ASIC says an ongoing investigation has resulted in the permanent banning of former National Australia Bank (NAB) branch manager Mathew Alwan from engaging in credit activities and providing financial services.

The ban is the result of an extensive ASIC investigation in respect of NAB employees in greater western Sydney who were accepting false documents in support of loan applications and falsely attributing loans as having been referred by NAB introducers in order to obtain commissions. This conduct was the subject of the first case study before the Financial Services Royal Commission.

From 2012 to 2015, Mr Alwan assigned 101 home loans as being referred to NAB by an introducer, causing a total of $186,725 to be paid to the introducer by way of commission. ASIC found in 25 of these loan applications, Mr Alwan had knowingly given NAB false or misleading information and documentation.

The introducer in question is Mr Alwan’s relative, a fact he did not disclose to NAB and actively concealed from the bank when questioned.

ASIC found that Mr Alwan’s conduct was dishonest, deliberate and repeated.

ASIC also found Mr Alwan personally lent money to a NAB staff member who reported to him and to a NAB customer while loan applications by each of them were pending approval, creating an unacceptable conflict of interest.

Mr Alwan has the right to lodge an application for review of ASIC’s decisions with the Administrative Appeals Tribunal.

ASIC’s ongoing investigation is considering whether a brief for criminal charges should be referred to the CDPP.

Background

On 16 November 2017, NAB announced a remediation program for home loan customers whose loans may not have been established in accordance with NAB’s policies.

NAB has identified that around 2,300 home loans since 2013 may have been submitted with inaccurate customer information and/or documentation, or incorrect information in relation to NAB’s Introducer Program.

Mr Alwan’s banning follows the permanent banning of former NAB employees Danny Merheb and Samar Merjan (also known as Samar Awad) from engaging in credit activities and providing financial services (refer: 18-205MR), and the seven year banning of former NAB branch manager Rabih Awad (refer: 18-211MR)

Industry participants are being to react to the Royal Commission report, of course arguing from their own corner. Here is the latest.

The Mortgage & Finance Association of Australia (MFAA) has released a full response after the interim report of the Royal Commission, saying there is no evidence of systemic misconduct and outlining responses to each issue raised in the original report; via Australian Broker.

The document from the picks up on concerns over commissions and the fact the report said loans written through mortgage brokers have higher leverage, more interest-only loans, higher debt-to-income and loan-to-value ratios, higher interest costs and an increased likelihood that borrowers will fall into arrears.

The association responded to this claim saying that the complexity of borrower situations was not considered, as it was often that “risky loans” gravitated to the broker channel. Customers in difficult financial situations can benefit from using a broker to obtain finance.

It was strong on its stance over broker commissions, saying, “If conflicted remuneration was causing systemic harm to consumers, then the data should show complaints and relative arrears high and rising, competition and consumer support shrinking and prices inevitably rising. But this is not the case.”

The MFAA also said that as the report had not discussed the benefit of competition or consumer choice, the questions it had reported did not take into account wider unintended consequences.

It also accused the interim report of being silent on many of the changes industry groups are already adopting, not taking into account these changes when forming its questions and considerations.

It added, “The MFAA believes the issues raised around remuneration can be effectively dealt with by the specific reforms being proposed by the Combined Industry Forum (CIF), a stronger customer duty and a governance framework with an enforceable industry code focused on conduct and culture.”

It also said, “A consumer fee-for-service model would harm customers (especially in rural and regional Australia), damage competition and threaten viability of broker small businesses. It would significantly benefit the major lenders, providing them with an unassailable stranglehold on the home lending market and interest rates.

“A consumer fee-for-service is not a viable solution to improve transparency around broker commissions and help consumers to make more informed choices.

“It would tip the balance back in favour of branch-based lending by making it significantly more expensive for a customer to use a broker rather than a bank branch to obtain a home loan.

“Smaller lenders that do not have branch networks would be pushed out of the market, stifling competition, and allowing major lenders to restore the massive net interest margins they imposed on mortgage products before broking made access to competitive credit services a reality.”

In its conclusion, the MFAA said it would be calling on policy makers to consider all consequences of any changes to regulation.

It added, “We will also be promoting the fact that there is no evidence of systemic misconduct, and that our industry is focused on making the changes required to continue to improve customer outcomes.

“We know we must ensure that the strong consumer trust and confidence in the broker channel is underpinned by governance and transparency for the long-term sustainability of our industry, and ultimately, in the service of competition in the mortgage lending market.”

Robbie Barwick from the CEC and I discuss a broad range of issues centered on fixing the banking system, and the Australian economy more broadly in the light of the Royal Commission interim report.

You may not agree with Robbie’s 5 point plan, but this is a thought provoking episode which will challenge a few assumptions along the way.

The use of the Household Expenditure Measure as a benchmark for borrowers’ living expenses has been called into question by the royal commission, which has suggested that more verification needs to be undertaken, via The Adviser.

The interim report from the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, which totals more than 1,000 pages over three volumes, has raised a number of “policy-related issues” arising from the first four rounds of public hearings, which covered consumer lending, financial advice, SME loans and the experiences of regional and remote communities with financial services entities.

As well as scrutinising broker commissions and banker incentives, Commissioner Kenneth Hayne looked at how lenders and brokers utilise the Household Expenditure Measure (HEM) when fulfilling their responsible lending obligations — an issue that arose during the first round of hearings and has recently been a source of debate in the broking industry.

In the interim report, Commissioner Hayne noted that the National Consumer Credit Protection Act 2009 (NCCP Act) requires credit licensees to assess whether the credit contract would be “unsuitable” for the consumer if the loan contract is made or (in the case of a credit limit increase) the limit is increased.

