This is an edit of a live discussion with Dr Cameron K. Murray, an independent economist who publishes at Fresh Economic Thinking https://www.fresheconomicthinking.com/. We discussed housing policy and economics in general.

Here is the link to Cameron’s new book, out February 27th 2024 https://www.amazon.com.au/Great-Housing-Hijack-keeping-Australia/dp/176147085X

He recently republished his book from 2017 Game of Mates: How favours bleed the nation as Rigged “How Networks Of Powerful Mates Rip Off Everyday Australians”.

This book will open your eyes to how Australia really works. It’s not good news, but you need to know it.’ – Ross Gittins

‘You’ll be shocked at how far the Mates have their hand in your pocket.’ – Nicholas Gruen

Australia has become one of the most unequal societies in the Western world, when just a generation ago it was one of the most equal. This is the story of how networks of Mates have come to dominate business and government, robbing ordinary Australians.

Every hour you work, thirty minutes of it goes to line the Mates’ pockets rather than your own. Mates in big corporations, industry groups, government departments, the halls of parliament and the media skew the system to suit each other. Corporations dodge taxes, so you pay more. You pay more for your house and higher interest rates on your mortgage, more for your medicines and transport, and more for your children’s education and insurance, because the Mates take a cut.

Rigged uncovers the pattern of political favours, grey gifts and information-sharing that has been allowed to build up over two decades. Drawing on extensive economic research, it exposes the Game of Mates as nothing less than cronyism on a grand scale across Australia and how we have fallen behind other countries in combating it.

I caught up with Cameron as he republishes his book from 2017 Game of Mates: How favours bleed the nation as Rigged “How Networks Of Powerful Mates Rip Off Everyday Australians”.

This book will open your eyes to how Australia really works. It’s not good news, but you need to know it.’ – Ross Gittins

‘You’ll be shocked at how far the Mates have their hand in your pocket.’ – Nicholas Gruen

Australia has become one of the most unequal societies in the Western world, when just a generation ago it was one of the most equal. This is the story of how networks of Mates have come to dominate business and government, robbing ordinary Australians. Every hour you work, thirty minutes of it goes to line the Mates’ pockets rather than your own. Mates in big corporations, industry groups, government departments, the halls of parliament and the media skew the system to suit each other. Corporations dodge taxes, so you pay more. You pay more for your house and higher interest rates on your mortgage, more for your medicines and transport, and more for your children’s education and insurance, because the Mates take a cut.

Rigged uncovers the pattern of political favours, grey gifts and information-sharing that has been allowed to build up over two decades. Drawing on extensive economic research, it exposes the Game of Mates as nothing less than cronyism on a grand scale across Australia and how we have fallen behind other countries in combating it.

We also discuss the recent Canberra event and housing policy in general.

Dr Cameron K. Murray is a Research Fellow in the Henry Halloran Trust at the University of Sydney and an economist specialising in property and urban development, environmental economics, rent-seeking and corruption. Professor Paul Frijters teaches at the London School of Economics and was previously Professor of Health Economics at the University of Queensland.

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

Inside The Tent: How Power Really Works... With Cameron Murray [Podcast]

It is time for a new way of talking about housing in Australia. The housing crisis is quickly turning into a crisis of care.

We call on the newly re-elected Morrison government and new Housing

Minister Michael Sukkar to recognise that the value of housing is not

just economic. Housing is an infrastructure of care. Australian

governments need to ask: is this a housing system that cares?

A location for essential care

Houses are hubs of care practices and relations. They are places of

everyday care, of cooking, cleaning and washing, of care between

household and family members. Houses are where we care for children,

elders, partners and ourselves.

Houses are also anchors for community and neighbourhood-based care.

We keep an eye on neighbours’ homes, support older neighbours to age in place, and care for pets.

This care work is what keeps us alive.

Even though care is not always done well, it is an essential practice

that is connected in fundamental ways with housing. Without housing it

can be very difficult to meet basic needs.

The care work of housing

But housing is more than just a place where care takes place. Housing

systems – through housing policy, markets and design – organise the

distribution of care and the ability of people to give and receive care.

In our research this drives us to ask: how does the housing system support or limit the capacity of households to care?

We argue that housing is a care infrastructure and call for this understanding of housing to be at the centre of housing reform.

Home owners benefit

In Australia we value housing as an individual investment and asset. The economic values of housing (how much we can buy, sell or otherwise leverage housing for) are at the heart of how housing is usually discussed.

For affluent households housing markets can work very well as a care

infrastructure. This is because these households can more readily afford

housing that meets household care needs. They are also more able to

invest in housing to cover the costs of care in later life and to

support the needs and ambitions of children. For home owners housing is a

private welfare net for funding care needs.

Australian housing and related policies create and reinforce the

value of home ownership. Subsidies for first home owners, the proposed

First Home Loan Deposit Scheme (which will be a focus of efforts by the new housing minister),

preferential treatment for owner occupation in pension tests and tax

breaks for investor landlords underpin the value of home ownership as an

infrastructure of care.

