A new report from Deloitte Access Economics has highlighted significant work remains on implementing key recommendations of the Financial System Inquiry (FSI).

The Customer Owned Banking Association (COBA) commissioned the report on implementation of FSI recommendations 1, 2, 3 & 30 because it is now more than two years since the report was delivered to Government and more than one year since the Government announced its response.

The Customer Owned Banking Association (COBA) engaged Deloitte Access Economics to report on progress in implementing the following recommendations of the 2014 Financial System (Murray) Inquiry (FSI):

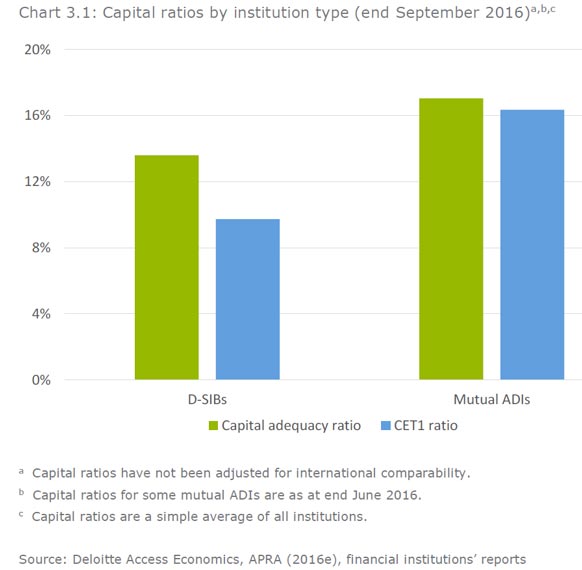

- Recommendation 1: Set capital standards such that Australian authorised deposit-taking institution capital ratios are unquestionably strong.

- Recommendation 2: Raise the average internal-ratings-based (IRB) mortgage risk weight to narrow the difference between average mortgage risk weights for authorised deposit-taking institutions using IRB risk-weight models and those using standardised risk weights.

- Recommendation 3: Implement a framework for minimum loss absorbing and recapitalisation capacity in line with emerging international practices, sufficient to facilitate the orderly resolution of Australian authorised deposit-taking institutions (ADIs) and minimise taxpayer support.

- Recommendation 30: Review the state of competition in the sector every three years, improve reporting of how regulators balance competition against their core objectives, identify barriers to cross-border provision of financial services and include consideration of competition in the Australian Securities and Investments Commission’s (ASIC) mandate.

Deloitte Access Economics finds that delays to implementation of the recommendations would adversely affect the ability of the financial system to realise the benefits of these reforms. These benefits were identified by the FSI as helping to:

- ensure the robustness of the financial system

- aid competition in the banking sector

- address the ‘too big to fail’ issue in the banking sector.

“The customer owned banking sector wants to see more urgency from government and regulators in implementing the key FSI reforms,” COBA CEO Mark Degotardi said.

“This report is timely because the House of Representatives Economics Committee has just found that Australia’s banking market is an oligopoly where the major banks have significant market power that they use to the detriment of consumers.

“The House Economics Committee found that a lack of competition in banking has significant adverse consequences for the economy and consumers.

“There is no time to waste, yet Deloitte Access Economics’ report card finds only limited progress on the key FSI recommendations.

“In relation to the Recommendation 30 requirement for regulators to explain how they balance competition with their other mandates, Deloitte Access Economics finds that there has been ‘little progress’.

“This is particularly disappointing because regulator decision-making can have a significant impact on competition. Deloitte Access Economics mentions two examples of this: APRA’s approach to regulatory capital instruments for customer owned banking institutions and APRA’s application of the cap on investor lending growth.

“Deloitte Access Economics’ report proposes a draft terms of reference for a Productivity Commission review of competition in the financial system, focusing on the banking sector.

“COBA welcomes Deloitte Access Economics’ suggestion the PC review should consider whether regulators’ rules and procedures are creating inappropriate barriers to competition and whether there is appropriate regard to other business models, including the customer owned model.”

Deloitte Access Economics has provided the following snapshot of the status of key FSI recommendations:

Table 1.1: Overall state of play

|

|

State of play |

| Recommendation 1

Capital levels |

Some progress, yet to be completed.

· Steps already taken which have seen an increase in the capital ratios of the Australian major banks. · Current schedule suggests that implementation may be completed in 2018. |

| Recommendation 2

Narrow mortgage risk weight differences |

Some progress, yet to be completed.

· Still in progress, although interim steps have been taken to narrow risk weights. · Current schedule suggests that implementation may be completed in 2018. |

| Recommendation 3

Loss absorbing and recapitalisation capacity |

Limited domestic progress; contingent on international developments.

· No set timeframe, but progress is expected to “hasten slowly”. |

| Recommendation 30

Strengthening the focus on competition in the financial system |

Limited progress.

· Current schedule suggests that implementation could be completed by end-2017. |

Source: Deloitte Access Economics