From the Sedgewick report, to the Productivity Commission and ASIC’s investigations, brokers – particularly their remuneration – have been under fire from all corners; via Australian Broker.

Now, a cohort of industry execs have come together to help the industry unite through a dedicated forum.

The Mortgage Industry Forum (MIF), is backed by 16 founding members from Yellow Brick Road, Foster Finance, Mortgage Success, Shore Financial, ALIC, Intelligent Finance and Loan Market, among others.

Revealing the details during a National Finance Broker Day event in Sydney, YBR executive chairman Mark Bouris said, “This is important. It’s about time we reacted and there is something happening, that I’m involved in, and I would be happy for you to join us.”

Reiterating that MIF is “not against ASIC” or intending to become a competitor to the MFAA or FBAA, the group is intended to be “adjunctive to the Combined Industry Forum”.

Bouris continued, “The objective is to assess all the recommendations that are being made about us as an industry

“I paid for it, we meet every week or two and we cull through every recommendation that has been made by the CIF, Sedgewick, every recommendation from the Productivity Commission, ASIC and anybody else who matters,” he added.

MIF has written and submitted its own report to Treasury and the royal commission, which contains industry observations and recommendations from the broker perspective, with a heavy focus on protecting trail commissions.

Bouris explained, “We are trying to build a case for brokers so we, as a segment of the market can hand over …. a document to show how we should be regulated or managed around fee structures, our obligations, our transparency, training and compliance for the future. “

Next, a survey of broker input on the six CIF recommendations – available for all brokers to contribute towards through MIF’s Facebook page – will also be taken to key decision makers.

“We need to take to the government a document that will say, of the 17,000 brokers in this country, this many support all the recommendations. Otherwise all we have is people speaking for us, on our behalf, and that doesn’t work,” Bouris continued.

In addition to gauging sentiment, the group will also make practical suggestions as to how brokers can demonstrate the ongoing work they do in return for trail commission. Further, the group will also suggest new tools to support compliance and best practice.

Among the ideas floated, Bouris revealed an idea for a broker app that records client conversations and uploads them to a cloud accessible by ASIC, banks, aggregators and other key players in monitoring and compliance.

Adding that he believes the chances “right now are 50/50” that remuneration structures will change, Bouris said, “If 20% of our income is lost, the industry will collapse and if our industry doesn’t survive, the banks will just get stronger.”

He added, “We are the easy ones to target. We are fragmented. Banks have teamed up together and they have massive balance sheets and lobby groups, they are politically connected and they are the biggest tax payers in the country – so nobody is going to hurt them.

“If you don’t support the group and something happens that isn’t in your favour, you have only yourselves to blame. Something radical could happen – I’ve seen it happen in the past.”

Yet again this week, the Hayne Royal Commission has brought disturbing news of misconduct toward customers of our largest financial institutions. This time super accounts have been plundered for the benefit of shareholders.

Recent research from economists at the United States Federal Reserve suggests this problem is not unique to Australia. If true, this supports the argument that larger financial institutions should be broken up or face more regulatory scrutiny.

The researchers found that larger banking organisations are more likely than their smaller peers to experience “operational losses”. And by far the most significant category (accounting for a massive 79%) within operational losses was “Clients, Products and Business Practices”.

This category captures losses from “an unintentional or negligent failure to meet a professional obligation to specific clients, or from the nature or design of a product”. When a bank is caught out engaging in misconduct toward customers, it is required to make good to customers – the so-called process of remediation.

It’s a category that perfectly captures the issues under review in the royal commission. Operational losses also include things like fraud, damage to physical assets and system failures.

In recent weeks we have heard a lot about Australian banks having to compensate customers. The cost to the bank is, however, far greater than the dollar value received by customers.

The administrative costs of such programs are significant, and then there are legal costs and regulatory fines.

While no-one feels sorry for banks having to suffer the consequences of their misconduct, regulators monitor these losses due to the possibility that they may increase the chance of bank failure.

Another aspect of the Federal Reserve’s study is the size of the losses. One example is where the five largest mortgage servicers in the United States reached a US$25 billion settlement with the US government relating to improper mortgage loan servicing and foreclosure fraud.

In another example, a major US bank holding company paid out over US$13 billion for mis-selling risky mortgages prior to the 2008 crisis. Settlements of this size have simply not occurred in Australia.

Why larger banks?

One might assume that economies of scale – reduced costs per unit as output increases – also apply to risk management. The larger the organisation, the more likely it has invested in high-quality, robust risk-management systems and staff. If this holds, then a large bank should manage risk more efficiently than a smaller one.

The possibility of unexpected operational losses should then be reduced. Larger financial institutions might also attract greater regulatory scrutiny, which might help to improve risk-management practices and reduce losses.

For every 1% increase in size (as measured by total assets) there is a 1.2% increase in operational losses. In other words, banks experience diseconomies of scale. And this is particularly driven by the category of Clients, Products and Business Practices.

In this category losses accelerate even faster with the size of the bank.

This could be the result of increased complexity in large financial institutions, making risk management more difficult rather than less. As firms grow in size and complexity, it apparently becomes increasingly challenging for senior executives and directors to provide adequate oversight.

This would support the argument that some financial institutions are simply “too big to manage” as well as “too big to fail”. If bigger financial institutions produce worse outcomes for customers, there is an argument for breaking up larger institutions or intensifying regulatory scrutiny.

Is the same thing happening in Australia as in the United States? The case studies presented by the royal commission suggest it could be, but it’s difficult for researchers to know exactly.

