The use and regard to expenditure benchmarks is “an area that is ripe for further guidance from ASIC”, and will be a focus of the updated RG 209 guidance next month, the financial services regulator has suggested. Via The Adviser.

Speaking at the parliamentary joint

committee on corporations and financial services hearing on its

oversight of the Australian Securities and Investments Commission (ASIC)

and the Takeovers Panel on Tuesday (19 November), chairman James

Shipton and commissioner Sean Hughes revealed some of the specific

issues that will be addressed in its upcoming revised guidance on responsible lending.

The chair told the parliamentary

joint committee that there was a need for “more contemporaneous”

guidance around responsible lending, particularly given the increasing

number of online lenders, the upcoming open banking scheme and increased

data, the evolution of business practices, updates to technology, and

automatisation of systems.

Commissioner Hughes elaborated that

the “greater use of technology and technological tools to verify borrow

information in real time” and have it “fully verified using technology

solutions within 58 minutes” was an advancement that was not available

when the National Consumer Credit Protection Act(NCCP) was written 10 years ago.

Another area that required updating was around expense benchmarks used to verify borrower expenses – such

as the Household Expenditure Measure (HEM) – particularly given the

fact that some categories of expenses are not included in HEM, such as

certain medical costs, superannuation contributions and mortgage

repayments.

Commissioner Hughes said: “We are not

requiring lenders to scrutinise how many cups of coffee you are having,

whether you are going to an expensive gym and all those things. That is

not what our guidance requires.

“What our guidance is suggesting (and I emphasize suggesting)

is that lenders could have regard to unusual patterns and expenditure,

which take a borrower outside normal patterns for that person.”

He continued: “There are some

categories of expense that require a lender to go above and beyond the

standardised benchmark. So, this is something we’ve recognised through

the consultation process that we have undertaken. It’s been something

that all the submissions have commented on, and we think it’s an area

that is ripe for further guidance from ASIC.”

Mr Hughes later told the committee that another area ASIC will be “zeroing in on” will be the level of enquiries needed for refinances, among other activities.

He said: “[W]hat we do want to

preserve, as part of our guidance in the next version, is the concept of

scalability. And this is something that other submitters [to the

consultation] have commented on as well.

“So for instance, if I use the

example of a borrower who is seeking to refinance an existing loan that

retains the same overall credit headroom – perhaps swapping out another

security, taking advantage of lower interest rates – we would say that,

if all other things haven’t changed and the borrower’s

capacity to repay the loan remains the same and their income seem

stable, that would not require a lender to do the forensic detailed

examination of how many cups of coffee, or gym memberships, etc., they

have that might be required in other instances.”

Other areas that the new guidance

will reportedly clarify include detailing situations where the

responsible lending guidance does not apply (such as small-business

lending) as well as when the guidance does apply outside of mortgages

(such as for credit cards and unsecured personal loans).

However, Mr Shipton emphasised that ASIC’s

new guidance will be “principles-based” rather than dogmatic, and

“provide discretion by financial institutions and lenders, to be able to

exercise their good professional discretion in determining these

areas”, given that there is “always going to nuance” and “unique

situations” in providing finance.

He continued: “There will never be able to be a set of rules or guidance written which will be able to precisely convey and allow for every precise circumstance. That’s why principles-based guidance is important. That’s what we’re going to, that’s what we’re going to be aiming to do.”

New guidelines to be applied by Australia’s banks to debt collection agencies have been released today.

This voluntary Industry Guideline complements the provisions of the Banking Code of Practice (the Code) set out in Chapter 14 (Customers who may be vulnerable), Chapter 41 (Financial Hardship) and Chapter 43 (Recovering a Debt).

This guideline reflects good industry practice and the ABA encourages members to use this guideline to set internal processes, procedures and policies. This Guideline should be read in conjunction with the:

Banking Code of Practice

ABA Industry Guideline: Financial abuse and family and domestic violence policies.

This Guideline will commence operation from 1 March 2020. Contractual arrangements with some debt buyers may not be able to be updated until their contracts are renegotiated. Some necessary changes may not be able to be made until after the 1 March 2020 implementation date – where this is the case banks will endeavour to comply with the guideline on a best endeavours basis in the first instance and where it is brought to their attention that they have not complied with the guideline, they will promptly rectify this issue for the customer.

The new guidelines outline the process banks must follow before they sell any debt and also what happens once that debt is sold. This includes:

Proactively contacting a customer to find other solutions before a debt is sold (this can include restructuring, consolidation and hardship support

Not selling any debt that is in the process of being disputed by a customer

Only contracting debt collectors that follow all regulatory codes and a bank’s own policies for supporting customers in hardship

Regular auditing of all contracted debt collectors to ensure they meet the high standard set by the new guidelines

The bank will require a debt collector to consult with a bank before bankruptcy is initiated, giving the bank an opportunity to repurchase the debt if a vulnerability is identified

As an interim before a government review, each bank will assess the bankruptcy threshold and determine an appropriate level (for competition reasons the industry as a whole cannot set its own level)

If a customer has an ongoing vulnerability and there is no reasonable prospect of the debt being repaid a bank will not sell this debt.

As part of the new guidelines the Australian Banking Association, along with consumer groups the Consumer Action Law Centre, Financial Counselling Australia and the Financial Rights Legal Centre, have written to Federal Attorney General Christian Porter requesting a review of the $5,000 threshold for forced bankruptcy.

CEO of the Australian Banking Association Anna Bligh said the new guidelines contained a wide range of new measures which would increase protections for customers with unsecured debt.

“Banks are stepping up to the plate to ensure vulnerable customers are protected and supported when struggling with unsecured debt such as credit cards and personal loans,” Ms Bligh said.

“Under the new guidelines banks will rigorously audit debt collectors to ensure customers are being treated fairly and with appropriate care, they’ll have the option to buy back debt before any bankruptcy proceedings begin and other significant increases in customer protections,” she said.

Fiona Guthrie, CEO of Financial Counselling Australia said “”Financial counsellors appreciate the speed with which the banking industry has responded to concerns about the mis-use of forced bankruptcy.

“This new guide includes some really important protections, including that even if a bank sells a debt, the debt purchaser cannot move to forced bankruptcy without the permission of the bank,” she said.

Gerard Brody, CEO of the Consumer Action Law Centre said “We applaud banks taking practical action to ensure forced bankruptcy is the last resort possible.”

“It is so important that debt buyers understand customer circumstances and explain why bankruptcy is appropriate before taking this sort of harsh debt collection action.

“No one should risk losing their home because they’ve found themselves in a vulnerable financial position,” he said.

CEO of Financial Rights Legal Centre Karen Cox said they appreciated the banks’ swift response on this important issue.

“This Guideline should mean that small bank debts do not easily lead to homelessness and disproportionate financial loss,” Ms Cox said.

