BOQ announced a 1% uplift in Cash Earnings to $360 million for the 2016 financial year and increased Statutory Net Profit after Tax 6% to $338 million. Cost management saved the day, as net interest margins were squeezed, and lending growth slowed in the second half.

Lending grew 5% or $2.2 billion at 0.8x System, with gross loans and advances totalling $43.2 billion, though this growth was moderated in the second half with the strategic shift to preserve margin and target deposit acquisition through retail channels. Lending growth was entirely funded by the 8% growth in customer deposits, which resulted in a 2% uplift to the deposit to loan ratio to 68%.

Loan growth moderated significantly in the second half in light of heightened competition in key markets, the prudential cap on investment housing and the strategic shift to preserve margin over asset growth with an emphasis on deposit gathering. The strategy of targeting niche customer segments is delivering results with BOQ Specialist, BOQ Finance and niche segments in BOQ Commercial demonstrating solid growth momentum. The Group’s maturing broker presence combined with the new Virgin Money mortgage offering, and a more productive branch network, supported by the digitisation investment being progressively rolled out, should continue to deliver success from the multi-channel strategy.

The housing portfolio grew 5% over the year. Above system growth in the first half was offset by a slight contraction in the second half as the business focused on margin preservation and deposit gathering.

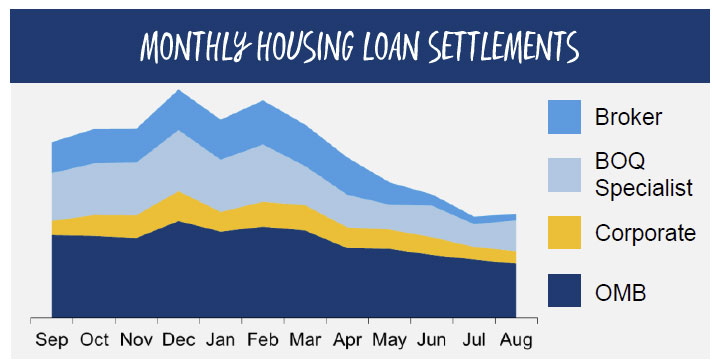

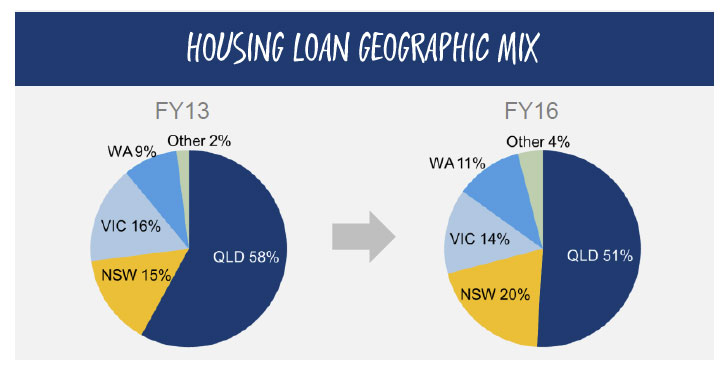

The broker channel continued to expand throughout the year, growing the accredited broker base and aiding BOQ’s geographic footprint with 84% of growth in this channel outside of Queensland.

The broker channel continued to expand throughout the year, growing the accredited broker base and aiding BOQ’s geographic footprint with 84% of growth in this channel outside of Queensland.

Growth through the broker channel moderated in the second half, with greater price sensitivity to new business acquisition pricing compared to other channels. Despite the slower volumes through the second half, the broker network still contributed 23% of total retail housing settlements during the year, albeit with settlement volumes reducing to 19% of total retail housing settlements in the second half.

Growth through the broker channel moderated in the second half, with greater price sensitivity to new business acquisition pricing compared to other channels. Despite the slower volumes through the second half, the broker network still contributed 23% of total retail housing settlements during the year, albeit with settlement volumes reducing to 19% of total retail housing settlements in the second half.