Australian banks are not required to publicly disclose comprehensive data on operational losses. APRA may have access to such information, but any analysis the regulator may have done of it is not in the public domain.

Perhaps this issue is something Commissioner Hayne should explore.

Author: Elizabeth Sheedy Associate Professor – Financial Risk Management, Macquarie University

AMP’s superannuation funds are permitted to underperform for five years before the investment committee is obliged to inform the relevant fund’s board, the royal commission has heard, via InvestorDaily.

The royal commission has been told that a consistently underperforming AMP fund could be underperforming for five years before the board of directors becomes notified.

The royal commission hearings into superannuation continued on Thursday, with AMP Superannuation Limited chairman Richard Allert in the witness box.

Mr Allert faced questioning by counsel assisting Michael Hodge about how AMP management and board addresses poorly performing investment funds.

The royal commission was told that ‘quarterly investment management reports’, which contain information about the performance of AMP’s funds in a given quarter, are put together by AMP’s Group Investment Committee.

However, the board of AMP Superannuation does not receive this report. Instead, it goes to AMP trustee services.

Mr Hodge confirmed with Mr Allert that the report would only be raised with the board if trustee services found an issue with the report, or if there was an “exception”.

“Unless an exception was triggered, then you wouldn’t expect this report to be provided to the board?” Mr Hodge asked.

“Correct,” Mr Allert said.

The royal commission heard that such an ‘exception’ would have three criteria: the first was the ‘identification’ criteria, which meant pinpointing “significant under-performance against peers/benchmarks over rolling 36 month period”.

The second criteria was a period of ‘further investigation’, and the third and final criteria was an exceptions report that was issued “if an investigation remains under investigation … for a period of eight or more quarters”.

“So it would seem as if it would be necessary for an investment to underperform for five years before it would be reported to the board,” Mr Hodge put to Mr Allert.

“No, I couldn’t accept that,” he responded.

After a protest from AMP legal counsel Robert Hollo, who called the question “a little unfair”, Royal Commissioner Kenneth Hayne AC QC interceded and Mr Hodge rearticulated his question.

“Is it possible for an exceptions report to come to the board about investment performance any earlier than where the underperformance has occurred over a five-year period?”

Mr Allert said it was possible. “If there was something that was really bothering the Group Investment Committee and relaying it to the Trustee Services or was bothering our trustee services representative on the GIC, they would alert the board to that fact.”

But this would occur outside of the exceptions framework, the royal commission was told.

One instance where Mr Allert could recall AMP trustee services raising an issue with the board this year was “in relation to products that had a cash element”.

Earlier this year the chief of a financial planning firm collapsed in the witness stand during Australia’s ongoing royal commission into misconduct in the financial services industry. He had to be taken to hospital in an ambulance – some would say a fitting metaphor for the state of the industry.

Fortunately for him the health care system doesn’t operate like the financial planning industry. If it did he might have been “treated” according to what was most profitable for the ambulance service rather than what was best for his well-being.

The Financial Services Royal Commission is exposing abundant evidence of unethical misconduct. Customers are being charged fees for services they never get or ever need, getting inappropriate advice, being offered irresponsible loans and sold worthless insurance contracts. It shows up an industry riddled with conflicts of interest and obsessed with extracting profits from customers in any way conceivable.

Sound familiar? The 2007-09 Global Financial Crisis was in large part caused by the same “profit at all costs” culture. It fuelled high-risk home lending to ordinary people who couldn’t afford it. Why haven’t things changed?

Despite the lessons of the GFC and a regulatory crackdown, the central problem with the global financial services industry is that, unlike the health industry, it has long stopped caring about its customers’ well-being.

Financial services, such as payments and basic forms of credit and insurance, are now essential for the economy and society to function. For this reason, the large financial services firms often receive privileges such as market protection and implicit government guarantees worth billions of dollars, underwritten by taxpayers. So how has the bar been allowed to sink so low?

The mindset behind the scandals

At the heart of the problem lies the mental model that the finance industry applies to itself and the world around it.

This thinking is dominated by the neoclassical model of economics in which people are “rational actors” who always do what is best for them. And they supposedly interact with each other through perfect markets, leading to the efficient allocation of resources.

While everyone understands this as an idealised abstraction, the impact of this working assumption is profound. It has led to an “input-oriented” model. Banks and other financial services companies are exclusively concerned with providing whatever inputs – financial products and services – their customers demand.

Bewildering arrays of products are sold using state-of-the-art marketing techniques, irrespective of whether the customers actually need them.

Undesired outcomes are often considered to be the customer’s responsibility. If the customer ends up with too much credit card debt, possibly as a result of aggressive marketing, don’t blame the bank.

Regulatory and public policy responses are also premised on this model. The dominant approach in financial regulation focuses on disclosure, requiring firms to provide more and more information about their financial products.

Product disclosure statements are now often hundreds or thousands of pages long. These are littered with legal and financial jargon that is often incomprehensible even to experts. Rather than clarifying the nature of financial products, disclosure requirements have only made them more opaque.

This rationalist approach has led the industry and regulators to promote financial literacy education as a solution to the problem. The idea is to educate consumers about financial products and services to help them navigate the financial system and make good decisions.

The Australian government spends tens of millions of dollars on financial literacy programs such as its MoneySmart program. The Bank of England recently launched econoME, a program with very similar aims.

This approach ignores a core aspect of finance. Many financial problems that consumers face are highly complex. For example, determining a person’s optimal lifetime saving and investment strategy to provide an adequate income in retirement is a formidable problem, even for a finance expert with a supercomputer.