We also appreciate the support of the banks in calling for an increase in the bankruptcy threshold so that people are no longer subject to similar risks from other types of small debt,” she said.

The chief executives of the big four banks have doubled down in defence of their mortgage pricing decisions after being accused of profiting off a “loyalty tax” imposed on customers. Via The Adviser.

Appearing before the House of Representatives standing committee on

economics on Friday (15 November), NAB chairman Philip Chronican and ANZ

CEO Shayne Elliott denied that the banks have been “profiting from

inertia” by charging existing mortgage customers higher rates in a lower

rate environment.

Deputy chair of the committee and Labor MP Andrew Leigh accused

the banks of imposing a “loyalty tax” on existing borrowers, which do

not receive rate discounts offered to new customers.

In response, NAB chairman Philip Chronican said there were a range of

factors influencing the bank’s pricing decisions, adding that the level

of discounting on a particular loan was determined by the

characteristics of the credit contract.

“On our variable rate mortgage products, we charge different rates

for different products for a whole range of reasons,” he said.

“The overwhelming majority of our variable mortgage rate customers,

in fact, 97 per cent, have discounts below the standard variable rate,

and each of those discounts are set with reference to the riskiness of

the loan, the size of the loan, and the combination of business that the

customer brings in.

“The discount is for the life of the loan, unless of course the

customer, at their discretion, comes back and wants to reunite with us

or refinance with another organisation if they can get a better deal.”

Mr Chronican said that in light of cuts to the cash rate, the bank has offered existing customers reviews of their home loans.

“We offer all of our customers a review of their mortgage and have

called all of our customers over the past 12 months, asking if they’d

like a review of their mortgage,” he said.

“In the month of October alone, 15,000 customers took advantage of that and we increased the discount on those.”

However, deputy chair of the committee Andrew Leigh pressed Mr

Chronican, asking: “Why is it that customers have to respond to a

request for a review rather than simply receiving the same rate as a new

customer would get? Aren’t you profiting from inertia?”

To which Mr Crhonican responded: “It doesn’t exactly feel like that. It’s a competitive market to get new business.

“We are accurately conscious that we want to retain our customers,

but as I’ve explained, the differences are not as great as many people

make them out to be.

“We compete at a point of time to get a customer, and we quote a discounted rate to get them and be competitive.”

He conceded: “We are conscious that overtime, those rates become

uncompetitive, but [it’s] hard to have an individual negotiated rate if

everybody has to get the same rate.”

Meanwhile, ANZ CEO Shayne Eliot flatly rejected claims that the bank

has been charging a loyalty tax, also citing competitive pressures.

“I don’t accept the concept of loyalty tax. What we do is we

competitively priced our products every day to offer the best price that

we can for the services that we provide,” he said.

“Given the nature of our products, you will no doubt be referring to

that there is a difference between what is known as the front book and

the back of book; the pricing that we charge a new customer today versus

the customer yesterday, or previously.

“But we don’t impose a tax. It’s an outcome of a highly competitive well-functioning market.”

When asked if it was “unusual” to charge customers different prices for

the same product, Mr Elliott said: “Well, it’s not the same product,

with respect. A mortgage today is not the same as a mortgage tomorrow or

week ago.

“We price mortgages on the day based on the environment they’re in,

the cost of funds on that day, the risk environment on that day and the

competitive environment on that day, so I’m not sure that they are

equivalent products.”

Scrutiny over the pricing behaviour of the big banks recently

intensified following their failure to pass on the RBA’s full 25 basis

point cuts to the cash rate.

This triggered Treasurer Josh Frydenberg to commission the Australian Competition and Consumer Commission (ACCC) to conduct a Home Loan Price Inquiry. The inquiry will review pricing behaviour from 1 January 2019 to examine:

the differences between advertised rates and the prices actually charged or paid;

the differences between rates paid by existing customers and those

paid by new customers (front and back book pricing behaviour);

pricing decisions in response to changes to the official cash rate; and

factors preventing customers from switching to cheaper home loans.

In exploring these matters, the ACCC will consider consumer decision

making and biases, information used by consumers, and the extent to

which lenders may contribute to consumers paying more than they need to

for home loans.

ANZ chief Shayne Elliott has revealed he was sent three remediation letters from the bank, insisting that the company will refund every single customer it has wronged, via Investor Daily.

Appearing

before a parliamentary committee on Friday, Mr Elliott commented many

customers receiving remediation wouldn’t have known there was an issue

at the time, pointing to himself as an example.

The bank is in the

process of working through 247 problem products and around 250 issues,

assessing customers and determining whether they were charged the wrong

interest or fees.

The majority of issues were revealed to be

associated with the banking side, rather than the wealth segment and

“fees for no service”.

“So the million customers that we’ve

refunded today, most of them got a cheque in the mail and a nice little

letter and they didn’t even realise it,” Mr Elliott said.

“I’ve had three. One was $30, one was $27 and one was $80. The average amount that’s being repaid out, you can do the maths.

“It’s

important we get the money back; I’m not diminishing that. But we are

remediating every single case. There’s nothing to do with complaints.

This had to do with we have discovered a mistake, and we have gone and

put it right.”

Mr Elliott predicted there are around 3.4 million

customers in total who are owed refunds from the bank, with around

one-third having received their remediation.

ANZ has set aside

$1.6 billion in reserves for remediation, with the amount that has been

refunded so far ($l67 million) being around a tenth of that.

Mr Elliott conceded the bank’s progress through returning customers’ money has been “modest”.

“We’ve taken provision of around $1.6 billion of that, maybe around $400 million has more to do with cost,” he said.

“That’s the cost of getting the money back.”

The

bank now has 1,100 staff working sorely on remediation, with a further

estimated 600-700 full-time employees lending a hand from other

departments. ANZ has around 38,000 staff in total.

Mr Elliott said ANZ will give the remediation team all of the resources it needs.

“That

team has no restriction on number of people they need to hire, none.

They can hire as many people as they want,” Mr Elliott said.

“They

have no budget restriction. Yeah, the restriction in a sense, the

binding constraint, if you will, is not money or headcount, its

expertise.

“We want to finish those [remediation programs] and

find any other problems we have. We have a productive program where we

are searching through every single product and process we have to see if

there’s anything that needs remediating, big or small, we add it to the

list and we get it done as fast as possible,” he said.

Despite

the bank’s remediation process having had a gradual pace, as far as Mr

Elliott is concerned, it is in the bank’s best interest to complete the

refunds as fast as it can.

“My shareholders have already paid the $1.6 billion, it’s gone from their accounts, it’s gone,” he said.

“So

when we take that provision, we’ve expensed it. So there is no benefit

in delay. So now actually, there’s benefit in speed because the delay

costs money because the longer [it is], the accrued interest keeps

mounting up, and I have to pay more and more.

