The screws are being turned more tightly by the banks as they respond to APRA’s “10% growth hurdles” for investment loans.

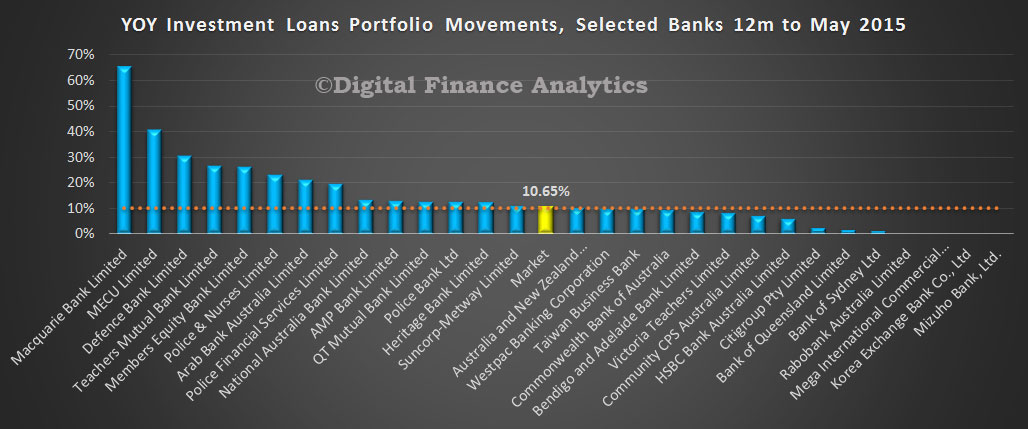

In our analysis of the latest loan data we highlighted that a number of large lenders were well about the 10% guidance, and the market was at 10.65%, so given this progress so far through to year, they would need to tighten criteria considerably in the second half to reduce flow to net out at 10%.

Westpac, the lender with the largest share of investment loans will now limit loan to value ratio (LVR) to no more than 80% down from 95% previously. In addition, they will now use a servicing interest rate benchmark of 7.25%, reducing the real world impact of ultra low interest rates.

Westpac, the lender with the largest share of investment loans will now limit loan to value ratio (LVR) to no more than 80% down from 95% previously. In addition, they will now use a servicing interest rate benchmark of 7.25%, reducing the real world impact of ultra low interest rates.

Also, ANZ is tuning its loan-to-value ratio down to 90%, when previously they would lend to 97%. They had already reduced LVRs to new customers down to 70%.

We had previously highlighted the changes made by NAB and CBA. NAB reduced its LVR to investors from 95% to 90%, and CBA is now using a floor assessment rate of 7.25% when assessing serviceability, as well as tightening how overtime and bonuses are factored into the assessment, reducing the assumed yield from rental properties and scrapping their $1,000 investment home-loan rebate offer.

We are also seeing some changes to discounts on offer, with a much stronger focus on attracting and refinancing owner occupied loans. Early results from the latest household surveys suggests that there is still enough of a supply of investment loans to meet demand, smaller banks, credit unions and building societies are active, and the non-bank sector has no “10% hurdle” at all. We are seeing wider pricing differences between investment and owner occupied loans.

We expect this investment lending tightening will continue, but it is too soon to judge whether it will have any absolute change to investment loan volumes, or whether it just moves new customers to other lenders still willing to do deals. Certainly demand for investment property has not weakened so far. Indeed, given recent stock market movements and low deposit rates, investment property remains very compelling for many.

One thought on “Banks Tighten Investment Property Loan Criteria Further”