financial institutions.