“There might be a

perverse incentive to not discover issues, if that makes sense. But once

you’ve discovered them, we have a legal obligation to provide and

expense the money. The 1.6 billion, as far as we’re concerned is we’ve

spent it – so now the sooner we get that money back to customers, the

better.”

Today I would like to address some of the issues that have been

raised in relation to responsible lending and demonstrate two facts.

First, that the concerns are misplaced. Second, the principles

underpinning these provisions remain sound, even in the changed economic

environment since 2010.

At the outset I want to emphasise that our guidance is just and only that,

guidance. It does not have the force of law. The fact that we are

updating our guidelines, does not change the law, which has been in

place since 2010. However, what has been made abundantly clear to us in

the course of our consultations, is that industry would welcome more

assistance in interpreting how to meet responsible lending obligations.

Put simply, this is what we are endeavouring to achieve. We are not, and

never have sought to impede the flow of credit to the real economy.

I want to take this opportunity to reflect upon three broad questions

that keep recurring in the work we are doing to update our guidance:

Why does responsible lending matter?

Why is ASIC updating its guidance, and why now?

What does an update to the guidance mean in practice for lenders and what will it achieve?

And importantly, along the way I will respond to some misconceptions

about responsible lending. There are some myths that need busting to

address exaggerated and inaccurate criticisms about our consultation on

revising this guidance.

Why does responsible lending matter?

Responsible lending is fundamentally about the credit industry’s

commitment to dealing fairly with its customers. Ensuring robust and

balanced standards of responsible lending to consumers has been, and

will continue to be, a key priority for ASIC.

Consumer credit is part of the life blood of our society and economy. A report by Equifax Australia in July 2019 estimated that 4.4million applications for consumer credit were expected to be made in the 6 months to the end of the year[1].

Inappropriate lending can have devastating consequences for

individuals and families, and on a broader scale, can undermine

confidence in financial markets.

Australia introduced a national consumer credit regime in 2009 to

avoid excesses in lending and predatory lending to consumers. In the

preceding period, the impact of the financial crisis had revealed a

number of shortcomings in policies and practices at financial

institutions abroad. Some of these practices were clearly aimed at

taking advantage of vulnerable borrowers.

Although lending standards in Australia were not as lax as other

countries, during the pre-crisis period the share of ‘low doc’ loans

written in Australia had grown strongly in the lead up to the crisis[2].

The responsible lending law reforms were introduced to Parliament to

curb undesirable market practices that many were concerned about at the

time, including[3]:

providing or recommending inappropriate, high cost and potentially unaffordable credit;

upselling of loans to higher amounts than were necessary to fulfil the consumer’s needs;

unscrupulous lenders providing consumers with unaffordable loans

that will default – thus facilitating the recovery of the equity in the

consumer’s home; and

inadequate financial disclosure, poor responses to financial difficulty and unsolicited credit limit increases.

The core principle behind this regime is simple and has not changed

since 2010 – despite what many critics and commentators have been

saying. A licensee must not enter into, or suggest or assist a customer

to enter into, a contract that is unsuitable. None of this is new. To

ensure this outcome the licensee must:

First – gather reliable information that will inform the licensee

about what the consumer wants and their financial situation. This

involves making reasonable inquiries about the consumer’s requirements

and objectives in relation to the credit product, and the consumer’s

financial situation, and taking reasonable steps to verify the

consumer’s financial situation.

And then, second – assess whether the contract will be ‘not unsuitable’ for the consumer.

Why is ASIC updating its guidance on responsible lending and why are we doing it now?

Since the introduction of the responsible lending laws, ASIC has

regularly reviewed industry practices and identified a range of

compliance issues. Some examples of our work include:

In 2015 we reviewed industry’s approach to providing interest-only

home loans. We identified practices that could result in borrowers being

unable to afford their loan repayments down the track, and we suggested

to lenders that they needed more robust processes to improve the

accuracy of their assessments regarding capacity to repay.

This was followed in 2016 by our review of large mortgage broker

businesses. This review resulted in ASIC setting out further actions

which credit licensees could take to reduce the risk of being unable to

demonstrate compliance with their obligations.

Alongside our industry reviews, we’ve undertaken a number of

enforcement actions to improve compliance. Our actions against The Cash

Store, Bank of Queensland, BMW Finance, Channic, Motor Finance Wizard,

ANZ (Esanda), and Thorn Australia send a clear message to industry and

consumers that ASIC will take action to stamp out irresponsible and

predatory lending, and deter breaches of the law.

More recently, the Royal Commission into the financial services

sector found some major shortcomings in the way in which responsible

lending laws were being applied by lenders.

At this point, I should say something briefly about the decision in

the proceedings that ASIC took against Westpac in 2017 – the so-called

‘Wagyu and Shiraz’ case. This preceded the Royal Commission, and

Commissioner Hayne did not directly address ASIC’s case against Westpac.

ASIC was unsuccessful in this matter and while we respect the judgment,

we have lodged an appeal.[4]

Almost every commentator has criticised this decision and suggested

that ASIC’s appeal creates avoidable uncertainty. Our objective in

appealing this decision is, in fact, to clarify the application of the

law. And we believe that doing so is in the best interests of both

consumers and lenders. It is an important part of ASIC’s mandate to

clarify the law where there is uncertainty, and thereby support and

guide industry to understand their obligations.

We decided to appeal because we consider that the decision creates

uncertainty about what a lender is required to do to comply with its

obligation to make an assessment of whether a loan is not unsuitable for

the borrower. And, if the judgment is to be understood as standing for

the proposition that a lender may do what it wants in the assessment

process (as His Honour found), then we consider that to be inconsistent

with the legislative intention of the responsible lending regime. The

Westpac case relates to the period between December 2011 and March 2015,

and although in the years since we have seen some improvements in

responsible lending standards amongst the industry, there is a real risk

that uncertainty in the approach required by lenders to comply with the

law could result in slippage by some lenders.

Put simply, we believe that the judgment left it too unclear what

steps are required of a lender. We are seeking clarity by appealing.

The proper forum to debate this is now the Full Federal Court. Like any

other litigant, we are availing ourselves of access to an appellate

body. We should not be criticised for accessing the Courts to resolve a

dispute, as all regulators do from time to time.

Notwithstanding our appeal in the Westpac case, we consider that ASIC

should still provide updated guidance mindful that the appeal has not

yet been heard. All of the ingredients necessary are there – judicial

decisions, ASIC enforcement action, thematic reviews, the Royal

Commission, changes to technology. The updated RG209 looks to build on

the existing guidance, which we believe is fundamentally sound, and to

bring those developments together in a single, instructive guide and to

clarify and provide more certainty to industry in key areas where we

can.

Some misconceptions about responsible lending

There are a number of myths and exaggerated claims about the supposed

effects of the responsible lending laws that need to be addressed.

These claimed effects are either not supported by the facts or data, or,

if they are real, they are the result of a fundamental misunderstanding

and misapplication of the law.

