Markets require regulators. As Adam Smith, the champion of the invisible hand, notes in The Wealth of Nations, when individual interests are left unregulated they work to turn competitive markets into monopolies.

But what happens when regulators meant to check individual interests fail to promote the public interest?

Consider Australia’s banking sector. The banking royal commission has

found plenty of fault in the ways the corporate and prudential

regulatory agencies performed their vital roles – due not to lack of

power but an unwillingness to use that power.

University of Chicago economist and 1982 Nobel laureate George

Stigler was the first to outline how regulators can become “captured” by

the very firms and industries they are meant to be regulating,

beginning with an article in 1971.

Stigler’s idea has come to be known as “regulatory capture theory”,

and it causes us to confront the uncomfortable question of how to ensure

regulators act in the public interest, not in the interest of the firms

they regulate.

Supply and demand

Stigler thought about regulation through the lens of supply and

demand. Self-interested politicians supply regulation. Firms demand it –

usually because they want a competitor regulated.

His classic example concerned regulations on the weight of trucks

that could travel on state roads in the United States in the 1930s. He

found empirical evidence that where trucks were more of a threat to

traditional train transport (like on short-haul routes where railroads

were less competitive) more stringent weight limits were enacted.

Rather than the regulator being a beneficent protector of the general

public interest, it had become a self-interested actor responding to

political pressure from the railroad owners.

This may strike you as rather cynical, but there is a swathe of evidence that across industries and time, regulators often act more in the interests of industries than the public.

These regulations usually have a plausible rationale behind them.

Consider licensing of doctors. Nobody wants a poorly trained doctor let

loose on them, so some form of certification makes sense. But does the

medical profession limit the number of doctors and exclude

foreign-trained doctors to push up their incomes? You be the judge.

It’s easy to think of other examples: “tickets” in the construction

industry, certification of train and truck drivers in mining, licensing

of plumbers, and on and on.

There are lots of ways this can arise. Politicians often depend on

support and campaign contributions. And there is all too often a

revolving door between regulators and the regulated.

Financial regulators

This brings us to the regulation of Australia’s banks.

The corporate and prudential regulatory agencies may have been

unwilling to use their power, but the the big four banks were not.

And the banks have plenty of power – financial and political. They

are utterly vital to the operation of the entire economy. They are among

the very largest companies in the country (so a lot of retirement

savings are invested in them). And they employ a lot of people.

We should stop assuming the Australian Securities and Investments

Commission and the Australia Prudential Regulatory Authority, among

others, are unquestionably acting in the public interest and start

asking a bunch of questions.

What are the backgrounds of the people who head up these

organisations and what perspective does that lead them to bring to the

job? What jobs do they get after they leave the regulator, and how might

that affect their motivations while acting as regulator? What would be

the social sanction imposed on them if they decided to get really tough

with financial industry players?

Regulators typically aren’t bad people. But sometimes they have bad

implicit incentives. And the laws they are tasked with enforcing often

favour a particular group – quite frequently those being regulated.

What about the politicians who make the laws in the first place? Are

they really acting for all Australians with a thoughtful and balanced

perspective? Or do they represent tribal interests?

We need to close revolving doors, provide more resources to regulators and scrutinise what they do much more. Let’s not be naive about regulation.

Author: Richard Holden, Professor of Economics, UNSW

While the banks would hope the fall-out from the Royal Commission can now be contained, and business as usual can apply, it seems another Inquiry is on the cards down the track, further evidence of continued pressure on the sector.

Treasurer Josh Frydenberg has told the banks and regulators that they will face an inquiry down the track to ensure they have lifted their game post-royal commission; via InvestorDaily.

In a letter to the ABA, ASIC and APRA, Mr Frydenberg directed the organisations to implement Commissioner Kenneth Hayne’s recommendations from the final report directed at them.

The Treasurer sent out three letters to the heads of the organisations and made it clear that the government wanted to see lasting change within the sector.

“We will establish a follow-up independent inquiry, commencing in three years, to assess changes in industry practice and consumer outcomes since the royal commission,” said Mr Frydenberg.

Alongside implementing recommendations, Mr Frydenberg underlined the importance of ASIC changing its approach to enforcement, particularly shifting to a ‘why not litigate’ stance.

“I am aware that change is already underway, including through the establishment of the Office of Enforcement within ASIC, the move to a ‘why not litigate’ approach to enforcement and the introduction of initiatives such as close and continuous monitoring, to more intensively supervise the sector,” Mr Frydenberg wrote.

Mr Frydenberg committed to ASIC it’s continued support in providing new powers, expanding its role as a super regulator, removing barriers and strengthening penalty provisions.

“The government remains committed to ensuring that ASIC has the resources it needs, and will give further consideration to ASIC’s resourcing needs as part of the 2019–20 budget,” he said.

ASIC and ABA were also told by Mr Frydenberg to work together to create an enforceable banking code of conduct.

“I also expect the ABA to work co-operatively with ASIC to have the relevant provisions of the banking code approved as ‘enforceable code provisions’ as soon as practicable after legislation providing ASIC with these powers has been enacted,” he said.

In a letter to the ABA, the treasurer said he expected the banking code to be amended to support more inclusive practices, expand the definition of small business and eliminate default interest from being charged on loads declared to be impacted by natural disasters.

Mr Frydenberg told ABA chief executive Anna Blight that it was imperative that its members commit to putting customers at the heart of their business.

“I ask that you work with your members to take action and truly commit to restoring trust in the financial system. Only strong and decisive action of the kind that leads to lasting change, will ensure that the misconduct revealed by the royal commission is not repeated and that the public’s trust is regained,” he said.

Mr Frydenberg also called on APRA to strengthen its regulating and enforcement approach and prompted the authority to act on issues relating to the prudential standards, ADI responsibilities and supervision of regulated firms.

“It is my expectation that APRA will consider seriously the findings that the royal commission has made, echoed in the Productivity Commission’s superannuation inquiry, including whether its supervisory approach is appropriate for its mandate with regard to superannuation,” he said.

The Treasurer reiterated the governments support for the body and said it would give further powers and funding to the authority as needed.

The letters come as the opposition party has accused the government of not moving fast enough to implement Commissioner Hayne’s findings.

Labor had tried to force Parliament to hold extra sitting weeks to pass legislation the dealt with the royal commission recommendations but has been unable to get the support of the crossbench.

