As the property market cools, some developers are getting into the lending game (and of course outside APRA supervision). First Time Buyers are significant targets.

Property developer Catapult Property Group has launched a new lending division that will help first home buyers get home loans with a deposit of only $5,000.

The Brisbane-based company encourages first home buyers in Queensland to enter the real estate market now by taking advantage of the state government’s $20,000 grant that is ending on 30 June 2018.

Catapult director for residential lending Paul Anderson said first home buyers do not require a 20% deposit plus fees to enter the property market.

“There are many banks that are happy to finance a purchase from as little as 5% deposit and in some cases even less than that,” he said. “When working with property specialists such as Catapult Property Group who have the builder, broker and financial advisors under the one roof, it’s possible to secure a loan with as little as $5,000.”

To get a home loan with a minimal deposit, the company requires that applicants have a full-time job with a stable employment history, a consistent rental payment record, and a clear credit score.

Borrowers may also need to get lenders’ mortgage insurance.

“Mortgage insurance on a $450,000 home purchase with a minimal deposit usually ranges from $7,000 to $14,000, which is added to your mortgage. This is a more realistic means of entering the property market than trying to save a potentially unattainable amount of around $100,000 for a deposit,” said Anderson.

The company says it has almost $130m of residential projects in Queensland and NSW.

More evidence of inflation lurking in the US economy, as the headline rate for January was higher than expected. This gives more support to the view the FED will indeed lift interest rates.

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.5 percent in January on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index rose 2.1 percent before seasonal adjustment.

The seasonally adjusted increase in the all items index was broad-based, with increases in the indexes for gasoline, shelter, apparel, medical care, and food all contributing. The energy index rose 3.0 percent in January, with the increase in the gasoline index more than offsetting declines in other energy component indexes. The food index rose 0.2 percent with the indexes for food at home and food away from home both rising.

The index for all items less food and energy increased 0.3 percent in January. Along with shelter, apparel, and medical care, the indexes for motor vehicle insurance, personal care, and used cars and trucks also rose in January. The indexes for airline fares and new vehicles were among those that declined over the month.

The all items index rose 2.1 percent for the 12 months ending January, the same increase as for the 12 months ending December. The index for all items less food and energy rose 1.8 percent over the past year, while the energy index increased 5.5 percent and the food index advanced 1.7 percent.

ASIC welcomes the passage through Parliament of the Bill to establish the Australian Financial Complaints Authority (AFCA).

AFCA will be the culmination of more than 20 months of public consultation and inquiry, commencing with the review of the dispute resolution framework by an independent panel led by Melbourne Law School’s Professor Ian Ramsay.

ASIC Deputy Chair Peter Kell said, ‘Fair, timely and effective dispute resolution is a cornerstone of the financial services consumer protection framework. The combination of firms’ internal dispute resolution procedures and access to a free independent external scheme currently provides redress for many tens of thousands of Australians each year. Strengthening these dispute resolution requirements will help deliver higher standards and better outcomes in the financial services market.’

‘The establishment of a single scheme for all financial services and superannuation complaints is a very positive development, building on the outcomes achieved over many years by the existing three schemes: the Financial Ombudsman Service (FOS), the Credit and Investments Ombudsman (CIO) and the Superannuation Complaints Tribunal.’

Higher monetary limits and compensation caps, including for primary production businesses, will give more consumers and small businesses access to a free and independent forum to resolve their complaints.

ASIC will work with Government and scheme stakeholders to ensure that the transition to the commencement of AFCA is as smooth as possible. In the interim, ASIC will retain direct oversight of the two ASIC-approved schemes – FOS and CIO – which will continue to provide high levels of service to consumers and firms. Separate arrangements are in place for the ongoing operation of the SCT to enable it to deal with existing complaints.

Important information about transition

AFCA will start accepting complaints no later than 1 November 2018

The operator of the scheme will be authorised by the Minister, and the scheme will be subject to ongoing oversight by ASIC.

In order to maintain access to external dispute resolution for consumers in the lead up to commencement of AFCA, ASIC will monitor member compliance with existing EDR scheme requirements as well as the effectiveness of scheme operations.

Members of each of CIO and FOS – including licensees and credit representatives – must continue to maintain their EDR membership through this period, including paying membership and other scheme fees in full as required. ASIC has asked the two schemes to report any failure of members to do so.

A memorandum of understanding between CIO and FOS will prevent members inappropriately moving between the schemes in the transition period.

ASIC will be consulting soon on updated Regulatory Guide 139 (REG 139), which will set out details of ASIC’s oversight of AFCA. This will be finalised and published when AFCA commences operations.

