Digital is where Australian advertisers are heading. According to eMarketer, total media advertising spend in Australia will reach $11.59 billion in 2015. Digital ad spend will pass $5 billion to account for 43.3% of total media ad spending, and mobile ad expenditure will total $1.46 billion—29.0% of digital and 12.6% of total media ad spending.

Author: Martin North

Martin North is the Principal of Digital Finance Analytics

Foreign Investors Fees Still In The Air

Speaking on ABC Insiders this morning Josh Frydenberg, Assistant Treasurer made the point that the foreign investor regulations, recently announced were open for consultation, and that a number of issues had yet to be resolved. For example, should a foreign investor pay the fee each time they apply to purchase a property (so bidding on multiple properties would mean multiple fees)? Or should they pay one fee to cover multiple potential transactions? If they are not successful in purchasing the target property, is the fee refundable? He appeared to be advocating paying the fee before putting a bid in, one fee for multiple bids, and refundable if unsuccessful.

However to decide, we need to know if the fee is simply to cover the cost of appropriate agency administration, or whether it is designed to be a barrier to transact. It is not clear for the available material which is envisaged. Administration would be a combination of assessing the credential of the individual (so once per person), and also the property (so once per property). Also, if unsuccessful, is it appropriate to refund the entire fee? After all, the work needs to be done before allowing a bid (else if you only pay after a successful transaction, what happens if you were declined subsequently, once you have contracted to purchase?)

He also confirmed there had been no action taken on a residential purchase by a foreigner since 2006, adequate data was not being collected, and cross agency communication was not effective.

Clearly more work needs to be done to design this right. DFA suggests that a foreign investor should be able to make application for approval to purchase property in Australia. This should be a licence, which needs to be maintained and renewed from time to time. Then there would be a fee payable on each property application. This latter fee would be refundable in the case of an unsuccessful sale. It would also reduce the red tape so some extent.

FCC And Net Neutrality

Net neutrality is important because it means that internet service providers need to make all content available from providers to consumers without any differentiation in terms of charging or quality of service for different types of traffic. It can apply to content including telephony, web browsing, video, television, and other digital services. Following legal battles in the USA, the Federal Communications Commission has set sustainable rules of the roads that will protect free expression and innovation on the Internet and promote investment in the nation’s broadband networks. It is an important stake in the ground, and means the internet will be more open, not less. So far as Australia is concerned, we think it is time to consider the right neutrality settings here. Today we have rules which assume television broadcasting is different from other content, and various barriers which limit competition, consumer choice, and keep content pricing higher than they should be. Given the emerging role of the NBN, It’s time that Australia carried out a broad based review into net neutrality and how it should be applied to the local telecommunications and content provider industries.

Here are details of the US announcement.

The FCC has long been committed to protecting and promoting an Internet that nurtures freedom of speech and expression, supports innovation and commerce, and incentivizes expansion and investment by America’s broadband providers. But the agency’s attempts to implement enforceable, sustainable rules to protect the Open Internet have been twice struck down by the courts.

The Commission—once and for all—enacts strong, sustainable rules, grounded in multiple sources of legal authority, to ensure that Americans reap the economic, social, and civic benefits of an Open Internet today and into the future. These new rules are guided by three principles: America’s broadband networks must be fast, fair and open—principles shared by the overwhelming majority of the nearly 4 million commenters who participated in the FCC’s Open Internet proceeding. Absent action by the FCC, Internet openness is at risk, as recognized by the very court that struck down the FCC’s 2010 Open Internet rules last year in Verizon v. FCC.

Broadband providers have economic incentives that “represent a threat to Internet openness and could act in ways that would ultimately inhibit the speed and extent of future broadband deployment,” as affirmed by the U.S. Court of Appeals for the District of Columbia. The court upheld the Commission’s finding that Internet openness drives a “virtuous cycle” in which innovations at the edges of the network enhance consumer demand, leading to expanded investments in broadband infrastructure that, in turn, spark new innovations at the edge.