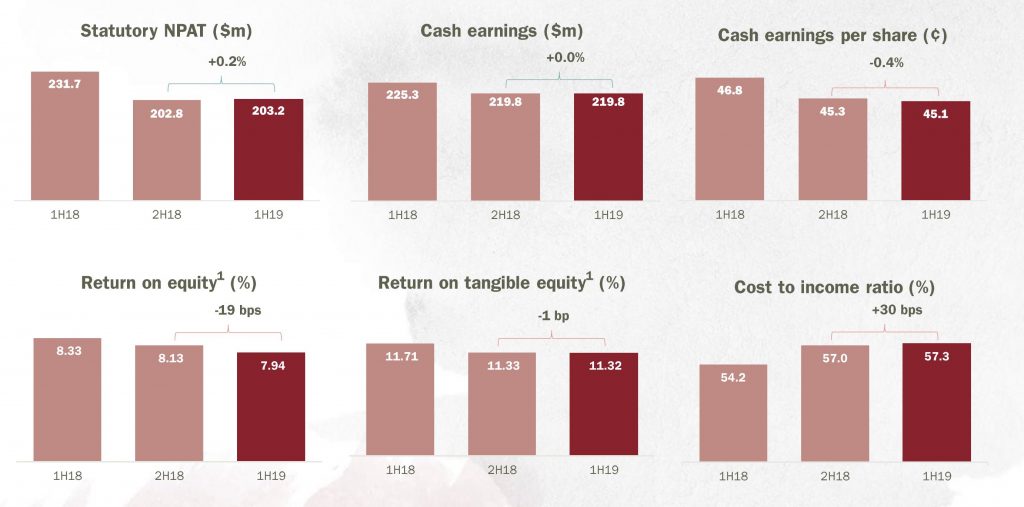

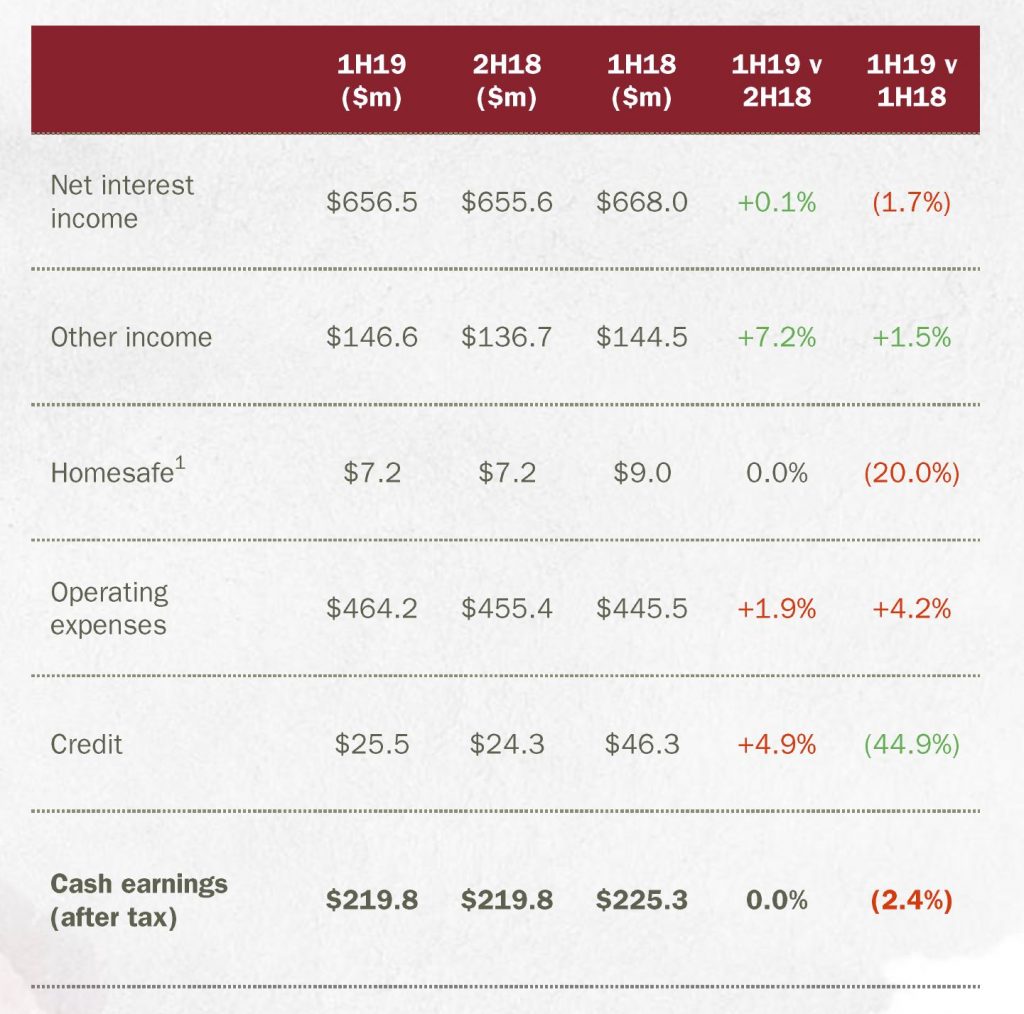

Yesterday Bendigo and Adelaide Bank released their results for the half year to December 2018. The after tax statutory profit was $203.2 million up 0.2% on the prior half, but significantly lower than the $231.7 million in 1H18. The cash earnings was flat at $219.8 million, but again lower than $225.3 million in 1H18. The earnings per share was 45.1 cents, down 0.2 cents and the fully franked dividend was 35 cents per share. The return on equity fell 19 basis point half on half.

They are positioning as “Australia’s fifth largest retail bank” and they saw a rise of 18% in new customers joining and according to research are the 9th most trusted brand in Australia. Have no doubt the franchise and “local” approach is attractive to some customers, but the question is, can the current formula work in the current tight margin, highly competitive market at a time when home loan momentum is falling. One signal is cost to income, which is rising – a reflection of the high touch model.

Mortgage book growth was 2.7%, compared with system growth of 3.3% with a portfolio of $23.1 billion. They saw more growth in investor loans than owner occupied loans.

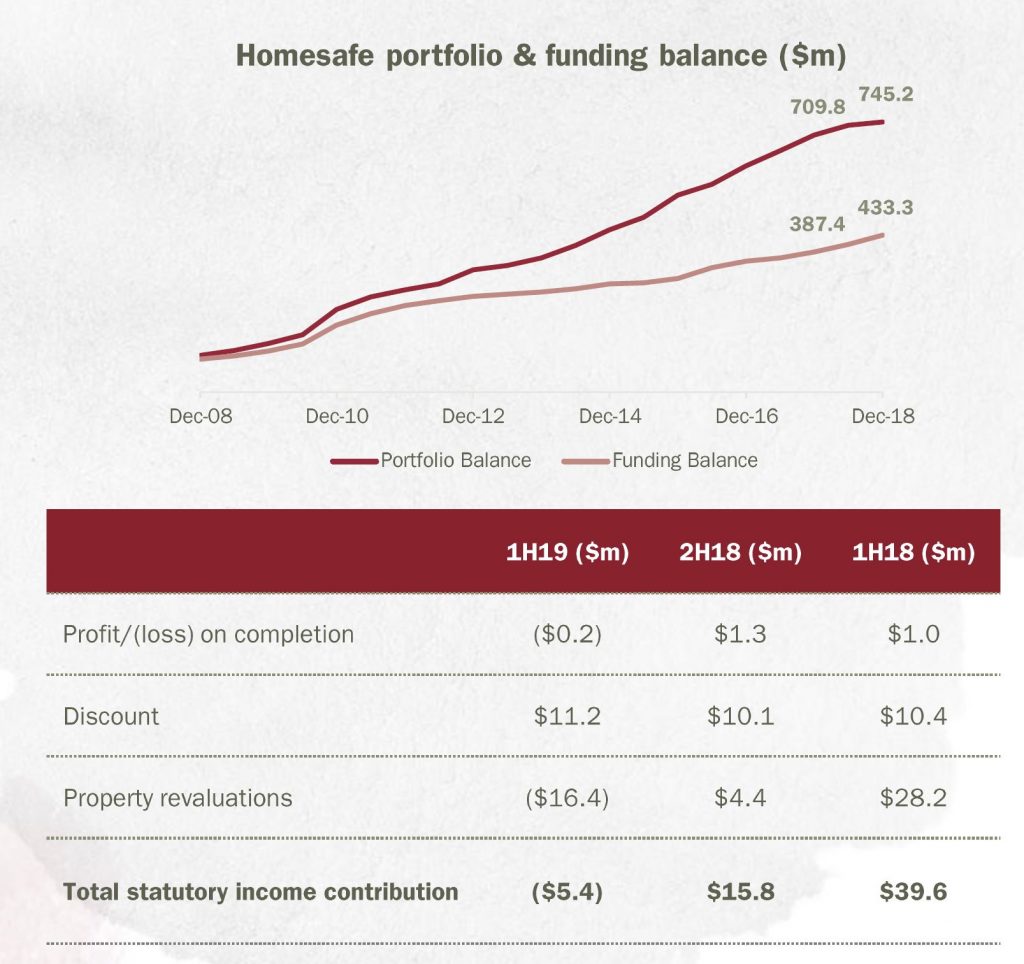

Earnings were support by other income (card activity and commissions on managed funds plus FX transactions), but net interest income was flat and Homesafe reflects changes to its accounting treatment.

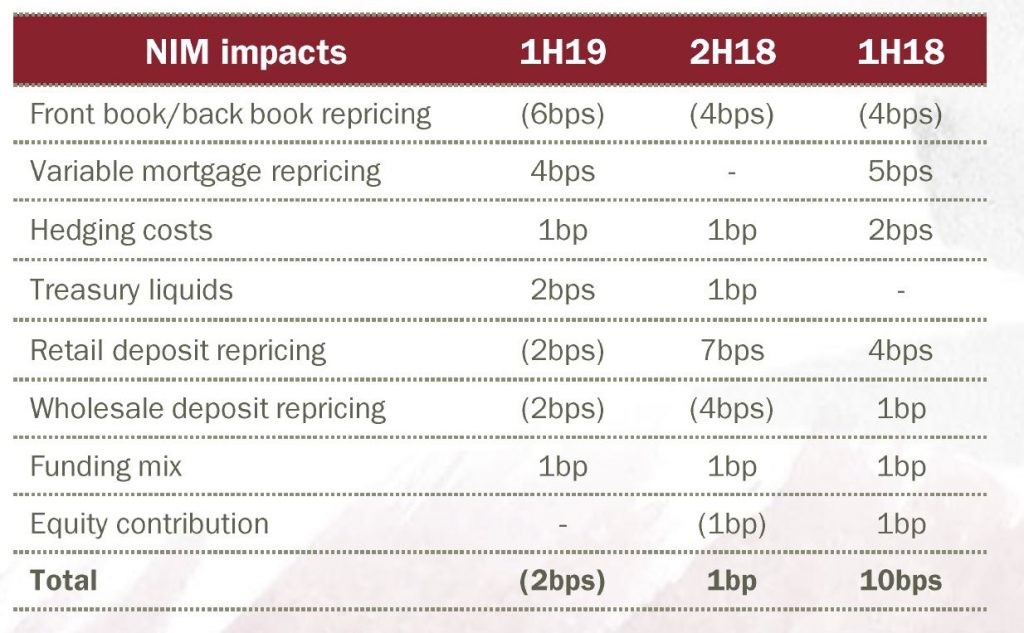

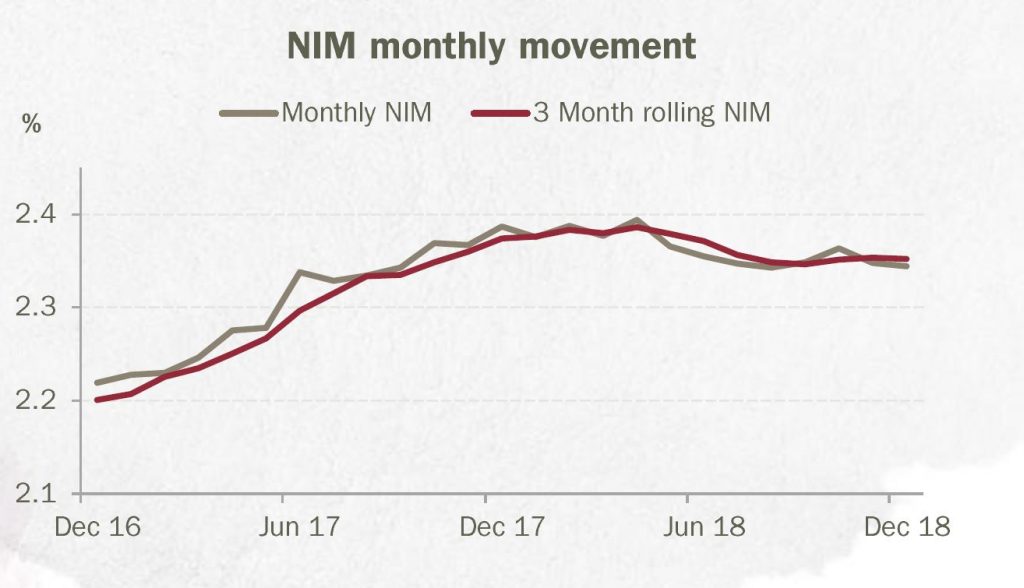

Net interest margin was down 2 basis points reflecting discounting for new loans, higher funding costs and deposit repricing.