Let me address a few of the most significant.

The first is the suggestion that small business lending is negatively affected by the responsible lending obligations.

There has been a lot of misinformation published recently in the

media and in the current corporate reporting season about the effect of

the responsible lending requirements on small business lending.

The responsible lending obligations administered by ASIC apply to credit provided to individuals for:

personal, domestic and household purposes (this includes buying/improving a home); and

residential investment purposes (this includes buying/improving/refinancing residential property for investment purposes).

They apply also to loans to strata corporations for these same

purposes. This is the one, very niche, area of application of the

responsible lending obligations to an entity rather than an

individual.

Otherwise, a loan to a company (including small proprietary companies) for any purpose is not subject to the responsible lending obligations.

Where there is a loan to an individual, the purpose of the loan

determines whether the loan is subject to the responsible lending

obligations. The nature of any security for the loan does not affect

this test, nor does the source of income to pay the loan back. In other

words, it is not an asset test but a predominant purpose test.

A loan to an individual predominantly for a business purpose is not

subject to responsible lending obligations. ‘Predominant’ simply means

‘more than half’.

So, if someone borrows $500,000 of which $300,000 is to be used to

establish a small business, and the remainder for making home

improvements, the loan is not subject to the responsible lending

obligations.

Similarly, if a small business operator obtains a loan to purchase a

motor vehicle which is to be used 60% of the time for work purposes but

will also be available for personal use, the loan is not subject to the

responsible lending obligations.

A loan to an individual for business purposes secured over a borrower’s home is not subject to the responsible lending obligations.

Of course, a lender may choose to apply its responsible lending

processes to business loans for its own commercial reasons to manage its

credit risk portfolio or to meet its prudential obligations.

AFCA in its role as the dispute resolution scheme for the credit

industry deals with both small business loans and consumer loans. There

has been some confusion in industry about whether the responsible

lending obligations are going to be applied by AFCA in relation to small

business loans. In evidence at ASIC’s public hearings in August this

year, AFCA undertook to clarify this misunderstanding in its forthcoming

guidance to its members.

There has also been a suggestion that ASIC’s guidance and

consultation has caused increases to credit application processing times

or rejection rates.

Contrary to some anecdotal statements, the evidence and data do not

point to ASIC’s guidance in RG 209 or our consultation to revise this

guidance, as having caused increases in credit application processing

times or rejection rates.

We do accept that, following the commencement of the Royal

Commission, lenders began to review their approach to responsible

lending and to tighten standards. And that these reviews, prompted by

the Royal Commission and not by ASIC’s guidance (which,

remember, has been unchanged since November 2014), have resulted in

them seeking more detailed information from borrowers and necessitated

some systems upgrades and staff training.

To the extent this had any effect on processing times, it was only at

the margins. In coming to that conclusion, we have actively sought

information about processing times.

The Australian Banking Association (ABA) recently disclosed

information to ASIC that shows, on average, approvals for mortgage loans

for ABA members in late 2018 took 4 days longer than they had in early

2018, but that by mid-2019 this had decreased to be just 2 days longer.

During ASIC’s recent public hearings in August, we asked some of the

major banks and other lenders about changes to loan application times

and rejection rates:

one bank confirmed it has not experienced material changes and approved between 80-85% of applications; and

two banks attributed any changes they have experienced to changes in demand for credit and changes in the bank’s own processes.

And, illustrative of the fact that adherence to responsible lending

laws does not have to spell lengthy processing times, Tic:Toc (a smaller

on-line lender) told us that their fastest time from a consumer

starting an application to being fully approved is 58 minutes. And that

includes full digital financial validation of the consumer’s financial

position.

The ABA has not indicated any direct impact by ASIC on ABA members’

processing times. The reasons given for an increase in approval times

instead included:

a new APRA reporting framework (inspection of record keeping);

an APRA review leading to internal changes to processes and procedures;

satisfying new risk limits imposed on certain lending by APRA;

AFCA decisions influencing interpretation of regulatory requirements; and

reinterpretation by the ABA members of responsible lending requirements.

Anecdotally, we have also heard of instances where front-line lending

officers are seeking to escalate loan approval decisions to their

managers, which may also have added to perceived delays.

Finally, there has been a suggestion that responsible lending has had a negative effect on economic growth.

We do not accept this. The evidence and data available to ASIC do not

suggest that the decision to update our guidance has contributed to the

current state of the economy by limiting access to credit.

Indeed, lending trend reports published by the ABA show that banks

are still lending – approval rates remain between 85-90% for home

lending and 90-95% for business lending (the latter of course should not

be captured by our guidance on the responsible lending obligations).

Instead, the main reason for slower credit growth has been a decline

in the demand for credit. Statements made during ASIC’s public hearings,

other information we have collected from industry, and recently

published economic statistics all support this view.

And, in fact, there are signs that this may be turning around.

The Australian Bureau of Statistics reported that (in seasonally

adjusted terms) lending commitments to households rose 3.2% in August

2019, following a 4.3% rise in July. Earlier this week, CBA announced a

3.5% increase in home lending and 2.8% in business lending for the 3

months to October.

This pick-up in recent approvals lends further support to the view

that it is not responsible lending obligations that have been dampening

credit availability. So too do the following sources:

The Reserve Bank of Australia (RBA) continues to comment on the

impact on credit of the construction cycle and of reduced demand for new

housing. The RBA found that housing turnover had declined to

historically low levels (below 4%) and has only just begun to rise.

The ABA lending trend report states that a significant shift in

market sentiment within the housing sector – following the election

outcome, RBA cash rate cut, and lowering of APRA’s serviceability floor –

is likely to be a key driver of a boost in investor loan applications.

In addition, the RBA’s recent Financial Stability Review explained

that uncertainty about the outlook for global economic growth has

increased in the last 6 months, with a greater chance of weak growth.

The Review refers to regulatory measures introduced in December 2014 and

in early 2017 (being the prudential measures put in place) as a ‘speed

bump’ for investment lending and interest-only lending. The Review also

refers to ‘tighter standards’ implemented by lenders, relating to their

own credit risk appetite and policies – these are adopted by banks to

manage their own credit risk exposure, rather than for the purpose of

complying with responsible lending obligations. And, finally, the Review

points to an increase of credit approvals in recent months which the

RBA expects to flow through to higher lending.

What does an update to the guidance mean and what will it achieve?

Our Regulatory Guides are intended to be useful and informative

documents and there has been a great deal of anticipation about the

upcoming revision. There are a few key points I would like to make about

what an update to our guidance means and will achieve.

First – our regulatory guidance was last updated in November 2014,

and the responsible lending obligations themselves have not materially

changed since 2010. For a topic like responsible lending, where the

application of the law continues to be clarified through court

decisions, and where the industry’s technologies and systems evolve and

change, it is appropriate to conduct periodic reviews and updates of our

guidance.