However, for the growing numbers of households not in a position to

own a home the picture is less rosy. In many cases housing becomes an

infrastructure that inhibits access to necessary care. As increasing numbers of households rent for longer periods, we risk a housing system that only cares for some.

Housing affordability

Housing affordability is a central concern. Lower income earners have

less ability to choose to live in places that are well serviced or

where family-based care networks are located. Less affluent areas often

have less access to public and private care services like doctors and other specialists.

Housing affordability also shapes the ability to afford other care

resources like quality food and electricity. Households that face high

housing costs are often forced to compromise in these areas.

In Emma’s and otherrelated research

older retirees in the private rental market depended on local food

charities for nutritious food. And in winter they restricted their use

of heating to avoid bill blow-outs.

There are also connections between paid work, caring capacity and

housing affordability. High-cost housing markets can drive people to

work longer hours and multiple jobs, or require multiple income earners

within a household. This can reduce the ability of individuals and

households to meet domestic care responsibilities.

Tenure and care

Non-home owners also face restrictions around their use of private rental properties. For a start, rental housing is notoriously insecure. There are also restrictions on the ability of renters to make a house into a home.

Private rental legislation typically does not require landlords to

agree to property modifications to meet the needs of a person with

disability or ageing body, even when tenant-funded.

Women in Emma’s research reported losing bonds to cover costs associated with removing modifications that had been agreed to during a tenancy. In Kathy’s research,

the fear of eviction meant private renters found it difficult to ask

for and be granted repairs that would make their homes habitable. They

endured leaking roofs and mouldy walls that made housing unsuitable for

meeting basic care needs.

As growing numbers of households find themselves locked out of home

ownership and face difficulties securing affordable housing in our expensive private rental markets, Australia badly needs housing reform.

The care work of housing must be at the centre of housing policy. The

new government and minister for housing must ask: first, is this a

housing system that cares? And, second, who does this housing system

care for?

Historically, this question has been answered with calls to increase

home ownership. But there is value in a diverse housing system because

different households have different needs.

Further, those who invest in housing are dependent on the people who will rent that housing. These people in turn have the right – and need – for housing that supports their care needs. Affordable housing is only the starting point.

Authors: Emma Power, Senior Research Fellow, Geography and Urban Studies, Western Sydney University; Kathleen Mee, Associate Professor of Geography, University of Newcastle