The exit margin was 2.34% and will remain under pressure ahead.

Homesafe contribution was subject to a review of their portfolio valuation methodology, as a result they removed the overlay and revised down valuation growth rates to 0% in year 1, 3% year 2 and 4% year 3 and beyond. The result was a $1.9m change to the valuation. Essentially, they tweaked the property valuations lower (from 6% growth) but then changed the discount rate to mask the effect. A little sneaky! We said last year their home price projections were heroic… but there is still more downside risk here in our view.

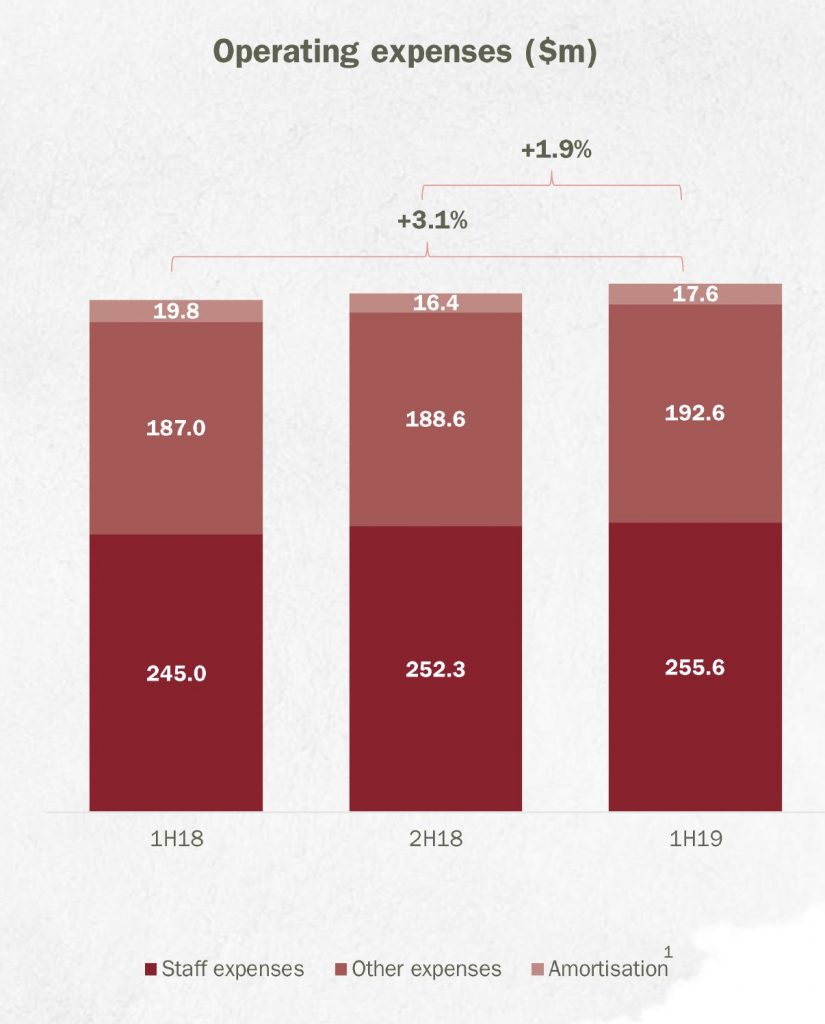

Their costs were higher, up 30 basis points to a cost income ratio of 57.3%, including higher staff costs, technology and legal and compliance.

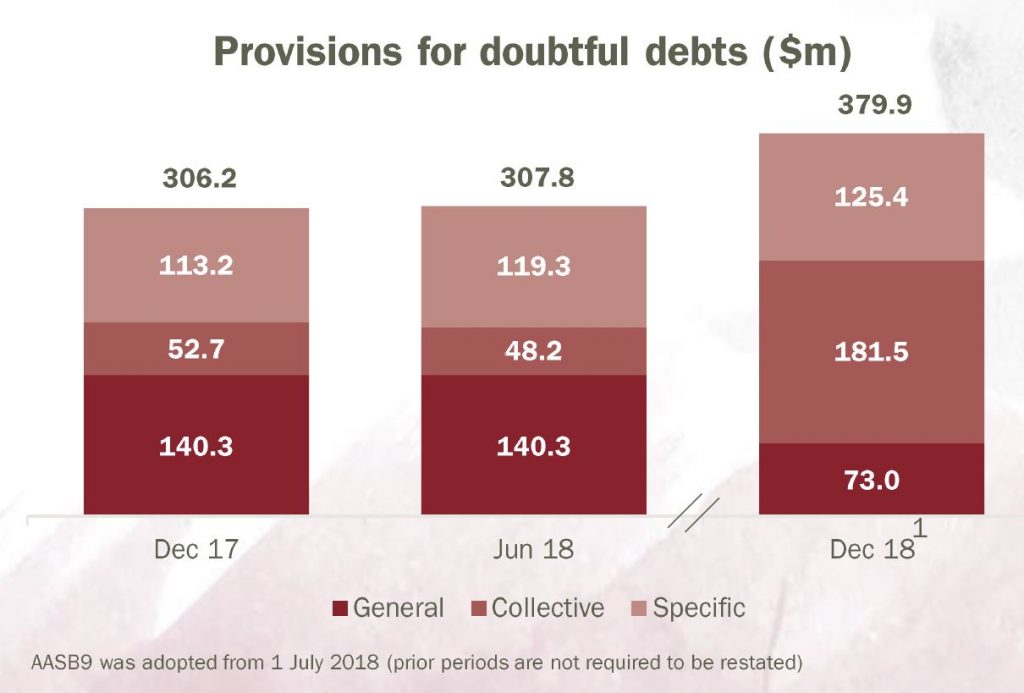

Along with the other banks, they continue to adjust their provisions to AASB9 which has lifted the collective provisions. It stands at 8 basis points, below the long term average.

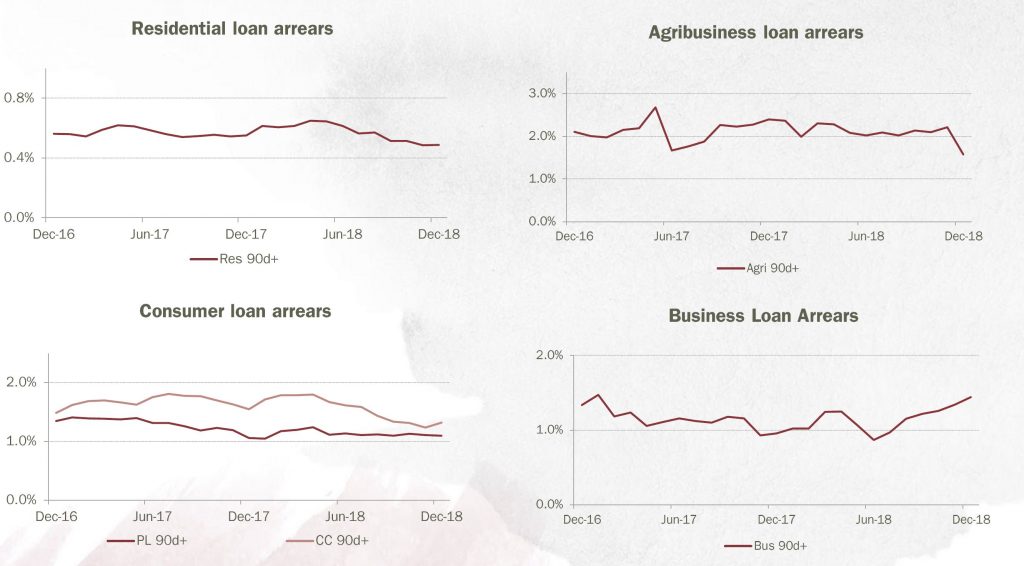

Arrears appears well contained at the moment. There was a small spike in 90 days plus credit card arrears, and business loans. Note though these figures EXCLUDE impaired loans over 90 days.

