The Australian Prudential Regulation Authority (APRA) today released Quarterly Authorised Deposit-taking Institution Property Exposures for the March 2015 quarter.

Quarterly ADI Property Exposures contains information on ADIs’ commercial property exposures, residential property exposures and new housing loan approvals. Detailed statistics on residential property exposures and new housing loan approvals are included for ADIs with greater than $1 billion in housing loans.

ADIs’ commercial property exposures were $234.2 billion, an increase of $15.1 billion (6.9 per cent) over the year. Commercial property exposures within Australia were $193.3 billion, equivalent to 82.5 per cent of all commercial property exposures.

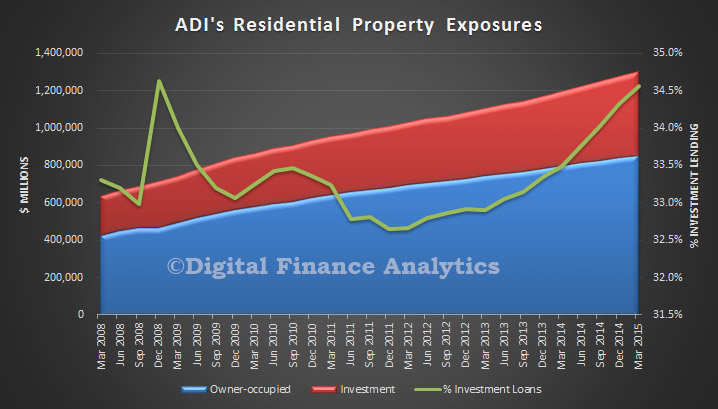

ADIs’ total domestic housing loans were $1.3 trillion, an increase of $107.1 billion (9.0 per cent) over the year. There were 5.3 million housing loans outstanding with an average balance of $243,000.

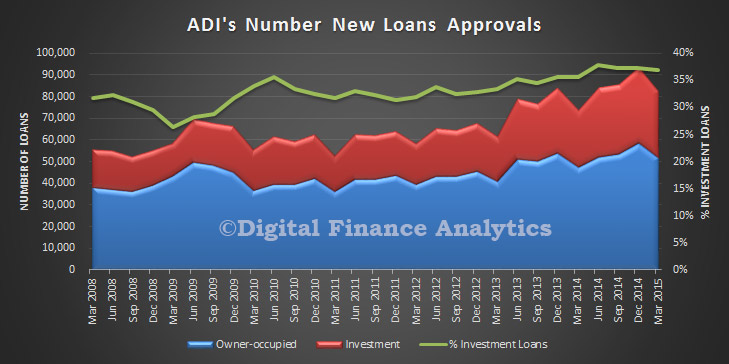

ADIs with greater than $1 billion of residential term loans approved $82.3 billion of new loans, an increase of $8.5 billion (11.5 per cent) over the year. Of these new loan approvals, $51.9 billion (63.0 per cent) were owner-occupied loans and $30.4 billion (37.0 per cent) were investment loans.

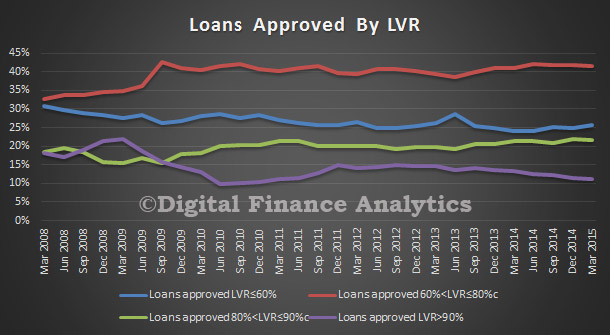

Looking in more detail at the data, looking first at the portfolio data, we see the rise on the value of home lending across the ADI’s and the rise in the proportion of investment loans in the mix. High LVR’s fell a little.