However, the court observed that nearly 15 years ago, the Commission constrained its ability to protect against threats to the open Internet by a regulatory classification of broadband that precluded use of statutory protections that historically ensured the openness of telephone networks. The Order finds that the nature of broadband Internet access service has not only changed since that initial classification decision, but that broadband providers have even more incentives to interfere with Internet openness today. To respond to this changed landscape, the new Open Internet Order restores the FCC’s legal authority to fully address threats to openness on today’s networks by following a template for sustainability laid out in the D.C. Circuit Opinion itself, including reclassification of broadband Internet access as a telecommunications service under Title II of the Communications Act.

With a firm legal foundation established, the Order sets three “bright-line” rules of the road for behavior known to harm the Open Internet, adopts an additional, flexible standard to future-proof Internet openness rules, and protects mobile broadband users with the full array of Open Internet rules. It does so while preserving incentives for investment and innovation by broadband providers by affording them an even more tailored version of the light-touch regulatory treatment that fostered tremendous growth in the mobile wireless industry.

Following are the key provisions and rules of the FCC’s Open Internet Order:

New Rules to Protect an Open Internet

While the FCC’s 2010 Open Internet rules had limited applicability to mobile broadband, the new rules—in their entirety—would apply to fixed and mobile broadband alike, recognizing advances in technology and the growing significance of wireless broadband access in recent years (while recognizing the importance of reasonable network management and its specific application to mobile and unlicensed Wi-Fi networks). The Order protects consumers no matter how they access the Internet, whether on a desktop computer or a mobile device.

Bright Line Rules: The first three rules ban practices that are known to harm the Open Internet:

- No Blocking: broadband providers may not block access to legal content, applications, services, or non-harmful devices.

- No Throttling: broadband providers may not impair or degrade lawful Internet traffic on the basis of content, applications, services, or non-harmful devices.

- No Paid Prioritization: broadband providers may not favor some lawful Internet traffic over other lawful traffic in exchange for consideration of any kind—in other words, no “fast lanes.” This rule also bans ISPs from prioritizing content and services of their affiliates.

The bright-line rules against blocking and throttling will prohibit harmful practices that target specific applications or classes of applications. And the ban on paid prioritization ensures that there will be no fast lanes.

A Standard for Future Conduct:

Because the Internet is always growing and changing, there must be a known standard by which to address any concerns that arise with new practices. The Order establishes that ISPs cannot “unreasonably interfere with or unreasonably disadvantage” the ability of consumers to select, access, and use the lawful content, applications, services, or devices of their choosing; or of edge providers to make lawful content, applications, services, or devices available to consumers. Today’s Order ensures that the Commission will have authority to address questionable practices on a case-by-case basis, and provides guidance in the form of factors on how the Commission will apply the standard in practice.

Greater Transparency:

The rules described above will restore the tools necessary to address specific conduct by broadband providers that might harm the Open Internet. But the Order recognizes the critical role of transparency in a well-functioning broadband ecosystem. In addition to the existing transparency rule, which was not struck down by the court, the Order requires that broadband providers disclose, in a consistent format, promotional rates, fees and surcharges and data caps. Disclosures must also include packet loss as a measure of network performance, and provide notice of network management practices that can affect service. To further consider the concerns of small ISPs, the Order adopts a temporary exemption from the transparency enhancements for fixed and mobile providers with 100,000 or fewer subscribers, and delegates authority to our Consumer and Governmental Affairs Bureau to determine whether to retain the exception and, if so, at what level. The Order also creates for all providers a “safe harbor” process for the format and nature of the required disclosure to consumers, which the Commission believes will lead to more effective presentation of consumer-focused information by broadband providers.

Reasonable Network Management:

For the purposes of the rules, other than paid prioritization, an ISP may engage in reasonable network management. This recognizes the need of broadband providers to manage the technical and engineering aspects of their networks.

- In assessing reasonable network management, the Commission’s standard takes account of the particular engineering attributes of the technology involved—whether it be fiber, DSL, cable, unlicensed Wi-Fi, mobile, or another network medium.