He highlighted that steps to ascertain whether the loan is unsuitable include “making reasonable inquiries” about the consumer’s requirements and objectives in relation to the credit contract, knowing the consumer’s financial situation and taking “reasonable steps” to verify the consumer’s financial situation.

However, Commissioner Hayne argued that the case studies from the first round of hearings suggested that “credit licensees too often have focused, and too often continue to focus, only on ‘serviceability’ rather than making the inquiries and verification required by law”.

He wrote in the interim report: “More particularly, identifying that the consumer’s income is larger than a general statistical benchmark for expenditures by consumers whose domestic circumstances are generally similar to those of the person seeking the loan does not reveal the particular consumer’s financial situation.

“All it does is convey information to the credit licensee that it may judge sufficient for it to decide that the risk of the consumer failing to service the loan is acceptable.

“Verification calls for more than taking the consumer at his or her word.”

Commissioner Hayne asked in the interim report: “If the consumer claims to have regular income, what step has the credit licensee taken to verify the claim?”

Lenders “more often than not” failed to verify outgoings

Noting that “verification is often not difficult” and can been made via bank statements, Commissioner Hayne added that although “the evidence showed that, more often than not, each of ANZ, CBA, NAB and Westpac took some steps to verify the income of an applicant for a home loan”, it also showed that “much more often than not, none of them took any step to verify the applicant’s outgoings”.

His interim report was critical of the industry’s reliance on HEM, with the report outlining: “The general tenor of the evidence was that a lender satisfied responsible lending obligations to verify a borrower’s financial position if the lender assessed the suitability of the loan by reference to the higher of a borrower’s declared household expenses and the Household Expenditure Measure (HEM) published by The Melbourne Institute (or some equivalent measure) and that verifying outgoings was ‘too hard’.

“But what was meant by verifying outgoings being ‘too hard’ was that the benefit to the bank of doing this work was not worth the bank’s cost of doing it.”

Commissioner Hayne highlighted the ANZ case study in which a borrower supplied ANZ a copy of his bank statement (from another lender) as verification of his income, but that the “outgoings recorded in that statement were obviously inconsistent with what the borrower recorded as his outgoings”.

He said: “ANZ’s procedures did not require consideration of, and in fact the relevant bank employees did not look at, the bank statement for any purpose other than verifying income.”

The commissioner noted that ANZ did not think that there was a “material uplift” in reviewing customer bank statements for general account conduct to identify whether there were “any obvious inconsistencies between a customer’s stated expenses and transaction history, or any general indicators of financial stress”.

He pointedly remarked that the bank “did not make reference to whether or not the responsible lending requirements suggested or required otherwise”.

Further, the interim report outlined that although Westpac (which recently paid a $35 million penalty for failing to verify expenses) has expanded its expenses categories this year, “in most cases, Westpac does not require customers to provide regular transaction statements for non-Westpac accounts, and the ‘verification’, as distinct from the ‘inquiry’, of the customer’s expenses remains largely with the customer”.

As well as the lack of income verification being undertaken, the interim report suggested that relying on the HEM benchmark was not always appropriate as it was only a “modest expenditure” calculation and “takes no account of whether a particular borrower has unusual household expenditures, as may well be the case, for example, if a member of the household has special needs or an aged parent lives with, or is otherwise cared for, by the family”.

Commissioner Hayne’s report concluded: “It follows that using HEM as the default measure of household expenditure does not constitute any verification of a borrower’s expenditure. On the contrary, much more often than not, it will mask the fact that no sufficient inquiry has been made about the borrower’s financial position. And that will be the case much more often than not because three out of four households spend more on discretionary basics than is allowed in HEM and there will be some households that spend some amounts on ‘non-basics’.”

He added: “Using HEM as the default measure of household expenditure assumes, often wrongly, that the household does not spend more on discretionary basics than allowed in HEM and does not spend anything on ‘non-basics’.”

As such, Commissioner Hayne asked: “Should the HEM continue to be used as a benchmark for borrowers’ living expenses?”

He also questioned whether the “processes used by lenders, at the time of the hearings, to verify borrowers’ expenses meet the requirements of the NCCP Act”.

The interim report has also asked members of the public to outline what steps, consistent with responsible lending obligations, a lender should take to verify a borrower’s expenses.

Submissions in response to the interim report can be made on the royal commission website and must be received no later than 5pm on 26 October 2018.

The commission will release a final report, which will include the topics of the fifth, sixth and seventh rounds of hearings (focusing on superannuation, insurance and “policy questions arising from the first six rounds”, respectively) by 1 February 2019.