It is beyond the capability of the average person to work out many financial decisions on their own, and we shouldn’t expect people to do so – just as we don’t expect the average person to perform brain surgery.

Focus needs to shift to financial well-being

If we accept that many aspects of finance are hard, we will need to give up on the rationalist model. Instead we need to switch to an outcome-focused model in which, as with the health care system, the primary concern is for people to reach a set of outcomes or goals – a certain level of financial well-being, for example.

Services offered by banks and regulations imposed by governments would then be evaluated on the extent to which they offer to improve people’s financial well-being. Banks would only offer services that have been shown to improve one or more dimensions of their customers’ financial well-being, aligning their interests more closely with those of their customers.

Financial services and their regulation would look radically different. For example, fewer decision options and simpler products would be more effective in improving financial well-being. New technologies such as artificial intelligence could likely play an important role in this new world of finance.

Importantly, both the development of services and their regulation should be based on evidence and delivered under a set of professional standards monitored by an independent standards-setting body. This would be similar to the processes and institutions used in the health system. Providers of financial services would then be subject to both a fiduciary duty and product liability.

The future of finance doesn’t lie in ever more regulation, or ever more sophisticated technology to squeeze higher margins out of legacy products. The future of finance lies in the rediscovery of what finance is for – to improve the financial and economic well-being of society.

Authors: Paul Kofman Professor of Finance, University of Melbourne;

Carsten Murawski Associate Professor in the Department of Finance and co-director of the Brain, Mind & Markets Laboratory, University of Melbourne.

CBA defied a request from APRA to accelerate the transfer of 60,000 members to MySuper in order to placate the bank’s aligned advisers, the royal commission has heard, via InvestorDaily.

Appearing before the royal commission hearings into superannuation yesterday, Colonial First State (CFS) executive general manager Linda Elkins was questioned about CBA’s handling of the MySuper transition.

From 1 January 2014, employers could only make default contributions to a registrable superannuation entity (RSE) offering a MySuper product.

Counsel assisting Michael Hodge established in his questions to Ms Elkins that CBA had breached the law 15,000 times by receiving default contributions into high-fee-paying accounts after 1 January 2014.

RSEs were also given a deadline of 1 July 2017 to transfer existing accrued default accounts (ADAs) to an approved MySuper product.

In June 2014, Mr Hodge established, the board of CFS was told by management that “APRA has requested that you accelerate the transition for 60,000 [ADA] members”.

“This suggestion has significant business implications as the original transition date is 2016,” the CFS board was told in June 2014.

Mr Hodge asked Ms Elkins: “Was one of the issues of which you were aware that immediately moving these ADAs over to MySuper would affect the relationship between Colonial and its advisers?”

“I was aware that advisers were impacted by this, yes,” Ms Elkins replied. “I don’t know that it follows it would affect our relationship with the advisers but we were aware that advisers were – were concerned, yes.”

Moving the 60,000 into lower-fee MySuper products would have the effect of turning off grandfathered commissions for advisers, the royal commission has heard.

CFS, like other retail super providers, was eager to have ADA clients make an “investment decision” so that they would be considered a ‘Choice’ member and therefore ineligible for transfer to a MySuper product.

“And that was why you were taking active steps for the benefit of advisers to obtain investment directions from members?” asked Mr Hodge.

“We were taking active steps to ensure the members had information to – to assist them with the choices they had,” replied Ms Elkins.

Hodge continued: “The purpose of obtaining those investment directions, or a purpose, I’m sorry, for obtaining those investment directions was to benefit advisers?

Fitch Ratings says the Commonwealth Bank of Australia’s full-year results to 30 June 2018 (FY18) broadly support the agency’s expectation that earnings pressure would emerge for Australian banks during 2018. An increase in wholesale funding costs led to a reduction in CBA’s net interest margin in 2H18, loan growth continued to slow and continued investment into the business and compliance contributed to higher expenses. Mortgage arrears also trended upwards due to some pockets of stress, and while they have not translated into higher provision charges as yet due to strong security values, continued moderation in Australian house prices may result in higher provisioning charges in future financial periods.

Most of the earnings issues appear applicable across the sector and are likely to remain into 2019, placing pressure on profit growth for all Australian banks. Increased regulatory and public scrutiny of the sector may make it difficult for the larger banks to reprice loans to incorporate the increase in wholesale funding costs, meaning net interest margins are likely to face some downward pressure. Loan growth is likely to further slow as the housing market continues to moderate, while compliance costs continue to rise due to the scrutiny on the sector.

The most prominent scrutiny is the royal commission into misconduct in the banking, superannuation and financial services industry, which has already identified a number of shortcomings within the industry. We expect the release of the interim royal commission report, due to be published by the end of September 2018, to give a better view of how widespread these shortcomings are and what impact they may have on the credit profile of Australian banks.

CBA’s FY18 results show a level of resiliency despite these issues. The bank reported cash net profit after tax from continuing operations declined 5% to AUD9.2 billion in FY18, but this was driven by a number of one-off charges, including a AUD700 million fine to settle a civil case in relation to breaches of anti-money laundering and counter-terrorism financing requirements. Cash net profit after tax from continuing operations rose by 4% to AUD10.0 billion when the one-off items were excluded.