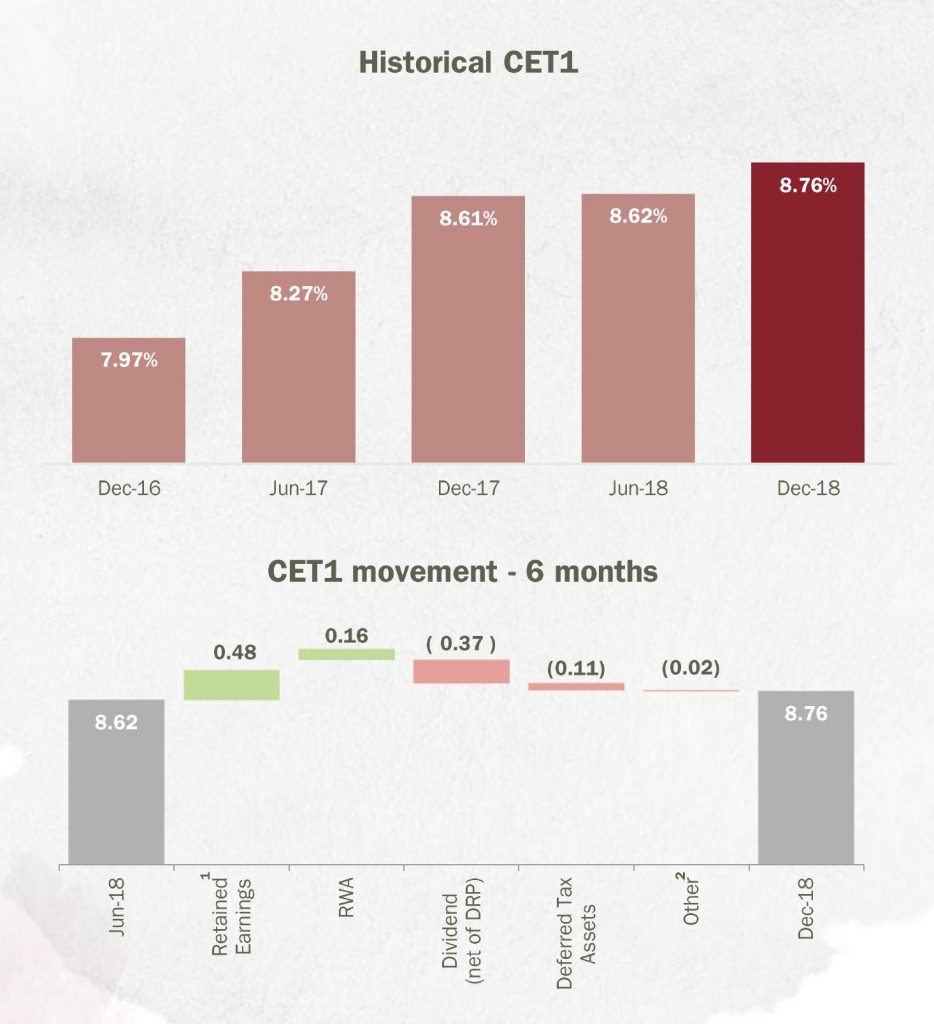

Capital position is 8.76% CET1, up 14 basis points. They are still working on advanced APRA accreditation (though the benefit looks increasing questionable in my view given APRA’s moves to lift the advanced ratios, relative to standard approaches.

Funding from deposits increased to 82.4% but they noted that higher BBSW impacted the cost of wholesale and securitisation funding.

So to conclude, we wonder about ongoing margin compression and the slowing housing sector and mortgage growth. Their cost base appears to contain significant fixed elements, which means they may have ongoing cost ratio issues. The benefit of advanced capital accreditation may be lower as APRA turns the screws. A tricky time for a player which gets the consumer, but has difficulty in competing in the current environment.

The government has announced the panel that will lead the capability review of the Australian Prudential Regulation Authority as recommended by the Hayne royal commission; via InvestorDaily.

One of Commissioner Hayne’s recommendations in his final report on the royal commission was to conduct regular capability reviews into both ASIC and APRA with a review to be undertaken immediately for APRA.

In Mr Hayne’s report he noted that ASIC had recently undergone a review while APRA had not and therefore recommended it be the first to undergo one.

“I recommend that a formal capability review be undertaken of APRA, with that review being completed as soon as is reasonably practicable after the publication of this report,” he said.

Treasurer Josh Frydenberg as part of his response to the royal commission accepted the need for regular reviews and recently announced the independent panel that would lead the APRA review.

Former chairman of the ACCC Graeme Samuel will be chairman of the review and will be joined by Diane Smith-Gander a former senior executive at Westpac and Grant Spencer a former acting governor of the Reserve Bank of New Zealand.

Mr Frydenberg said the review would look into APRA’s ability to promote financial stability, as well as its capabilities to regulate superannuation entities and its enforcement activities.

“The APRA capability review will provide a forward-looking assessment of APRA’s ability to respond to an environment of growing complexity and emerging risks for APRA’s regulated sectors,” he said.

APRA and ASIC were found by the royal commission to be too soft on misconduct and prone to negotiate settlements and part of the panel’s role will be to review the authority’s readiness to respond to issues as raised in the commission.

APRA recently appointed John Lonsdale to lead a review into the authority’s enforcement policies, stating that it would be completed by the end of March this year.

The government has yet to respond to the recommendations that the APRA-administered BEAR be extended to insurers and super funds or that the principles of the BEAR regime be applied to the regulators as well.

APRA recently released a statement saying it was committed to implementing the recommendations with a plan to implement by the end of 2020.

“There are 10 recommendations requiring APRA’s direct attention. Of the 10, it is expected that nine will be completed by the end of 2020; of those, four are expected to be completed in 2019,” a press release from APRA said.

APRA also said it is examining 12 matters in relation to individual entities that were referred by the royal commission and is working with ASIC to address those.

APRA also said it would work with Treasury, ASIC and other stakeholders to implement the extension of BEAR and strengthening of trustee duties.

The panel will commence in March 2019 to report to the government by the end of June.

Welcome to the Property Imperative weekly to the ninth of

February 2019 – our digest of the latest finance and property news with a

distinctively Australian flavour.

This was a mega week in which the Royal Commission reported, mortgage brokers were crushed, the RBA cut growth expectations, and we saw more confirmation of the pressures on households. And NAB lost both its Chairman and CEO. So let’s get started.

Read the transcript or watch the video.

The final report from the Royal Commission was disappointing, in that

whilst 20 plus companies will be referred for potential criminal proceedings,

and NAB was called out for not getting it, and the 76 recommendations may be

worthy, – we discussed the recommendations in more detail in our post “A Banking Royal

Commission Special Report” , the report failed to address two

critical issues. Hayne has left lending practices where they are (yes, the

banks have tighter standards now, at least temporarily, but he left the

household expenditure measure benchmark question hanging) and failed to address

the question of conflict between providing advice and selling financial

services products, which was at the heart of the hearings. Too often advice let

to customers buying products which maximised the income of advisors and firms, when

they were not necessarily in the best interests of said customer. See our post “Why The Royal Commission Report Is A Fail”.

Paul Keeting, the architect of financial deregulation in the 1980’s was

quoted as saying in the Australian “The royal commissioner should have

recommended — this conflict between product and advice — be prohibited. This he

monumentally failed to do. He should have acted upon the examination and the

evidence of these serious conflicts of interest.”

Finance sector stocks when higher before the report was released, and

some are suggesting insiders made $20 billion or so as a result. A leak was

denied by The Government of course, but we are not so sure. There were massive stock movements at 11:00

am on Monday, when remember the report was made public AFTER the market had

closed at four PM.

Mortgage brokers got a shock, because their business models are potentially

crushed. The Commission proposes that trail commissions – payments in

subsequent years to brokers by banks for loans they introduced – should be

banned – as quote “they are payments for no value”. And in due course brokers

need to move to a fixed fee arrangement, paid for by the borrower, which would

make the arrangement more transparent, but may restrict competition, and swing

momentum back to the big banks, who would be set to benefit. I discussed this

with mortgage broker and financial adviser Chris Bates – see “What Does The Hayne

Report Mean To Mortgage Brokers And Financial Advisers?”. They will also be given a requirement to act

in the best interest of their clients, something which is assumed by many

customers of brokers today, but which is not currently the case.

So, in summary, Hayne will be remembered more for the exposes in the

hearings, where the bad conduct and criminal behaviour of the finance sector were

revealed, rather than firm recommendations to make substantive changes. It

mostly falls back to the institutions and regulators to heal themselves. I am

less confident, so expect bad practice to continue. NAB lost their chairman and CEO, they were

both called out as not getting the problem in the bank – and it is possible

that other heads will roll as criminal proceedings commence, but I suspect most

will remain unpunished.

The RBA had a big week, with Governor Lowe speaking at the National

Press Club on Wednesday, and then releasing the Statement on Monetary Policy on

Friday. Lowe’s view is that economic growth will slow a bit compared with

previous forecasts – 3% this year and 2.75% beyond. He believes income growth

will start to lift as the unemployment rate slides further. He thinks this will

be enough to keep the economy ticking over. Despite this, there is now, he says

equal weight to both a fall in the cash rate or a rise. And in the SMOP, there was recognition that

falling home prices may have a dampening effect on consumption and growth as

the “wealth effect” dissipates. Many

suggest, this downside risk is still underplayed. Plus, the new headline inflation number for

June 2019 came it at a low 1.25% in the statement, which is a significant

reduction.

Damien Boey at Credit Suisse said “We cannot help but feel that the RBA

is missing something in all of this, hence its rather shallow downgrades to

consumption growth forecasts, and its optimistic forecast for only a 10%

reduction in residential investment this year. … If the Bank does not

understand or admit to the nature of banking and credit problems, it will

always think that the economy is healthier than it is. It will always have too

high a view of the potency of rate cuts, and therefore delay them until the

last minute”.

Westpac’s Bill Evans said of the

RBA’s move, “This move to a balanced

rate outlook is significant because it clearly establishes that the Bank is

prepared to contemplate rate cuts – a position that has really only emerged

since the housing markets have reversed. It is also consistent with changes

announced by other central banks notably the US Federal Reserve.” Of course, bond rates remain higher in the US

than here, which is unusual, and signals higher bank funding costs ahead. This was something which CBA signalled in

their results out this week. So, I am expecting more out of cycle mortgage rate

hikes ahead.

