This from Business Insider. British banking pioneer Anthony Thomson, the entrepreneur who co-founded the highly successful Metro Bank in the wake of the GFC (the UK’s first new high street bank in 150 years), and in 2014, the country’s first digital bank, the now publicly listed Atom, has set his sights on Australia with a new digital challenger bank.

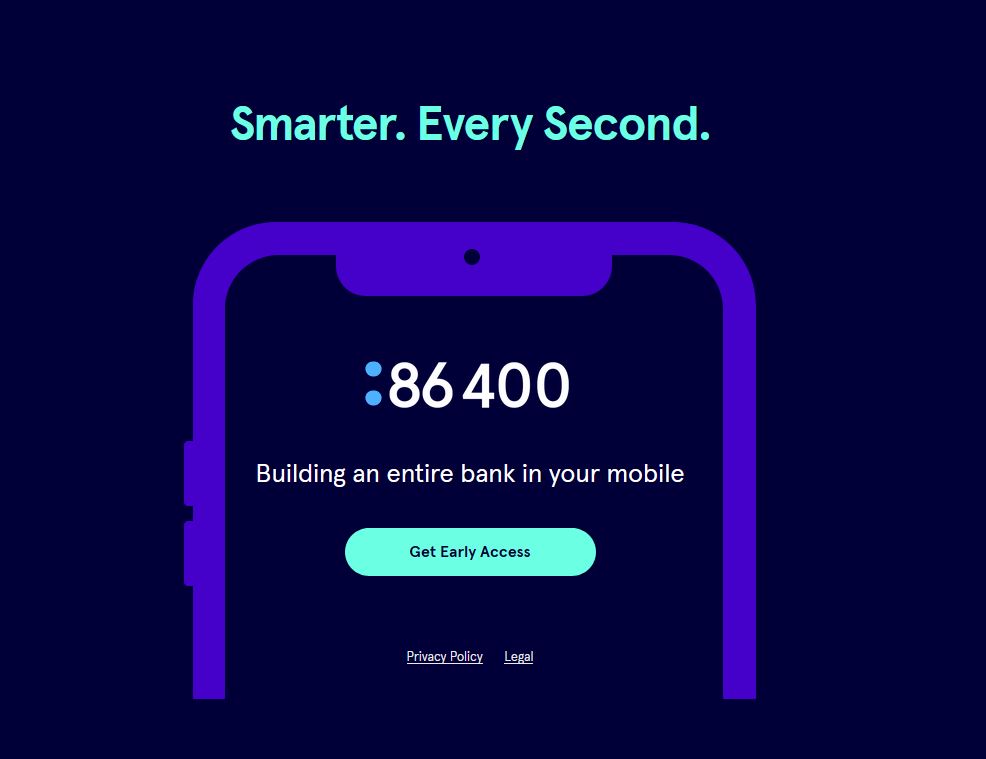

Banking startup 86 400 (named after the seconds in a day) will launch in early 2019, and is wholly funded by the Sydney-based payments services company Cuscal, best known for rediATMs.

Thomson has signed on as chairman with former ANZ Japan CEO, Robert Bell as CEO. Cuscal Payments CIO Brian Parker takes on that role at 86 400.

The heavy-hitting management team also includes Westpac’s former digital GM, Travis Tyler; CBA’s former International Chief Risk Officer, Guy Harding, as CRO; and Cuscal’s former Head of Finance, Neal Hawkins, as CFO.

While the project has been set up and funded by Cuscal (which is part-owned by the likes of Bendigo Bank and Mastercard) – one of the key architects of the New Payments Platform (NPP), a real-time payments system – it will operate as a separate entity, with a separate board and team.

NPP is at the core of 86 400’s real-time banking pitch, something Thomson says the big banks “have been very slow to make available”.

The neobank will look to raise more than $250 million capital over the first three years of operation and will likely take additional shareholders on board.

Having raised more than $AU1 billion for his previous ventures, Thomson says 86 400 is his “best prepared, most capable and well-funded venture to date” and in “the unique position of not going out to look for money”.

And he’s not mucking around.

“I’m not here to build a small bank. We’re here to build a big bank,” he said.

Eight years on, Metro Bank is worth $AU1.95 billion with annual revenues in excess of $AU500 million, having floated in 2014.

By October last year, Atom – Thomson left the business in January – had around £900 million ($AU1.6 billion) in deposits, but lost £42 million ($AU75m) in 2016.

86 400’s app-based banking has been 18 months in development, with a team of 60 based in Sydney, amid conversations with Australian Prudential Regulation Authority (APRA) for a full banking license as an Authorised Deposit-taking Institution (ADI) expected by the end of the year.

It plans to launch in beta towards the end of 2018 before going public in the first quarter of 2019 with a transaction and savings account. It will operate on both iOS and Android smartphones.

The launch comes amid a litany of complaints about the behaviour of the Big Four banks at the royal commission into misconduct in the financial services sector.

Cuscal managing director Craig Kennedy, said the organisation put forward the idea because they believed “nobody in Australia is leveraging all of the capabilities available to maximise the banking experience on your mobile”.

Cuscal produced Australia’s leading white-label mobile banking app, and has led the way in digital banking solutions.

Thomson, who last year invested in Melbourne-based fintech startup, Timelio, said Australia needed another bank “because the big banks have treated customers really, really badly”.

“Look at the levels of dissatisfaction with the banks… all of the big banks have negative net promotor scores,” he said.

“I read a piece of data which really stuck in my mind. It was from the Australia Institute and said that 2.9% of Australian GDP goes to bank profits. So $3 out of every $100 hardworking Australians make in their businesses goes to the banks in profits. This is just enormous. It’s three times bigger than the UK – and I think the UK banks rip off their consumers.

“So I think there’s a real opportunity to create the first real alternative to the real banks. Someone who does put the customer first.”

Like other digital startups, part of the opportunity CEO Robert Bell sees is avoiding the baggage around the industry’s incumbents.

“Large banks have an enormous drag in terms of very big, costly legacy real estate/branch networks, legacy technology that’s very expensive to change. Most of their digital pieces have been add-ons,” he said.

“We’ve got the huge advantage that we’re starting from scratch.”

The heart of 86 400 is its investment in what Bell calls “digital working memory”. It’s data analysis that has the potential to warn you like a parent or spouse about when you’re being a spendthrift – budgeting for the avocado toast generation – with a predictive cashflow model.

“For example, helping customers know what there balance will be in one week’s time or four week’s time if the normal things that happen in their life happen over the next couple of weeks,” he said.

“No one gives any insight into what might happen in the future.”

Thomson says: “As we get to know you, and with your permission, we can use the data to better predict what your needs are going to be. So we know that in summer you go on holidays and your insurance comes up for renewal, we can start to model that and bring it to you attention in advance”.

If you’re the sort of person who runs out of cash three days before your next payday, it could come in handy to amend your spending habits.

Bell says 86 400 plans to launch with no or low fee accounts as “just the start”, promising “value customers have never had from a bank before”.

86 400’s launch could potentially take advantage of growing resentment towards the major banks in the wake of the royal commission.

While dissatisfaction may be growing, customer churn remains surprisingly low. However, the banks are facing something of the perfect storm of a potential margin squeeze from a likely rise wholesale funding costs ahead, at the same time that credit growth has risen faster than deposit growth in recent months.

The risk of out-of-cycle mortgage rate increases is rising in Australia, giving borrowers another reason to start shopping around.

While Thomson and Bell were keen to downplay any focus on interest rates for 86 400’s potential savers and borrowers, the neobank’s tech-focused low operating costs will negate pressure on its margins as it cases new business.