ASIC will also publicly consult on new IDR standards and the mandatory IDR reporting requirements that are also contained in the AFCA Bill – but this consultation will not take place until afterAFCA commencement.

Current legislative IDR requirements for superannuation trustees and retirement savings account providers (including 90-day timeframes and requirements for written reasons) will continue to apply in their current form until ASIC consults on and then issues updated IDR policy (RG 165).

ANZ today noted the release of the Australian Prudential Regulation Authority’s (APRA) discussion paper on revisions to capital requirements and confirmed ANZ’s APRA CET1 position of 10.8% as at December 2017 is already in compliance with APRA’s existing Unquestionably Strong requirements.

The paper outlines proposed changes to the capital framework following the finalisation of the Basel III reforms in December 2017 and changes to its risk framework, with APRA’s implementation timetable extending to 2021.

ANZ will continue to consult with APRA to fully understand the impact of the proposed changes. APRA has confirmed that if the proposed changes result in an overall increase in risk weighted assets, it will reduce the capital ratio benchmark of 10.5% flagged in July 2017.

ANZ’s current capital ratio of 10.8% includes the proceeds of the sale of Shanghai Rural Commercial Bank and a small benefit of the sale of its Asian retail and wealth businesses. Further benefits will be achieved following completion of other asset sales, including the sale of the Australian wealth businesses.

APRA has also proposed a minimum leverage ratio requirement of 4% for Internal Ratings-Based (IRB) banks and changes to the leverage ratio exposure measure calculations for implementation by 1 July 2019. ANZ’s leverage ratio at December 2017 is 5.5%.

ANZ’s previously announced buy-back up to $1.5 billion of shares on-market relating to the sale of ANZ’s 20% stake in Shanghai Rural Commercial Bank remains ongoing.

ANZ Chief Financial Officer Michelle Jablko said: “The divestment of non-core businesses should continue to provide ANZ with the flexibility to consider further capital management initiatives in the future. Further initiatives will be considered once we receive the proceeds of our announced sales and will remain subject to business conditions and regulatory approval.”

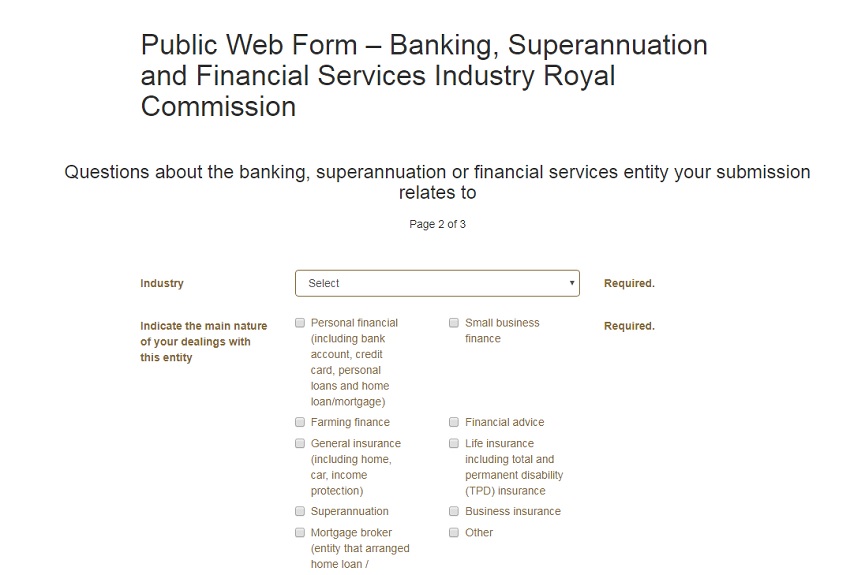

Following an article in The Adviser highlighting a ‘major flaw’ in the online form for the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, the commission has now updated the form to better reflect channel choice.

On Wednesday, The Adviser ran a story in which Queensland-based broker Nicki McDavitt warned that the figures cited by the initial hearing of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry could be wrong, after she identified what she called a “major flaw” in the commission’s online form.

The form asks users to identify the “nature of the dealings” in which misconduct took place.

However, the only option specifically relating to home loans fell under the category ‘mortgage broker’. Ms McDavitt therefore said that the commission’s figures on mortgage broker-related misconduct could be “false” as they may include information relating to bank branch home loans (and therefore be miscategorised).

However, the royal commission has today (14 February) updated the form to allow users to select ‘home loan/mortgage’ under the ‘personal finance’ option (see below). The mortgage broker option has also been updated to read ‘entity that arrange homed loan/mortgage’

Speaking to The Adviser following the change, Ms McDavitt said: “I’m absolutely thrilled. I’m thrilled that I was listened to and I’m thrilled that it has been changed.”