The launch of the Virgin Money mortgage product in May provided another channel for BOQ to engage with a new customer demographic. The Virgin brand attracts a different customer, more affluent and likely to be metro-based with a strong propensity to engage through digital channels. Virgin Money has engaged with complementary broker groups PLAN and FAST with over 800 brokers now accredited. Virgin Money is about to launch with two additional large broker groups in the coming months. This could provide an uplift in performance in 2017.

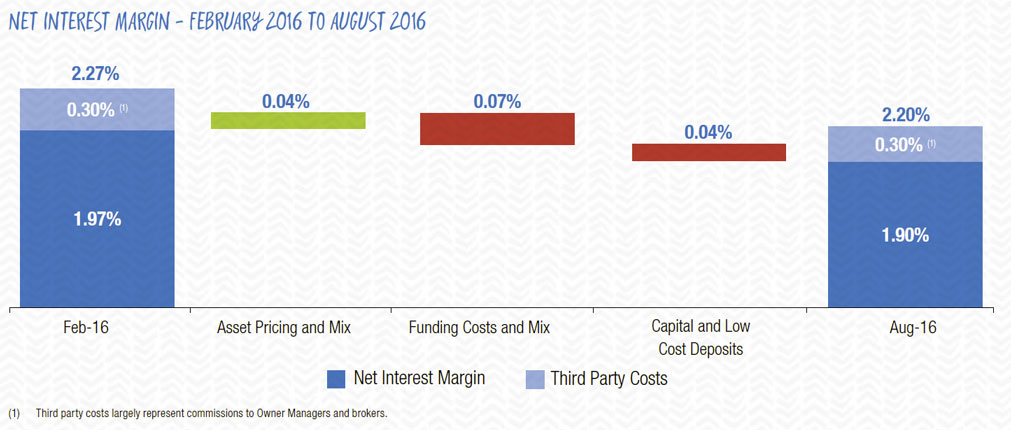

Net Interest Margin contracted 3bps over the year to 1.94%, with the second half margin declining to 1.90%.

The highly competitive rates in lending and deposits across the industry have translated into reduced new business margins and increased levels of retention repricing of existing customers. Further, the confluence of market dynamics in wholesale funding and hedging costs, and the low yield environment, accelerated the margin decline in the second half.

The highly competitive rates in lending and deposits across the industry have translated into reduced new business margins and increased levels of retention repricing of existing customers. Further, the confluence of market dynamics in wholesale funding and hedging costs, and the low yield environment, accelerated the margin decline in the second half.

Repricing actions during the year positively impacted NIM by 9 basis points. Front to back book repricing impacts and retention repricing activity had a 3 basis point contractionary impact on NIM in the half, similar to the impact in the prior half. The competition for funding intensified over the second half at the same time as the yield curve contracted, with a 4 basis point impact to NIM. Half of this impact was evident in retail liabilities as increased competition meant absolute term deposit rates did not fall in line with movements in the yield curve. The majority of this impact emerged in the last quarter. A further 2 basis points of impact occurred in wholesale funding costs. The low yield curve continues to impact returns on BOQ’s replicating portfolio, covering the investment profile of BOQ’s capital and low cost deposits totalling $4.8 billion at year end and causing a 4 basis point reduction in the half.

Operating expenses increased 4% on the prior year to $520 million.

This included a $10 million uplift in amortisation expense as a number of strategic initiatives have been delivered, together with costs associated with the newly launched Virgin Money mortgage offering ($3 million). The benefit of the $15 million investment in organisational operating model changes announced to the ASX in February will be fully realised in line with stated targets, with further opportunities identified. This includes the cost of the operating model restructuring program of $15 million, with a similar level of one-off expenses in the prior year. The result also includes the uplift in intangible IT asset amortisation ($10 million), as the digitisation program and key strategic initiatives have been delivered.

This included a $10 million uplift in amortisation expense as a number of strategic initiatives have been delivered, together with costs associated with the newly launched Virgin Money mortgage offering ($3 million). The benefit of the $15 million investment in organisational operating model changes announced to the ASX in February will be fully realised in line with stated targets, with further opportunities identified. This includes the cost of the operating model restructuring program of $15 million, with a similar level of one-off expenses in the prior year. The result also includes the uplift in intangible IT asset amortisation ($10 million), as the digitisation program and key strategic initiatives have been delivered.