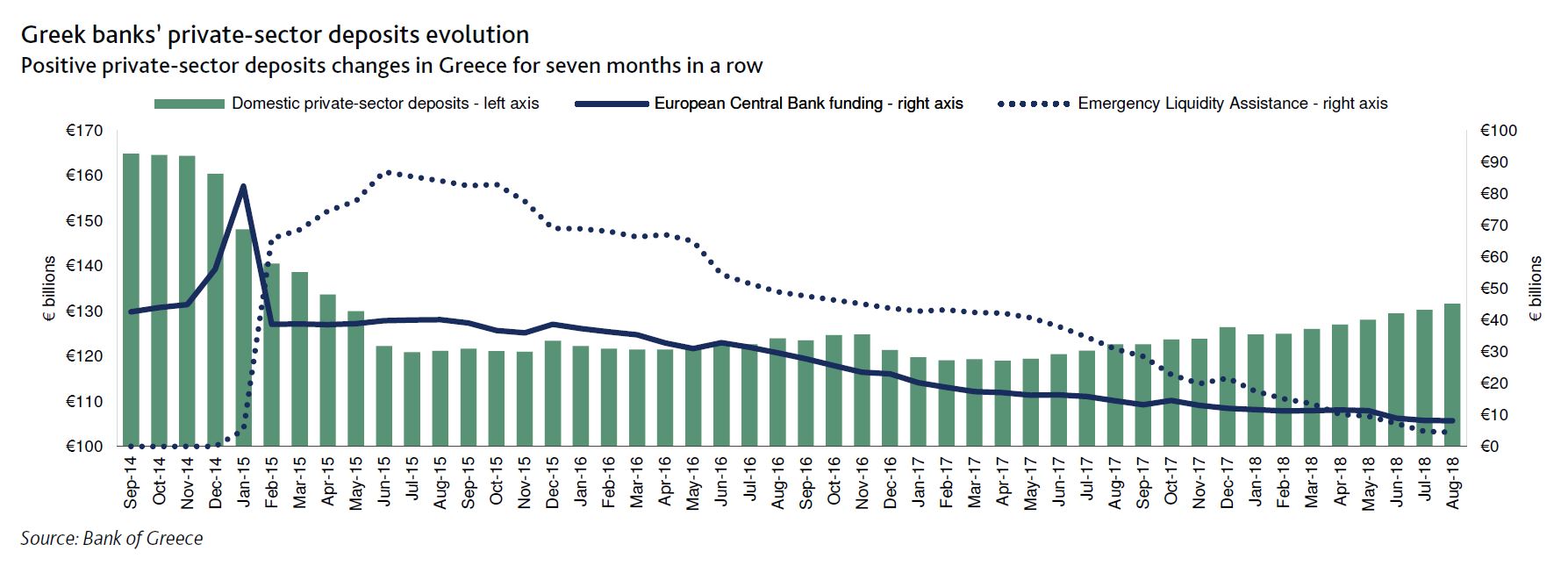

On 1 October, Greece (B3 positive) further relaxed capital controls that had been in place since June 2015 following an announcement by the Ministry of Finance in the government gazette. The country’s improving economic prospects and an increase in private-sector deposits in recent months allowed for the easing of capital controls, which will likely strengthen depositors’ confidence and help banks further improve their funding profiles, a credit positive.

The gradual return of deposits to the banking system over the past seven months and greater optimism following Greece’s successful exit from its economic adjustment programme are the key drivers behind the Ministry of Finance and the Bank of Greece’s decision to significantly loosen capital controls. In addition, a material reduction in banks’ dependence on central bank funding through the Bank of Greece’s Emergency Liquidity Assistance (ELA) mechanism signifies banks’ liquidity improvement in recent quarters.

As part of the relaxation of capital controls, the new measures include unlimited cash withdrawal for domestic deposits either through banks’ branches or ATMs; cash withdrawals from a credit and prepaid cards abroad of up to €600 per day and up to €5,000 per month; an increase in the limit on fund transfers abroad by companies to €100,000 per customer per day from €40,000 previously; and the ability for check payments in cash.

The easing of restrictions will likely encourage households and companies to return to local banks any money held outside of Greece’s banking system. An increase in customer deposits in recent years has helped Greek banks reduce their ELA balance, which totalled approximately €4.5 billion, or 2% of total banking assets at the end of August 2018, versus 21% in August 2015.

Also driving the ELA decrease was an increase in interbank lending transactions/repos as international investors’ appetite for Greek risk increased and they accepted a wider range of Greek assets as collateral for such repos. The ELA reduction supports Greek banks’ net interest margins because both the repo transactions and the new deposits carry a lower interest rate than the more expensive ELA, which costs around 1.5%.

Three of six rated Greek banks have fully repaid their ELA balances: National Bank of Greece S.A. , Piraeus Bank S.A. and Pancretan Cooperative Bank Ltd . We also expect Eurobank Ergasias S.A. and Alpha Bank AE to repay their ELA balance over the next few months, while Attica Bank S.A. will likely take a bit longer to fully eliminate its ELA.

The relaxation measures gradually ease capital controls put in place in June 2015 to stem deposit outflows from Greek banks during the first half of that year (see exhibit). However, the successful implementation of Greece’s economic adjustment programme, which concluded in August this year, and prospects of a gradual return to economic growthare already driving higher private-sector customer deposits, which grew by 4.1%, or €5.2 billion, during the first eight months of 2018.

Following the political and economic turmoil in 2015, tensions have eased over the past two years. The current government has managed to legislate a large number of reform measures, despite its slim majority in parliament and without triggering large-scale protests, as had been the case during the previous two adjustment programs. However, domestic politics and social instability remain the main risks to policy implementation and economic recovery. A potential prolonged political uncertainty, combined with looser capital controls, could cause significant deposit outflows, as was the case in the first half of 2015.

An incentive program run by a major bank, which rewards bankers with bonuses for achieving home loan sales targets, was a “significant cause” of misconduct involving “collusion” between its employees and introducers, according to Commissioner Kenneth Hayne.

In the interim report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, Commissioner Kenneth Hayne alleged that NAB’s Star Sales Incentive Plan, which offered rewards for employees that achieve home loan sales targets, was a “significant cause” of misconduct involving the bank’s employees and third-party introducers in the years between 2013 and 2016.

In March, during the course of the first round of public hearings held by the commission, it was revealed that some NAB employees had engaged in fraudulent conduct when processing home loans referred to the bank by introducers.

In one instance, a NAB employee was found to have wilfully entered false information on a customer’s profile and in relation to an introducer’s contact details, and had accepted, or encouraged other employees to accept, documentation from an introducer as verification to support lending applications.

NAB acknowledged in its written submission to the royal commission that the misconduct that was identified “was attributable to several systemic issues in relation to its Introducer Program” and the structure of its incentive program.