Ms McDavitt said the Royal Commission thanked her for bringing it to their attention as they had “not even realised that it was not even there” and brought it up with the web designers who changed it today (14 February).

“I said to [the contact]: ‘It does mean that those statistics that you have been flouting will be wrong’ and she acknowledged that it could be a risk, but said: ‘Thankfully we’ve caught it early’. And I said ‘yes’.”

The Adviser had asked the commission yesterday (13 February) for a comment on the issue and whether it would be changing the form, and received the following response: “The online submission process is working well and based on the number of submissions received to date, we are confident that those using the form have been able to identify correctly the nature of their dealings, including to identify home loans taken out with banks.

“We are also reviewing submissions as they come in to ensure that they are appropriately categorised.

“We are committed to ensuring that the information on our website is clear and easy to understand, so we will continue to review and improve the website going forward.”

The heads of both the mortgage broker associations had spoken to The Adviser this morning, both highlighting that they would be raising this issue of the online form error with the royal commission.

Speaking to The Adviser after the change, the executive director of the FBAA, Peter White, welcomed the change, but added that he believed the bank branches “still get off lightly, as the grouping/sections for arranging loans is highlighted separately for brokers, whereas the bank branches are not identified separately but rather in the cluster titled ‘Personal Financial’”.

He added: “This should read as ‘Personal Banking’ or the like, and then have the itemisation in brackets following it.”

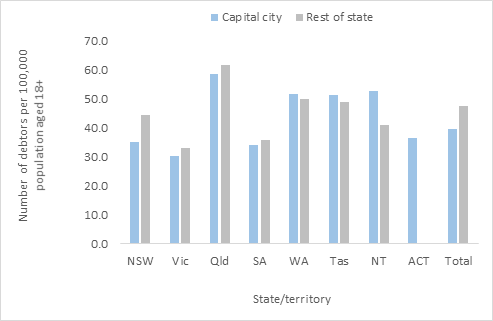

The latest data from The Australian Financial Security Authority (AFSA), regional personal insolvency statistics for the December quarter 2017, shows that on a relative basis more are in distress in the regions than in the major centres.

That said, there were 7,687 debtors who entered a new personal insolvency in the December quarter 2017 in Australia. Of these, 4,785 debtors or 62.2% were located in greater capital cities.

New South Wales – There were 1,320 debtors who entered a new personal insolvency in Greater Sydney in the December quarter 2017. The regions with the highest number of debtors were Campbelltown (NSW) (91), Wyong (80) and Gosford (74). There were 913 debtors who entered a new personal insolvency in rest of New South Wales in the December quarter 2017. The regions with the highest number of debtors were Newcastle (51), Lower Hunter (41) and Wagga Wagga (40).

Victoria – There were 1,064 debtors who entered new personal insolvencies in Greater Melbourne in the December quarter 2017. The regions with the highest number of debtors were Wyndham (72), Tullamarine – Broadmeadows (65) and Casey – South (63). There were 367 debtors who entered a new personal insolvency in rest of Victoria in the December quarter 2017. The regions with the highest number of debtors were Geelong (54), Bendigo (33) and Ballarat (29).

Queensland – There were 1,021 debtors who entered a new personal insolvency in Greater Brisbane in the December quarter 2017. The regions with the highest number of debtors were Springfield – Redbank (77), Ipswich Inner (60) and North Lakes (54). There were 1,141 debtors who entered a new personal insolvency in rest of Queensland in the December quarter 2017. The regions with the highest number of debtors were Ormeau – Oxenford (102), Townsville (101), Rockhampton (64) and Toowoomba (64).

South Australia – There were 347 debtors who entered a new personal insolvency in Greater Adelaide in the December quarter 2017. The regions with the highest number of debtors were Salisbury (54), Onkaparinga (41) and Playford (40). There were 106 debtors who entered a new personal insolvency in rest of South Australia in the December quarter 2017. The regions with the highest number of debtors were Eyre Peninsula and South West (20), Murray and Mallee (18) and Barossa (16).

Western Australia – There were 776 debtors who entered a new personal insolvency in Greater Perth in the December quarter 2017. The regions with the highest number of debtors were Wanneroo (114), Rockingham (81) and Swan (81). There were 199 debtors who entered a new personal insolvency in rest of Western Australia in the December quarter 2017. The regions with the highest number of debtors were Bunbury (38), Mid West (27) and Goldfields (25).

