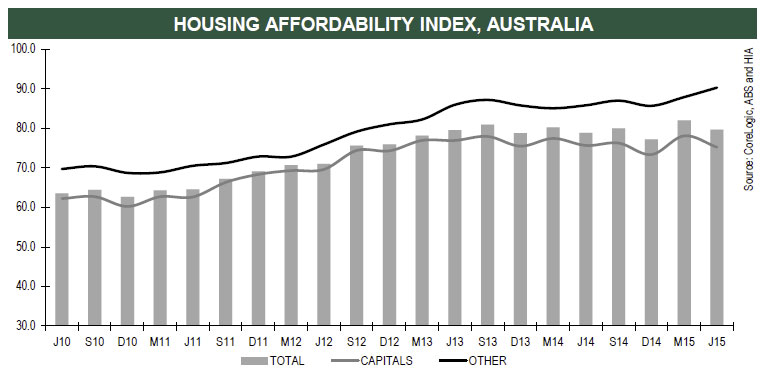

The HIA Affordability Index fell in the June 2015 quarter, signalling a deterioration in affordability conditions, said the Housing Industry Association industry.

“The positive impact of a second interest rate cut for the year in May was overwhelmed by an increase in the CoreLogic RP Data median dwelling price and the persistence of sluggish earnings growth,” said HIA Chief Economist, Dr Harley Dale. “The net negative impact of these factors saw the national HIA Affordability Index fall by 2.9 per cent to 79.7 in the June 2015 quarter.”

“The national affordability result masks wide variations around the country, an unsurprising finding given the lack of geographical consistency to the current residential cycle,” Harley Dale said.

During the June 2015 quarter, affordability deteriorated by 3.6 per cent in capital city markets, driven by Sydney and Melbourne. This was in stark contrast to a 2.7 per cent improvement for regional Australia. Compared with the June quarter last year, capital city affordability worsened by 0.6 per cent, while in regional Australia affordability saw a 5.2 per cent improvement.

“The large differences in the results for the capital city Affordability Index and its regional counterpart, together with the variation in outcomes between capital cities, exposes the folly of sweeping generalisations which refer to an Australian housing boom,” said Harley Dale. “That is simply not what is occurring – in many parts of Australia the extremely low interest rate environment is delivering historically favourable affordability conditions.”

“It is against this backdrop that authorities have escalated their requirements for the rationing of credit to residential investors. The risk is that this will obstruct new housing supply, aggravating affordability conditions in markets around Australia,” concluded Harley Dale.

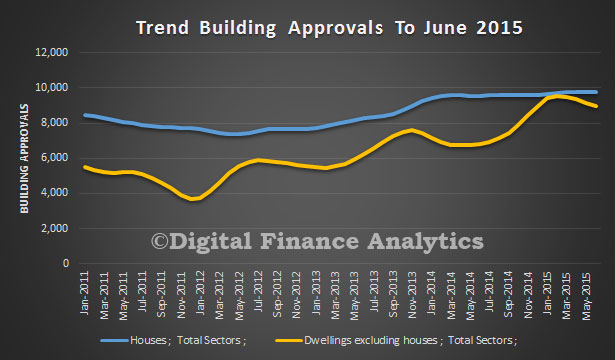

Australian Bureau of Statistics (ABS) building approvals show that the number of dwellings approved fell 1.2 per cent in June 2015, in trend terms, and has fallen for four months. The fall in unit approvals was the reason, confirming a continued slow down.

There were some significant state variations.

Dwelling approvals decreased in June in South Australia (4.1 per cent), New South Wales (2.9 per cent), Victoria (1.8 per cent) and Western Australia (0.4 per cent) but increased in the Australian Capital Territory (14.6 per cent), Northern Territory (8.7 per cent), Queensland (0.2 per cent) and Tasmania (0.1 per cent) in trend terms.

In trend terms, approvals for private sector houses were flat in June. Private sector house approvals rose in New South Wales (2.0 per cent), Queensland (0.3 per cent) and South Australia (0.2 per cent) but fell in Victoria (1.3 per cent) and Western Australia (1.0 per cent).

The value of total building approved fell 0.9 per cent in June, in trend terms, and has fallen for four months. The value of residential building fell 1.0 per cent while non-residential building fell 0.6 per cent in trend terms.