My own view has been for some time that cash rate cuts won’t have much

impact, but thanks to the budget trends, there is capacity for quite big tax

cuts to try and stimulate consumption. I expect the upcoming budget to start

that trend, and there will be more fiscal loosening later in the year as the

economy weakens.

The latest news on home prices is more of the same. Down, down, prices are down. CoreLogic’s 5-city dwelling price index slide another 0.24%. The quarterly declines are rising to 3.57% and values have fallen by 8.5% since their most recent peak, with Sydney down 12.5%, Melbourne down 9.0% and Perth down 16.7%. Remember these are averages, and in some areas, prices are down more than 20%; with more to come. And the auction results remain in the doldrums, on low volumes and clearance rates the national auction clearance rate dropped 5.0% to 42.8%. In Sydney auction clearance rate fell by 4.2% to 49.5% though in Melbourne it rose a tad to 44.3%, both well below the trends from a year ago.

And by the way CBA senior economist, Gareth Aird showed the correlation

between home prices and jobs growth, which goes counter to the RBA’s view that

jobs momentum will support prices.

Another reason why we think prices will go on sliding.

All of this is in stark contrast to the ME Bank Household Comfort report

out this week. The most shocking chart

was the high proportion of households who still think prices will rise. Only

13% of homeowners and 11% of investors expect the value of their properties to

fall this year, versus 38% of homeowners and 52% of investors that believe

property prices will rise either a “little” or a “lot”. Clearly more should be

watching our shows. But then price growth expectations, are wired in – many

have never seen falls – and the real estate sector, still are saying things are

on the turn, and she’ll be right. Sorry, to disappoint, but there are more

falls to come. And by the way that same

report said it was the renting sector who are felling more bullish as rents

slide.

The ANU, as reported in the Australian, said that the average household

has seen no gains in their after-tax income since the end of 2010, which was

when the economy was emerging from the global financial crisis. According to ANU’s

Centre for Social Research and Methods, the fall in the past three years was

greater than during the last recession in 1991-92. In fact, living standards

peaked in 2011. There was no improvement for the next four years, but incomes

started falling behind rising living costs from late 2015 onwards. Many will

not be surprised, and it helps to explain why we think household consumption

will continue to fall.

NABs surveys this week also highlighted concerns among households. They

said that anxiety increased most over the cost of living, and despite a healthy

labour market, concerns over job security also climbed to its highest level

since mid-2016.

“In terms of household finances, retirement remains the big worry,

followed by providing for the family’s future, raising $2,000 for an emergency,

and medical and healthcare costs”.

“Against this background, almost four in 10 Australians said they had

experienced some form of financial hardship last quarter, the highest in two

years.” And importantly spending plans are being curtailed, which will flow on

to lower growth of course.

And our own

mortgage stress data for January underscored the pressure on

households. The long grind in WA

continues, with more households under financial pressure, but we are seeing

further deterioration in other states too. The number of households in severe

stress continues to rise. The latest RBA data on household debt to income to

September fell a little to 188.6, but remains highly elevated. The housing debt

ratio continues to climb to a new record of 139.6, according to the RBA. This shows that household debt to income is

still increasing. This high debt level

helps to explain the fact that mortgage stress continues to rise. Across

Australia, more than 1,026,106 households are estimated to be now in mortgage

stress (last month 1,023,906), another new record. This equates to more than

31% of owner-occupied borrowing households. In addition, more than 25,750 of

these are in severe stress (last month 22,000). We estimate that more than

63,000 households risk 30-day default in the next 12 months, up 1,000 from last

month. We continue to see the impact of flat wages growth, rising living costs

and higher real mortgage rates. Bank

losses are likely to rise a little ahead. See our Video “Mortgage Stress

Exists – Believe It!”

Despite the popular view that household finances are fine, in fact the

continued accumulation of larger mortgages compared to income whilst costs are

rising, and incomes static explains the issues we are now seeing. Housing credit growth is running

significantly faster than incomes and inflation and continued rises in living

costs – notably child care, school fees and electricity prices are causing significant

pain, this despite some relief at the bowser. Many continue to dip into savings

to support their finances. We are

seeing a rise in households seeking help with their finances, including access

to debt counsellors and other advice channels. WA is seeing very strong growth

in cries for help!

Indeed, the ABC reported that the National Debt Helpline said calls had

skyrocketed in Western Australia amid epidemic of financial stress. And we note

that the Treasurer just announced a review of financial counselling: “ It

will consider gaps and overlaps in current services and the adequacy of

appropriate delivery models for future funding”. Last week John Adams and

I highlighted the

possible link between mortgage stress and family violence, as suggested by the

police.

And finally in our local round up, Business Confidence is

also tanking according to Roy Morgan Research who released their Survey for

January. They say that confidence has dropped to its lowest level since August

2015 and it was the worst January result ever. “The decline in Business

Confidence to begin 2019 comes amidst a slew of poor economic news with

significant declines in house prices in Sydney and Melbourne over the last 12

months now joined by lower than expected retail trade figures for December”. This

is consistent with the NAB results we reported last week.

So, to the markets. Locally, the ASX 100 had a good run, as the Hayne effect dissipated. The index slid a little on Friday though thanks to the RBA’s downgrades, slipping 0.3% to end at 5,006.4, territory not seen since October, and up 3.56% on a year ago. The local volatility index was down 0.29% to 12.90, and 30.48% lower than a year back, reflecting a “risk on” peak back then.

Since the FED turned turtle on its interest rate policy, the markets confidence is roaring back. Not surprisingly, the ASX Financials Index was up this week, as banks were back in favour, despite a small fall on Friday, to end at 5,911.90, still 5.71% lower than a year ago. Individual banks moved round a bit with ANZ up 0.11% on Friday to end at 26.89, down 2.79% from a year back. CBA also rose, up 0.93% on their results, which revealed strong capital but weaker margins and profit below expectation and ended at 74.75, which is 2.58% lower than a year back. NAB fell following the resignation of the CEO and Chairman, to end at 24.75. In fact, this is not the first time NAB has lost leadership after a crisis. Their shares are down 12.27% lower than a year ago, suggesting that relative to peers they have a lot to do to regain market confidence. Their quarter disclosure which came out on Friday, would have not lifted expectations, as again margin is under pressure, and capital fell. It will be interesting to see if the proposed divestments of NABs and CBA wealth businesses continue given Haynes weak recommendations. Strategy may yet be reversed. Westpac fell 0.33% on Friday to end at 26.79, and down 10.84% from a year back. They still have their wealth businesses.

Among the regionals, Bank of Queensland rose 0.09% to 10.66, but is still 10.56% down from a year ago. Suncorp fell 0.22% to 13.61, up 3.73% from last year, and Bendigo and Adelaide Bank fell 1.59% to 11.15, up 0.36%. They may be more impacted by the proposals to charge customers for mortgage advice. AMP was down 1.21% on Friday, having had a small bounce from the Royal Commission report, because it will allow them to continue to run their advice and product businesses in tandem. AMP ended at 2.44 and remains 51.49% lower than a year ago. Macquarie fell 1.23% to 121.57, but is up 19.5% from a year back, benefitting from its international businesses.

Lenders Mortgage Insurer Genworth was up 1.62% on the

latest results, which showed a strong capital position, even if mortgage

delinquencies were a little higher, especially in NSW. They ended at 2.51 and

is 10.58% lower than 12 months ago. Given lower mortgage volumes, their growth

appears limited and if household pressures continue, we must expect more

defaults ahead. Mortgage Choice, the aggregator, was hit by the Hayne

recommendations on mortgage brokers this week, but rose on Friday, up 2.44% to

84 cents, down 62.61% from a year ago. Given they have advice businesses in

their portfolio, I suspect they might do quite well from the changes, if they

can morph their business effectively.

The Aussie ended the week at 70.91, up 0.04%, having been

above 72 earlier in the week after the Hayne report came out. But the RBA’s

neutral stance on future interest rates – signalling more trouble in the

economy, dragged it back. We still expect further falls ahead. It is still

9.89% lower than a year ago.

The Aussie Gold Cross rate rose 0.49% to end at 1,853.59,

up 9.97% on a year ago, while the Aussie Bitcoin Cross rose 4.88% to 4,672.3,

down 53.42% on a year back.

Overseas, at the close, the Dow Jones Industrial Average

declined 0.25%, to 25,106.33 and is 1.11% up from a year back. The S&P 500

index gained 0.07%, to 2,707.88 and is up 0.91% from a year ago, It has risen

more than 15 percent from 20-month lows in December, spurred by a dovish

Federal Reserve and largely positive fourth-quarter earnings, as well as hopes

for an eventual U.S.-China trade deal, despite lingering scepticism over the

United States and China reaching a trade deal before the March 1 deadline. Of

the S&P 500 companies that have reported quarterly results, 71.5 percent

have beaten profit estimates but analysts now expect current-quarter profit to

dip 0.1 percent from the year before, not grow the 5.3 percent estimated at the

start of the year. The S&P 100 was down a little to end at 1.190.16, up

0.28% over the year. The CBOE Volatility Index, which measures the implied

volatility of S&P 500 options, was down 3.97% to 15.72 and is down 40.97%

form 12 months ago. The S&P Financials index was down 0.94% on Friday to

427.88 and remains 8.02% down from a year back. Bellwether Goldman Sachs fell

0.73% on Friday to 191.67 and is 24.89% lower than last year.