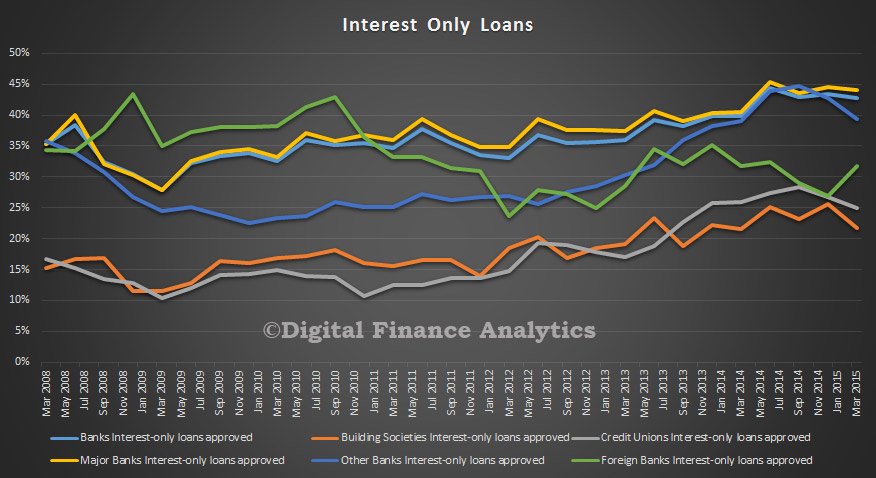

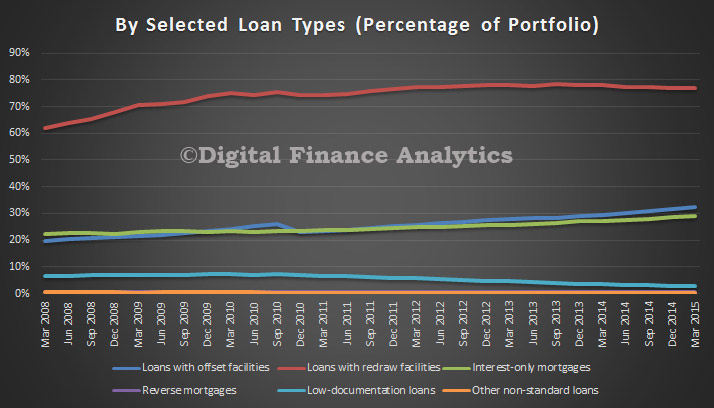

The mix of loan type shows a continuing slow rise in interest-only loans (28.9% of all loans) and offset loans (32.3%), and a slight fall in loans with redraw (77.1% of loans).

The mix of loan type shows a continuing slow rise in interest-only loans (28.9% of all loans) and offset loans (32.3%), and a slight fall in loans with redraw (77.1% of loans).

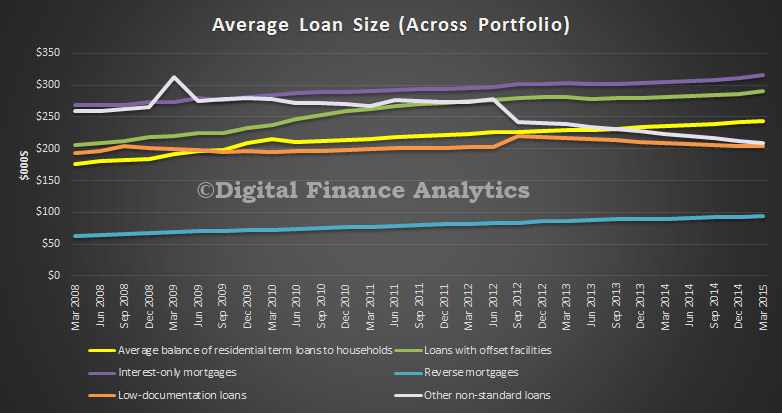

Across the portfolio, the average balance on interest-only loans is the highest, at $315,000, whilst reverse mortgages sat at $94,000.