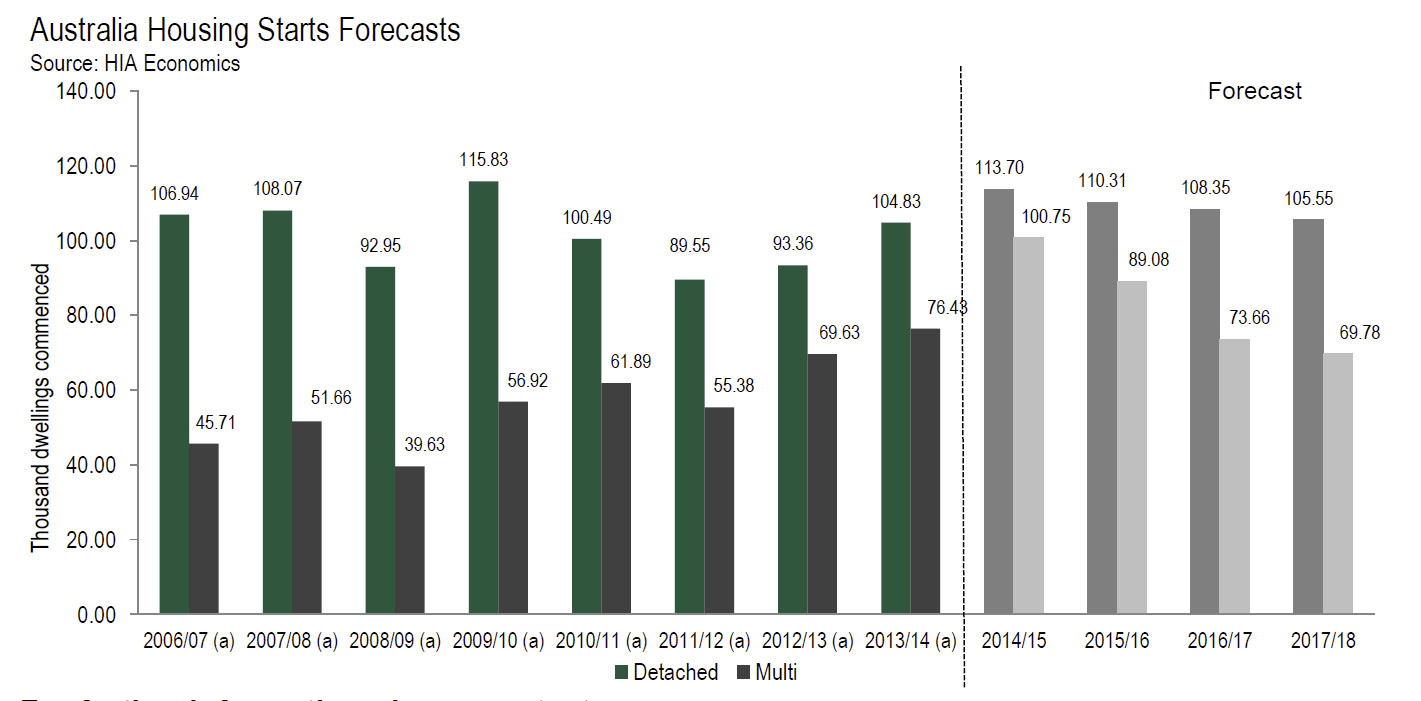

New home commencements have peaked, but will remain at a very high level in 2015/16 according to new analysis from the Housing Industry Association (HIA). “It is likely that new dwelling commencements peaked at a record level of 215,000 in the financial year just passed, and indeed the risk is for this apex to be even higher,” said HIA Chief Economist, Dr Harley Dale. “This is an extraordinarily high level which is 15 per cent above the previous cyclical record of 187,000 dwelling commencements achieved in 1994.”

HIA expects a cyclical peak of nearly 214,500 new dwelling commencements for the 2014/15 financial year, although there is the risk that the 2015 calendar year delivers an even higher record. It is expected that both detached house and ‘multi-unit’ commencements have reached cyclical highs, but a further surge in unit construction could yet deliver a 2015 calendar year peak. Detached house commencements are expected to have reached a level of 113,700 in 2014/15, 9 per cent above the long term average. Multi-unit construction has shot the lights out, hitting a level 117 per cent above the long term average with the number of commencements expected to reach 100,747.