The NASDAQ Composite index climbed 0.14% to 7,298.20 on

Friday and is up 3.35% from last year at this time. Apple was up 0.12% to 170.41 and is 7.15%

higher than last year. Google’s Alphabet fell 0.32% to 1.102.38 and is 4.78%

than a year back. Amazon fell 1.62% to 1,588.22 but is 13.95% higher than 12

months ago and Facebook is up 0.57% to 167.33, down 7.66% from a year back.

Intel fell 0.79% to 48.84 and is up 8.52% from last year.

Investors remain jittery about trade tensions between the

U.S and China, which have been the catalyst for the global trade war that

rocked equity markets. Although the sides met for talks last week in

Washington, there have been no signs of progress. On Thursday, U.S. stock

markets fell after President Trump said that he had no plans to meet with Chinese

President Xi before March 2, when further U.S. tariffs are scheduled to be

imposed.

The Feds pussy cat approach to future rate rises has seen

the 10-year bond rate come back, and on Friday it was at 2.63, down 0.76%. The

3-month rate was at 2.42, up 0.41%. The

US Dollar index was up 0.13% to 96.64, up 7.04% from last year, while the

British Pound USD slid a little to 1.2945 and is 6.71% lower than 12 months

back.

The UK Footsie was down 0.32% to 7.071.18 as the Brexit

discussions continue, and the deadline looms. Its down 2.55% from a year back.

The Footsie Financials Index was down 0.84% to 646.19, down 3.85% from last

year. The Euro USD was at 1.1331, down 7.53% from 12 months back. The European

Commission has projected moderate growth in the EU in 2019, but economic

uncertainty has dampened confidence. The forecast lowered its growth forecast

for the eurozone to 1.9% in 2018, down from 2.1% in the November forecast. The

report highlighted Brexit and the slowdown in China as key sources of uncertainty

for European economies, adding that the projections were subject to downside

risks.

Deutsche bank was down 2.56% on Friday, to 7.223 and is 40.09% down from

this time last year. The Chinese Yuan US Dollar ended at 0.1483 and is 7.02%

lower than last year. Crude Oil Futures rose a little, up 0.11% to 52.70 but

remains 15.08% lower than last year at this time.

Gold futures were higher, up 0.32% to 1,318.35, down 2.48% from a year

ago, Silver was up 0.73% to 15.83 and is 3.04% lower than last year, while

Copper was down 0.55% to 2.81, down 8.29% from 12 months ago. And finally, the

Bitcoin USD ended the week at 3.716.9, up 8.17% but is still 54.69% lower than

a year ago. The total capitalization of the derivatives markets at BTC/USD was

$156 million US Dollars. Worth bearing in mind how small the market truly is!

So, we see the change in the wind which the Fed triggered earlier in the

month flowing on to strong markets, despite the uncertainties around global

growth ahead. Locally as the dust settles on the Hayne report, we expect bank

stocks to remain volatile – remember there are still more criminal cases in the

works – eventually. But meantime the focus will be on the Australia economy, as

the leading indicators signal more trouble ahead, and the RBA plays catch up.

In this context, there can be little expectation of a rebound in home

prices, nor a resurgence of lending for mortgages, I think the current settings

will mean falls continue, and may accelerate. The next thing to watch for are

“unnatural acts” fiscally speaking when the budget comes down in April, before

a May election. Unless something unexpected resets the timetable.

Meantime, my advice remains be very cautious about property. There is no

hurry to buy. Falling prices may offer opportunity later, but buying into a

falling market, even at these low interest rates is tricky, and as I have

indicated I expect more out of cycle hikes to come. So, caution is the watch word. But the good

news/bad news is the risk of a financial apocalypse has abated in favour of

another round of debt creation – which postpones what may well be eventually a

significant reset. We will update our

scenarios soon.

And before I go, a quick reminder that our next live stream event is now scheduled for Tuesday 19th February at 8:00 PM Sydney – here is the link to the reminder. You can ask a question live or send them in beforehand. I look forward to seeing you there.

And by the way, if you value the content we produce, please do consider supporting our efforts. You can make a one off donation via PayPal, or consider joining our Patreon programme. We really appreciate your support to help us continue to make great content.

To lose one is unfortunate, to lose two… well… Tough times for certain senior bankers!

In an ASX statement NAB said that CEO Andrew Thorburn will finish at NAB on 28 February, while Dr Ken Henry indicated that he would retire from the board once a new permanent chief executive had been appointed.

The NAB board said it will

initiate a global search process for the chief executive role while

actively considering a range of internal candidates.

In addition, it has asked

director Philip Chronican to serve as acting chief executive effective 1

March until an appointment is made.

Mr Thorburn said it has been an honour to be the chief executive of NAB, and to have been part of NAB since 2005.

“I acknowledge that the bank has

sustained damage as a result of its past practices and comments in the

royal commission’s final report about them,” Mr Thorburn said.

“I have always sought to act in the best interests of the bank and customers and I know that I have always acted with integrity.

“However, I recognise there is a

desire for change. As a result, I spoke with the board and offered to

step down as CEO, and they have accepted my offer.”

Dr Henry said the board had recognised that change was necessary.

“The timing of my departure will minimise disruption for customers, employees and shareholders,” he said.

“This is naturally a difficult

decision but I believe the board should have the opportunity to appoint a

new chair for the next period as NAB seeks to reset its culture and

ensure all decisions are made on behalf of customers.”

Mr Chronican said he was

privileged to have been asked to step in as acting chief executive while

the board selected a new chief executive.

“I recognise the important responsibility in stepping into this role at a difficult time for NAB,” he said.

“I am confident in our existing

strategy to transform the bank to be better for customers and will work

with everyone at NAB to earn the trust and respect of the community.”

The royal commission may be over but Canberra’s scrutiny of Australia’s four major banks is still underway with another round of hearings planned for March; via InvestorDaily.

The House of Representatives Standing Committee on Economics will conduct public hearings in March as part of its ongoing investigation into the banks.

The committee has already held four rounds of hearings as part of its review and has made a suite of recommendations for reform.

Some of the recommendations have been adopted by the government, like the set up of AFCA and the BEAR regime as well as increased resources for the ACCC.

The committee also recommended the establish of the open banking regime, which will come into force later this year, that will make it easier for bank start-ups to enter the sector.

The committee is led by chairman Tim Wilson who said the hearings were important in the wake of the royal commission.

“These hearings provide an important mechanism to hold the four major banks to account before the Parliament.

“These hearings will, in particular, provide an opportunity to scrutinise the banks on the findings of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry,” he said.

Mr Wilson is currently under fire from the Labor party for his position as chairman of the committee due to his franking credit investigation.

Mr Wilson has been accused by Labor MP Matt Thistlethwaite of using the hearings to lobby and recruit for the liberal party.

“It’s unethical and an improper use of taxpayer funds.

“They were handing out fliers and encouraging members of the audience at the Sunshine Coast based forum to join the national Liberal Party,” said Mr Thistlethwaite.

Mr Thistlethwaite in the past has called the inquiry an abuse of the committee process.

“Liberal MPs are using taxpayer dollars to run around the country encouraging people to do their part and undermine Labor policy,” he said.

Tim Wilson has also been accused of unethical behaviour by Labor after a leaked audio tape allegedly had fund manager Geoff Wilson of Wilson Asset Management boasting about speaking to Mr Wilson MP.

The leaked audio had Mr Wilson telling investors that it would be nice if one of the hearings was on the same day as his own upcoming franking credit roadshow where he dismissed labor policy.

“I was saying it would be nice if one of the hearings could be on a day, we are doing a roadshow. Then we could do a little protest, we could have our placards and we could walk down there.”

There was indeed a parliamentary hearing at the same time as the roadshow; however, the audio as revealed by the Sydney Morning Herald did not include any indication that this was due to any conversation between Geoff Wilson and Tim Wilson.

Further there was alleged indiscretion because of Mr Wilson’s investments in a Wilson Asset fund; however, this is listed on Mr Wilson’s register of parliamentary interests.

Mr Wilson said the work of the inquiry was for the people of Australia and was necessary in assessing the impact what a franking credit regime change could have.

“There’s a material impact on their quality of life as a result of a change of law.

“What we’ve heard across the country is people will lose 20–30 per cent of their income regardless of who they are.”

RBA Governor Philip Lowe, addressed the National Press Club today, providing an upbeat assessment of the economy. He was even money on the next rate move, but interestingly he blamed lack of supply of housing not credit supply, or low interest rates for high home prices. He believes wages will rise, eventually. And finally he down rated the international risks, such asset price bubbles, in favour of a arrange of more political risks. Mr optimistic.

And regulators are not be blamed for the poor outcomes from the finance sector, as highlighted by the Royal Commission.

The Aussie slid on the remarks.

Thank you for the opportunity to address the National Press Club. It is an honour to have been invited.

The media and the RBA have a special relationship. Most people in the community hear the RBA’s

messages through the media. You report on what we say, you filter it and you critique it. We

also help you with your work. The RBA is a reliable source of information and analysis on issues

that your audiences care about, including interest rates, housing prices and jobs. This means we

have a strong mutual interest in understanding one another. I hope that today will help

strengthen that understanding.

This is my first public speech for 2019, so I would like to talk about the year ahead and some of

the key issues that the RBA will be focusing on. I will first discuss the global economy and

then turn to the Australian economy and particularly the outlook for household spending. I will

finish with a few remarks on the outlook for monetary policy.