Second – the consultation process has involved multiple steps. We

allowed three months to receive submissions, in order to get thoughtful

and broad feedback. We exercised our power to conduct public hearings –

for the first time in more than 15 years. This proved to be a very

useful and respectful forum to talk to industry participants about their

views. We have also recently concluded a group of round-table sessions

with stakeholders including ADIs, non-bank lenders, brokers, providers

of small amount credit contracts and consumer leases, and consumer

representative groups. This enabled us to test and distil the

conclusions we were drawing on necessary changes.

Third – it is critical everyone is clear that our guidance does not,

and the revised guidance will not, create new obligations. Simply

because it cannot do that. Our regulatory guides are just that – guidance – about approaches that licensees can adopt to reduce the risk that they fail to comply with the responsible lending laws.

Fourth – The submissions were wide ranging, but many made the point

that they were looking for more guidance not less, albeit while

retaining flexibility to exercise judgments in implementing responsible

lending practices.

We made it very clear in the consultation paper that we wanted to update and clarify our existing guidance and provide additional guidance.

When we release the updated regulatory guide in a few weeks, I urge

licensees to take the guidance on board and to compete with each other

on the quality of products and services to consumers. Not focus on

processes which merely seek to achieve a minimum level of compliance.

Conclusion

In conclusion, I hope that I have given context for what we are doing

and why, and busted some myths about the practical effects of

responsible lending.

We all have a role to play to ensure that both consumers and

investors can continue to have confidence in the efficient and fair

operation of our credit markets. As the leaders and responsible managers

of our credit institutions, it falls to you to implement processes that

ensure consumers are provided with products that are affordable for

them and suit their needs.

We intend for our update to Regulatory Guide 209 to provide greater

clarity to industry. All the same, there is little doubt that we will

continue to be engaged in conversation with industry about responsible

lending.

Australians in dispute with their

bank, insurance provider, super fund, or other financial firms have lodged

73,000 complaints with the financial sector’s new ombudsman and have been

awarded $185 million in compensation, in the first 12 months of its operation.

The Australian Financial Complaints Authority (AFCA) is celebrating 12 months since it opened its doors as the nation’s one-stop-shop for complaints about financial firms, replacing three former external dispute resolution schemes.

People made 73,272 complaints to

AFCA between 1 November 2018 and 31 October 2019. This represents a 40 percent

increase in complaints received compared to AFCA’s predecessor schemes, which

in the 2017/18 financial year received a combined total of 52,232 complaints.

Of the complaints made, 56,420 have

been resolved with the majority resolved in 60 days or less.

Research conducted in July this

year showed that just three percent of Australians knew about AFCA. Yet,

despite the need to raise awareness, Australians are making nearly 200

complaints a day.

AFCA Chief Executive Officer and

Chief Ombudsman David Locke said AFCA was a fair, free and independent service

that was fast becoming valued by the public and its members for its approach to

dispute resolution.

“Every day we continue to hear from

people who are dissatisfied with the way their financial firm has handled their

complaint. These matters have not been resolved internally by financial firms

and so the individual then brings their complaint to AFCA,” Mr Locke said.

“We take our commitment to fairness

and independence very seriously, and where possible we encourage the financial

firm and complainant to resolve the matter among themselves. The statistics

show that this happened with 70 percent of all claims resolved in the past 12

months.

“Still, the increase in complaint

numbers we are witnessing at AFCA indicates that there is still work to be done

by firms to improve their practices and restore public faith in financial

firms. AFCA will continue to focus on member engagement to help firms to

enhance their own internal dispute resolution procedures.”

Mr Locke said he was proud of the

significant milestones that AFCA and its people had achieved in its first year

of operation.

“Establishing AFCA as a new

organisation and handling a 40 percent increase in complaints was never going

to be easy and we are still improving the way we operate,” he said.

“I am very proud of the AFCA team

and what has been achieved so far. I am fortunate to work with a great team of

people who are professional, passionate about fairness and independence, and

who care about our customers.

“AFCA has also been in a major growth

phase of staff to meet demand and has launched the first leg of a national

roadshow to promote its service across the country.

“The Financial Fairness Roadshow

has been a great success. So far we’ve been to 26 locations across Tasmania,

Victoria, the ACT and regional New South Wales, where we’ve spoken with more

than 7,000 people.

“We plan to tour the rest of the

country in the first half of 2020.”

Mr Locke said AFCA had also hosted

forums for small business, consumer advocates and AFCA members in 10 locations

coinciding with the Roadshow’s itinerary.

In a fresh blow to Westpac, the Federal Court this morning delivered the corporate regulator a win in its appeal against a previous ruling on Westpac’s telephone campaigns. Via Financial Standard.

The full court this morning

said ASIC’s appeal will be allowed with costs, while Westpac-related

companies’ cross-appeal will be dismissed.

In 2014 and 2015, Westpac ran telephone and snail-mail campaigns to encourage customers to roll over external superannuation accounts into their existing accounts with Westpac Securities Administration Limited and BT Funds Management.

ASIC was primarily concerned with the telephone calls.

The

corporate regulator claimed that the two Westpac companies had breached

their FoFA-stipulated best interest duty by advising rollovers to

Westpac-related super funds without a proper comparison of options, as

required by law.

And so, it initially launched civil penalty proceedings against the two Westpac subsidiaries in December, 2016.

The

Federal Court handed down its judgment in January this year, with a

mixed outcome. It decided that ASIC had failed to demonstrate that the

two Westpac companies had provided personal financial product advice to

15 customers in regards to the consolidation of superannuation accounts.

However,

the judge added the Westpac subsidiaries contravened the Corporations

Act in 14 of 15 customer phone calls by implying the rollover of super

funds into a BT account was recommended. This came about through a

“quality monitoring framework” where BT staff were coached in sales

technique.

ASIC appealed the January judgment. Westpac also made a counter appeal.

ASIC has imposed additional licence conditions on the Australian

financial services (AFS) licence of IOOF Investment Services Ltd (IISL)

as part of an application by IISL to vary its licence.

IISL sought a variation to its licence to facilitate the transfer of

managed investment scheme, investor directed portfolio services (IDPS)

and advice activities from IOOF Investment Management Ltd (IIML) to

IISL. The transfer is part of a reorganisation of the broader corporate

group (IOOF Group).

In granting the licence variation, ASIC has decided to impose

additional conditions relating to the governance, structure and

compliance arrangements of IISL.

ASIC’s decision to impose additional licence conditions took into

account concerns highlighted by the Financial Services Royal Commission

about the real and continuing possibility of conflicts of interests in

IOOF Group’s business structure, ASIC’s past supervisory experience of

these entities and material supplied by IISL as part of its licence

variation application. IISL agreed to the imposition of the additional

licence conditions.