“The approaching down cycle is likely to be considerably smaller for detached house commencements than for multi-units. Governments’ policy failure means that there is unrealised demand for new detached housing due to a range of supply side constraints led by a lack of shovel ready land,” concluded Harley Dale.

In 2013 alone, more than 500 houses were demolished in Nashville, Tennessee, a sharp increase from previous years. And hundreds of additional teardowns are expected in a city that’s projected to add a million residents over the next two decades.

Nashville is hardly the only North American city to experience a recent wave of teardowns. In Vancouver, a housing and real estate expert reports that the city issued more than 1,000 demolition permits in 2013. She points out that most of the demolitions are of single-family homes, and each sends “more than 50 tonnes of waste to landfills.”

While preservationists have long decried the loss of historic fabric and cultural capital through teardowns, the environmental costs of demolition are increasingly coming to the fore.

A waste of energy and a waste of space

The negative environmental consequences of teardowns are manifest. According to the Chicago Metropolitan Agency for Planning (CMAP), demolition and construction now account for 25% of the solid waste that ends up in US landfills each year. Further, when a building comes down and its materials are hauled off to the dump, all the energy embedded in them is also lost. This consists of all that was expended in the original production and transportation of the materials, as well as the manpower used to assemble the building.

As CMAP explains, “examining embodied energy helps to get at the true costs of teardowns and links it to issues of air pollution and climate change (from the transport of materials and labor), natural resource depletion (forests, metals, gravel) and the environmental consequences of extracting materials.”

Often, a more environmentally friendly, quaint home is “replaced by a very expensive, much larger house, which is frequently left vacant.” Meanwhile, in the most desirable cities, in their tony suburbs, and in popular resorts, investors park their assets in “McMansions” that are sporadically occupied.

Additionally, bigger houses necessarily encroach upon open space. Not only does expansion entail the uprooting of mature plantings – which benefit air quality – but it also eliminates trees that can provide shade and minimize energy required to cool buildings in warmer months.

Urban facelifts erase more than crumbling buildings

In city neighborhoods, opponents of demolition will often cite the loss of historic character.

Advocates for development, on the other hand, frequently argue that demolition rids cities of decrepit, obsolete houses, paving the way for multi-unit developments. In this sense, cities can become more efficient with their limited space, avoiding suburban sprawl while alleviating the long, traffic-snarled commutes of those who travel to the city.

In many cities, however, new construction on the sites of torn-down houses is aimed at attracting relatively affluent young or middle-aged professionals – the demographic that appreciates urban amenities like shops, restaurants and museums.

Time was that a “walking world” – that is, an environment in which services and amenities are available within walking distance of one’s home – was possible for all city-dwellers, regardless of class. Today, in many urban areas, housing in the dense central core is the purview of the rich, and the less affluent are pushed to the outskirts.

As a result, formerly diverse neighborhoods become economically monolithic. Longtime residents scatter as home values – and taxes – are driven up by new construction.

Withering cultural capital

Teardowns also have negative cultural implications.

All houses tell a story: they’re evidence of how earlier generations thought about domestic life and designed spaces to reflect their daily needs. When we demolish them, we lose those crucial traces of the past.

Of course, older houses often cannot satisfy contemporary demands for amenities, and were frequently built on a smaller scale. Modestly scaled houses from the 19th and early 20th centuries – which represent a wide range of architectural styles – are sometimes built out or renovated. But often developers and homeowners opt to (as a “For Sale” sign in my neighborhood recently put it) “scrape the lot.”

For whatever reason, high square footage has become a prerequisite for new homes in the United States, where the average size of a house built since 2003 is more than double that in England. The United States Census Bureau reports that between 1973 and 2008 the average square footage of new houses soared from 1,660 to 2,519, only dipping after the Great Recession.

Small houses aren’t alone in falling victim to the wrecking ball. The Los Angeles Times recently reported on the demolition of mansions in desirable LA neighborhoods that had sold for as much as US$35 million.

Actress Jennifer Aniston has taken a stand against her mega mansion-inhabiting peers, arguing that “The very idea that a building of 90,000 square feet can be called a home seems at the least a significant distortion of building code.”