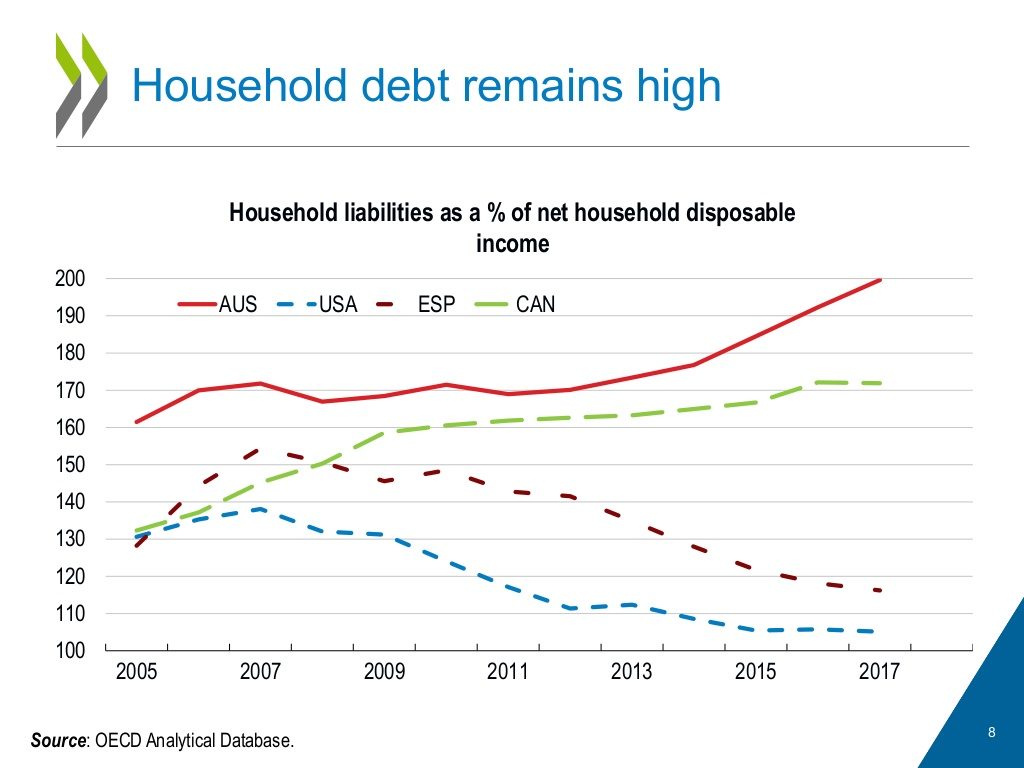

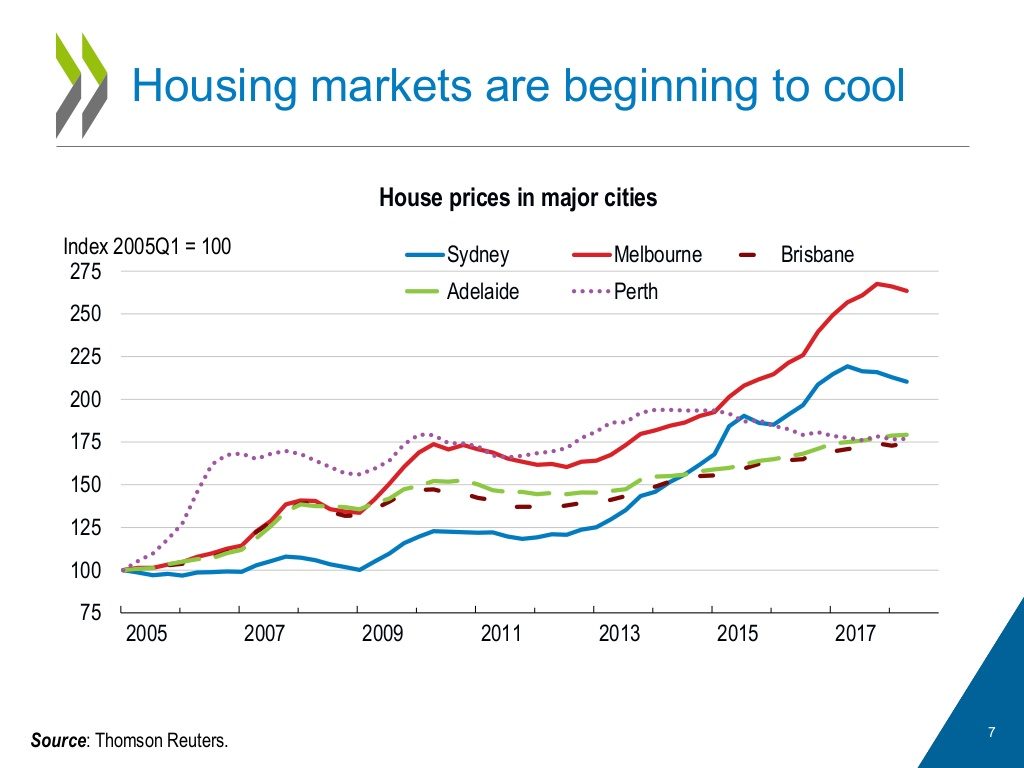

The OECD says Australia’s housing market is a source of vulnerability. Prices have more than doubled in real terms since the early 2000s and household debt has surged. The market has started to cool over the last year, with prices falling most notably in Melbourne and Sydney. So far, data point to a soft landing without substantial consequence for the overall economy. Nevertheless, risk of a hard landing remains.

To date the decrease in house prices has been gradual. Prudential

measures taken by the Australian authorities restricting certain types

of housing credit have played a role. So too has a pick-up in new

housing supply and construction activity remains elevated. Furthermore,

some evidence suggests that Australia’s house prices have not been

hugely overvalued; the IMF has estimated that as of Q3 2017 prices were

above equilibrium by only between 5 and 15% (Heilbling andLi, 2018).

Several features of Australian financing limit the risk of financial

fall-out from a house-price correction. Banks are well capitalised and

their liquidity position is sound. Indebtedness is concentrated in

middle- and high-income households, and data indicate declining

financial stress in recent years, despite rising mortgage debt.

Moreover,many mortgage holders have accumulated substantial buffers of

advance payments(“mortgage prepayments”).

Nevertheless, risk of a macroeconomic downturn from the cooling

housing market remains. Not withstanding the estimates that Australia’s

market is not greatly overvalued, house prices could fall more

substantially. Should this happen, household consumption could weaken.

Households would cut their spending due to lower housing wealth and due

to increased economic uncertainty generated by downturn. Households

would also reduce expenditures related to the purchase, sale and

maintenance of housing (such as spending on renovation and interior

decoration). Sustained decreases in house prices would also weaken

construction activity. Weakened aggregate demand could in turn lead to

losses on loans to businesses, putting stress on the financial sector.

The OECD’s 2018 Economic Survey of Australia

recommends authorities prepare contingency plans for a severe collapse

in the housing market. These should include the possibility of a crisis

situation in one or more financial institutions.

Once taken for granted by the mainstream, home ownership is increasingly precarious. At the margins, which are wide, it is as if a whole new form of tenure has emerged.