- However, the network practice must be primarily used for and tailored to achieving a legitimate network management—and not business—purpose. For example, a provider can’t cite reasonable network management to justify reneging on its promise to supply a customer with “unlimited” data.

Broad Protection

Some data services do not go over the public Internet, and therefore are not “broadband Internet access” services (VoIP from a cable system is an example, as is a dedicated heart-monitoring service). The Order ensures that these services do not undermine the effectiveness of the Open Internet rules. Moreover, all broadband providers’ transparency disclosures will continue to cover any offering of such non-Internet access data services—ensuring that the public and the Commission can keep a close eye on any tactics that could undermine the Open Internet rules.

Interconnection: New Authority to Address Concerns

For the first time the Commission can address issues that may arise in the exchange of traffic between mass-market broadband providers and other networks and services. Under the authority provided by the Order, the Commission can hear complaints and take appropriate enforcement action if it determines the interconnection activities of ISPs are not just and reasonable.

Legal Authority: Reclassifying Broadband Internet Access under Title II

The Order provides the strongest possible legal foundation for the Open Internet rules by relying on multiple sources of authority including both Title II of the Communications Act and Section 706 of the Telecommunications Act of 1996. At the same time, the Order refrains – or forbears – from enforcing 27 provisions of Title II and over 700 associated regulations that are not relevant to modern broadband service. Together Title II and Section 706 support clear rules of the road, providing the certainty needed for innovators and investors, and the competitive choices and freedom demanded by consumers, while not burdening broadband providers with anachronistic utility-style regulations such as rate regulation, tariffs or network sharing requirements.

- First, the Order reclassifies “broadband Internet access service”—that’s the retail broadband service Americans buy from cable, phone, and wireless providers—as a telecommunications service under Title II. This decision is fundamentally a factual one. It recognizes that today broadband Internet access service is understood by the public as a transmission platform through which consumers can access third-party content, applications, and services of their choosing. Reclassification of broadband Internet access service also addresses any limitations that past classification decisions placed on the ability to adopt strong open Internet rules, as interpreted by the D.C. Circuit in the Verizon case. And it supports the Commission’s authority to address interconnection disputes on a case-by-case basis, because the promise to consumers that they will be able to travel the Internet encompasses the duty to make the necessary arrangements that allow consumers to use the Internet as they wish.

- Second, the proposal finds further grounding in Section 706 of the Telecommunications Act of 1996. Notably, the Verizon court held that Section 706 is an independent grant of authority to the Commission that supports adoption of Open Internet rules. Using it here—without the limitations of the common carriage prohibition that flowed from earlier the “information service” classification—bolsters the Commission’s authority.

- Third, the Order’s provisions on mobile broadband also are based on Title III of the Communications Act. The Order finds that mobile broadband access service is best viewed as a commercial mobile service or its functional equivalent.

Forbearance: A modernized, light-touch approach

Congress requires the FCC to refrain from enforcing – forbear from – provisions of the Communications Act that are not in the public interest. The Order applies some key provisions of Title II, and forbears from most others. Indeed, the Order ensures that some 27 provisions of Title II and over 700 regulations adopted under Title II will not apply to broadband. There is no need for any further proceedings before the forbearance is adopted. The proposed Order would apply fewer sections of Title II than have applied to mobile voice networks for over twenty years.

• Major Provisions of Title II that the Order WILL APPLY:

- The proposed Order applies “core” provisions of Title II: Sections 201 and 202 (e.g., no unjust or unreasonable practices or discrimination)

- Allows investigation of consumer complaints under section 208 and related enforcement provisions, specifically sections 206, 207, 209, 216 and 217

- Protects consumer privacy under Section 222

- Ensures fair access to poles and conduits under Section 224, which would boost the deployment of new broadband networks

- Protects people with disabilities under Sections 225 and 255

- Bolsters universal service fund support for broadband service in the future through partial application of Section 254.

• Major Provisions Subject to Forbearance:

- Rate regulation: the Order makes clear that broadband providers shall not be subject to utility-style rate regulation, including rate regulation, tariffs, and last-mile unbundling.