However, the bank claimed that there was no evidence that the incentive program was a “significant” cause of the conduct, as opposed to having “contributed to a small number of people choosing to behave unethically”.

Commissioner Hayne, however, has dismissed NAB’s contention, claiming that its employees, which engaged in misconduct, were motivated by the incentive program.

“I do not accept this last proposition,” Mr Hayne said. “The proposition makes sense only if it is read as asserting that some of those who engaged in the relevant conduct [were] driven by the pursuit of financial gain, but that there was, or may have been, some other unknown reason why others participating in the conduct acted as they did.”

Commissioner Hayne continued: “NAB has not previously suggested that those who acted as they did were motivated by anything but financial gain.

“The evidence shows that from as early as April 2015, NAB was aware that one of the potential root causes of the conduct was the Star Sales Incentive Plan that the relevant bankers were operating [under].

“The investigation of the conduct confirmed that the incentive program was driving inappropriate behaviour.”

Commissioner Hayne added that the “scorecards by which employees were assessed” were “weighted heavily in favour of financial matters”, stating that “marginal weight attributed to compliance-related matters”.

“In the words used in one of the documents produced by NAB, the ‘risk/reward equation for bankers [was] unbalanced in favour of sales over keeping customers and the bank safe’,” the commissioner said.

While Commissioner Hayne noted that NAB has since moved many of its employees to a different incentive plan (the Short Term Incentive Plan), and proposes to introduce further changes to its remuneration structures from 1 October 2018, “that program presently continues to reward bankers with bonuses for achieving targets for the sale of home loans,” he said.

Further, Commissioner Hayne noted that NAB employees were also told that introducers were required to refer a minimum of $2 million in loans per year for personal lending and $10 million a year for business lending, which he claimed “tied” the commissions paid to introducers to the amounts of loans referred that were drawn down.

“This created a further incentive for collusion between bankers and introducers and NAB itself identified introducer commission structures as potentially not driving the right behaviours,” Mr Hayne said.

Commissioner Hayne concluded: “The incentive arrangements used by NAB for bankers and for introducers were a significant cause of the conduct.”

RC looks at broker commissions

The financial services royal commission has taken a close look at remuneration structures (and more specifically, commissions) operate in the mortgage space, and has gone as far as to question whether some broker commissions are in breach of the NCCP.

In the interim report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, Commissioner Kenneth Hayne claimed that lenders paying value-based upfront and trail commissions could be in breach of section 47(1)(b) of the National Consumer Credit Protection Act (NCCP).

Section 47(1)(b) states that licensees must “have in place adequate arrangements to ensure that clients are not disadvantaged by any conflict of interest that may arise wholly or partly in relation to credit activities engaged in by the licensee or its representatives”.

Commissioner Hayne pointed to conclusions reached by the Australian Securities and Investments Commission (ASIC) in its broker remuneration review and by Commonwealth Bank (CBA) in its submission to the Sedgewick review.

The commissioner stated that such reports suggested that value-based commissions were “reliably associated” with higher leverage, and that loans written through brokers have a higher incidence of interest-only repayments, higher debt-to-income levels, higher loan-to-value ratios and higher incurred costs compared with loans negotiated directly with the bank.

“Those conclusions point towards (I do not say require) a conclusion that the lenders did not have adequate arrangements in place to ensure that clients of the lender are not disadvantaged by the conflict between the intermediary’s interest in maximising income and the borrower’s interest in minimising overall cost,” Commissioner Hayne said.

However, Commissioner Hayne claimed that breaches of section 47 “are duties of imperfect obligation in as much as breach is neither an offence nor a matter for civil penalty”.

The public is being invited to respond to Commissioner Hayne’s interim report from the financial services royal commission, which covers the first four rounds of hearings.

Submissions in response to the interim report can be made on the Royal Commission website and must be received no later than 5pm on 26 October 2018.

Lenders paying value-based upfront and trail commissions to mortgage brokers could be in breach of their legal obligations, according to the interim report of the financial services royal commission.

In the interim report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry, Commissioner Kenneth Hayne has claimed that lenders paying value-based upfront and trail commissions could be in breach of section 47(1)(b) of the National Consumer Credit Protection Act (NCCP).

Section 47(1)(b) states that licensees must “have in place adequate arrangements to ensure that clients are not disadvantaged by any conflict of interest that may arise wholly or partly in relation to credit activities engaged in by the licensee or its representatives”.

Commissioner Hayne pointed to conclusions reached by the Australian Securities and Investments Commission (ASIC) in its broker remuneration review and by Commonwealth Bank (CBA) in its submission to the Sedgewick review.

The commissioner stated that such reports suggested that value-based commissions were “reliably associated” with higher leverage, and that loans written through brokers have a higher incidence of interest-only repayments, higher debt-to-income levels, higher loan-to-value ratios and higher incurred costs compared with loans negotiated directly with the bank.

“Those conclusions point towards (I do not say require) a conclusion that the lenders did not have adequate arrangements in place to ensure that clients of the lender are not disadvantaged by the conflict between the intermediary’s interest in maximising income and the borrower’s interest in minimising overall cost,” Commissioner Hayne said.

However, Commissioner Hayne claimed that breaches of section 47 “are duties of imperfect obligation in as much as breach is neither an offence nor a matter for civil penalty”.

He continued: “Instead, breach of the general obligations may enliven ASIC’s power under section 55 to cancel or suspend the licensee’s licence.

“Hence, to refer this issue to ASIC would be to refer a matter that could not lead to any enforcement action other than cancellation or suspension of a licence.”