Balance-sheet metrics remain consistent with Fitch’s expectations. The bank reported a stable common equity Tier 1 ratio of 10.1%, which incorporates the AUD1 billion additional operational risk charge (essentially an increase of AUD12.5 billion in operational risk-weighted assets) put in place following the publication of the independent prudential inquiry report in May 2018. The divestiture of a number of assets planned for FY19 as well as CBA’s ability to generate capital through retained earnings mean the bank is well-positioned to meet the regulator’s “unquestionably strong” capital requirements ahead of schedule. CBA’s liquidity coverage ratio (131%) and net stable funding ratio (112%) both increased due to an improvement in the bank’s deposit mix towards more stable deposit types and a lengthening in the average term to maturity of its wholesale funding.

Fitch continues to monitor CBA’s progress in remediating shortcomings in its operational risk controls and governance identified in the May 2018 independent prudential inquiry report as risks around this process were a key driver of Fitch’s revision of CBA’s Outlook to Negative. CBA noted in the FY18 results announcement that the remediation program has received approval from the Australian Prudential Regulation Authority and that it aims to make significant progress in implementing the program over FY19. However, CBA also noted that full remediation would be a multiyear process for the bank.

The Productivity Commission Report into Competition in The Australian Financial System looked specifically at the role and function of the big four banks. Today we look at some of the evidence which they presented, in the light of the Green’s recently released policy on “Breaking Up the Banks”.

Whilst the market dominance of the big four, Westpac, CBA NAB and ANZ does not necessarily in itself mean the market is not competitive, the Productivity Commission suggests that such dominance may allow them to stifle competition by maintaining prices at artificially high levels or limiting innovation without losing any market share.

In many banking systems globally, larger institutions have more market power, and Australia is no exception. Their sheer size allows the major banks to spread their fixed costs (such as investment in new IT systems) across a broader asset base. They are also able to grow more quickly, as they have greater capacity to respond to an increase in demand. At the same time, size can create challenges — for example, changes are more difficult to implement in very large systems. There is a tipping point beyond which large organisations are no longer efficient and they operate at declining returns to scale.

The clearest and most powerful advantage that larger banks have over smaller ADIs, and one that gives them substantial market power, is their ability to raise funds at lower costs. Larger banks have better credit ratings, and as a result, investors and depositors are willing to lend them funds at lower rates. In part, these credit ratings can reflect the ability of larger banks to hold more diversified lending portfolios. However, these ratings also benefit from explicit and implicit government guarantees, such as being considered ‘too big to fail’. Their lower costs of funding enable the bigger banks to maintain their profits and offset some of the increases in their costs resulting from regulatory change, which may prove more difficult for smaller institutions.

Larger operators also benefit, to an extent, from integration, which gives them the ability to exert additional control over some markets. Vertical integration allows larger institutions to have more control over the costs of their inputs, while smaller entities rely on third parties to access funding markets and other types of services. In effect, small ADIs compete against the major banks, but also depend on them to access the funds that allow them to continue competing. Cross-product (conglomerate) integration gives the larger institutions the opportunity to cross subsidise some of their products, and also offer consumers an integrated bundle of services, which may help to lock customers into the provider and raise customer switching costs.

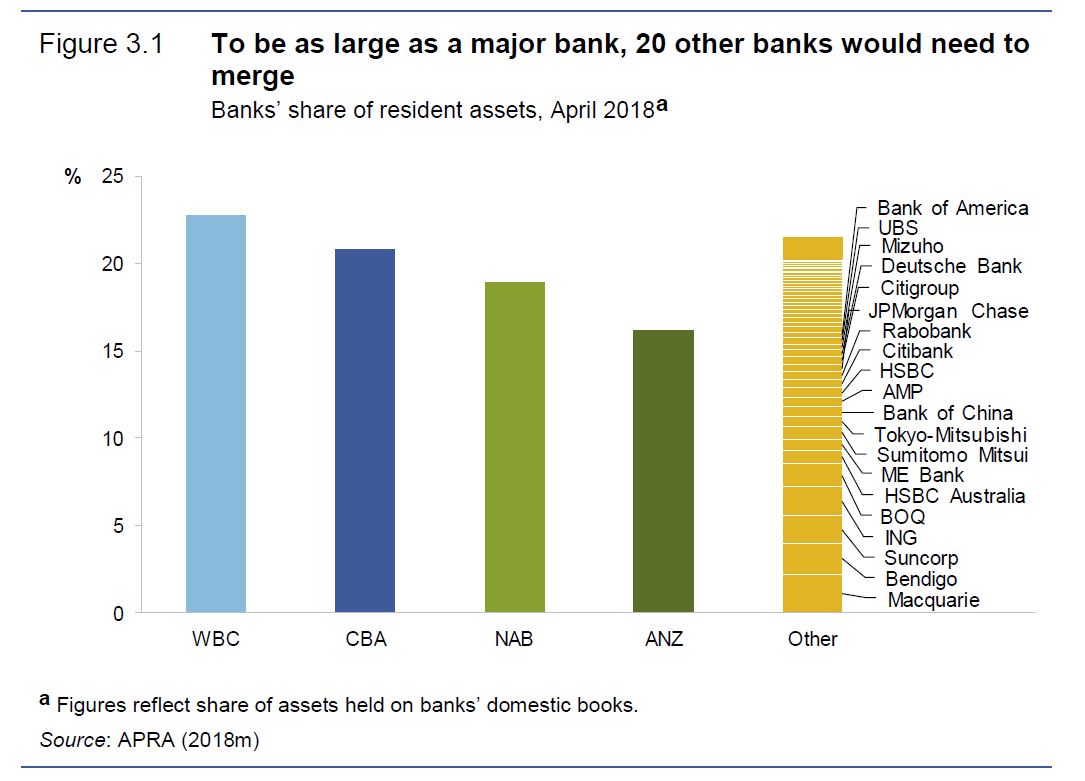

Despite the consolidation of some smaller players, the major banks still maintain substantial market power — because the difference in size between them and the other providers in the market is exceptional. Based on the value of their assets in April 2018, ANZ (the smallest of the majors) was seven times bigger than Macquarie, the next bank by size of assets. Twenty banks (ranking 5th to 24th by size of assets) would need to merge in order to match ANZ. Only if all banks in Australia, other than the big four, merged would they be able to rival the biggest two — Westpac and the CBA.