Whatever the drivers, significant and lasting shifts are shaking the foundations of home ownership. The effects are far-reaching and could undermine both the financial and wider well-being of all Australian households.

Over the course of 100 years, Australians became accustomed to smooth housing pathways from leaving the parental home to owning their house outright. However, not only did the 2008-09 global financial crisis (GFC) underline the risk of dropping out along the way, but more recent Australian evidence has shown that the old pathways have been displaced by more uncertain routes that waver between owning and renting.

The Household, Income and Labour Dynamics in Australia (HILDA) Survey indicates that, during the first decade of the new millennium, 1.9 million spells of home ownership ended with a move into renting (one-fifth of all home ownership spells that were ongoing in that period). It also shows that among those who dropped out, nearly two-thirds had returned to owning by 2010. Astonishingly, some 7% “churned” in and out of ownership more than once. Many households no longer either own or rent; they hover between sectors in a “third” way.

The drivers of this transformation include an ongoing imperative to own, vying with the factors that oppose this – rising divorce rates, soaring house prices, growing mortgage debt, insecure employment and other circumstances that make it difficult to meet home ownership’s outlays.

Those who use the family home as an “ATM” are at added risk. This relatively new way of juggling mortgage payments, savings and pressing spending needs makes some styles of owner occupation more marginal – as the tendency is to borrow up, rather than pay down, mortgage debts over the life course.

A retirement incomes system under threat

Since its inception, the means-tested age pension system has been set at a low fixed amount. Retired Australians could nevertheless get by provided they achieved outright home ownership soon enough. The low housing costs associated with outright ownership in older age were effectively a central plank of Australian social policy.

Moreover, developments in the Australian housing system could undermine a second retirement incomes pillar – the superannuation guarantee. An important goal of the superannuation guarantee is financial independence in old age. But if superannuation pay-outs are used to repay mortgage debts on retirement, reliance on age pensions will grow rather than recede.

Such policy interest is not surprising. Housing wealth dominates the asset portfolios of the majority of Australian households, boosted by soaring house prices. If home owners can be encouraged or even compelled to draw on their housing assets to fund spending needs in retirement, this will ease fiscal pressures in an era of population ageing.

However, the welfare role of home ownership is already important in the earlier stages of life cycles. Financial products are increasingly being used to release housing equity in pre-retirement years. This adds to the debt overhang as retirement age approaches. It also increases exposure to credit and investment risks that could undermine stability in housing markets.

A gender equity issue

A commonly overlooked angle relates to gender equity. Australian women own less wealth than men, and they also hold more housing-centric asset portfolios.

Hence, women are more exposed to housing market instability associated with precarious home ownership. Single women are especially vulnerable to investment risk when they seek to realise their assets.

A neglected economic lever

Housing and mortgage markets played a central role in the GFC. Today, it is widely agreed that resilient housing and mortgage markets are important for overall economic and financial stability. There are also concerns that the post-GFC debt overhang is a drag on economic growth.

However, the policy stance in the wake of the GFC has been “business as usual”. There has been very little real innovation in the world of housing finance or mortgage contract design in recent years. This might change if housing were steered from the periphery to a more central place in national economic debates.

Forward-looking policy response is needed

Growing numbers of Australians clearly face an uncertain future in a changing housing system. The traditional tenure divide has been displaced by unprecedented fluidity as people juggle with costs, benefits, assets and debts “in between” renting and owning.

This expanding arena is strangely neglected by policy instruments and financial products. Politicians cling to an outdated vision of linear housing careers that does little to meet the needs of “at risk” home owners, locked-out renters, or churners caught between the two.

The hazards of a destabilising home ownership sector are wide-ranging, rippling well beyond the realm of housing. Part of the answer is a new drive for sustainability, based on a housing system for Australia that is more inclusive and less tenure-bound.

Author: Rachel Ong, Professor of Economics, School of Economics and Finance, Curtin University; Gavin Wood, Emeritus Professor of Housing and Housing Studies, RMIT University; Susan Smith,