At the outset, I want to emphasise that we don’t have a crystal ball that allows us to see

the future with certainty. I know many of you are looking for definitive answers to questions

like, ‘Where will the cash rate be this time next year?’, ‘How

much will housing prices fall?’, ‘When will wages growth

reach 3 per cent?’. They are all good questions. The reality, though, is that

the future is uncertain. None of us can say with certainty what will happen.

What the RBA can do, though, is highlight the issues that are likely to shape the future, explain

how we are thinking about those issues, and discuss how they fit into our decision-making

framework. That is what I hope to do today.

The Global Economy

I will start with the global economy, because what happens overseas has a major bearing on what

happens in Australia. My main point here is that while some of the downside risks have

increased, the central scenario for the world economy still looks to be supportive of growth in

Australia.

It is worth recalling that 2018 was a good year for the world economy. Growth in the advanced

economies was above trend in the first half of the year, unemployment rates reached their lowest

levels in many decades, inflation was low and financial systems were stable (Graph 1).

These are positive outcomes. We should not lose sight of this.

Graph 1

There was, though, a change in momentum in the global economy late in the year. This change was

particularly evident in Europe and it was also evident in China. It has been widely reported in

the media, but it is important to keep things in perspective.

Some slowing in global growth was expected, given that labour markets are fairly tight and the

policy tightening in the United States was aimed at achieving a more sustainable growth rate.

So, I have been a little surprised at some of the reaction to the lowering of forecasts for

global growth, which has been quite negative. We need to remember that the IMF’s central

forecast is still for the global economy to expand by 3.5 per cent in 2019 and by 3.6 per cent

in 2020 (Graph 2). If achieved, these would be reasonable outcomes and not too different

from the recent past.

Graph 2

What is of more concern, though, is the accumulation of downside risks. Many of these risks are

related to political developments: the trade tensions between the United States and China; the

Brexit issue; the rise of populism globally; and the reduced support from the United States for

the liberal order that has supported the international system and contributed to a broad-based

rise in living standards. One could add to this list the adjustments in China as the authorities

rein in shadow financing.

The origins of these diverse issues are complex, but there is a common economic element to some

of them: that is, the extended period of little or no growth in real incomes for many people. In

a number of countries, growth in real wages has been weak or negative for years. Advances in

technology and greater competition as a result of globalisation also mean that many people worry

about their own future and that of their children. Politicians, understandably, are responding

to these concerns. Time will tell, though, whether the various responses help or not. I suspect

that some of them will not.

Over recent months, the accumulation of downside risks has been evident in business and consumer

surveys. It was also evident in increased volatility in financial markets around the turn of the

year, with declines in equity prices and an increase in credit spreads (Graph 3). Since

then, though, markets have been more settled and some of the earlier decline in equity prices

has been reversed. This has been partly on the back of a reassessment of the path of monetary

policy in the United States, with markets no longer pricing in further increases in US interest

rates. There has also been a noticeable fall in long-term government bond yields.

Graph 3

The adjustments in financial markets over our summer sometimes generated reporting that, to me,

seemed overly excitable. I lost count of how many times I read the words ‘crash’,

‘plunge’ and ‘dive’. Yet there is a positive side to some of these

adjustments, which gets less reported on. The risks associated with stretched valuations in some

equity markets have lessened. So, too, have concerns that very low credit spreads could lead to

an excessive build-up of risk. And risks in many emerging market economies have also receded,

helped by the lower global interest rates and lower oil prices. So it is important to look at

the whole picture.

For Australia, what happens in China is especially important. Growth there has slowed. From a

medium-term perspective, this has a positive side, as it mainly reflects efforts to rein in

risky financial practices and stabilise debt levels. But the slowing is probably faster than the

government had hoped for, with the economy feeling the effects of the trade dispute with the

United States and the squeezing of finance to the private sector. The authorities have responded

by easing policy in some areas, but they are walking a fine line between supporting the economy

and addressing the debt problem. There is also the question of how the economy responds to the

policy easing.

More broadly, we cannot insulate ourselves completely from the global risks, but keeping our

house in order can go a long way to assist. Our floating exchange rate and the flexibility we

have on both monetary and fiscal policies provide us with a degree of insulation. So, too, does

our flexible labour market. Ensuring that we have predictable and consistent economic policies,

credible public institutions and a reform agenda that supports a strong economy can also help in

an uncertain world.

The Domestic Outlook

I would now like to turn to the outlook for the Australian economy. Much as is the case globally,

the downside risks have increased, although we still expect the Australian economy to grow at a

reasonable pace over the next couple of years.

The Australian economy is benefiting from strong growth in infrastructure investment and an

upswing in other areas of investment. The labour market is also strong, with many people finding

jobs. This year, we will also benefit from a further boost to liquefied natural gas (LNG)

exports. The lower exchange rate and a lift in some commodity prices are also assisting. Against

this generally positive picture, the major domestic uncertainty is the strength of consumption

and the housing market.

We will be releasing a full updated set of forecasts in the Statement on Monetary

Policy (SMP) on Friday. Close readers of the SMP will notice that we will now be

publishing forecasts for a wider set of variables than has previously been the case.[1] We hope that

this helps people understand the various forces shaping the economy.

Today, I can give you a summary of the key numbers.

Our central forecast is for the Australian economy to expand by around 3 per cent over

2019 and 2¾ per cent over 2020 (Graph 4). For 2018, the outcome is expected

to be a bit below 3 per cent. This type of growth should be sufficient to see further

gradual progress in lowering unemployment.

Graph 4

These forecasts are lower than the ones we published three months ago. For 2018, the outcome is

affected by the surprisingly soft GDP number in the September quarter and the ABS’s downward

revisions to estimates of growth earlier in the year. We are expecting a stronger GDP outcome in

the December quarter, with other indicators of economic activity painting a stronger picture

than suggested by the September quarter national accounts.

For 2019 and 2020, the forecasts have been revised down by around ¼ percentage point,

largely reflecting a modest downgrading of the outlook for household consumption and residential

construction. I will talk more about this in a moment.

The outlook for the labour market remains positive. The national unemployment rate currently

stands at 5 per cent, the lowest in over seven years (Graph 5). In New South

Wales and Victoria, the unemployment rate is around 4¼ per cent. You have to go

back to the early 1970s to see sustained lower rates of unemployment in these two states. The

forward-looking indicators of the labour market also remain positive. The number of job

vacancies is at a record high and firms’ hiring intentions remain strong. Our central

scenario is that growth will be sufficient to see a modest further decline in unemployment to

around 4¾ per cent over the next couple of years.

Graph 5

The other important element of the labour market is how fast wages are increasing. For some time,

we have been expecting wages growth to pick up, but to do so gradually. The latest data are

consistent with this, with a turning point now evident in the wage price index (Graph 6).

Through our discussions with business we are also hearing more reports of firms finding it

difficult to find workers with the necessary skills. In time, this should lead to larger wage

rises. This would be a positive development.

Graph 6

Given this outlook, we continue to expect a gradual pick-up in underlying inflation as spare

capacity in the economy diminishes (Graph 7). However, the lower forecast for growth means

that this pick-up is expected to occur a bit later than we’d previously thought. Underlying

inflation is now expected to increase to about 2 per cent later this year and to reach

2¼ per cent by the end of 2020. The latest CPI data were consistent with this

outlook. The headline CPI number was, however, a bit lower than we had previously expected,

reflecting the decline in petrol prices that started late last year. We expect headline

inflation to decline further this year as the full effect of lower petrol prices shows up in the

figures.

Graph 7

So that is the summary of the key numbers.

As always, there is a range of uncertainties, many of which will be discussed in the SMP on

Friday. Today, though, I would like to focus on the outlook for household spending, which is

closely linked to the housing market and the prospects for growth in household income.

Before I do that, I would like to touch on one related uncertainty that we have been paying

attention to – that is the supply of credit. This is because a strong economy requires

access to finance on reasonable terms. Over recent years there has been a needed tightening of

credit standards. But the right balance needs to be struck. As lenders have sought to find that

balance, we have had some concerns that the pendulum may have swung too far the other way,

especially for small business.

In that context, I welcome the report of the Royal Commission and the Government’s response.

The Commission’s recommendations that bear on credit provision are balanced and sensible,

and should remove some uncertainty. I also welcome the Commission’s focus on: the importance

of service – as opposed to sales – in the financial sector; the necessity of dealing

properly with conflict of interest issues; and the importance of accountability when things go

wrong. These are all issues I have spoken about on previous occasions. Addressing them is

central to rebuilding the all-important trust in our financial system.

Housing Prices and Household Income

But back to household consumption and the housing market.

You might recall that 18 months ago, one of the most talked about issues in the country was the

high and rising cost of housing. This was understandable. In some of our cities, purchasing a

home had become a very difficult stretch for many people, and this had become a major social

issue.

Today, the talk is about prices falling in our two largest cities. We have moved almost

seamlessly from worrying that prices were going up, to worrying that they are going down.

There is no single reason for this change, but, rather, it is the result of a number of factors

coming together.

One is that housing prices simply increased to the point in Sydney and Melbourne where demand

tailed off, as purchasing a home had become very expensive and less attractive as an investment.

A second is that the building boom over recent times significantly increased the supply of

dwellings. It took a number of years before the rate of home construction picked up in response

to faster population growth, but eventually it did pick up. This explains much of the cycle.

A third factor is that the demand from overseas investors softened, partly in response to the

Chinese authorities making it more difficult to move money out of China.

And a fourth factor is that lending standards have been tightened and credit has become more

difficult to obtain.

Importantly, unlike most other housing price corrections, this one has not been associated with

rising unemployment or higher interest rates. Instead, mainly structural factors –

relating to the underlying balance of supply and demand – in our largest cities have been

at work.