Turning to approvals by quarter, we see a steady rise in approval volumes, with 37% by number investment loans. Remember that earlier APRA showed that more than 50% of loans by value were for investment loans, so we again see evidence that investment loans are larger by value.

Turning to approvals by quarter, we see a steady rise in approval volumes, with 37% by number investment loans. Remember that earlier APRA showed that more than 50% of loans by value were for investment loans, so we again see evidence that investment loans are larger by value.

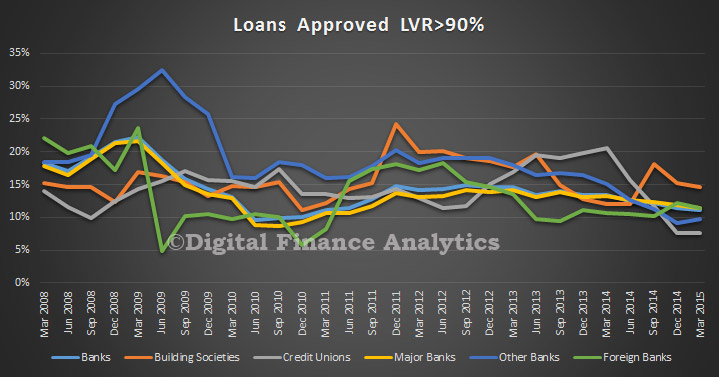

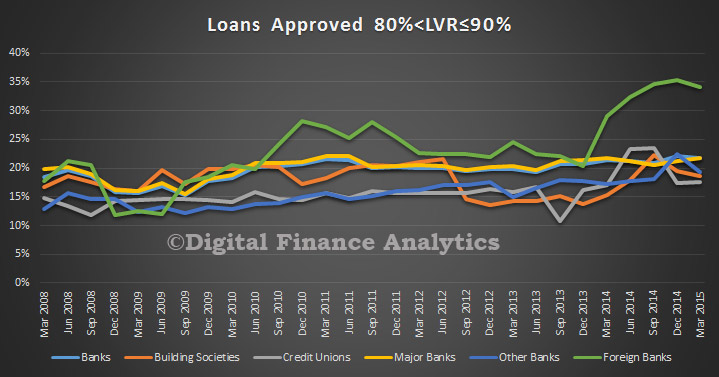

Looking at LVR bands, we see a slight fall in loans over 90% LVR (from 14% to 11%) a slight rise in the 80-90% band, (from 16% to 22%). So the regulators influence is showing though to some extent.

Looking at LVR bands, we see a slight fall in loans over 90% LVR (from 14% to 11%) a slight rise in the 80-90% band, (from 16% to 22%). So the regulators influence is showing though to some extent.