- Universal Service Contributions: the Order DOES NOT require broadband providers to contribute to the Universal Service Fund under Section 254. The question of how best to fund the nation’s universal service programs is being considered in a separate, unrelated proceeding that was already underway.

- Broadband service will remain exempt from state and local taxation under the Internet Tax Freedom Act. This law, recently renewed by Congress and signed by the President, bans state and local taxation on Internet access regardless of its FCC regulatory classification.

Effective Enforcement - The FCC will enforce the Open Internet rules through investigation and processing of formal and informal complaints

- Enforcement advisories, advisory opinions and a newly-created ombudsman will provide guidance

- The Enforcement Bureau can request objective written opinions on technical matters from outside technical organizations, industry standards-setting bodies and other organizations.

Fostering Investment and Competition

All of this can be accomplished while encouraging investment in broadband networks. To preserve incentives for broadband operators to invest in their networks, the Order will modernize Title II using the forbearance authority granted to the Commission by Congress—tailoring the application of Title II for the 21st century, encouraging Internet Service Providers to invest in the networks on which Americans increasingly rely.

- The Order forbears from applying utility-style rate regulation, including rate regulation or tariffs, last-mile unbundling, and burdensome administrative filing requirements or accounting standards.

- Mobile voice services have been regulated under a similar light-touch Title II approach, and investment and usage boomed.

- Investment analysts have concluded that Title II with appropriate forbearance is unlikely to have any negative on the value or future profitability of broadband providers. Providers such as Sprint, Frontier, as well as representatives of hundreds of smaller carriers that have voluntarily adopted Title II regulation, have likewise said that a light-touch, Title II classification of broadband will not depress investment.

Mortgage Arrears Higher In Mining Post Codes – Fitch

Fitch Ratings says in a new report that a reduction in mining investment and slower mining industry employment has resulted in higher delinquency rates over the past 18 months in areas where a significant population is employed in the industry, compared with delinquencies in non-mining areas.

Only 0.8% of Australian mortgages are located in mining postcodes (defined by Fitch as postcodes in which more than 20% of residents worked in the mining industry – employment based on 2011 census data). As a result, mortgages in Australia performed well overall, thanks to the stable economy, steady unemployment rate and record-low mortgage rates.

While Fitch expects the rapid change in industry dynamics that has occurred in the mining sector to impact both mortgage delinquencies and local property markets, Australian RMBS transactions are typically well-diversified geographically. As a result, Fitch does not expect the fall in mining employment to have a material effect on securitised portfolios and does not expect it to affect RMBS ratings in the medium term.

The Reform Imperative

John Fraser, Secretary to the Treasury spoke today to the Committee for Economic Development of Australia (CEDA). The speech, “Australia’s Economic Policy Challenges” outlined some important priorities for economic reform, as well as setting out the background to the reform imperative.

Boosting productivity will require improvements across all markets – input markets such as the labour market, financial markets, and infrastructure markets as well as final goods and services markets. Failure to undertake necessary reforms in related markets will mean that the potential benefits of reform in any single market are not realised. The Government has commissioned a number of policy reviews that will recommend ways to enhance Australia’s economic prosperity. Making the most of these reform opportunities is essential, where three areas stand out as priorities for raising Australia’s productivity performance.

The first is tax reform.

Studies have consistently shown that tax reform offers one of the largest policy opportunities to increase incomes and living standards. And the fact is that the structure of our tax system today looks remarkably like it did back in the 1950s — but our economy looks very different. That may tell us something. Tax reform can promote strong investment and encourage workforce participation. Our company tax rate is high by international standards. In the context of far more mobile capital, high tax rates are dampening investment and productivity, while continuing personal income tax bracket creep would have negative impacts on workforce participation and incentives. An important criterion for a well-functioning tax system is fairness, where there are some contentious and important issues that need to be explored. For example, substantial tax assistance is provided to superannuation savings. We need to consider whether the level and distribution of these concessions remains appropriate. These are the types of issues that will be considered in the upcoming Tax White Paper.

A second priority is continuing to modernise the workplace relations system.