Tasmania – There were 89 debtors who entered a new personal insolvency in Greater Hobart in the December quarter 2017. The regions with the highest number of debtors were Hobart – North West (30), Hobart Inner (16) and Brighton (13). There were 110 debtors who entered a new personal insolvency in rest of Tasmania in the December quarter 2017. The regions with the highest number of debtors were Launceston (32), Devonport (25) and Burnie – Ulverstone (20).

Northern Territory – There were 55 debtors who entered a new personal insolvency in Greater Darwin in the December quarter 2017. The regions with the highest number of debtors were Darwin Suburbs (19), Palmerston (14) and Litchfield (12). There were 26 debtors who entered a new personal insolvency in rest of Northern Territory in the December quarter 2017. The regions with the highest number of debtors were Alice Springs (12) and Katherine (8).

Australian Capital Territory – In the December quarter 2017, there were 113 debtors who entered a new personal insolvency in the Australian Capital Territory. The regions with the highest number of debtors were Belconnen (32), Gungahlin (32) and Tuggeranong (30).

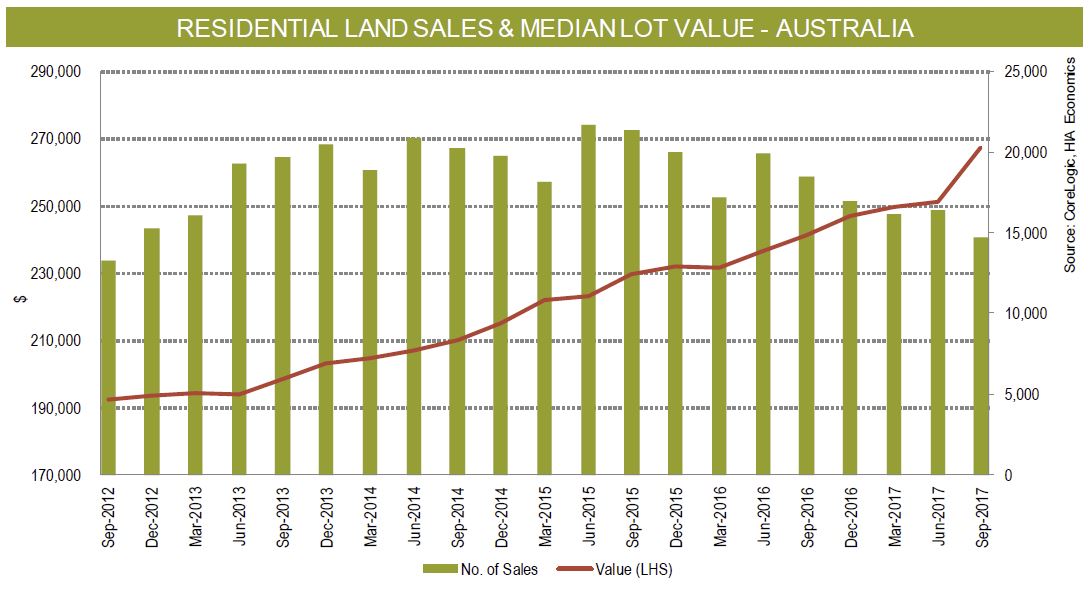

The latest HIA-CoreLogic Residential Land Report shows that the median vacant residential land lot price rose nationally by 6.5 per cent during the September 2017 quarter to reach $267,368.

“Yet again, the price of residential land in Sydney and Melbourne has touched fresh all-time highs.

“Transactions on the land market continue to drop, indicating that supply is simply not matching demand sufficiently.

“The high cost of new residential land is at the heart of Australia’s housing affordability crisis.

“The housing industry’s ability to ramp up the supply of new dwellings as demand dictates is hampered by the inconsistency of the land supply pipeline. The time it takes for land to be made available to builders is unnecessarily long,” concluded HIA Senior Economist Shane Garrett.

According to Eliza Owen, CoreLogic’s Commercial Research Analyst, “The 6.5 per cent acceleration in vacant residential land prices suggests strong demand, even in the context of our largest residential markets passing peak growth rates for the current cycle. The CoreLogic Hedonic Home value index is showing a 1 per cent quarterly decline in capital city dwellings in the three months to January, led by the Sydney market which saw a 2.5 per cent decline.

“Despite the softening in capital growth, land prices were driven higher by long term confidence in some Australian metropolitan markets. Indeed, developers may act counter-cyclically to secure vacant land on the fringe of metropolitan areas before the next upswing. This is reflected in Melbourne, which saw over one in five of the 14,704 vacant land transactions in the year to September.

“In Victoria, CoreLogic development data indicates that 48.6 per cent of residential subdivisions in 2017 commenced on the fringes of Melbourne, such as in Hume, Whittlesea and Wyndham. This further demonstrates the high levels of demand for housing that is connected to the facilities and employment opportunities of major cities,” concluded Eliza Owen.