In summary, the additional conditions specifically cover:

governance – by requiring that IISL has a majority of

independent directors with a breadth of skills and background relevant

to the operation of managed investment schemes and IDPS platforms;

the establishment of an Office of the Responsible Entity (ORE) – that is adequately resourced and reports directly to the IISL board, with responsibility for:

oversight of IISL’s compliance with its AFS licence obligations;

ensuring IISL’s managed investment schemes are operated in the best interests of their members; and

overseeing the quality and pricing of services provided to IISL by all service providers (including related companies),

the appointment of an independent expert, approved by ASIC, to report on their assessment of the implementation of the additional licence conditions.

ASIC Commissioner Danielle Press said, ‘ASIC is serious about

improving the quality of governance and conflicts management across the

funds management sector and ensuring that investors’ best interests are

the highest priority of fund managers.

‘ASIC will use its licensing power, including through the imposition

of tailored licence conditions to address governance weaknesses, the

risk of poor conduct or vulnerabilities to conflicts of interest in a

licensee’s business model.’

The Australian Prudential Regulation Authority (APRA) has advised that it will not appeal the Federal Court decision to dismiss APRA’s court action against IOOF entities, directors and executives.

The case examined a range of legal questions relating to superannuation law and regulation that had not previously been tested in court, relating to the management of conflicts of interest, the appropriate use of superannuation fund reserves and the need to put members’ interests above any competing priorities.

APRA had initiated the action last December due to its view that IOOF entities, directors and executives had failed to act in the best interests of their superannuation members. Before taking the court action, APRA had sought to resolve concerns with IOOF over several years but considered that it was necessary to take stronger action – through use of directions, conditions and court action – after concluding the company was not making adequate progress, or likely to do so in an acceptable period of time.

After receiving the judgment on 20 September, APRA reviewed the reasons for the decision and concluded that it will not appeal the matter.

APRA Deputy Chair Helen Rowell said the judgment nevertheless raised some issues of wider importance for APRA in its supervision of superannuation trustees. APRA is considering any further action that may need to be taken in relation to these, such as revising its prudential standards or seeking legislative amendments, to ensure that member interests are protected to the maximum extent possible.

APRA notes that, notwithstanding the decision not to appeal the judgment, additional licence conditions that APRA imposed on IOOF in December remain in force and APRA’s strengthened supervision focus on ensuring that IOOF implements the changes needed to comply with these conditions continues.

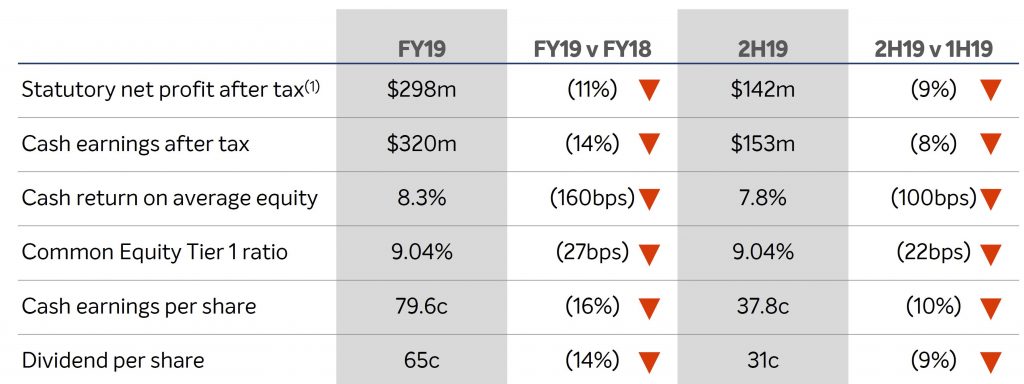

Bank of Queensland today announced FY19 cash earnings after tax of $320 million, down 14 per cent on FY18. Statutory net profit after tax decreased by 11 per cent to $298 million. Basic cash earnings per share was down 16 per cent to 79.6 cents per share. We expect many banks to report a similar story ahead.

The Board has announced a final dividend of 31 cents per share, for a full year dividend of 65 cents per share. This is a reduction of 11 cents per share from FY18. The final dividend payout ratio of 82% was consistent with the interim dividend payout ratio.

They described this as “Disappointing results reflect challenging operating environment”, reflecting a challenging operating environment characterised by slowing credit demand, lower interest rates, a rise in regulatory costs and changes impacting non-interest income.

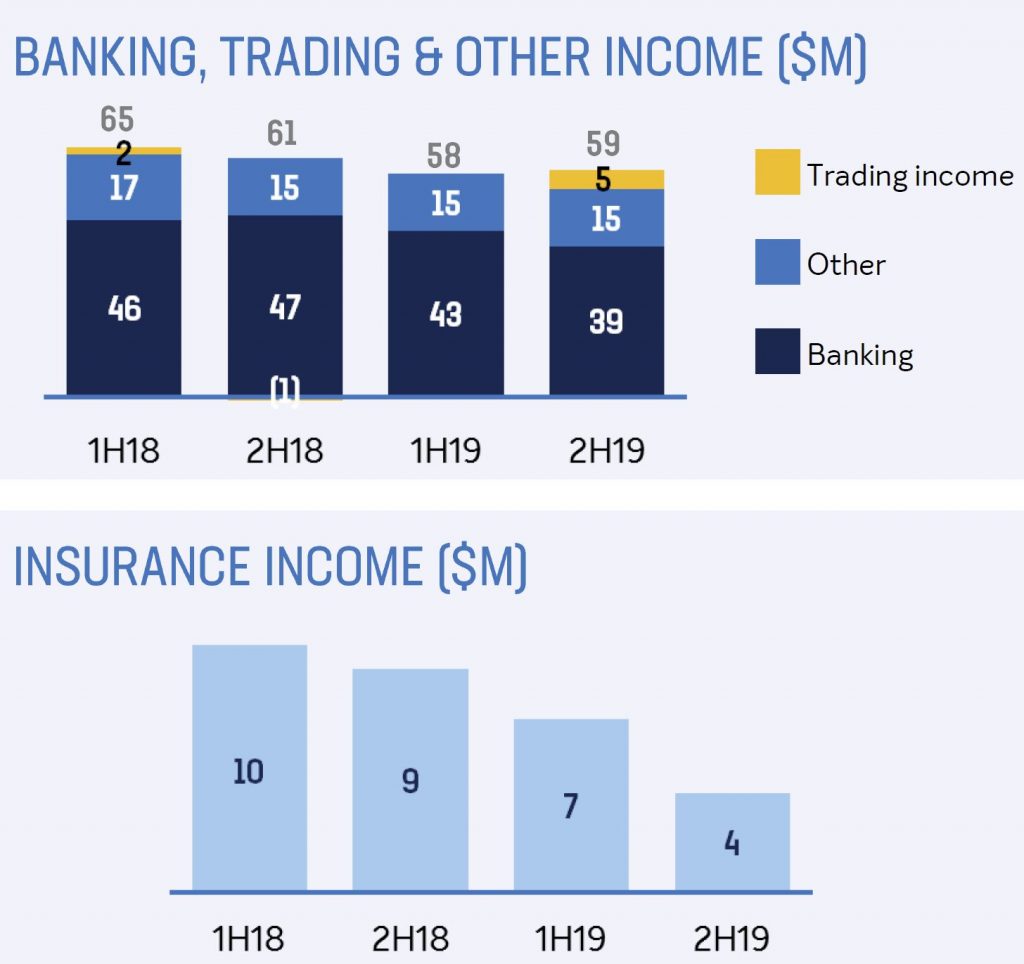

Total income decreased by $21 million or two per cent from FY18.