Workplace regulation has been progressively and substantially reformed in recent decades. Many of the fundamental reforms were undertaken in the 1980s and 1990s, in particular the shift from centralised wage fixing to enterprise bargaining. These reforms have delivered substantial benefits. But elements of our workplace relations system may need to change to fit the workplaces of our future. The Productivity Commission’s Inquiry into the Workplace Relations Framework to be delivered later this year will be an important opportunity to create a modern system that will support jobs, promote productivity and lift living standards. A more flexible workplace relations system that supports the economy will help Australia respond to the challenge of lifting productivity growth. The rise of Asia, the ageing of the population and the transition away from resource-led growth will require significant adjustment. It is especially important that workplace laws are not impeding workplace transformation.

A third priority area for structural reform is driving greater competition in goods and services markets.

Previous product market reforms, and those associated with the Hilmer review in the 1990s, pushed competition into non-tradable sectors like electricity, telecommunications and rail freight. These were important changes, contributing to a GDP increase of around 2½ percentage points over the course of that decade. The proposals in Ian Harper’s draft report released in late 2014 provide the opportunity to boost Australia’s productivity performance. The final report will be released in March. Ian Harper proposes that we apply competition law and a new set of competition principles to all purchasing activities of government such as health, education and aged care. Even small improvements here, where government has a large footprint and where Australia’s population will impose greater demands on health and aged care, can deliver big benefits over time. The importance of strengthening competition was also a theme of the Financial System Inquiry. The Inquiry concludes that competition and competitive markets are at the heart of the philosophy of the financial system and the primary means of supporting the system’s efficiency. We must ensure that our banking and financial system more generally are more competitive. The Inquiry also recognised that, as the financial system becomes increasingly sophisticated and innovative, the importance of receiving appropriate financial advice and access to appropriate and competitively priced products has increased.

These are challenging issues and will require the Commonwealth and the State governments to work together.

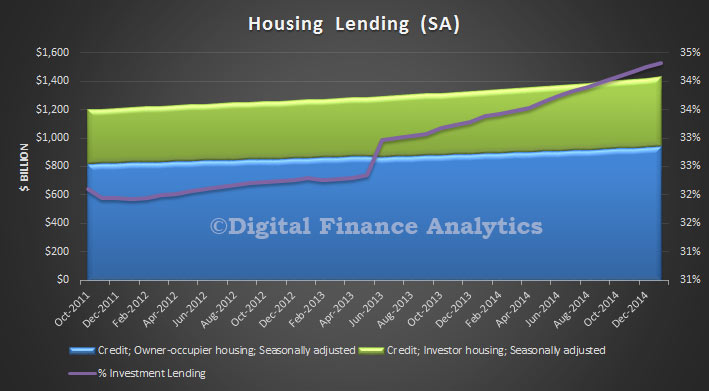

Home Lending Up To $1.43 Trillion

Latest data from the RBA shows that home lending is worth $1.43 trillion, to end January. In the month, lending rose $8.5 billion, or 0.6%. However, investment home lending grew at 0.8%, whilst owner occupied lending grew at 0.49%. Investment lending was at a record 34.3% of total housing.

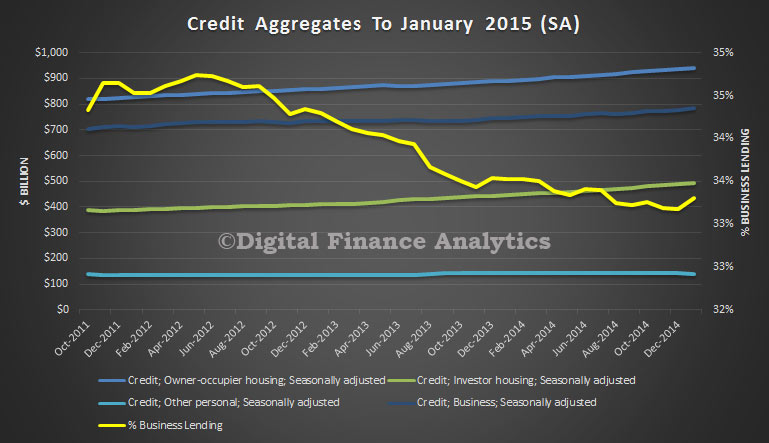

More broadly, total lending was up 0.6% from last month, and 6.2% year on year. The share of lending to business continued to fall as a share of total lending, now down to one third of all funds borrowed. This needs to be lifted if sustainable growth is to be delivered. Banks are biased toward ever more home lending, thanks to lower losses and advantaged capital requirements.

