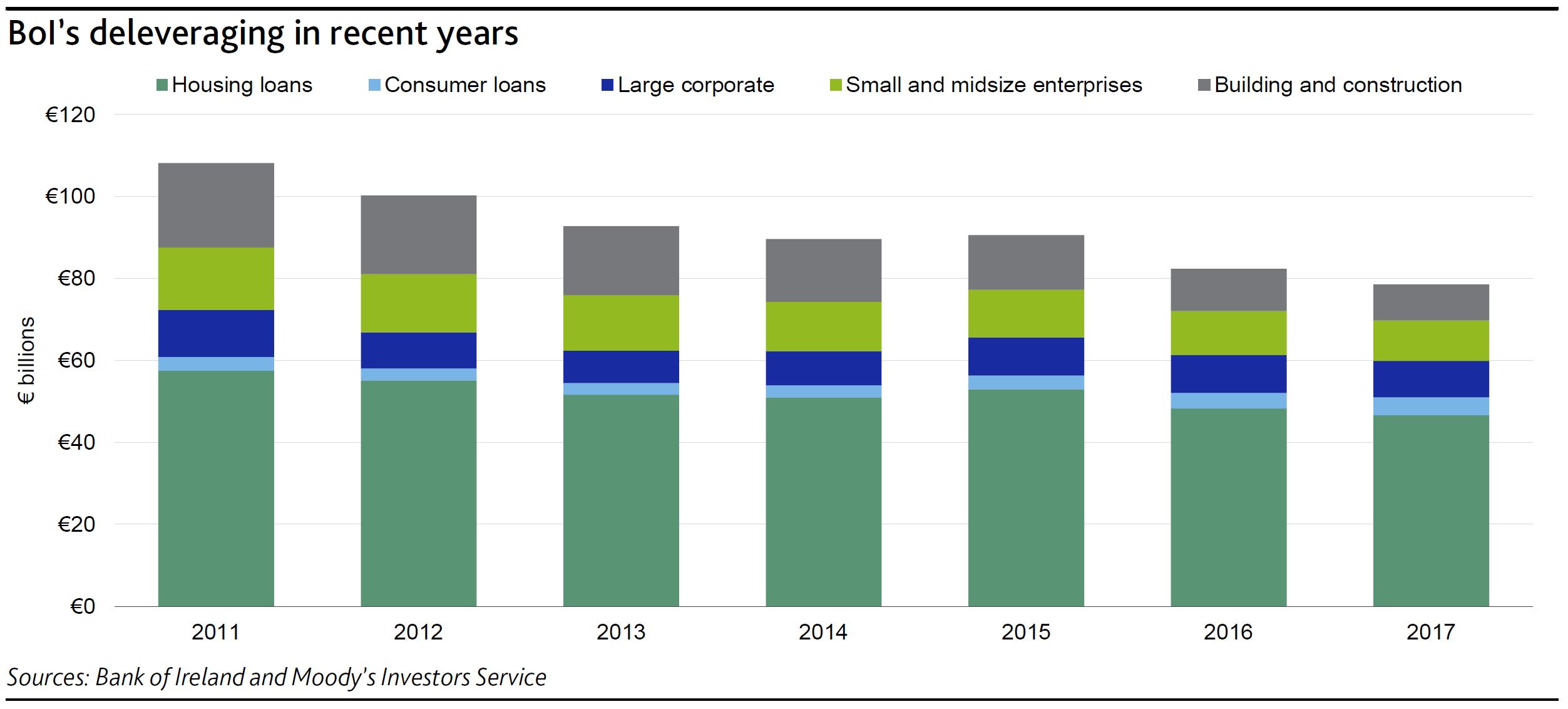

Last Wednesday at an investor day, Bank of Ireland announced a challenging growth strategy for the next three years that moves the bank to a growth phase from a restructuring phase according to Moody’s.

BOI plans to increase its loan book by 20%, or €14 billion, by 2021 (20% on the retail Irish portfolio, 10% on its retail UK portfolio and 50% on its corporate portfolio), with a 4.7% compound annual growth rate. It expects to achieve growth mainly by financing new house building and increasing residential mortgages and small and midsize enterprise (SME) lending in both Ireland and the UK, where it operates through subsidiary Bank of Ireland (UK) Plc. The bank’s new strategy follows years of deleveraging.

BOI’s plan is credit negative because its restructuring is still ongoing and presents many challenges. Additionally, the announced shift towardgrowth is focused on corporate loans and in particular on the construction and real estate sectors, which we consider high-risk sectors. We believe that BOI’s new strategy increases its exposure to downside risks, and particularly increases its UK operation’s vulnerability to macroeconomic uncertainties related to Brexit and a potential slowdown or downturn in the Irish property market.

Even though BOI’s stock of problem loans diminished to €4.0 billion at year-end 2017 from €6.2 billion at year-end 2016, one-third of its Irish buy-to-let loans are classified as nonperforming and about 15% of the Irish non-property SME portfolio is nonperforming. The property and construction portfolio, to which the bank plans to increase its exposure, remains the worst performer, with 19% of total loans classified as nonperforming at year-end 2017. BOI has a large portion (€4.6 billion) of vulnerable restructured loans that we consider as having a high probability of falling back into nonperformance in the event of macroeconomic headwinds.

The new strategy primarily aims to boost the bank’s profitability (target return on tangible equity above 10% by 2021 versus 6.9% in 2017) through higher loan volume and stronger operating efficiency (the bank aims to reduce its cost base to €1.7 billion in 2021 from €1.9 billion in 2017, with a target cost/income ratio of 50% by 2021). The bank also plans to expand its wealth management and insurance businesses, and has increased the planned investment in its digital and commercial transformation to €1.4 billion from €900 million previously budgeted.

BOI expects sound GDP performance in both Ireland and the UK to support its growth strategy. The bank also expects rising employment and increasing population that increases housing demand, particularly in the main Irish cities, where, despite the past five years of recovery, the housing undersupply problem has remained. BOI CEO Francesca McDonagh, who was appointed in May 2017, set the new strategic plan and moved away from the bank’s previous strategic focus on deleveraging and asset de-risking