An important aspect of banks’ size is their geographical reach, either through branches or other distribution networks. In 2017, there were about 5300 bank branches, over 390 credit union branches and 74 building society branches. The major banks accounted for 60% of all branches, and only two other ADIs (Bendigo and Adelaide Bank and Bank of Queensland) had branches in every state and territory. Major banks are also strongly represented in other distribution networks, such as mortgage brokers.

At the same time, customer satisfaction levels reported by individual banks, including the major banks, remains high. While consumers may be disillusioned with the banking system, it seems they are satisfied with their chosen institution. Of course, consumers may not always be aware of the alternative services and prices available from other institutions — or even their own institution — that may be more suitable for their circumstances.

Australia’s major banks have some of the strongest business brands in our economy. Industry estimates put the value of their brands between $6 and $8 billion, with CBA having the highest brand value. Their public image has been affected by a series of scandals and the continued community perception that they do not operate in their customers’ best interests

The major banks benefit from the perception that they are safe, stable institutions, and that the government will step in to help them if needed. This supports their existing market power, and in some cases increases it further — during the global financial crisis (GFC), consumers transferred some of their savings to the major banks, as they were perceived as safer. Even when no financial crisis looms, small institutions may find it difficult to attract consumers from rivals that are perceived as safer. This is despite the fact that retail deposits benefit from the same government guarantee, regardless of ADI size.

Consumer behaviour may also contribute to market power; the low levels of consumer switching and a general disengagement from financial services help ADIs maintain their position in the market, and make it harder for new competitors to gain any significant market share.

The major banks benefit from a substantial asset base and stable market shares, which give them the ability to cope more easily with regulatory change, while also investing and innovating — which in turn can contribute further to their market power. Small institutions argue that their regulatory burden is disproportionately large. For some, the pace and extent of regulatory change has left them limited resources to increase market share.

Measures introduced by the Australian Government and APRA are intended, in part, to offset the cost advantages of large banks — examples include the major bank levy and potentially the specific prudential regulation imposed on domestically significant banks, which applies to the big four banks. It has been argued by Government that when such regulations raise the costs of the major banks, they may help smaller competitors.

But the PC says the objective of competition policy is not to assist some competitors by adding burdens to others, but rather to have the least necessary intervention that is consistent with allowing choice and innovation to meet consumer interests in an efficient manner. Viewed simply, to raise the cost of businesses that have market power — while doing nothing to address adverse use of that market power — risks seeing those costs imposed on customers.

They conclude that the major banks benefit from advantages of scale, scope and branding which give them substantial market power and the ability to remain broadly insulated from competitive threats posed by smaller incumbents or new entrants. They concluded that this balance of power gives the major banks the ability to pass on cost increases and set prices that maintain high levels of profitability — without losing market share.