Honorary Professor of Geography, University of Cambridge

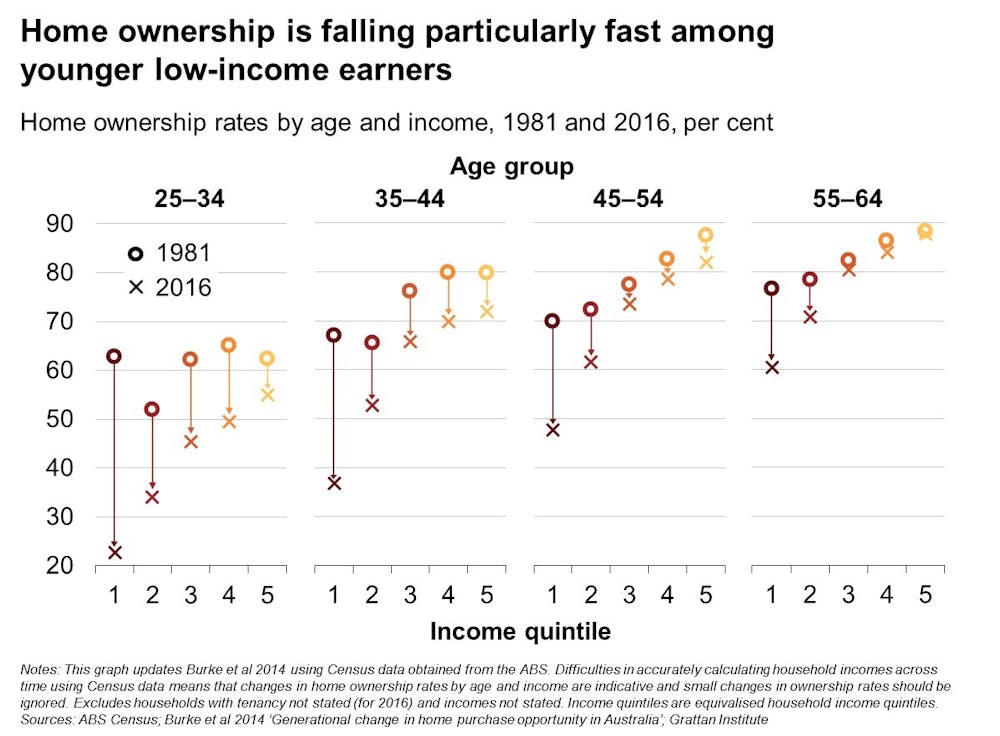

Rising housing costs are hurting low-income Australians the most. Those at the bottom end of the income spectrum are much less likely to own their own home than in the past, are often spending more of their income on rent, and are more likely to be living a long way from where most jobs are being created.

Low-income households have always had lower home ownership rates than wealthier households, but the gap has widened in the past decade. The dream of owning a home is fast slipping away for most younger, poorer Australians.

As you can see in the following chart, in 1981 home ownership rates were pretty similar among 25-34 year olds no matter what their income. Since then, home ownership rates for the poorest 20% have fallen from 63% to 23%.

Home ownership rates also declined more for poorer households among older age groups. Home ownership now depends on income much more than in the past.

Lower home ownership rates mean more low-income households are renting, and for longer. But renting is relatively unattractive for many families. It is generally much less secure and many tenants are restrained from making their house into a home.

For poorer Australians who do manage to purchase a home, many will buy on the edges of the major cities where housing is cheaper. But because jobs are becoming more concentrated in our city centres, people living on the fringe have access to fewer jobs and face longer commutes, damaging their family and social life.

Prices for low-cost housing have increased the fastest

The next chart shows that the price for cheaper homes has grown much faster than for more expensive homes over the past decade. This has made it much harder for low-income earners to buy a home.

If we group the housing market into ten categories (deciles), we can see the price of a home in the lowest (first and second) deciles more than doubled between 2003-04 and 2015-16. By contrast, the price of a home in the fifth, sixth and seventh deciles only increased by about 70%.

Tax incentives for investors may explain why the price of low-value homes increased faster. Negative gearing remains a popular investment strategy; about 1.3 million landlords reported collective losses of A$11 billion in 2014-15.

Many investors prefer low-value properties because they pay less land tax as a proportion of the investment. For example, an investor who buys a Sydney property on land worth A$550,000 pays no land tax, whereas the same investor would pay about A$9,000 each year on a property on land worth A$1.1 million.

Rising housing costs also hurt low-income renters

As this last chart shows, more low-income households (the bottom 40% of income earners) are spending more than 30% of their income on rent (often referred to as “rental stress”), particularly in our capital cities. In comparison, only about 20% of middle-income households who rent are spending more than 30% of their income on rent.

Why are more low-income renters under rental stress?

Secondly, rents for cheaper dwellings have grown slightly faster than rents for more expensive dwellings. Finally, the stock of social housing – currently around 400,000 dwellings – has barely grown in 20 years, while the population has increased by 33%.

As a result, many low-income earners who would once have been in social housing are now in the private rental market.

What can be done about it?

Increasing the social housing stock would improve affordability for low-income earners. But the public subsidies required to make a real difference would be very large – roughly A$12 billion a year – to return the affordable housing stock to its historical share of all housing.

In addition, the existing social housing stock is not well managed. Homes are often not allocated to people who most need them, and quality of housing is often poor. Increased financial assistance by boosting Commonwealth Rent Assistance may be a better way to help low-income renters meet their housing costs

Boosting Rent Assistance for aged pensioners by A$500 a year, and A$500 a year for working-age welfare recipients would cost A$250 million and A$450 million a year respectively.

Commonwealth and state governments should also act to improve housing affordability more generally. This will require policies affecting both demand and supply.

An emerging technology, blockchain, could transform the way we buy and sell real estate by doing away with the hidden costs and inefficiencies of our housing markets.