The commissioner added that any consideration of changes to the way breaches of section 47 are enforced would be “overtaken by any industry-wide change to remuneration structures”, noting that “where the failure (if that is what it is) is industry-wide, it would not be the occasion to consider cancellation or suspension”.

Commissioner Hayne concluded: “For these reasons, I go no further than noting that continuing to pay intermediaries a value-based upfront and trail commission after the deleterious consequences of the practice had been identified might have been a breach of Section 47(1)(b) of the NCCP Act.”

Welcome to the Property Imperative weekly to 29th September 2018, our digest of the latest finance and property news with a distinctively Australian flavour.

Another mega week, with the Royal Commission interim report out, the FED lifting rates, APRA releasing their banking stress tests, more class actions launched and Banks lifting their provisions to cover the costs of remediation, so let’s get stuck in…

Watch the video or read the transcript.

And by the way you value the content we produce please do consider joining our Patreon programme, where you can support our ability to continue to make great content..

The Royal Commission Interim Report came out on Friday and turned the spotlight on the Greed driving Financial Services to sell at all costs, take fees from dead people, and reward anti-customer behaviour. The report also called into question the role of the regulators, saying they were weak, and did not do their job. In fact, it’s not the lack of appropriate law, but it is noncompliance, without consequence which is the issue. They also raised the question of the STRUCTURE of industry. We discussed this in an ABC Radio National Programme, alongside Journalist Adele Ferguson and Ex. ACCC boss Graeme Samuel, and also in our show “Inside The Royal Commission Interim Report”.

The Royal Commission has touched on the critical issues which need to be considered. But now we have to take the thinking further. In terms of structure, we should be thinking about how to break up the financial services sector into smaller more manageable entities that are not too big to fail. We should separate insurance from wealth management from core banking, and separate advice from product selling and manufacturing. There is a clear opportunity to implement Glass Steagall, which separates risky speculative activity from core meat and potatoes banking services we need. There is a big job to be done in terms of cultural change, within the organisations, as they shift to customer centricity – building their businesses around their customers. This requires different thinking from the top. Also Regulators have clearly not been effective because they were too close and too captured. This must be addressed. The industry has played them, being prepared to pay small penalties if they get caught as just a cost of doing business. No real consequences.

Poor culture is rife across the industry and regulators. For example, LF Economics Lyndsay David tried under a FOI request to get APRA to release details of its targeted reviews into the mortgage sector from 2016. Specifically whether Treasury were aware of the results. They were not.

The review was never intended to made public but was revealed during the Hayne Royal Commission. It found that at Westpac only one in 10 of banks’ lending controls were operating effectively. In fact, APRA had ordered these “targeted review” in October 2016 and were conducted by PWC for WBC and CBA. On 12 October 2016, APRA issued a letter to the Bank and 4 other large banks requesting that they undertake a Review into the risks of potential misrepresentation of mortgage borrower financial information used in loan serviceability assessments. In its letter, APRA referenced assertions made by commentators that “fraud and manipulation of ADI residential mortgage origination practices are relatively commonplace”. Frankly the fact that these were buried, and the APRA still refuses to release they tells us more about APRA than anything else. After all we know mortgage fraud was widespread.

In this light, the APRA stress tests results, is on the same theme, high level, and vague, compared with the bank by bank data the FED releases, it’s VERY high level! In APRA’s view, the results of the 2017 exercise provide a degree of reassurance: ADIs remained above regulatory minimum levels in what was a very severe stress scenario. John Adams and I discussed this recently in our post “The Great Airbrush Scandal” APRA is not convincing.

ASIC revealed this week that it has identified serious, unacceptable delays in the time taken to identify, report and correct significant breaches of the law among Australia’s most important financial institutions. It can they say take over 4.5 years to identify that a breach incident has occurred! ASIC chair said “Many of the delays in breach reporting and compensating consumers were due to the financial institutions’ inadequate systems, procedures and governance processes, as well as a lack of a consumer orientated culture of escalation”.

So now there is a growing sense of panic as according to the Australian, for example, from APRA who says a horde of Australia’s biggest financial institutions and superannuation funds have been forced by the prudential regulator to ram through an in-depth review of their culture and governance before the royal commission ends next year. After copping heavy criticism over the course of Kenneth Hayne’s royal commission over a lack of enforcement in the financial sector, the Australian Prudential Regulation Authority has demanded Westpac, ANZ and National Australia Bank mimic the landmark cultural investigation of Commonwealth Bank the regulator launched late last year. Along with the major banks, some of the nation’s biggest union and employer-backed super funds — such as the $40 billion Hostplus, $35bn fund Cbus and $50bn REST super fund — have also been asked by APRA to review their culture.

And from the industry, for example the AFR reported that Westpac hauled each of its 40,000 bankers into urgent briefings by chief executive Brian Hartzer this week, before the Royal Commission Report came out, who warned them to bring forward customer problems.

Westpac also announced that Cash earnings in Full Year 2018 will be reduced by an estimated $235 million following continued work on addressing customer issues and from provisions related to recent litigation. This included increased provisions for customer refunds associated with certain advice fees charged by the Group’s salaried financial planners due to more detailed analysis going back to 2008. These include where advice services were not provided, as well as where we have not been able to sufficiently verify that advice services were provided; Increased provisions for refunds to customers who may have received inadequate financial advice from Westpac planners; Additional provisions to resolve legacy issues as part of the Group’s detailed product reviews; Provisions for costs of implementing the three remediation processes above; and Estimated provisions for recent litigation, including costs and penalties associated with the already disclosed responsible lending and BBSW cases. Costs associated with responding to the Royal Commission are not included in these amounts.

Across the industry more than $1 billion has been put aside, so far and more to come. And guess who will ultimately pick up the tab for these expenses – yes we the customers will pay!