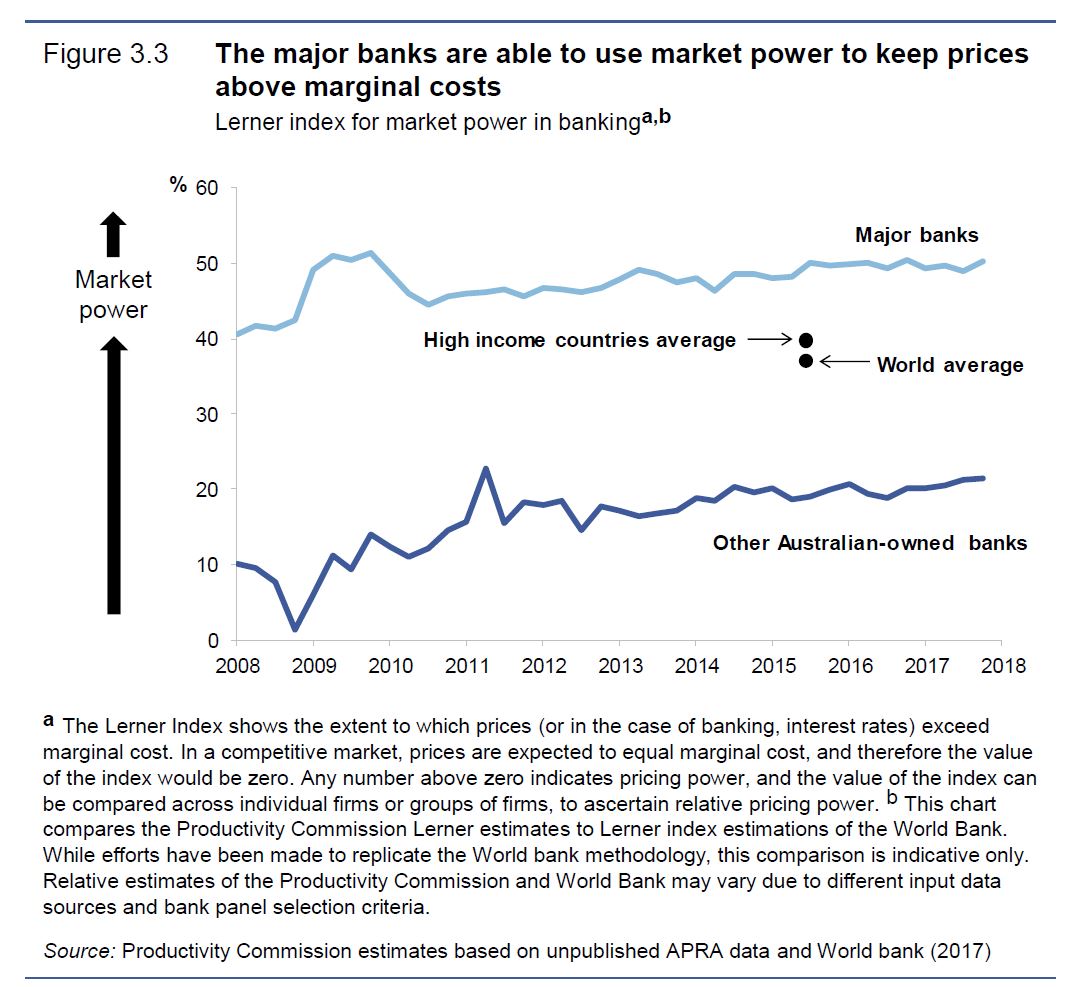

While high concentration on its own is not necessarily indicative of market power resulting in inefficient pricing or (tacitly collusive) oligopolistic behaviour and the major banks have all argued that vigorous competition in the banking system is evident in a number of market outcomes, their analysis shows that major banks are the dominant force in the market. As a result, they are able to charge higher premiums above their marginal costs, compared with other institutions. Approximately half of the loan price that major banks charge is a premium over the marginal cost — double the margin that other Australian-owned banks have.

In fact, they say, over the past five years, changes to prudential regulations have increased the cost of funding for the major banks. However, and as has been anticipated by regulators, they have been able to recoup these higher costs by increasing interest rates for borrowers. According to the ACCC, the big four banks tend to disregard the pricing decisions of smaller lenders — rather, they focus on the expected reactions of the other majors and any changes they may make to interest rates. As a result, each of the banks examined by the ACCC ‘generally aim to set their headline variable rates to broadly align with the big four banks’ . The major banks view this behaviour as an attempt to compete and maximise their profits — but the end result from a consumer point of view is non-competitive pricing. The lack of price competition is reinforced by obfuscation. The prices that ADIs advertise are often not indicative of what consumers actually pay, as we discussed the other day.

The PC concludes that oligopoly behaviour and the ability to use market power adversely are evident Indeed, the major banks themselves are unable to identify competitive threats in the domestic markets, and they focus on large technology companies overseas as their future potential competitors. Such threats have yet to eventuate, and will in any event need to exist in the regulated environment that consciously limits rivalrous behaviour. Whilst the ‘tail’ of smaller providers aims primarily to match the major banks in their pricing, they are subject to similar or, at times, more costly regulation and do not benefit from the funding or efficiency advantages of the major banks, so they are often unable to offer prices that are substantially lower. Some of the smaller banks, in particular foreign institutions, operate in niche markets (such as agribusiness) where they can potentially benefit from specialisation and set prices that reflect their capacity to price discriminate. Others, such as credit unions and other mutually owned institutions, are consolidating in order to benefit from economies of scale. But in the market for retail banking services, it is the major banks that dominate, and other players follow their lead.

So, standing back, the Big Four are dominant, exert structural market power to the detriment of their customers and the broader society. We are paying through the nose to bolster their profitability. Something needs to change. I will share my own thoughts in a subsequent post.

Yesterday’s royal commission hearings began with a ruling by commissioner Kenneth Hayne on NAB’s application to prevent seven documents from being published.

The ruling came after a fiery exchange on Wednesday afternoon in which an angry commissioner Hayne warned NAB counsel Neil Young not to “direct” NAB witness Nicole Smith.

One of the seven documents ruled on yesterday was a document from ASIC entitled ‘Outline of Suspected Offending by the NAB Group’.

“The parts of the document for which the direction is sought concern ascertaining the extent of the charging of fees for no service and what approach should be adopted for compensating those who have been charged,” said the commissioner.

Mr Hayne said he would need to weigh up the “balance” between the interest of an individual, the public interest, and NAB’s legitimate desire to protect private commercial interests.

“In attempting to strike the balance that is to be drawn between those competing elements, it is to be noted that it would be in the interests of NAB to pay the least sum available by way of remediation,” Commissioner Hayne said.

“It would be in the interests of persons charged fees, in circumstances where no service has been provided, to be provided with adequate compensation.

“It is in the public interest that there be an open and transparent inquiry about how both the regulator and the regulated deal with the issue of remediation,” he said.

For those reasons, said the commissioner, “the application for non-publication is refused”.

Counsel assisting Michael Hodge then stood up at the bench to reject comments by Mr Young on Wednesday afternoon that “might be taken to be an implicit criticism of the staff of the royal commission”.

“You were also told, commissioner, in relation to the outline of contraventions from ASIC that I was taking Ms Smith to, that the National Australia Bank had not been notified that this document would be the subject of publication. That is incorrect,” Mr Hodge said.

“There was no fault on the part of the staff of the commission or the solicitors assisting the commission, and that everything has occurred in accordance with the practice guidelines that have been published by you in February of this year,” he said.