More broadly, total lending was up 0.6% from last month, and 6.2% year on year. The share of lending to business continued to fall as a share of total lending, now down to one third of all funds borrowed. This needs to be lifted if sustainable growth is to be delivered. Banks are biased toward ever more home lending, thanks to lower losses and advantaged capital requirements.

Groupthink Stems From The Council of Financial Regulators

Behind the scenes, it is the mysterious Council of Financial Regulators which is coordinating activity across the Reserve Bank, APRA, AISC and Treasury. This body, is the conductor of the regulatory orchestra, and although formed initially in 1998, it has only had an independent website since 2013. It is the coordinating body for Australia’s main financial regulatory agencies. It is a non-statutory body whose role is to contribute to the efficiency and effectiveness of financial regulation and to promote stability of the Australian financial system. The Reserve Bank of Australia (RBA) chairs the Council and members include the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC), and The Treasury. The Council of Financial Regulators (CFR) comprises two representatives – the chief executive and a senior representative – from each of these four member agencies.

The CFR meets in person quarterly or more often if circumstances require it. The meetings are chaired by the RBA Governor, with secretariat support provided by the RBA. In the CFR, members share information, discuss regulatory issues and, if the need arises, coordinate responses to potential threats to financial stability. The CFR also advises Government on the adequacy of Australia’s financial regulatory arrangements. A formal charter was only adopted on 13 January 2014.

The Council of Financial Regulators (CFR) aims to facilitate cooperation and collaboration between the Reserve Bank of Australia, the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission and The Treasury. Its ultimate objectives are to contribute to the efficiency and effectiveness of regulation and to promote stability of the Australian financial system.

The CFR provides a forum for:

- identifying important issues and trends in the financial system, including those that may impinge upon overall financial stability;

- ensuring the existence of appropriate coordination arrangements for responding to actual or potential instances of financial instability, and helping to resolve any issues where members’ responsibilities overlap; and

- harmonising regulatory and reporting requirements, paying close attention to the need to keep regulatory costs to a minimum.

So, given the intended independence of the RBA, from Government, there is an important question to consider. How can this be seen to be true? More likely, we think there is significant potential for groupthink. In addition, no minutes of discussions are made public. We think its time for greater transparency and openness.

“Sunlight is said to be the best of disinfectants; electric light the most efficient policeman” said U.S. Supreme Court Justice Louis Brandeis. We agree.

Reforms to the Bank of England’s Market Intelligence programme

Some central banks, including the Bank of England, have moved away from an era of ‘constructive ambiguity’ to greater openness and transparency. The RBA is less transparent, and the Australian Regulatory system is opaque and largely still done behind closed doors and quiet whispers. This is because they are too aligned to the major financial services incumbents, and are over focussed on financial stability. In particular the role and activity of the Council of Financial Regulators is completely opaque. So it is interesting to see where the Bank of England is headed.

The Bank of England today announced the outcome of a root-and-branch review of its Market Intelligence (MI) programme. In a speech at Warwick University, Minouche Shafik said the resulting changes – alongside progressive steps to make the Bank’s liquidity insurance framework more transparent – show clearly that the Bank is not just “open for business” but also “open about our business.”

MI is the ongoing process of discussion with financial market participants to identify insights relevant to policymaking. The Bank’s Governors and Court of Directors endorsed all 11 recommendations stemming from the MI Review, which will make the gathering and use of MI more transparent, robust and effective. The recommendations include:

- A MI Charter which explains clearly the terms of the Bank’s engagement with financial market participants, and its rationale for gathering MI;

- A strengthened set of policies that govern MI gathering, supported by expanded training for staff; and

- A new executive-level committee to oversee the MI programme, to ensure it retains the necessary flexibility, focus and relevance to the policy challenges of today and tomorrow.