Even in less supercharged real estate markets, large and well-built homes fall victim to rising land prices that make them more valuable as dirt.

One example is Georgia’s Glenridge Hall, an historic Tudor Revival mansion, which The Georgia Trust, a statewide historic preservation organization, designated a “place in peril” earlier this year.

Featured in films and providing some of the setting for the first season of The Vampire Diaries, Glenridge Hall had been preserved, until recently, by descendants of the original owner. But the architecture and planning firm Duany Plater-Zyberk & Company – darlings of the New Urbanism movement, which advocates for the revival of traditional town planning and walkable mixed-use developments – demolished the building to make way for a new mixed residential and commercial “English Village.”

As I pointed out in my recent book, the builders of Tudor mansions like Glenridge Hall in the 1920s and 1930s attached a great deal of significance to the historic feel of their homes: in famous Tudors like the Virginia House and Agecroft Hall, they went so far as to import materials from actual English Tudors.

Unfortunately, for today’s wealthy builders and buyers, the past carries little cachet. For many, older homes are considered an obstacle rather than a badge of distinction. And when these radical presentists are given free rein to tear down the remains of the past, we all lose.

Author: Kevin D Murphy, Andrew W Mellon Chair in the Humanities and Professor and Chair of History of Art at Vanderbilt University

The HIA-CoreLogic RP Data Residential Land Report to the March 2015 quarter shows price growth accelerating as turnover falls sharply. The residential land price in Australia increased by 4.1 per cent compared with the previous quarter whilst residential land transactions fell by 5.2 per cent compared with the previous quarter. Higher land prices translate to more expensive housing, and is pricing new home buyers out of the housing market as well as capping the construction cycle.

“This is not a good combination – escalating residential land values and a related decline in sales volumes,” said HIA Chief Economist, Harley Dale. “The upcycle in detached and low density housing construction has been strong, without being stellar. The combination of significantly reduced turnover and strong price growth suggests that supply bottlenecks in residential land are intensifying. That is pricing new home buyers out of the housing market and capping the construction cycle at a lower level than would otherwise be the case.”

“The provision of adequate, affordable, shovel-ready land is a crucial element to addressing housing affordability pressures across the residential property market,” said Harley Dale. “More needs to be done to expedite supply in 2015/16. Removing the obstacles to affordable land supply is a core requirement of a successful taxation and federalism white paper reform process.”

During the March 2015 quarter, the residential land price in Australia increased by 4.1 per cent compared with the previous quarter. This represented an increase of 8.2 per cent compared to the same quarter of last year. to be 17.6 per cent lower than the same period 12 months earlier. The March 2015 quarter represents the third consecutive decline in land transactions in Australia.

According to CoreLogic RP Data research director, Tim Lawless, the trend towards fewer land sales has been evident since mid-2013 and is visible across each of the capital city vacant land markets. “The number of vacant land sales peaked over the June 2013 quarter and have since reduced by almost 30 per cent. To see the price of land consistently rising over the same time frame suggests low supply is the main driver of this price growth rather than a slowdown in demand.”

“Higher land prices translate to more expensive housing which is an unfortunate circumstance for those looking to purchase a detached house. Sydney stands out as the most expensive land market with a rate per square metre of $678, followed closely by Perth with a rate per square metre of $664.”