Employee numbers have decreased 2% over the year as a result of the organisational operating model reshaping. Investment has been made to support the launch of the Virgin Money mortgage product and to support the channel diversification strategy. BOQ continued to optimise the branch network with a reduction in the branch footprint of 23 locations across the year to 211 branches, mainly reflecting consolidations and retirements.

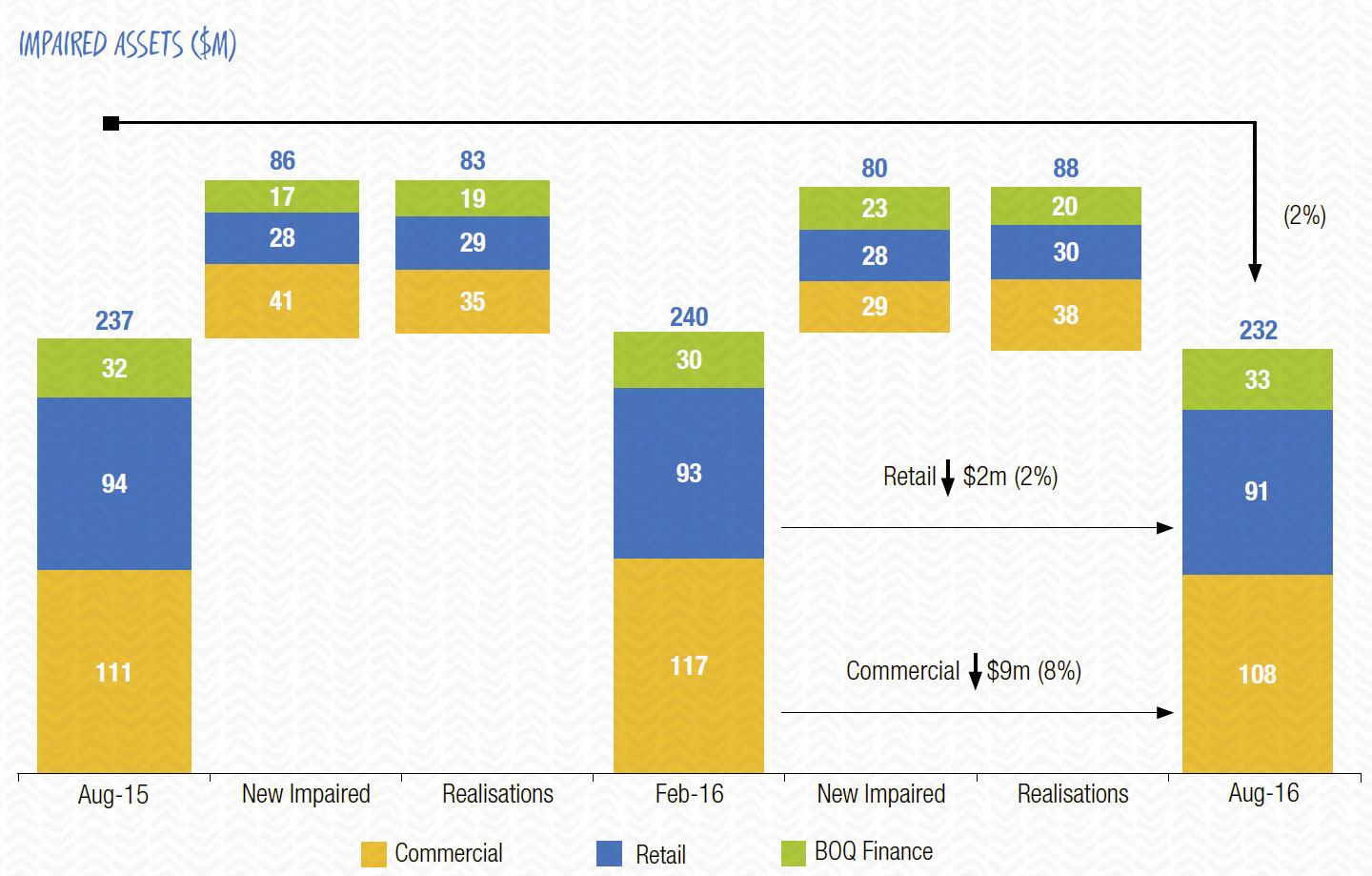

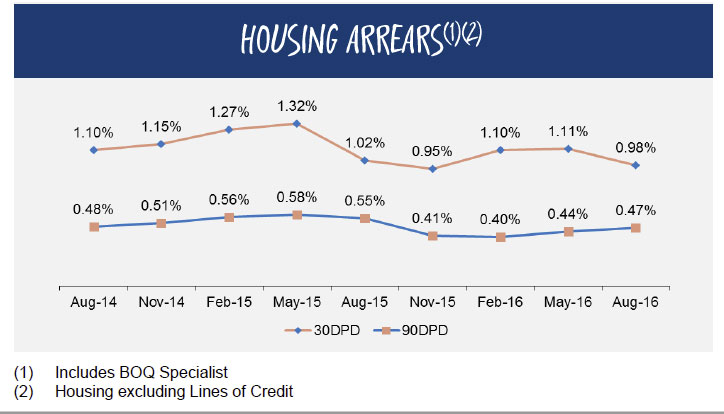

Further improvement in asset quality was evident across the portfolio.

Loan impairment expense reduced by 9% to $67 million in 2016, or a reduction of 2bps to 16bps of gross loans and advances. The second half result was 14bps of gross loans and advances.

Loan impairment expense reduced by 9% to $67 million in 2016, or a reduction of 2bps to 16bps of gross loans and advances. The second half result was 14bps of gross loans and advances.