The Bank of England also today published its formal response to the recommendations of Lord Grabiner, following the publication of his Foreign Exchange Market Investigation Report in November 2014. At the time, the Bank endorsed the recommendations – which covered documentation, education, and the need for greater clarity over the Bank’s market intelligence role – and committed to implementing them in full and as quickly as possible.

In today’s response, the Bank outlined the actions that have been, or are being, taken to fulfil the recommendations. They will result in stronger systems and controls around the Bank’s engagement with market participants.

In a speech on Thursday – Goodbye ambiguity, hello clarity – Bank of England Deputy Governor Minouche Shafik explains why this greater clarity around the Bank of England’s interactions with financial markets is essential.

Central banks, including the Bank of England, have moved away from an era of ‘constructive ambiguity’ to greater openness and transparency. For example, the Bank now has a well-defined set of facilities for the provision of liquidity to the financial system that have evolved to meet changing needs. The Bank’s dialogue with markets dates back to 1786 but the days of men in top hats and fireside chats are now a distant memory. The Bank’s MI function is a highly professional network of staff covering 23 different markets and sectors, providing first-hand insights on short-term moves and long-term trends relevant to all the Bank’s policy functions.

In the speech, Minouche says:

“The ability of the Bank’s MI function to provide insights to senior policymakers over the past 8 years, as the first waves of the crisis rushed onto the Bank’s doorstep, and then as solutions flowed back out across the system, has been vital to our effectiveness”.

Welcoming the changes to the MI programme announced today, Minouche said:

“The Bank has been at the centre of one of the world’s major financial centres for hundreds of years. Today the Bank has a broader role than ever before. A clear understanding of the root causes of developments in financial markets must underpin the decisions we make about monetary policy and regulation of financial markets. Aligning our Market Intelligence function closely to the Bank’s mission, so that its purpose is clear and its approach is transparent, will ensure we continue to seize that opportunity”.

Capex On The Slide

The ABS data released today shows the continued fall in mining expenditure, and no counterbalancing movement in other sectors. Total new capital expenditure trend estimate was $37,693 m, down 3.9% YOY.

It does not bode well. Business confidence remains low, and given that household debt is still high, we do not expect housing, and households to fill the gap. We are effectively running out of runway as mining investment trails off. So, housing is the only game in town. Given the data now, it is much more likely we will see interest rates lower for longer than previously anticipated. However, the continued reliance on unproductive lending for housing in not a recipe to drive business investment. We need some new thinking on how to stimulate business investment. Our surveys suggest that it is not interest rates which is the problem, so cutting further wont help much. APRA needs to step up here, turn to tap down on housing lending, and make business lending more likely. The details of the ABS data are summarised below.

- The trend volume estimate for total new capital expenditure fell 0.8% in the December quarter 2014 while the seasonally adjusted estimate fell 2.2%.

- The trend volume estimate for buildings and structures fell 1.5% in the December quarter 2014 while the seasonally adjusted estimate fell 2.6%.

- The trend volume estimate for equipment, plant and machinery rose 0.9% in the December quarter 2014 while the seasonally adjusted estimate fell 1.3%.

- This issue includes the fifth estimate (Estimate 5) for 2014-15 and the first estimate (Estimate 1) for 2015-16.

- Estimate 5 for 2014-15 is $152,656m. This is 8.6% lower than Estimate 5 for 2013-14. Estimate 5 is 0.4% higher than Estimate 4 for 2014-15.

- Estimate 1 for 2015-16 is $109,799m. This is 12.4% lower than Estimate 1 for 2014-15.