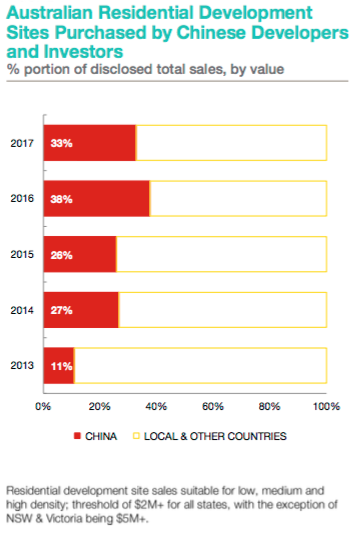

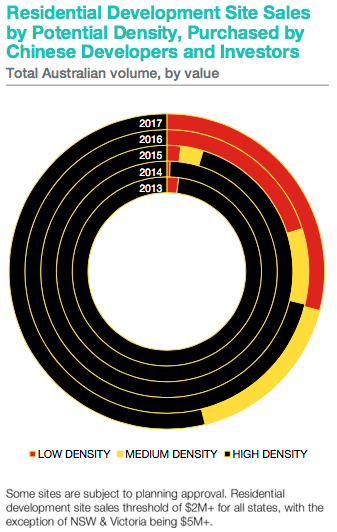

A new report from Knight Frank claims that in 2017, one-third of Australian residential development sites were sold to Chinese investors and developers.

In total, site sales to Chinese investors and developers equated to $2.02 billion, according to the report ‘Chinese Developers in Australia – Market Insight 2018’.

The report has been released to coincide with Chinese New Year, which this year is on Friday 16 February, 2018.

Knight Frank’s head of residential research, Australia, Michelle Ciesielski said, “Chinese developers have continued to dominate foreign investment in residential development sites across Australia. Many are now well-established in the local market.”

The share of sales to Chinese buyers has tripled since 2013, but decreased from the 38 per cent recorded in 2016, she said.

Source: Knight Frank Research.

Tighter regulation in both Australia and China has not dampened Chinese interest in Australian real estate

“Sustained developer interest in the Australian market has come in spite of government efforts in both Australia and China to tighten credit conditions as they relate to residential investment and development,” said Ciesielski.

“In Australia, the Australian Prudential Regulatory Authority has encouraged local financial institutions to impose stricter controls, while in China the government has attempted to moderate capital outflow with China’s Central Bank imposing new rules for companies which make yuan-denominated loans to overseas entities.

“However, in mid-2017, this was relaxed somewhat – resulting in a boost to market confidence.” said Ciesielski.

Melbourne received the highest proportion of Chinese buyers of development sites

The level of Chinese investment in residential development sites varied from state to state:

in Victoria, 38.7 per cent of residential site sales were to Chinese buyers

in New South Wales, 35.6 per cent of residential site sales were to Chinese buyers, and

in Queensland, Chinese buyers comprised 7.4 per cent of total residential site sale volumes.

Ciesielski said Melbourne was the most popular city for Chinese investors because it has sustained population growth, strong residential capital gains, and relatively low total vacancy rates.

“Many developers consider that Melbourne offers better relative value when compared to Sydney,” she said.

Chinese developers are shifting their focus to lower density developments

The report shows that Chinese developers and investors are increasingly focused on lower density developments in Australia, with 29 per cent of all sites purchased suited to low density, up from two per cent in 2013.

Source: Knight Frank Research.

Knight Frank’s head of Asian markets, Australia, Dominic Ong said, “As Chinese developers gain experience in higher-density projects across the major cities, there has been diversification in many of their portfolios to include medium and lower-density sites.

“These lower-density projects have also become more popular with local developers – especially in NSW, with the draft Medium Density Design Guide being released, identifying the ‘missing middle’ to encourage more low-rise, medium-density housing to be built.

“This type of project also tends to have less hurdles with the imposed tighter lending restrictions, and overall, lowers the delivery risk to the developer,” said Ong.

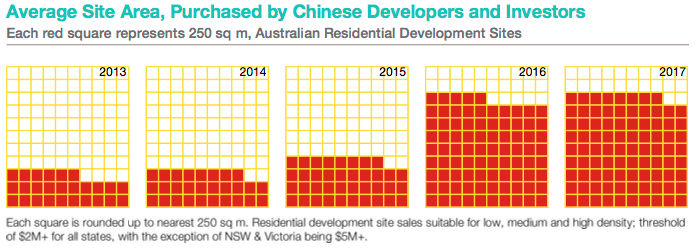

Chinese developers are buying larger plots

Ciesielski said that because Chinese buyers are shifting to lower-density developments, the size of the sites they are buying is larger.