Net interest income decreased $4 million, driven primarily by a five basis point reduction in net interest margin to 1.93 per cent. This reduction is attributable to the declining interest rate environment and continued strong competition for loans and deposits.

Non-interest income decreased 12 per cent or $17 million, driven by declines in Banking, Insurance and Other income but partially offset by improved Trading income. Banking income reduced $11 million due to lower fee income and a change in arrangements related to BOQ’s merchant offering. Insurance income reduced $8 million or 42 per cent due to changes in the insurance sector which ultimately impacted distribution of St Andrew’s consumer credit insurance through its corporate partners.

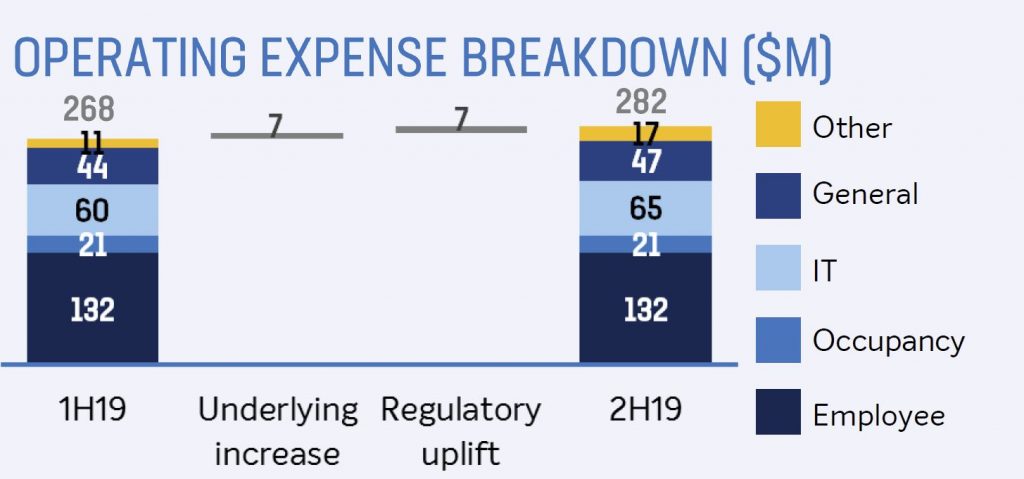

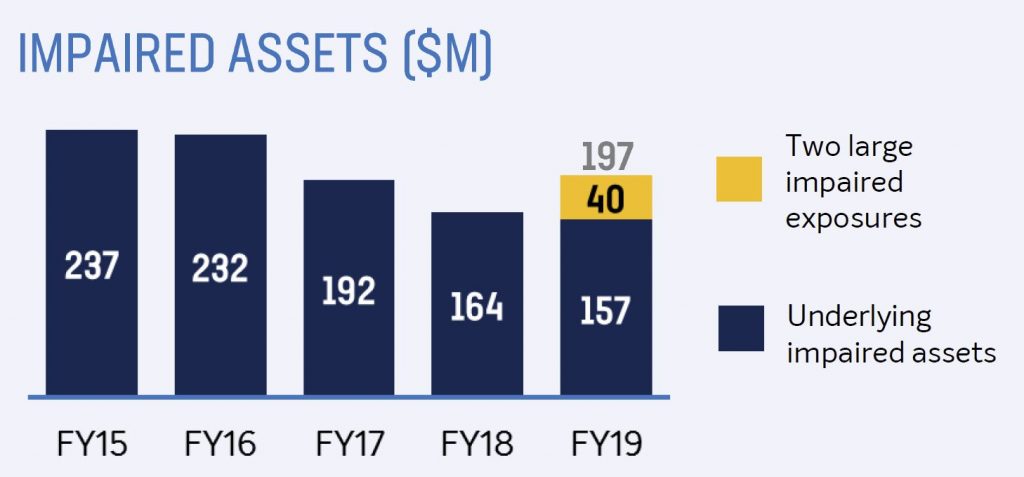

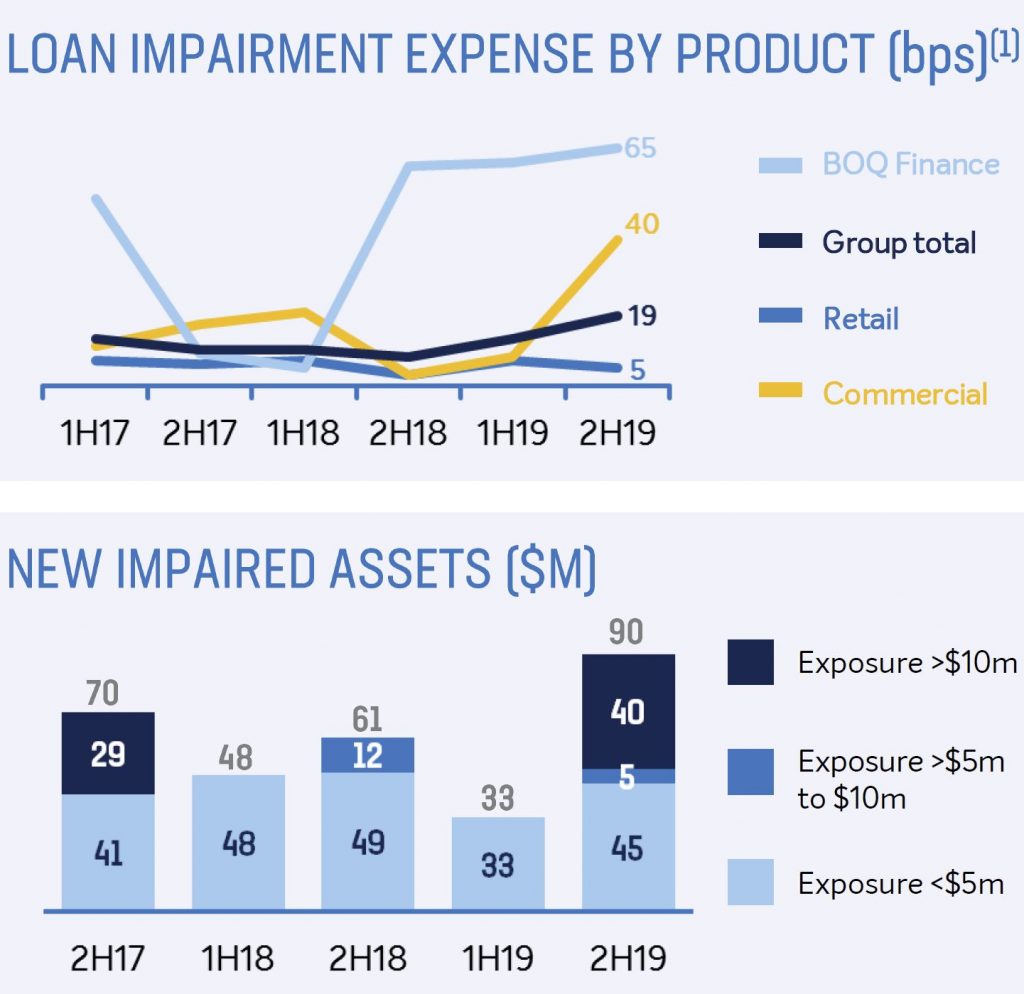

In line with the guidance provided at the 1H19 result, operating expenses increased by $23 million or four per cent from FY18. The increase in expenses was more pronounced in the second half, due to an increase in business deliverables addressing regulatory and compliance requirements. While loan impairment expense increased $33 million to $74 million, equivalent to 16 basis points of gross loans, underlying asset quality remains sound with impairments and arrears remaining at low levels.

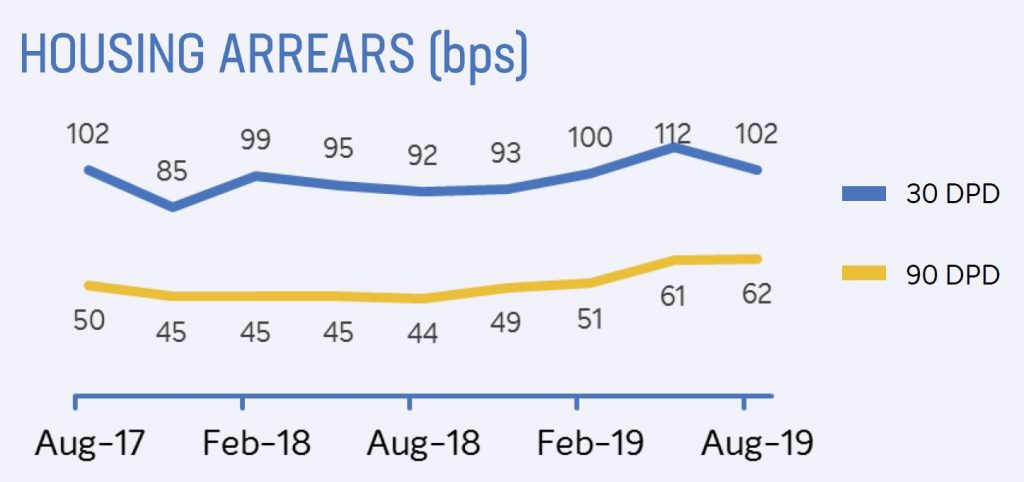

Housing loan arrears over 90 days rose, while 30 day fell.

Implementation of BOQ’s new AASB 9 collective provision model drove an increase in collective provisions due to changes in BOQ’s portfolio and a weaker economic outlook. The increase in collective provisions contributed $22 million of the loan impairment expense uplift.

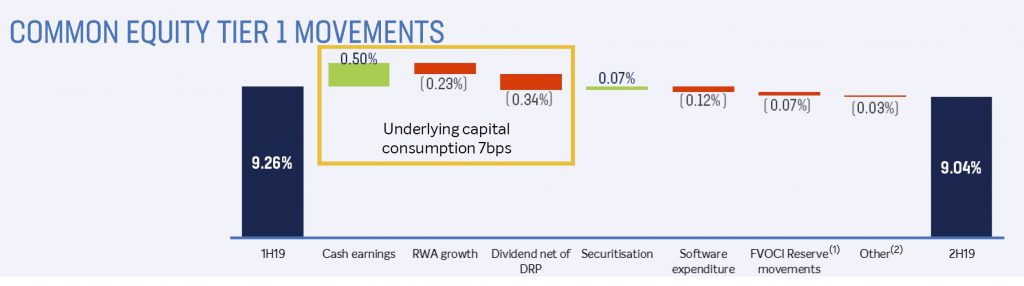

BOQ remains appropriately capitalised with a Common Equity Tier 1 ratio of 9.04 per cent, which is a decrease of 27 basis points from FY18. The reduction was driven by a combination of asset growth being tilted to more capital intensive business lines, increased capitalised investment, reduced earnings and lower participation in the dividend reinvestment plan.

Overall lending growth of two per cent was achieved over the year.