Blockchain is an online ledger that records transactions. It’s capable of recording the movement of any kind of asset from one owner to the next.

It’s public and isn’t owned by any one corporation, there are no charges to record transactions. Its openness ensures the integrity of transactions and ownership, as everyone involved has a stake in keeping it honest.

This means there are fewer intermediaries; less middle-men who increase the costs and time to complete a transaction.

There are risks associated with the system as it’s only as strong as the code that supports it, which has come under attack in the past. Despite this, examples from overseas show it is possible to apply this technology successfully to our housing market.

Problems in how the property market is run

For buyers able to find the right property, secure a mortgage and save a deposit, they must also pay for a range of so-called “hidden costs”. These are additional payments associated with the transaction over the cost of the home itself. Many legal and title-related costs would become near-obsolete in a blockchain system.

The combined costs of title registration, title insurance, and legal fees associated with register the property transfer approach A$1,000 on the average Australian house. Costs continue to rise as the prudent buyer undertakes further due diligence, through building inspection documentation, previous sales records and so forth.

On top of the financial cost, it then typically takes over a month to settle a real estate transaction in Australia. The blockchain system can speed things up, as currently tedious checks undertaken by hand, move to an automated system overseen and approved by the relevant stakeholders.

There is also the risk that land titles offices with a single database simply get things wrong too. In 2016 it was reported that 300 incorrect certificates had been issued in NSW, with 140 of those being recent property buyers affected by government plans for major motorways in Sydney’s west.

There are now concerns that the system’s quality could be compromised in several states, including NSW and South Australia, as land titles offices become privatised.

A blockchain real estate market

If blockchain were applied to the property market in Australia, every property would be encoded with a unique identifier. Property IDs already exist in most land registry systems, so these would need to be migrated to a blockchain.

Next, the blockchain ecosystem then needs to have defined who the people behind the transaction are, those stakeholders that include the owner, lender, and government.

Transactions of property are conducted via “smart contracts” – digital rules in the blockchain that process the agreement and any specified conditions. Buying and selling could still take place via agents, or the smart contract can be advanced to incorporate the sale rules and make this decision automatically. The blockchain for each property grows as transactions are added to the ledger.

A housing market without agents, conveyancers and a land-titles office may seem decades away, but a handful of countries have already piloted blockchain land registration system.

In Australia, our current land titles system is among the world’s best, but it is not infallible. A range of hidden taxes and transaction costs increase market inefficiencies.

And while the electronic system Property Exchange Australia or PEXA, has brought us to the point of a near paperless property market, it’s still an intermediary between the parties and the record of the transfer in the Torrens system – our current land title system.

The added advantage of a blockchain system is in eliminating risks, in particular the risk of records being accessed fraudulently and altered or deleted because it is a permanent and immutable record. This means that a huge amount of computing power would be required, probably along with some collusion, and the alteration is easily detected across the ledger. That’s not to say the blockchain system is perfect.

Blockchain’s advantage in restricting any changes to historical records becomes a disadvantage when incorrect or fraudulent entries are added. Digital currency managers, Ether and Bitfinex, learned this the hard way through cyber attacks.

Last year these attacks siphoned off over US$50 million in ether tokens from The DAO, the largest crowdfunded venture capital fund. This breach led to a controversial split of Ether into two separate active digital currencies.

Only months later, Hong Kong-based crytocurrency trading firm, Bitfinex, had the equivalent of US$68 million stolen by hackers in a security breach reminiscent of the hack that bought down Mt Gox in 2014. It is little comfort to cautious market regulators that the thieves behind these attacks can not spend it without revealing their identity on the blockchain.

These hacks demonstrate that blockchain systems are only as secure as the code which supports them. As a nascent technology, its cracks are detected only when they are exposed.

Where blockchain has worked before

Sweden became the first western country to explore the use of blockchain for real estate in July last year. At the time, the Swedish Land Registry partnered with blockchain startup ChromaWay to test how parties to a real estate transaction – the buyer, seller, lender, government – could track the deal’s progress on a blockchain.

Other countries at the forefront of blockchain for real estate include The Republic of Georgia, Honduras, and Brazil which announced a pilot program earlier this month. While this might seem like a disparate list, it’s in these countries where the long-term potential of a blockchain for real estate are most significant.

Systemic corruption and insecure database management in these countries, and many other emerging economies, is seen as a major constraint on growth and prosperity. Why would you invest in a house, or any other asset, if there is a distinct possibility that the record of your ownership could simply disappear?

With ever increasing demands for improvements to transaction efficiency and local real estate industry giants like CoreLogic appointing research teams dedicated to new technology applications, it might not be long before we see a real estate blockchain system in Australia.

Author: Danika Wright, Lecturer in Finance, University of Sydney

Sydney’s housing affordability crisis is being artificially exacerbated by “lunacy” tax incentives, a new report has claimed.