“In 2017, the average site purchased was 21,785 square metres, increasing three-fold since 2013,” she said.

Source: Knight Frank Research.

“It’s expected lengthier due diligence will be carried out for those now established in the local market, and for new developers coming into Australia, transactions will be reliant on the ability to transfer their funds,” concluded Ciesielski.

As part of the discussion paper, released today APRA, says that addressing the systemic concentration of ADI portfolios in residential mortgages is an important element of the proposals. They have FINALLY woken up to the risks in the system, just years too late! We have significant numbers of loans in the system currently that would now not pass muster.

These proposals, which focus in on mortgage serviceability, would change the industry significantly, as lower risk loans will be more highly prized (so expect low rate offers for lower LVRs), whilst investment loans, and interest only loans are likely to cost more and be harder to find. Combined this could certainly move the market! The proposals introduce “standard” and “non-standard” risk categories.

The proposals are for consultation, with a closing data 18 May 2018.

As well as increasing the risk weights for some mortgages, they also continue to close the gap between the advanced (IRB) internal approach used by large lenders, and the standard approach used by smaller players. Those in transition (e.g. Bendigo Bank) may find less of an advantage in moving to advanced as a result.

Also they are proposing some simplification for small ADI’s as the cost of these measures may outweigh the benefit to prudential safety. Proportionate and tailored requirements for small ADIs could reduce regulatory burden without compromising prudential safety and soundness. Calibration of a simpler regime would be broadly aligned to the more complex regulatory capital framework, yet would be designed to suit the size, nature, complexity and risk of small ADIs.

Here are some of the key paragraphs from their paper.

APRA’s view is that there are potential systemic vulnerabilities to the financial system created from high levels of residential mortgage lending for investment purposes. As noted by the RBA, investment lending can amplify borrowing and house pricing cycles:

Periods of rapidly rising prices can create the expectation of further price rises, drawing more households in the market, increasing the willingness to pay more for a given property, and leading to an overall increase in household indebtedness.

Similarly, the significant share of interest-only housing lending, including to owner-occupiers, is a structural feature that increases the risk profile of the Australian banking system. Interest-only borrowers face a longer period of higher indebtedness, increasing the risk of falling into negative equity should housing prices fall. Borrowers may also use interest-only loans to maximise leverage, or for short-term affordability reasons. Even though loan servicing ability (serviceability) is now tested at levels that include the subsequent principal repayments, borrowers may face ‘payment shock’ when the interest-only period ends and regular repayments increase, in some cases significantly. This payment shock is particularly acute when interest rates are low.

Over the past two decades, residential mortgages in Australia as a share of ADIs’ total loans have increased significantly, from just under half to more than 60 per cent. While losses incurred on residential mortgage portfolios in this period have been limited, this level of structural concentration poses prudential and financial stability risks, particularly in an environment of high household debt, high property prices, weak income growth and strong competitive pressures among lenders. In such circumstances, households, individual ADIs and the broader banking sector are vulnerable to economic shocks.

Similar to other jurisdictions facing comparable risks, APRA has undertaken a series of actions to help contain the risks associated with ADIs’ residential mortgage portfolios. These actions include promoting significantly strengthened loan underwriting practices, increasing the amount of capital held by IRB ADIs for residential mortgage exposures and establishing benchmarks to moderate lending for property investment and lending on an interest-only basis. As set out in APRA’s July 2017 information paper on unquestionably strong capital, APRA also intends to further strengthen capital requirements for residential mortgage lending to reflect the concentration risk it poses to the banking sector.

A key focus is the appropriate capital requirement for investment and interest-only mortgage loans. Although, as a class, investment loans have typically performed well under normal economic conditions in Australia, this segment has not been tested in a nationwide downturn. Further, an increasing proportion of highly indebted households own investment property relative to past economic cycles. Experience in the United Kingdom and Ireland during the global financial crisis, for example, showed that previously better-performing investment loans can fall into arrears in higher volumes than loans to owner-occupiers in times of stress.

So now they propose to target higher-risk residential mortgage lending, balanced against the need to avoid undue complexity. Under the proposals, residential mortgage exposures would be segmented into the following categories with different capital requirements applying to each segment:

loans meeting serviceability requirements made to owner-occupiers where the borrower’s repayment is on a principal and interest (P&I) basis;

loans meeting serviceability requirements made for investment purposes or where the borrower’s repayment is on an interest-only basis; and

other residential property exposures, including those that do not meet serviceability requirements.