Mr Hodge went on to describe the tardiness with which NAB had supplied documents requested by the royal commission.

NAB produced 31 documents on 9 July 2018 following a request by the commission for documents relating to NULIS and ‘fees for no service’, said Mr Hodge.

“After that date, the National Australia Bank produced in excess of three and a half thousand documents regarding the ‘fees for no service’ issue, of which in excess of 3000 were produced to the commission last week,” he said.

In respect of the seven ASIC documents commissioner Hayne ruled on yesterday morning, four were produced to the royal commission on the afternoon of 3 August 2018 and three were never produced by NAB, said Mr Hodge.

“It may be that, unfortunately, that particular manner of responding to your compulsory notice has contributed to some of the difficulties that the National Australia Bank has faced in dealing with these confidentiality claims,” Mr Hodge said.

Mr Hodge uncovered at least 100 instances of potentially criminal breaches by NAB in his subsequent examination of the seven ASIC documents and his questioning of Ms Smith.

NAB chief executive Andrew Thorburn made a public apology for NAB’s “failure to act with honour” via a video posted on Twitter late on Thursday afternoon.

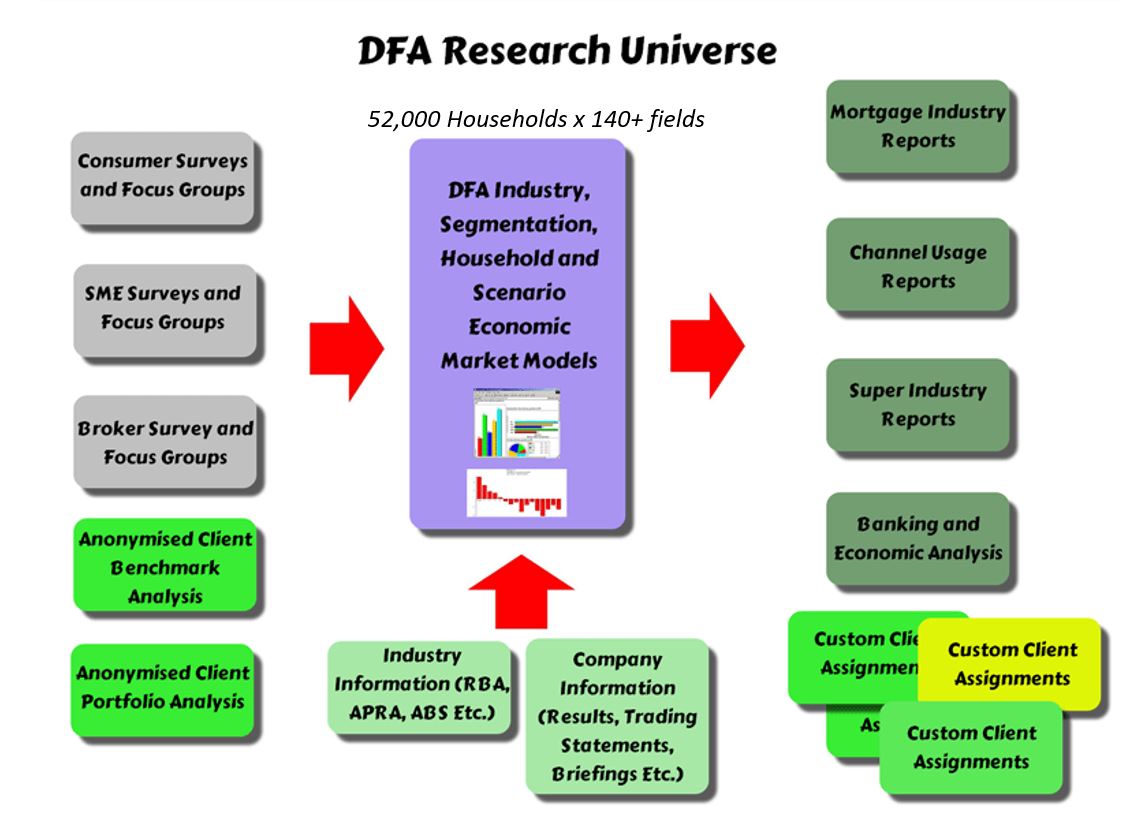

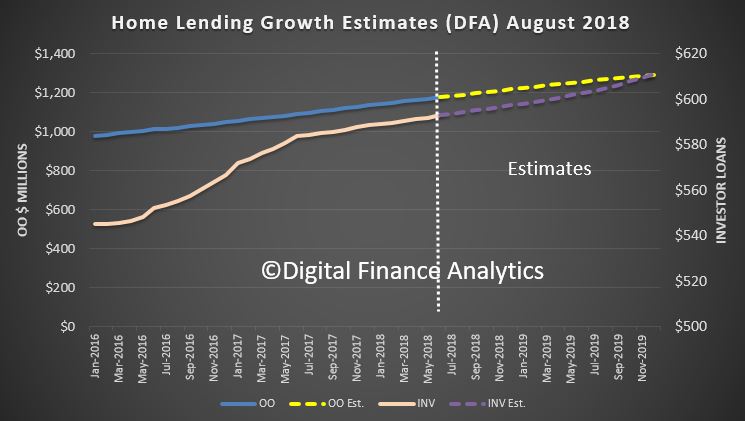

One of my clients asked me to share my thoughts on the trajectory of future home loan growth, in the light of the current market dynamics. We run a series on this in our Core Market Model, and it is updated each time we get data from our surveys, APRA, ABS or RBA.