According to the analysis by the UNSW’s City Futures Research Centre, up to 90,000 properties are sitting empty in some of Sydney’s most sought-after suburbs as investors chase capital gains over rental returns.

The analysis’ researchers, Professor Bill Randolph and Dr Laurence Troy, said this is thanks to the “perverse outcomes” of tax incentives such as negative gearing, Fairfax has reported.

“Leaving housing empty is both profitable and subsidised by government,” Randolph and Troy told Fairfax.

“This is taxation lunacy and a national scandal.”

According to Fairfax, the 2011 census revealed that in Sydney’s “emptiest” neighbourhood of the CBD, Haymarket and The Rocks, one in seven dwellings was vacant.

Close behind were Manly-Fairlight, Potts Point-Woolloomooloo, Darlinghurst and Neutral Bay-Kirribilli, which all had vacancy levels above 13%. These neighbourhoods, together with central Sydney, account for nearly 7,200 empty homes.

The UNSW analysis of the 90,000 unoccupied dwellings across metropolitan Sydney compared the number of empty homes in a suburb against the rate of return investors made by renting out a property.

It found that properties in neighbourhoods with lower rental yields and higher expected capital gains were more likely to be unoccupied.

Gordon-Killara on the north shore had the highest share of vacant apartments, with more than one in six unoccupied on Census night, according to Fairfax. By contrast, only one in 42 dwellings (2.4%) in Green Valley-Cecil Hills, in Sydney’s west, was unoccupied.

These results suggest property investors in some of Sydney’s most desirable areas have become indifferent to whether their investment property is rented or not. Instead, investors are chasing capital gains with rental losses offset by negative gearing and capital gains concessions.

According to Troy and Randolph, this calls into question Sydney’s housing supply and affordability problem.

“If you choose to accept that there is a housing shortage in Sydney, then the sheer scale and location of these figures strongly suggest that this is an artificially produced scarcity,” they said, according to Fairfax.

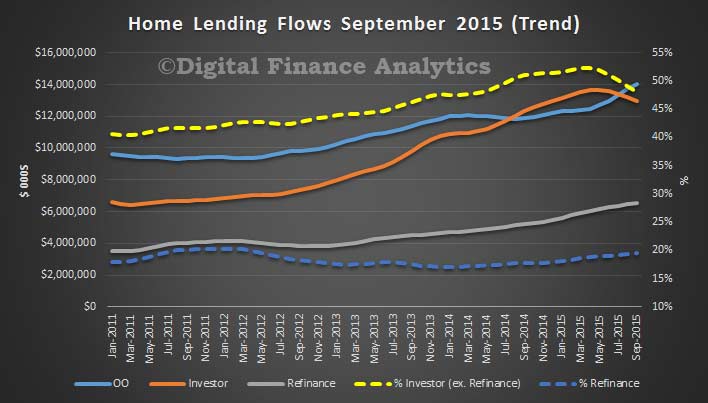

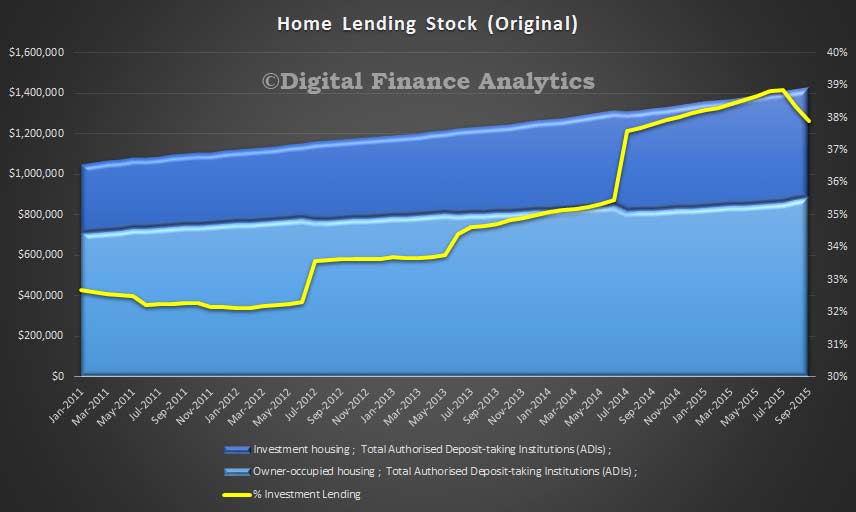

The latest home finance data from the ABS confirm the trend that investor loans are on the slide, and being replaced by growth in owner occupied loans and refinancing. In September, trend, owner occupied housing commitments rose 2.0% to $20.5 bn while investment housing commitments fell 1.9% to $12.9 bn. The number of commitments for owner occupied housing finance rose 0.7% in September whilst the number of commitments for the purchase of new dwellings rose 1.3% the number of commitments for the purchase of established dwellings rose 0.8%. The number of commitments for the construction of dwellings fell 0.1%.