Specifically, for the standard approach, APRA proposes that APS 112 would require ADIs to designate as non-standard eligible mortgages those where the ADI:

did not include an interest rate buffer of at least two percentage points and a minimum floor assessment interest rate of at least seven per cent in the serviceability methodology used to approve the loan;

did not verify that a borrower is able to service the loan on an ongoing basis (i.e. positive net income surplus); and

approved the loan outside the ADI’s loan serviceability policy.

APRA is also considering excluding certain other categories of loans considered higher risk from the definition of standard eligible mortgages, such as those with very high multiples of a borrower’s income.

APRA proposes to formalise through amendments to APS 112 its existing requirement that loans to self-managed superannuation funds secured by residential property should be treated as non-standard loans, reflecting the relative complexity of these loans and the fact that ADIs do not have recourse to other assets of the fund or to the beneficiary.

APRA also proposes that reverse mortgages, which are currently risk-weighted at 50 per cent (where LVR is less than 60 per cent) or 100 per cent (for LVRs over 60 per cent), would be treated as non-standard in light of the heightened operational, legal and reputational risks associated with these loans.

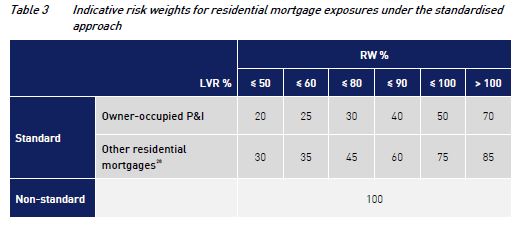

Subject to final calibration, APRA proposes that all non-standard eligible mortgages would be subject to a risk weight of 100 per cent.

APRA proposes to segment the standard eligible mortgage portfolio into lower-risk and higher-risk exposures in addition to assigning risk weights according to LVR. This approach is aligned to, but deliberately not strictly consistent with, the Basel III ‘material dependence’ concept, to appropriately reflect Australian conditions.

For the lower-risk segment, APRA proposes to broadly align the risk weights with those under the Basel III framework loans where repayments are not materially dependent on cash flows generated by the property securing the loan. This category would include owner-occupied P&I loans and would apply after consideration of any lenders mortgage insurance (LMI).

The higher-risk segment would include interest-only loans, loans for investment property and loans to SMEs secured by residential property. The determination of higher risk weights for this segment would be either by way of a fixed risk-weight schedule, or a multiplier on the risk weights applied to owner-occupied P&I loans. The benefit of a multiplier is that APRA could more easily vary the capital uplift for these higher risk loans over time depending on prevailing prudential or financial stability objectives or concerns.

Table 3 shows the indicative proposed risk-weight schedule based on the Basel III risk weights for materially dependent residential mortgage exposures.

APRA is also considering whether exposures to individuals with a large investment portfolio (such as those with more than four residential properties) would be treated as non-standard residential mortgage loans or as loans secured by commercial property. APRA invites feedback on this issue.

APRA expects to continue to incorporate relatively lower capital requirements in the standardised approach for exposures covered by LMI. LMI can reduce the risk of loss for an ADI, subject to meeting the insurer’s conditions for valid claims and the financial capacity of the LMI to pay claims. APRA is considering the appropriate methodology to recognise LMI in the capital framework for both the standardised and IRB approaches. For the standardised approach to credit risk, APRA expects that any capital benefit would continue to apply to loans with an LVR over 80 per cent. APRA’s preferred approach is to increase the Table 3 risk weights (as finally calibrated) for standard loans with an LVR over 80 per cent that do not have LMI. For the IRB approach, APRA is considering potential options for the recognition of LMI.

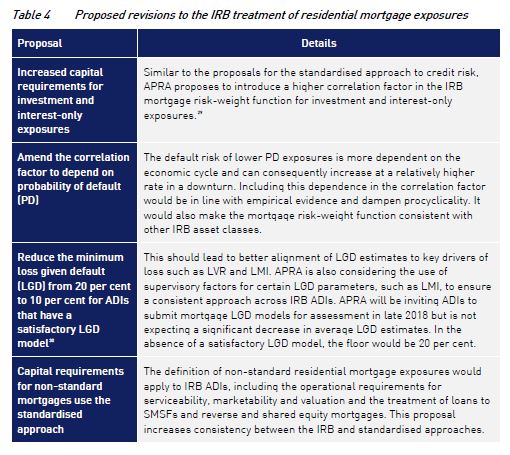

For IRB Bank (those using their own internal models, APRA believes that material changes are required in Australia in order to:

improve the alignment of capital requirements with risk for particular exposures;

further address the FSI recommendation that the difference in average mortgage risk weights between the standardised and IRB approaches is narrowed; and

ensure an appropriate overall calibration of capital for residential mortgage exposures given the concentration of IRB ADI portfolios in this segment.