The question is: what effect will this change have on household spending?

Here, my earlier observation about not having a crystal ball is relevant. At this point, though,

what we are seeing looks to be a manageable adjustment in the housing market. It is not expected

to derail economic growth. The previous trends in debt and housing prices were becoming

unsustainable and some correction was appropriate. We recognise that this correction will have

an effect on parts of the economy. But our economy should be able to handle this, and it will

put the housing market on a more sustainable footing.

There are a few considerations here.

The first is that the recent housing price declines follow very large increases in prices (Graph 8).

Even after the recent declines in Sydney, prices are still 75 per cent higher over the

decade. In Melbourne, they are 70 per cent higher. While the price falls are no doubt

difficult for some, including people who purchased in the past couple of years, there are many

people sitting on very significant capital gains and there are others who now will find it

easier to purchase a home. And of course, in a number of cities and much of regional Australia,

things have been more stable.

Graph 8

A second consideration is that most households do not change their consumption in response to

short-term changes in their wealth. Sensibly, many people tend to take a longer-term

perspective. During the recent upswing in housing prices, the strategy of borrowing against the

extra equity in your home looked less sensible than it once was, especially as debt levels rose.

Some home-owners also see themselves as being part of the ‘bank of mum and dad’.

This meant that they refrained from spending the extra equity so that they were able to help

their children purchase their own property.

A third and perhaps the most important consideration, is that household income growth is expected

to pick up and income growth usually matters more for consumption than changes in wealth.

For some years, growth in nominal aggregate household income has been unusually slow, averaging

just 2¾ per cent since 2016 (Graph 9). For some home-owners, rising housing

prices have provided an offset to this, even though the effect may have been smaller than in the

past. As a result, aggregate consumption has grown faster than income for the past few years.

But a shift is now taking place. Over the next year, we are expecting a pick-up in household

disposable income to provide a counterweight to the wealth effects of lower housing prices.

Graph 9

Labour market outcomes are key to this assessment. Continued employment growth and higher wages

growth should boost disposable incomes. The announced tax cuts should also help here. In our

central scenario, consumption is expected to grow at around 2¾ per cent over the

next couple of years, broadly in line with expected growth in disposable income. This is a bit

lower than our earlier forecast for consumption.

There are, of course, other possible outcomes. Continued low income growth, together with falling

housing prices, would be an unwelcome combination and would make for a softer outlook for the

economy. Some Australian households have high levels of debt, so there is a degree of

uncertainty about how they would respond to this combination. So we are monitoring things

closely.

The adjustment in the housing market is also affecting the economy through residential

construction activity and the spending that occurs when people move homes. Residential

construction activity is currently around its peak level and the large pipeline of approved

projects is expected to support activity for a while. Developers, though, are finding it more

difficult to sell apartments off the plan, and lenders are less willing to provide finance.

Sales of new detached dwellings have also slowed. The central forecast is for dwelling

investment to decline by about 10 per cent over the next two and a half years.

Putting all this together, our economy is going through an adjustment following the turn in the

housing markets in our largest cities. It is important that we keep this in perspective though.

The correction in the housing market follows an extended period of strength. It is largely due to

structural supply and demand factors, and is occurring against the backdrop of a robust economy

and an expected pick-up in income growth. Our financial institutions are also in a strong

position to deal with the adjustment. Indeed, lending standards were strengthened as the upswing

went on. From this perspective, the adjustment in the housing market is manageable for the

financial system and the economy. This adjustment will also help increase the affordability of

housing for many people. Even so, given the uncertainties, we are paying very close attention to

how things evolve.

Monetary Policy

This brings me to monetary policy.

The cash rate has been held steady at 1½ per cent since August 2016. This setting

has helped support the economy. The Reserve Bank Board has sought to be a source of stability

and confidence while our economy adjusted to the end of the mining investment boom and responded

to the shifting sands of the global economy.

Over the past couple of years, economic conditions have been moving in the right direction. The

labour market has strengthened, and the unemployment rate has fallen and a further decline is

expected. Inflation is also above its earlier trough, although it has not changed much over the

past year. Our expectation has been – and continues to be – that the tighter labour

market and reduced spare capacity will see underlying inflation rise further towards the

midpoint of the target range. Given this, we have maintained a steady setting of monetary policy

while the labour market strengthens and inflation increases.

Looking forward, there are scenarios where the next move in the cash rate is up and other

scenarios where it is down. Over the past year, the next-move-is-up scenarios were more likely

than the next-move-is-down scenarios. Today, the probabilities appear to be more evenly

balanced.

We will be monitoring developments in the labour market closely. If Australians are finding jobs

and their wages are rising more quickly, it is reasonable to expect that inflation will rise and

that it will be appropriate to lift the cash rate at some point. On the other hand, given the

uncertainties, it is possible that the economy is softer than we expect, and that income and

consumption growth disappoint. In the event of a sustained increased in the unemployment rate

and a lack of further progress towards the inflation objective, lower interest rates might be

appropriate at some point. We have the flexibility to do this if needed.

The Board will continue to assess the outlook carefully. It does not see a strong case for a

near-term change in the cash rate. We are in the position of being able to maintain the current

policy setting while we assess the shifts in the global economy and the strength of household

spending.

It has long been the Board’s approach to avoid reacting to the high-frequency ebb and flow of

news. Instead, we have sought to keep our eye on the medium term and put in place a setting of

monetary policy that helps deliver on our objectives of full employment, an inflation rate that

averages between 2 and 3 per cent, and financial stability.

Thank you for listening. I look forward to answering your questions.

Ever since financial deregulation in the 1980s we’ve had a finance industry scandal followed by an inquiry, a quick fix, and a declaration that it shouldn’t happen again.

In the early 1990s there were royal commissions into the A$1.7 billion Tri-continental/ State Bank Victoria collapse, the A$3.1 billion State Bank of South Australia collapse and the WA Inc

collapse which explored the interrelated activities at Rothwells bank,

the A$1.8 billion collapse of Bond Corporation and the A$1.2 billion

siphoned from Bell Resources.

And now, bang on schedule, we have Kenneth Hayne delivering the final report

of a royal commission into systemic misconduct in banking,

superannuation and financial services industry to a government that

voted 26 times against holding it.

There are two particularly striking things about the 10-15 year cycle.

One is the rhythm of public inquiries followed by reports, then

(sometimes) trials, then books, then almost everyone forgetting (except

for those personally scarred) only for problems to resurface later.

The other is that the times between have been punctuated by

government-commissioned banking and financial system reviews: the 1991 Campbell Inauiry, the 1996 Wallis Inquiry, the 2010 Cooper superannuation review and the 2012 Murray Review .

Each either missed or downplayed the links between poor governance,

industry structure, systemic misconduct and prudential risk.

Has Kenneth got the frequency right this time?

Commissioner Kenneth Hayne’s 1000-page final report hasn’t gone far enough to end this cycle.

While his referral of 24 misdeeds for possible criminal and civil

prosecution will help in righting past wrongs and perhaps focus the

minds of directors and executives, the impact will be generational

rather than permanent.

The flurry of prosecutions and actions will again reveal problems with the law – gaps in coverage, inadequate penalties and cases the law won’t allow to stand up.

Taken together the recommendations are a patchwork of measures that

if implemented will over time be eaten away – and at some point will be

dismantled – because the rationale for their adoption will be forgotten.

Even before they are implemented they will have to run the gauntlet

of a massive subterranean lobbying effort from industry to water them

down, something Hayne indicated he expected.

The deepest flaw lies unaddressed…

Even though Hayne emphasises the link between systemic misconduct,

governance, structure and prudential (system-wide) risk, something that

Treasury, the RBA and Australia’s three business regulator amigos, APRA,

ASIC and the ACCC, have long rejected, he makes no concrete suggestions to tackle it.

As we have written previously, research tells us big systemically

important shareholder-focused universal for-profit banks that cross-sell

products are more profitable than smaller banks in the good times but

are more prone to misconduct and to failure in the worse times.

Australia’s big four fit the bill – they’re big, they have been

vertically integrated one-stop shops, they are very, very profitable and

they are very focused on shareholder returns.

While the banks, apart from Westpac, have divested themselves of

wealth management and insurance arms for now there is nothing stopping

them reacquiring them in the future.

This means we are once again 10 or 15 years away from systemic

misconduct resurfacing as big banks seek to become more profitable.

…and putting the onus on directors won’t much help

While heads might roll in yet another round of internal investigations to fix bank culture, it is wise to remember that as Adele Ferguson observed ANZ’s internal investigation of the Opes Prime collapse left the bigger governance lessons “unlearned”.

Directors and senior executives of failed companies continue to live charmed lives.

The directors of Babcock and Brown were cheered as they left the building, while friends and family of the disgraced One.Tel director Jodee Rich have resurfaced at Hayne and other public inquiries.

Some of the One.Tel directors have had long corporate careers. The former chair at of the collapsed Allco Finance Group Bob Mansfield went on to review the ABC.

Without them we could very easily have another crisis and another royal commission in 15 to 15 years time.

Ireland has taken a been prepared to change corporate structures.

After the meltdown of its financial system triggered by the end of a

“classic vanilla property boom” its parliament legislated to appoint public interest directors to the boards of its failed banks.

These changes were designed to ensure banks directors put the public

interest first, ahead of shareholders interests and even customers

interests.

It’s beyond time we did it here.

Authors: Andrew Linden, Sessional Lecturer, PhD (Management) Candidate, School of Management, RMIT University; Warren Staples,