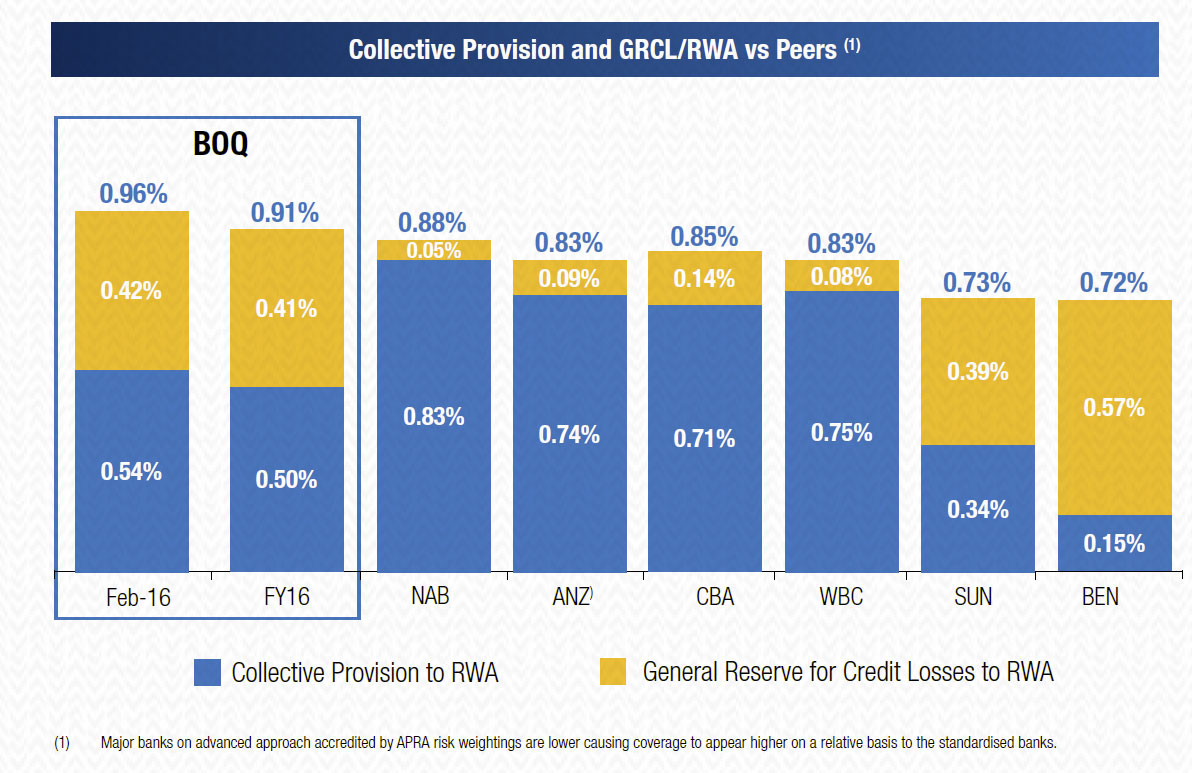

BOQ achieved positive improvements in credit quality metrics across the portfolio compared to the prior year and continues to maintain higher provisioning coverage.

BOQ achieved positive improvements in credit quality metrics across the portfolio compared to the prior year and continues to maintain higher provisioning coverage.

However, 30 day delinquencies rose in the critical home lending portfolio.

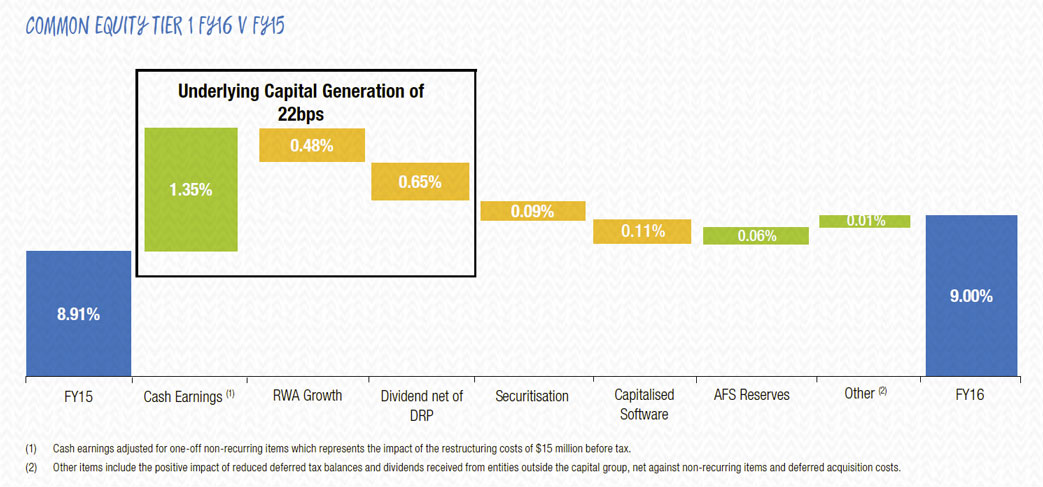

During the year BOQ continued to strengthen its balance sheet with strong capital generation enabling an increase in the Common Equity Tier 1 ratio (‘CET1’) to 9.0%, which positions it well for evolving regulatory capital requirements.

During the year BOQ continued to strengthen its balance sheet with strong capital generation enabling an increase in the Common Equity Tier 1 ratio (‘CET1’) to 9.0%, which positions it well for evolving regulatory capital requirements.

APRA requires ADIs to maintain a minimum 100% LCR. The LCR requires sufficient High Quality Liquid Assets to meet net cash outflows over a 30 day period, under a regulator defined liquidity stress scenario. BOQ manages its LCR on a daily basis with a buffer above the regulatory minimum in line with the BOQ prescribed risk appetite and management ranges. BOQ’s average LCR remained consistent over the August quarter at 129% (31 May 2016 quarter: 129%).

APRA requires ADIs to maintain a minimum 100% LCR. The LCR requires sufficient High Quality Liquid Assets to meet net cash outflows over a 30 day period, under a regulator defined liquidity stress scenario. BOQ manages its LCR on a daily basis with a buffer above the regulatory minimum in line with the BOQ prescribed risk appetite and management ranges. BOQ’s average LCR remained consistent over the August quarter at 129% (31 May 2016 quarter: 129%).

The Board has determined a final dividend of 38 cents per share fully franked, with the total dividends of 76 cents for the year, an increase of 3% on the 2015 financial year.