Another class action was announced this week as Law firm Slater and Gordon said it had filed class action proceedings in the Federal Court against National Australia Bank and MLC on behalf of customers sold worthless credit card insurance. Most were existing NAB customers and the bank should have known the insurance was likely to be of little or no benefit to them. Despite knowing this, NAB have continued to push the insurance widely, reaping millions in premiums while doing so. most people were sold the insurance over the phone and were not given a reasonable opportunity to understand the terms and conditions of the policy.

We continued to debate the trajectory of home price falls, as Media Watch discussed the 60 Minutes segment we were featured in. Once again somewhat myopic views were expressed by host Paul Barry, as we discussed on our recent post. You can also watch the 60 Minutes segment on YouTube which covers my views more comprehensively. Prices are set to fall further. Period.

Realestate.com.au says that according to a survey of property experts and economists further falls in housing prices across Australia’s cities are expected. They suggest an 8.2% fall in house prices in Sydney, a 8.1% fall in Melbourne and a 7% fall in Brisbane. In fact all centres are expected to see a fall. Finder.com.au insights manager Graham Cooke was quoted as saying that the cooling market conditions made it harder for existing homeowners to build up equity. But they could be good news for first-home buyers with a deposit in hand. “If you’re thinking of getting into the market over the next few years, hold out until prices have dropped further and use this time to save for your upfront costs,” he said. “Right now, there’s no need to jump on the first suitable property you see. Waiting a few years could potentially save you thousands of dollars.”

Damien Boey at Credit Suisse said this week that by the start of 2020, Sydney house prices could have dropped by 15-20% from their 2017 peak. The market is heavily oversupplied, even before we consider the risk of higher insolvency activity and foreclosure sales. He argues that demand is the problem – not credit supply. We could ease lending standards from here, and still not cause housing demand to bounce back. Investors cannot sustain capital growth by themselves. They need a “greater fool” to on sell their houses too. But foreign demand is weak, and first home buyers are priced out of the market. Specifically, Chinese demand for property is weak, as evidenced by low levels of outward direct investment, and the failure of the AUD to rise in response to CNH weakness. Promised relaxation of capital controls has not eventuated, and CNY devaluation pressure has had a negative impact on credit conditions, as well as the ability of Chinese residents to export capital abroad. Finally, dwelling completions are still rising in response to high levels of building approvals from more than a year ago – the building lead time has lengthened significantly. As for the RBA, any rate cuts from here are unlikely to be passed on in full to end borrowers, given counterparty credit risk concerns in the interbank market.

UBS Global Housing Bubble Index came out and showed that Sydney had slipped from 4th to 11th in a year. They noted that Prices peaked last summer and have slid moderately as tighter lending conditions reduced affordability. Particularly since the land tax surcharge more than doubled and a vacancy fee was introduced, the high end of the market has suffered most. The vacancy rate on the rental market has also climbed. Nevertheless, inflation-adjusted prices are still 50% higher than five years ago, while rents and incomes have grown at only single-digit rates.

Corelogic reported further prices falls this week in Sydney, down 0.57%, Melbourne down 0.79%, Adelaide, down 0.15%, Perth down 0.73%, while Brisbane rose a little up 0.06%. Melbourne looks to be the weakest centre currently, and we continue to expect to see further falls.

CoreLogic says that last week 2,404 homes went to auction across the combined capital cities, returning a final auction clearance rate of 52.4 per cent, slightly higher than the 51.8 per cent the previous week which was the lowest seen since Dec-12. Over the same week last year, 2,782 homes went to auction and a clearance rate of 66.2 per cent was recorded.

Melbourne’s final clearance rate was recorded at 53.8 per cent across 1,161 auctions last week, compared to 54.1 per cent across a lower 988 auctions over the previous week. This time last year a higher 1,361 homes were taken to auction across the city and a much stronger clearance rate was recorded (70.6 per cent).

Sydney’s final auction clearance rate came in at 51.1 per cent across 851 auctions last week, up from 48.6 per cent across 669 auctions over the previous week. Over the same week last year, 1,033 Sydney homes went to auction returning a final clearance rate of 65.9 per cent.

Across the smaller auction markets, clearance rates improved across Adelaide and Tasmania, while Brisbane, Canberra and Perth saw clearance rates fall week-on-week.

Of the non-capital city auction markets, the Geelong region was the best performing in terms of clearance rate (61.1 per cent), followed by the Hunter region where 58.8 per cent of homes sold.

The combined capital cities are expecting 65 per cent fewer homes taken to market this week, with half the nation host to an upcoming public holiday, combined with both the NRL and AFL grand finals being held over the weekend, it looks to be a quiet week for the auction markets.

There are 846 capital city auctions currently being tracked by CoreLogic this week, down from the 2,404 held last week and lower than the 969 auctions held over the same week last year.

Finally, the latest RBA and APRA lending statistics, plus the June quarter household ratios, shows that credit growth is still too strong, with the 12-month growth by category shows that owner occupied lending is still growing at 7.5% annualised, while investment home loans have fallen to 1.5% on an annual basis. Overall housing lending is growing at 5.4% (compared with APRA growth of 4.5% over the same period, so the non-banks are clearly taking up some of the slack). Still above wages and inflation. Household debt continues to rise.

The non-bank sector (derived from subtracting the ADI credit from the RBA data) shows a significant rise up 5% last month in terms of owner occupied loans. APRA needs to look at the non-banks. And quickly. This was confirmed looking at the rising household debt to income ratios, where in short the debt to income is up again to 190.5, the ratio of interest payments to income is up, meaning that households are paying more of their income to service their debts, and the ratio of debt to home values are falling. All three are warnings. The policy settings are not right. You can watch our show “What Does The Latest Data Tell Us? But for now it is worth highlighting that despite all the grizzles from the property spruikers, mortgage lending is STILL growing…. and faster than inflation. We have not tamed the debt beast so far, despite failing home prices. No justification to ease lending standards – none.