The proportion of investor loans fell back to 48%, whereas a few months back it was well above 50%. Refinance of owner occupied loans continues to rise, to nearly 20% of all loans written, a level not seen since 2012. So the relative shift away from investment loans is confirmed, in response to regulatory intervention.

In stock terms, the mix of investment loans – as reported in original terms, has fallen back to 38%, but is still way higher than when regulators officially started to worry about the systemic risks of investment loans above mid thirties. we can expect to see further data revisions in coming months, as banks continue to reclassify loans.

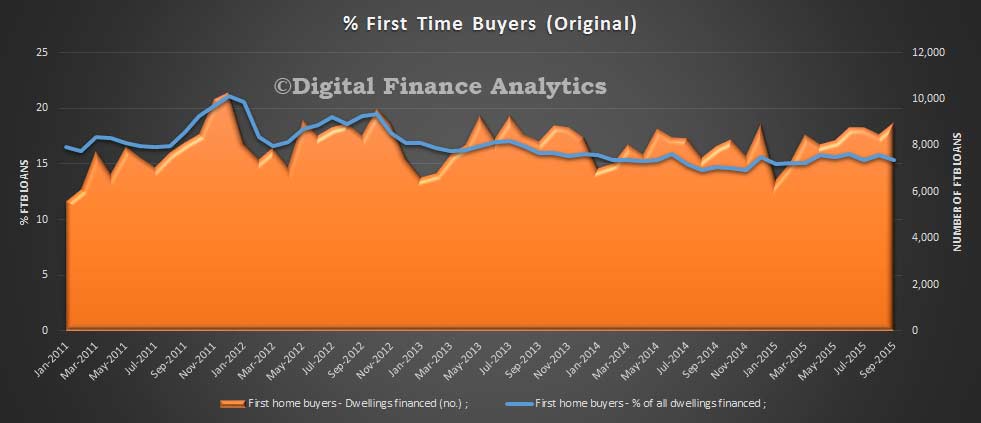

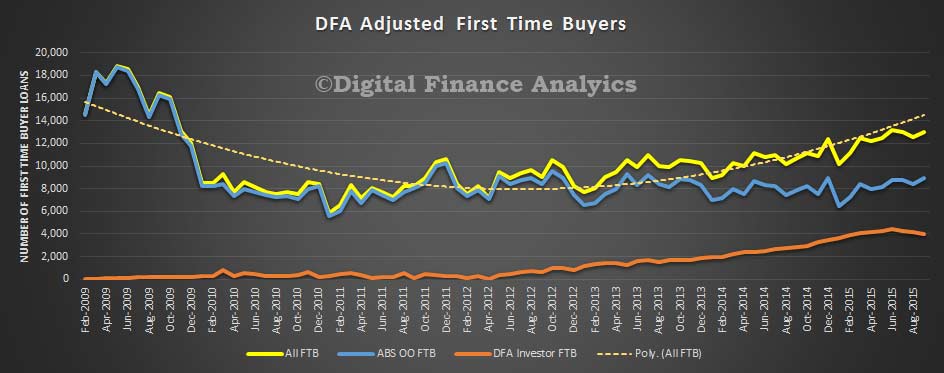

Turning to first time buyers, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 15.4% in September 2015 from 15.8% in August. However, this does not tell the full story.

Looking at DFA adjusted data, to take account of first time buyers going direct to the investment sector, we see a further fall in new FTB investor loans, down more than 2% in the month. The number of FTB loans for owner occupation rose however, by 6%, so the overall volume of loans is up. The average FTB loan was 2% larger this month.

The strategies of the banks are clear, focus on owner occupied loans, and offer deep discounts to wrest refinanced loans from competitors, whilst using back-book repricing to fund it. At what point will the regulators step-up their surveillance of owner occupied lending? We think they should do so now.

The RBA released their latest Financial Stability Review today. It is worth reading through the 66 pages, because there are a number of important themes, relating to housing. Underlying this though is a beat which could be interpreted as the RBA admitting they have misread the housing sector.

In summary, they recognise that underwriting standards were not as good as initially thought, the investment loan and interest only loan sectors carry potentially higher risks, and the changes to capital and regulatory standards will have a mitigating impact, over the medium term. That said, households remain well placed (despite the highest ever debt at lowest ever interest rates).

They are however concerned about the impact of the current residential construction boom.

They also highlight risks from lending by banks to the commercial property sector, and the ongoing use of SMSF’s to invest in property.

There is also a section of the capital ratios for the banks, both under then IRB and standard approaches to capital ratios. Of particular note is for banks using the standard approach, they show how the presence of Lender Mortgage Insurance (LMI) and different LVR’s impact the capital weights. Despite the upcoming move from 17 to 25 basis points for banks under the advanced IRB approach, banks with the standard approach remain at a competitive disadvantage.

Blog")