So I included the data from the ABS in terms of lending flows, factored in deep discounting and rate cuts from some lenders (like ANZ) and the ability of some lenders, like Macquarie, HSBC and some Credit Unions, to fly higher than the APRA imposed cap on investor loan growth.

In fact we run three scenarios, a base case, which we will discuss in a moment, an aggressive growth case, and a lower bounds case. We have assumed no move in the RBA cash rate over the next 18 months, a continued fall in the pressure on the BBSW rate, and some continued momentum from first time buyers. We also factored in the ongoing shift from interest only loans to principal and interest loans, and appetite for finance from some household sectors, especially those seeking to refinance, including those seeking to assist their offspring to buy via the banks of Mum and Dad. Our model has been tracking close to the RBA data in recent months, so we are pretty confident about the trends. But it is only a projection, and it will be wrong!

The first chart shows the overall value of housing loan portfolios, split between owner occupied and investor loans. The astonishing momentum in investor lending up until mid 2017, when APRA’s new regulations kicked in, eases back, and the current growth in investor loans portfolios is pretty flat. In fact we expect a small rise in the months ahead, as some non-bank lenders have to compete harder with the APRA “approved” lenders who can go above the cap. Remember though lenders still have tighter underwriting standards than before, so there is not going to be a massive resurgence in my view, at least until the Royal Commission reports. Owner occupied loans will continue to lift, as first time buyers are still active, and attracted by the lower property prices.

Refinancing of existing loans does continue, though some are having difficulty finding a loan, as we discussed yesterday.

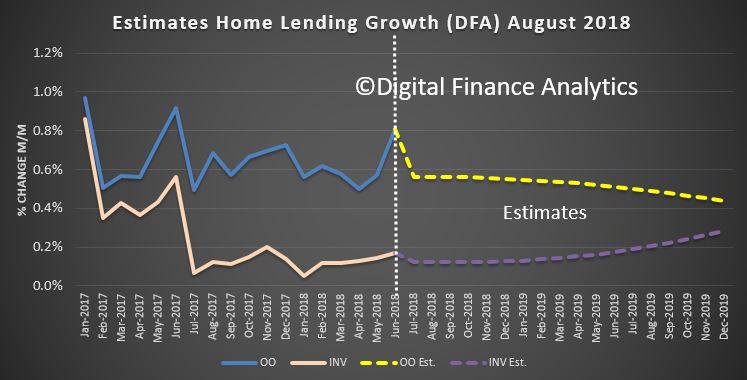

Turning to the percentage change, our base case is for a slow rise in investor lending and a slow fall in owner occupied loans, with an overall growth still well above inflation at between 5-6%.

This suggests that the lenders will need to compete hard for business which is available, continue with more rigorous loan assessments and manage tighter margins as a result.

As a result, we think property prices will continue to go lower through 2019, but does not as yet signal a crash.

This could all change if funding costs go higher, or the banks get slugged with more costs relating to poor practice, or even face criminal cases relating to charging fees for no service, or making unsuitable loans to borrowers.

As a result there is significantly more downside risk than upside gain at the moment. Our worst case scenario actually sees the overall lending portfolio shrink. If this were to happen, then all bets are off, and we must expect significantly more property price falls through 2019. Actually we do not think, as some are saying, that the worst is over. Rather its just the end of the beginning!

Leader of the Australian Greens Dr Richard Di Natale and Treasury Spokesperson Sen. Peter Whish-Wilson have unveiled a proposal for a sweeping overhaul of our banking and financial services sector, as well as the regulatory and governance system underpinning it. Simply put: it’s time to break up the banks.

“The Hayne Royal Commission has proven that the foundations of our banking and financial system are rotted through. It’s past time we stopped letting these huge corporations get away with fraud, bribery and other systemic abuses of the customers they are supposed to serve,” Di Natale said.

“The Greens led the charge to establish a Royal Commission into the banking sector and we are the only party with a real, simple solution to the abuses it has uncovered: break up the banks.”

“It’s time that banks became banks again. Australians are sick and tired of these massive financial institutions getting away with murder because they can throw stacks of money at the two old political parties. Our banks should be working for us, not against us and this policy will make sure that happens.

Under the Greens proposal:

Banks will no longer be able to own wealth management businesses that both create financial products and spruik them to unsuspecting customers.

Consumers will be able to easily distinguish between the simple and essential products and services that the vast majority of Australians use—deposits and loans, superannuation and insurance—and the more complex and selective activity that is the domain of big business, the wealthy, and the adventurous.

By removing hidden conflicts of interest, Australians will be able to trust that the advice they’re getting from their banker is designed to line their own pocket, not the other way round.

The watchogs have failed. We would strip ASIC of its responsibility for overseeing consumer protection and competition within the essential services of basic banking, insurance and superannuation and return them to the ACCC.

“I have been grilling the banks and ASIC in Senate Inquiries for five years and have come to the conclusion that fiddling around the edges isn’t going to change things. ASIC is just too close to the banks and is more interested in keeping the financial sector happy than it is in protecting consumers,” Whish Wilson said.

“This policy is about putting consumer welfare back in as a primary objective of how we regulate our banks. The Howard and Keating deregulation agenda put the banks first and these reforms are about putting the people first.

“We need to break up the banks so they are no longer too big to regulate. We have to strip consumer protection powers over the banks from ASIC and APRA and give them to the ACCC. We need to have a regulator that is interested in policing the banks and pursuing justice when wrongdoing occurs, not one that issues speeding fines for highway robbery.