So to a quick look at the markets. The ASX 200 Financial Sector Index was up 1.20% on Friday to close at 6,127 – in a relief rally that the Royal Commission report was not worse (and the prospect of less regulation was mooted). We think this will reverse as the full implications of the report are digested, but of course the market profits from volatility. CBA, the biggest owner occupied mortgage lender was up 1.9% to close at 71.41, despite some analysts now suggesting a fair price closer to 65.00. Both are a long way from the 81.00 it reached in January. It will not return there anytime soon.

Westpac rose 1.16% to close at 27.93, still well off its November 2017 highs of 33.50, National Australia Bank rose 1.76% to 27.81 and ANZ closed at 28.10 up 1.4%. AMP, who has already been hit hard by the Royal Commission rose 1.59% to 3.19, still way down on its March highs before the revelations came out. Macquarie Group fell 1.34% and ended at 126.04. Suncorp ended at 14.46, up 0.84% and Bendigo Adelaide Bank rose 1.22% to 10.75. The Aussie ended up a little to 72.22, 0.19% higher on Friday, but with still more falls expected ahead, we think it could test 71.00 quite soon.

In the US markets, the Dow Jones Industrial ended at 26,458, up 0.07%, but off its recent highs, the NASDAQ ended up 0.05% to 8,046, while the S&P 500 was flat at 2,913. The Volatility index was lower, at 12.12, down 2.34%. The bulls are, in the short term at least, firmly in control.

Gold was up 0.74% to 1,196, but still in lower regions than last year, reacting to the strength of the US Dollar. Oil was higher again, up 1.41% to 73.53. In fact, until sizable supply is offered up by OPEC some are suggesting we could see prices above the $100 per barrel market, but $100 seems an overreach on the current charts.

On the currencies, the Yuan USD was up 0.31% to 14.56, as China continues to manage the rate lower. Of course the trade wars are in full play.

President Trump has announced a 10% tariff on $200 billion in Chinese imports. That tariff is currently 10%, but at the end of 2018, that’s expected to rise to 25%. This is the third round of tariffs, and it’s the largest round of tariffs. Back in July, we had $34 billion worth of Chinese goods tariffed. Then, in August, we had a follow-on of $16 billion in tariffs. So, this is really a huge jump up of $200 billion. This is affecting all kinds of goods. The U.S. brings in a little over $500 billion worth of goods from China. The $250 billion so far this year is roughly half, but Trump has said that if China were to take retaliatory action on these tariffs, which they have, in fact, then he’s going to put in place another $267 billion worth of imports. For all intents and purposes, that would put a tariff in place on 100% of U.S.-China trade.

China also announced some tariffs on $60 billion worth of goods that also went into effect on September 24th. This is in addition to, China had also had previously announced tariffs of $50 billion. The total U.S.-China trade is about $130 billion dollars of imports of United States goods into China. This second round of Chinese tariffs is going to now cover $110 billion dollars of the $130 billion of U.S.-China trade — again, almost 100% of the entire trading relationship.

So, this is pretty significant in that almost all the cards have been played here. If all the threats and allegations with regard to tariffs are followed through upon, all of U.S.-China trade is set to be under some kind of tariff barrier in 2018. This will be a big deal.

The 10 Year Bond rate was up 0.29% to 3.065 after the Fed rate hike this week. The Fed moved as expected, and continues to highlight more upward movements in the months ahead – in fact their language is arguably more bullish now. The target range for the federal funds rate is now 2 to 2-1/4 percent. In their projection release, they see GDP sliding from 2019…. while inflation is expected to rise. The 3-month rate was up 0.35% on Friday to 2.207., still signalling a recession risk down the track. We discussed the impact of the US Rated move in our show “The FED Lifts, More Ahead And What Are The Consequences?”

Finally, turning to Crypto, Bitcoin ended down 1.43% to 6,617. Little signs of new directions here in the short term.

So in summary a week dominated by the Royal Commission locally, against a back cloth of higher international interest rates, and risks. We are, as they say, set for interesting times ahead.

Towards the end of the report, which runs to several hundred pages, there is a summary of the issues and questions. The very last item is the most significant “Is structural change in the industry necessary”. To which I believe the answer is YES…

The many questions can then be distilled and organised in three categories:

• Issues

• Causes

• Responses

8.1 Issues

The issues can be divided into four groups. First, there are issues about access to banking services. Second, there is a group of issues about the roles and responsibilities of intermediaries – those who stand between the purchaser of a financial service and the provider of that service. Third there is a group of issues about responsible lending. And fourth, there is a group of issues about regulation and the regulators.

The issues intersect and overlap in different ways. Putting the issues in groups should not be allowed to diminish the importance of identifying and responding to those intersections and overlaps.

8.1.1 Access

Do all Australians have adequate and appropriate access to

banking services?

8.1.2 Intermediaries

• For whom do the different kinds of intermediary act?

– mortgage brokers

– mortgage aggregators

– introducers

– financial advisers

– authorised representatives of Licensees

– point of sale sellers of loans

• For whom should each kind of intermediary act?

• If intermediaries act for the consumer of a financial service

– What duty do they now owe the consumer?

– What duty should they owe?

• Who is responsible for each kind of intermediary’s defaults?

• Who should be responsible?

• How should intermediaries be remunerated?

• Are external dispute resolution mechanisms satisfactory?

• Should there be a mechanism for compensation of last resort?