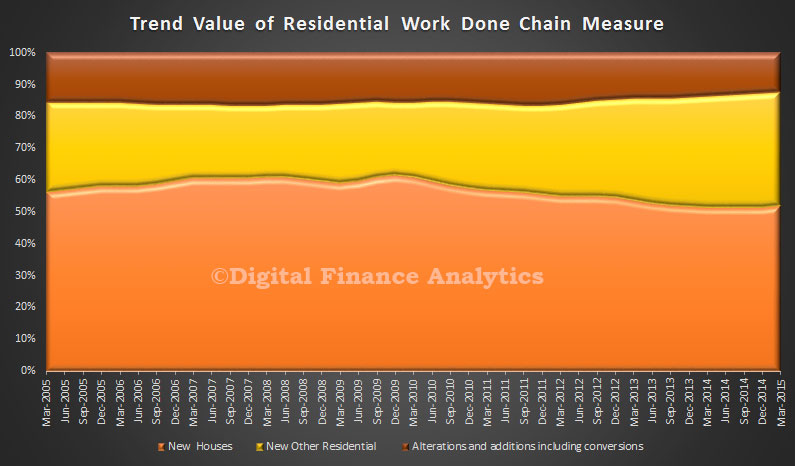

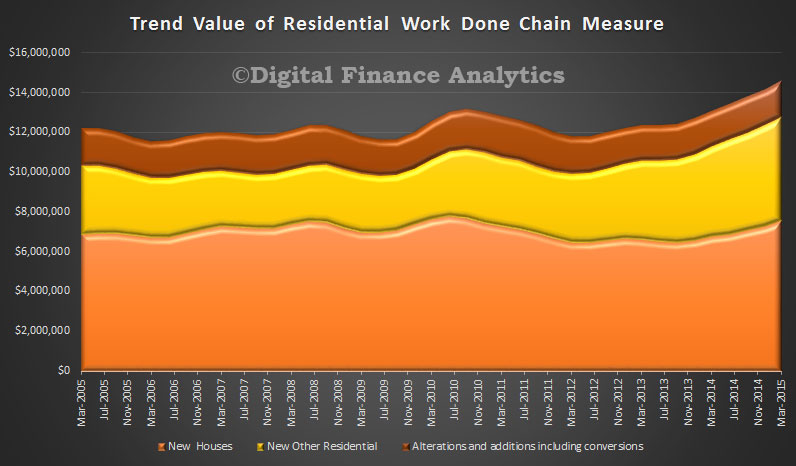

The ABS issued their March 2015 data on Building Activity. The trend estimate of the value of total building work done rose 2.0% in the March 2015 quarter. The trend estimate of the value of new residential building work done rose 3.6% in the March quarter. The value of work done on new houses rose 3.9% while new other residential building rose 3.1%. The trend estimate of the value of non-residential building work done was flat in the March quarter. The most striking trend is the continued relative growth in the value of units, versus houses.

It was a strong result, reflecting the speculative demand for investment property. The data says 53,900 dwellings were commenced during the March 2015 quarter. Units = ‘other dwelling’ commencements (predominantly multi-unit) jumped by 19.2 per cent to 25,140 whilst detached dwelling commencements were steady, increasing by 0.7 per cent in the March 2015 quarter to 28,761. Victoria was a stand out with more than 9,000 multi-unit dwellings started in the quarter, which is a record. In the part year, March 2015, almost 205,000 new dwellings were commenced, and breaking the 200,000 barrier for the first time.

There are some significant state variations, new home starts increased in New South Wales (up by 1.9 per cent), Victoria (up by 18.8 per cent), Queensland (up by 20.9 per cent) and the Northern Territory (up by 12.0 per cent). But there were significant declines, most notably in South Australia, down 18.0 per cent, Western Australia (down by 4.8 per cent), Tasmania (down by 14.7 per cent) and the ACT (down by 14.4 per cent).

The ABS released their data on Building Approvals for May 2015. Using our preferred data view, trend, which irons out some of the variables, the estimate for total dwellings approved fell 0.1% in May after rising for 11 months. The trend estimate for private sector houses approved rose 0.1% in May and has risen for six months. The trend estimate for private sector dwellings excluding houses was flat in May after rising for 11 months. The trend estimate of the value of total building approved fell 0.9% in May and has fallen for three months. The value of residential building rose 0.1% and has risen for 11 months. The value of non-residential building fell 3.4% and has fallen for five months.

Overall levels of approvals are still running higher than anytime this century, thanks to the growth in units, which we this are correlated to the high demand for investment property. High density development is more profitable for builders, and we know demand remains strong in the current low interest rate environment from local and international purchasers. The fall in the AU dollar makes foreign investment even more attractive. However, high volume builds, constructed for profit, will tend to degrade quite quickly, and compliance to building regulations will not necessarily be sufficient to ensure quality long term homes.

Comparing the seasonally adjusted estimate for total dwellings approved rose 2.4% in May following a fall of 5.2% in the previous month. The seasonally adjusted estimate for private sector houses fell 8.4% in May after rising for two months. The seasonally adjusted estimate for private sector dwellings excluding houses rose 16.6% in May following a fall of 16.9% in the previous month. The seasonally adjusted estimate of the value of total building approved rose 2.1% in May following a fall of 3.1% in the previous month. The value of residential building rose 3.3% following a fall of 3.7% in the previous month. The value of non-residential building fell 1.1% and has fallen for two months.