Continued growth momentum was evident in BOQ’s niche business segments. The BOQ Finance portfolio achieved growth of $667 million or 15%, while BOQ Specialist grew lending balances by $756 million across its commercial and housing loan portfolios which are focused on the medical segment. Virgin Money also delivered a consistently strong level of housing loan growth, with the portfolio growing by $914 million to over $2.5 billion.

A key imperative remains rebuilding the foundation for growth in BOQ’s retail bank, which saw a further contraction of $1.4 billion in its residential housing loan book.

Solid progress has also been made across a number of key foundational investments during the year. BOQ’s core technology infrastructure modernisation program has continued to track to plan, with implementation continuing through FY20. This will deliver a more modern, cloud-based technology environment which will allow for improved change capability.

During the year, work began on development of a new mobile banking application for BOQ customers, with a launch expected in 2020. Lending process improvements have also been a key focus to improve customer experience, particularly for home loan applications. A number of regulatory projects have also progressed during the year to address various regulatory and industry changes. These are all critical investments that will support BOQ’s transformation and future aspirations.

Investment in the implementation of a new Virgin Money digital bank has also progressed during the year, with a customer launch planned for 2020. This will require $30 million of capitalised investment during FY20 to complete the phase one build which will deliver a transaction and savings account offering to customers. This is an investment in long term value creation for this iconic brand which has demonstrated success in attracting customers across its existing product suite. It is also anticipated that this investment in a new digital banking platform will be leveraged across the Group in the years ahead.

Commenting on the results and outlook for BOQ, new Managing Director & CEO George Frazis said that there are challenges ahead, however fundamentally, BOQ is a good business.

“Our capital is well positioned for ‘unquestionably strong’, we have a good funding position and our underlying asset quality is sound. “There are numerous opportunities ahead for a revamped BOQ and I will be working closely with the executive leadership team to complete our strategic and productivity review, with a market update on our plans in February 2020,”