8.1.3 Responsible lending

• Consumers

– Should the test to be applied by the lender remain ‘not unsuitable’?

– How should the lender assess suitability?

– Should there be some different rule for some home loans?

• Should the NCCP Act apply to any business lending? In particular, should any of its provisions apply to:

– SMEs?

– agricultural businesses?

– some guarantors of some business loans?

• To what business lending should the Banking Code of Practice apply?

– Is the definition of ‘small business’ satisfactory?

• Should lenders adopt different practices or procedures with respect to agricultural lending?

• Are there classes of persons from whom lenders

– should not take guarantees; or

– should not take guarantees unless the person is given particular information or meets certain conditions?

• How should lenders manage exit from a loan

– at the end of the loan’s term;

– if the borrower is in default?

8.1.4 Regulation and the regulators

• Have entities responded sufficiently to the conduct identified and criticised in this report?

• Has ASIC’s response to misconduct been appropriate?

– If not, why not?

– How can recurrence of inappropriate responses be prevented?

• Has APRA’s response to misconduct been appropriate?

– If not, why not?

– How can recurrence of inappropriate responses be prevented?

8.2 Causes

What were the causes of the conduct identified and criticised in this report?

• Conflict of interest and duty?

• Remuneration structures?

• Culture and governance?

• Regulatory response?

8.3 Responses

What responses should be made to the conduct identified and criticised in this report?

• Are changes in law necessary?

– Should the financial services law be simplified?

– Should carve outs and exceptions be reduced or eliminated? In particular, should

• grandfathered commissions

• point of sale exceptions to the NCCP Act

• funeral insurance exceptions

be reduced or eliminated?

• How should entities manage conduct and compliance risks?

• How should

– APRA

– ASIC

respond to conduct and compliance risk?

• Should the regulatory architecture change?

– Are some tasks better detached from ASIC?

– Are some tasks better detached from APRA?

– What authority should take up any detached task?

– Should either or both of ASIC and APRA be subject to

external review?

• What is the proper place for industry codes of conduct?

– Should industry codes of practice like the 2019 Banking Code

of Practice be given legislative recognition and application?

• Should an intermediary be permitted to

– recommend to a consumer

– provide personal financial advice to a consumer about

– sell to a consumer

any financial product manufactured by an entity (or a related party

of the entity) of which the intermediary is an employee or

authorised representative?

• Is structural change in the industry necessary

The Royal Commission has released its interim report. Here is the executive summary, pointing to GREED as the underlying factor and making the point that it is adherence to the law and regulatory supervision of the law are the main issues. Essentially selling products and services (at all costs) appear to be the driver. I discussed this on Radio National this morning – even highlighting the GREED driving behaviour.

The Commission’s work, so far, has shown conduct by financial services entities that has brought public attention and condemnation. Some conduct was already known to regulators and the public generally; some was not.

Why did it happen? What can be done to avoid it happening again? These are now the key questions.

In this Interim Report these questions – ‘why’ and ‘what now’ – are asked with particular reference to banks, loan intermediaries and financial advice, with a view to provoking informed debate about both questions.

Why did it happen?

Too often, the answer seems to be greed – the pursuit of short term profit at the expense of basic standards of honesty. How else is charging continuing advice fees to the dead to be explained? But it is necessary then to go behind the particular events and ask how and why they came about.

Banks, and all financial services entities recognised that they sold services and products. Selling became their focus of attention. Too often it became the sole focus of attention. Products and services multiplied. Banks searched for their ‘share of the customer’s wallet’. From the executive suite to the front line, staff were measured and rewarded by reference to profit and sales.

When misconduct was revealed, it either went unpunished or the consequences did not meet the seriousness of what had been done. The conduct regulator, ASIC, rarely went to court to seek public denunciation of and punishment for misconduct. The prudential regulator, APRA, never went to court. Much more often than not, when misconduct was revealed, little happened beyond apology from the entity, a drawn out remediation program and protracted negotiation with ASIC of a media release, an infringement notice, or an enforceable undertaking that acknowledged no more than that ASIC had reasonable ‘concerns’ about the entity’s conduct. Infringement notices imposed penalties that were immaterial for the large banks. Enforceable undertakings might require a ‘community benefit payment’, but the amount was far less than the penalty that ASIC could properly have asked a court to impose.

What can be done to prevent the conduct happening again?

As the Commission’s work has gone on, entities and regulators have increasingly sought to anticipate what will come out, or respond to what has been revealed, with a range of announcements. These include announcements about new programs for refunds to and remediation for consumers affected by the entity’s conduct, about the abandonment of products or practices, about the sale of whole divisions of the business, about new and more intense regulatory focus on particular activities, and even about the institution of enforcement proceedings of a kind seldom previously brought. There have been changes in industry structure and industry remuneration.

The law already requires entities to ‘do all things necessary to ensure’ that the services they are licensed to provide are provided ‘efficiently, honestly and fairly’. Much more often than not, the conduct now condemned was contrary to law. Passing some new law to say, again, ‘Do not do that’, would add an extra layer of legal complexity to an already complex regulatory regime. What would that gain?

Should the existing law be administered or enforced differently? Is different enforcement what is needed to have entities apply basic standards of fairness and honesty: by obeying the law; not misleading or deceiving; acting fairly; providing services that are fit for purpose; delivering services with reasonable care and skill; and, when acting for another, acting in the

best interests of that other? The basic ideas are very simple. Should the law be simplified to reflect those ideas better?

This Interim Report seeks to identify, and gather together in Chapter 10, the questions that have come out of the Commission’s work so far. There will be a further round of public hearings to consider these and other questions that must be dealt with in the Commission’s Final Report.