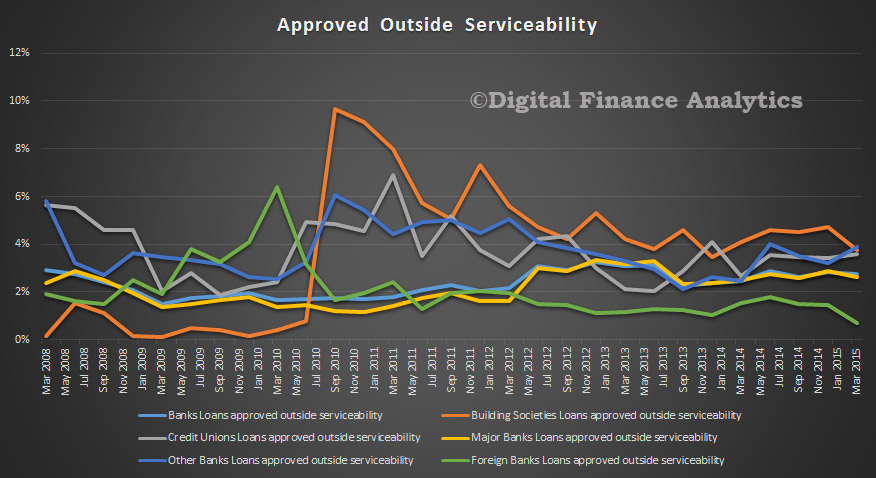

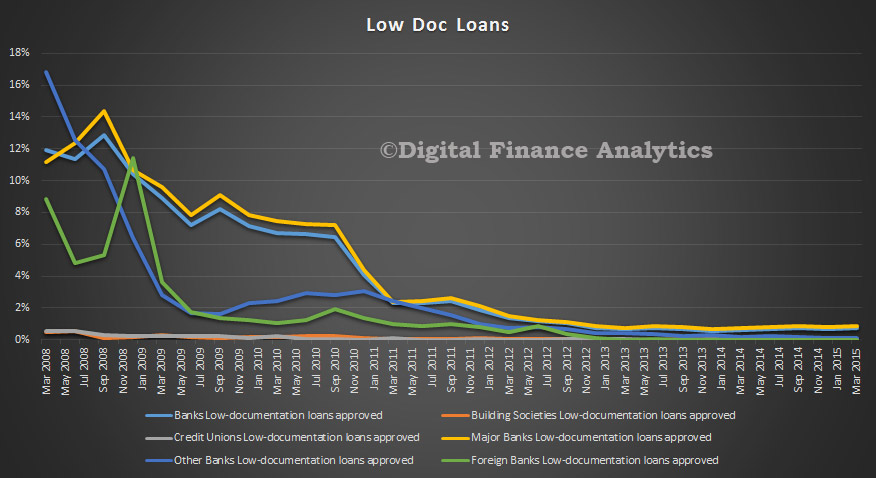

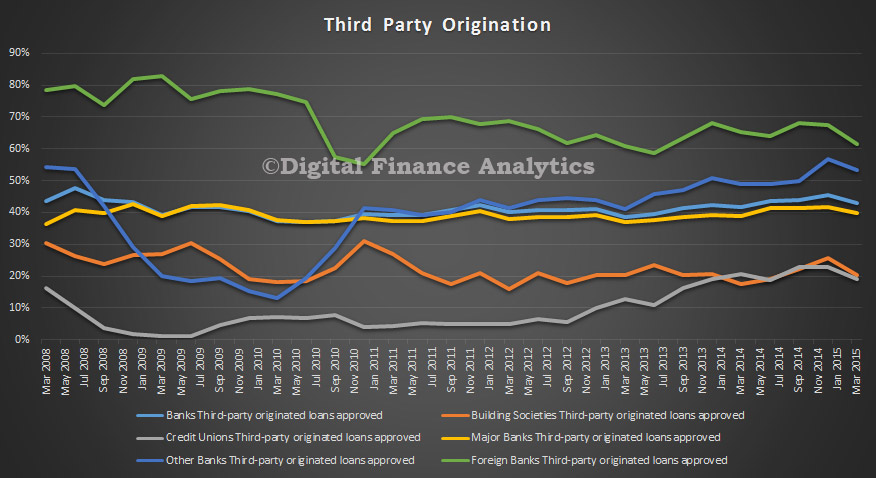

Finally, we see that third party loans by volume (not value) fell from 45% to 42% this quarter. Interest only loans accounted for 42% of approvals. Low doc and loans outside serviceability were low.

Finally, we see that third party loans by volume (not value) fell from 45% to 42% this quarter. Interest only loans accounted for 42% of approvals. Low doc and loans outside serviceability were low.

So overall, we see buoyant loan growth, supported by rises in investment lending and interest only loans. We will be watching the data next quarter as the Regulators tighten the screws. We think the property worm is about to turn.

So overall, we see buoyant loan growth, supported by rises in investment lending and interest only loans. We will be watching the data next quarter as the Regulators tighten the screws. We think the property worm is about to turn.