On their own, however, these IRB mortgage risk-weight functions are not expected to result in a sufficient level of capital to meet APRA’s objectives for increased capital for residential mortgage exposures. However, any further increase in correlation for the IRB mortgage risk-weight function creates inconsistencies with correlation factors for other asset classes.

As a result, other adjustments are likely to be necessary to meet unquestionably strong capital expectations. For residential mortgages, this is expected to be through additional RWA overlays on top of the outputs of the IRB risk-weight function, including both an overlay specifically for residential mortgages and an overlay for total RWA.

The exact form and size of these overlays will be determined after APRA has completed its QIS analysis. In determining final calibration of the regulatory capital requirement for residential mortgage exposures, APRA will consider the appropriate difference in the average risk weights under the IRB and standardised approaches, consistent with recommendation 2 of the FSI. As detailed in the final report of the FSI, given the IRB approach is more risk sensitive, some difference between the average risk weights for residential mortgage exposures under the different approaches to credit risk may be justified; however, it should not be of a magnitude to create unwarranted competitive distortions.

SME exposures secured by residential property that meet certain serviceability criteria would be included in the same category of exposures as residential mortgages for investment purposes and interest-only loans.

In APRA’s experience, these exposures have historically had higher losses than non-SME owner-occupier residential mortgage exposures.

For SME exposures that are not secured by property, APRA proposes to reduce the 100 per cent risk weight currently applied under APS 112 to 85 per cent. This gives some recognition to the various types of collateral, other than property, that SMEs provide as security. APRA does not propose to implement the Basel III 75 per cent risk weight for retail SME exposures, as there is insufficient empirical evidence that retail SME exposures in Australia exhibit a lower default or loss experience through the cycle than corporate SME exposures. SME exposures in this category would be limited to corporate entities where consolidated group sales are less than or equal to $50 million.

The Australian Prudential Regulation Authority (APRA) has released two discussion papers for consultation with authorised deposit-taking institutions (ADIs) on proposed revisions to the capital framework.

The key proposed changes to the capital framework include:

lower risk weights for low LVR mortgage loans, and higher risk weights for interest-only loans and loans for investment purposes, than apply under APRA’s current framework;

amendments to the treatment of exposures to small- to medium-sized enterprises (SME), including those secured by residential property under the standardised and internal ratings-based (IRB) approaches;

constraints on IRB ADIs’ use of their own parameter estimates for particular exposures, and an overall floor on risk weighted assets relative to the standardised approach; and

a single replacement methodology for the current advanced and standardised approaches to operational risk.

The paper also outlines a proposal to simplify the capital framework for small ADIs, which is intended to reduce regulatory burden without compromising prudential soundness.

The papers include proposed revisions to the capital framework resulting from the Basel Committee on Banking Supervision finalising the Basel III reforms in December 2017, as well as other changes to better align the framework to risks, including in relation to housing lending. APRA is also releasing a discussion paper on implementation of a leverage ratio requirement.

In the papers released today, APRA is not seeking to increase capital requirements beyond what was already announced in July 2017 as part of the ‘unquestionably strong’ benchmarks.

During the process of consultation, APRA will undertake further analysis of the impact of these proposed changes on ADIs. This analysis will include a quantitative impact study, which will be used to, where necessary, calibrate and adjust the proposals released today.

APRA Chairman Wayne Byres said that, taken together, the proposed changes are designed to lock in the strengthening of ADI capital positions that has occurred in recent years.

“These changes to the capital framework will ensure the strong capital position of the ADI industry is sustained by better aligning capital requirements with underlying risks. However, given the ADI industry is on track to meet the ‘unquestionably strong’ benchmarks set out by APRA last year, today’s announcement should not require the industry to hold additional capital overall,” Mr Byres said.

APRA has also released today a discussion paper on implementing a leverage ratio requirement for ADIs. The leverage ratio is a non-risk based measure of capital strength that is widely used internationally. A minimum leverage ratio of three per cent was introduced under Basel III, and is intended to operate as a backstop to the risk-weighted capital framework. Although the risk-based capital measures remain the primary metric of capital adequacy, APRA has previously indicated its intention to implement a leverage ratio requirement in Australia. This approach was also recommended by the Financial System Inquiry in 2014.

APRA is proposing to apply a higher minimum requirement of four per cent for IRB ADIs, and to implement the leverage ratio as a minimum requirement from July 2019.

In addition to the two papers released today, APRA will later this year release a paper on potential adjustments to the overall design of the capital framework to improve transparency, international comparability and flexibility.