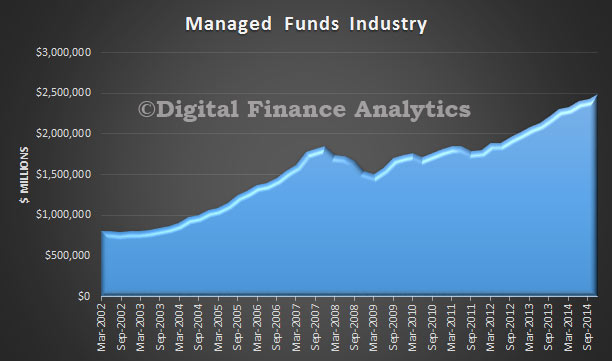

Funds Under Management Now $2.5 Trillion

ABS released their funds management data to December 2014. The managed funds industry had $2,489.9b funds under management (including some changes to the data capture and revisions), an increase of $57.6b (2%) on the September quarter 2014 figure of $2,432.3b. The main valuation effects that occurred during the December quarter 2014 were:

- the S&P/ASX 200 increased 2.2%

- the price of foreign shares, as represented by the MSCI World Index excluding Australia, increased 0.8%

- A$ depreciated 6.7% against the US$.

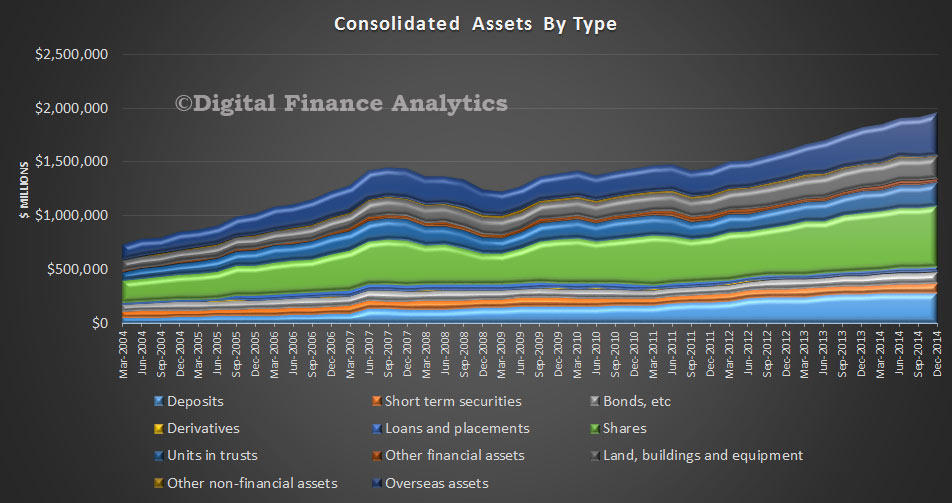

At 31 December 2014, the consolidated assets of managed funds institutions were $1,958.5b, an increase of $48.8b (3%) on the September quarter 2014 figure of $1,909.7b. The asset types that increased were:

At 31 December 2014, the consolidated assets of managed funds institutions were $1,958.5b, an increase of $48.8b (3%) on the September quarter 2014 figure of $1,909.7b. The asset types that increased were:

- overseas assets, $29.6b (8%)

- shares, $14.6b (3%)

- short term securities, $8.6b (10%)

- bonds, etc., $4.3b (4%)

- derivatives, $0.8b (65%)

- other non-financial assets, $0.2b (2%).

These were partially offset by decreases in:

- other financial assets, $3.4b (11%)

- deposits, $3.2b (1%)

- land, buildings and equipment, $1.5b (1%)

- loans and placements, $1.0b (2%)

- and units in trusts, $0.2b (0%).

At 31 December 2014, there were $503.9b of assets cross invested between managed funds institutions whilst the unconsolidated assets of superannuation (pension) funds increased $54.4b (3%), public offer (retail) unit trusts increased $4.5b (2%), life insurance corporations increased $4.3b (2%), cash management trusts increased $0.8b (3%), and common funds increased $0.2b (2%). Friendly societies were flat.

At 31 December 2014, there were $503.9b of assets cross invested between managed funds institutions whilst the unconsolidated assets of superannuation (pension) funds increased $54.4b (3%), public offer (retail) unit trusts increased $4.5b (2%), life insurance corporations increased $4.3b (2%), cash management trusts increased $0.8b (3%), and common funds increased $0.2b (2%). Friendly societies were flat.