These seasonally adjusted series are too volatile to draw any conclusions, in DFA’s view, though others will I am sure prefer to focus here!

According to the latest ABS data, released today, during May 2015, total new dwelling approvals rose by 2.4 per cent to 19,414 in seasonally-adjusted terms, compared with 18,964 in April. An uplift in multi-unit approvals saw a 15.1 per cent rise during May although detached house approvals fell by 8.5 per cent. A total of 218,442 approvals were recorded in the year to May, which is a new record for approvals over any twelve-month period since records began in 1983.

There were significant state variations with seasonally-adjusted new dwelling approvals strongest increase in Victoria (+11.0 per cent), followed by New South Wales (+8.8 per cent) and Queensland (+3.6 per cent). A slight increase was also recorded in Western Australia (+0.2 per cent). New dwelling approvals fell significantly in Tasmania (-32.6 per cent) and in South Australia (-9.9 per cent).

The HIA New Home Sales Report, a survey of Australia’s largest volume builders, recorded the first decline for 2015 in May. The four month winning streak came to a modest end in May 2015 with total seasonally adjusted new home sales falling by 2.3 per cent. The decline was driven by a 5.1 per cent dip in detached house sales, reflecting weaker monthly demand in four out of the five states surveyed. DFA observes that the rotation from houses to units continues to build momentum, in answer to the demand for investment property, where returns to builders are also higher.

The mature stage of the new home building cycle primarily reflects further momentum in the ‘multi-unit’ sector, together with persistence of healthy conditions in New South Wales and Victoria. New sales of multi-units increased by 7.6 per cent during the month to yet a new record level, with sales volumes up by 26.7 per cent over the three months to May. Meanwhile strength in detached houses sales is evident in NSW and Victoria, with growth in the May 2015 ‘quarter’ of 5.2 per cent and 6.2 per cent, respectively.

In the month of May 2015 detached house sales increased by 3.3 per cent in Queensland, but fell by 2.3 per cent in NSW, 9.9 per cent in Victoria, 5.2 per cent in South Australia, and 8.1 per cent in Western Australia. In the May 2015 quarter, detached house sales increased in NSW (+5.2 per cent) and Victoria (+6.2 per cent). Sales fell over the three month period in SA (-8.1 per cent), Queensland (-7.5 per cent), and WA (-1.3 per cent).

In some states the total tax bill amounts to over 40 per cent of the final price of a new home, taxes on new housing are a brake on economic activity, and represent a constraint on housing affordability and labour productivity.

There is no question that Stamp Duty is one of the key offenders, with research undertaken last year for HIA by Independent Economics identifying it as is the most inefficient tax in Australia’s entire taxation system. As a tax on moving, it discourages households from relocation when this decision may better suit their needs in terms of size, location or employment opportunities. Unfortunately, the economy and the community do not get the best use out of the available housing stock. “However, there are many other taxes on new homes including developer infrastructure levies, which can be over $70,000 on a new house and land package, and which unfairly require new home buyers to fund community assets upfront.

Equally, GST is levied on new homes but not existing properties. Adding tens of thousands of dollars on a new home, GST creates a price differential between new and existing residential properties, which hits affordability, supply, employment and economic activity. Affordability is further eroded by the cascading effect of ‘taxing taxes’, whereby a tax such as stamp duty is levied on an amount that already includes a range of other costs. GST on infrastructure levies alone can add more than $5,000 to the final cost of a new home, while stamp duty on the total GST adds around $3,000. Infrastructure charges, GST and stamp duty add $140,000 and more to the cost of a new home in Sydney, while a plethora of other taxes, levies, fees, changes, rates and duties take the total tax grab to over 40 per cent of a new house and land package.

Taxes add more than $250,000 to the price of a new home in Sydney, accounting for 40 per cent ($1,350 per month) of repayments for the life of a home mortgage. Incredibly, in supplying shelter for Australians, residential building contributes 13 per cent of all GST revenue collected by the Commonwealth. Sadly, that taxation revenue drives up the cost of housing.