The Elephant In The Room Property Podcast is run by Veronica Morgan & Chris Bates. I had a chat with them the other week. Now released as Episode 123 | To buy, or not to buy: that is the question.

Their introduction:

Sensationalist media, conflicting reports and anecdotal evidence, but what does the data say?

After Chris’s numerous appearances on Martin North’s ‘Walk The World’ Youtube channel we finally have brought Martin to our own turf. Martin is the founder of Digital Finance Analytics, a boutique research, analysis and consulting firm, he is one of the most regarded authorities in the research space with several media contributions such as ABC new, AFR and 60 minutes. In this data driven episode, we get down to the question at hand: do you buy or do you sell, what is the data showing, and is it reliable? Find out if people are borrowing too much, what properties are beating the downturn and how are individuals discovering the opportunity.

Here’s what we covered:

How are the 1000 households surveyed every week reflective of Australia?

How did Martin enter into the finance commentary arena?

What patterns are showing which suburbs are going up and which are going down.

How are the 250,000 first home buyers (per year) finding ways to enter the market?

Why newly built properties are at the greatest risk.

How is the data segmented to better reflect real profiles?

Will there be low or high capital growth over the coming years?

Are we reaching our ‘peak debt’?

How many properties are vacant in Australia?

Why is there simultaneous oversupply and undersupply in the market?

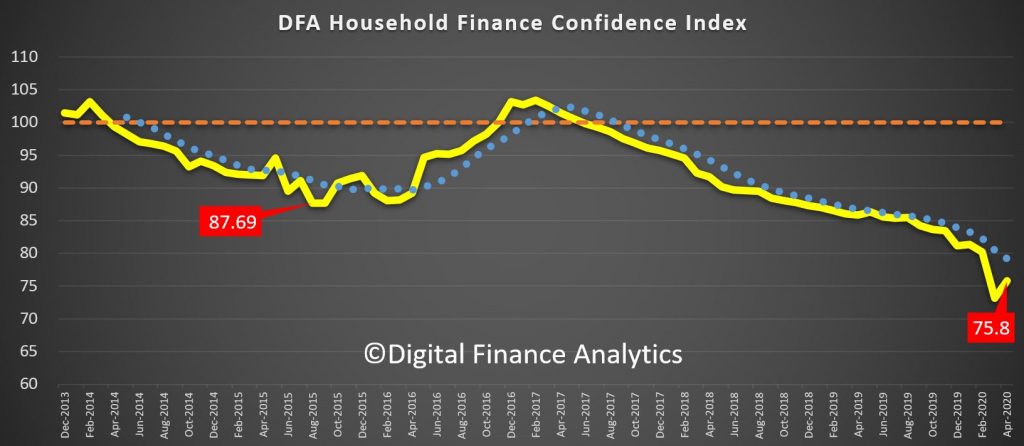

Our latest household financial confidence index improved a little in April, up from 73.2 in March to 75.8 in April. That said, it is still well below the 100 which is a neutral setting, meaning that households are extremely cautious about their finances.

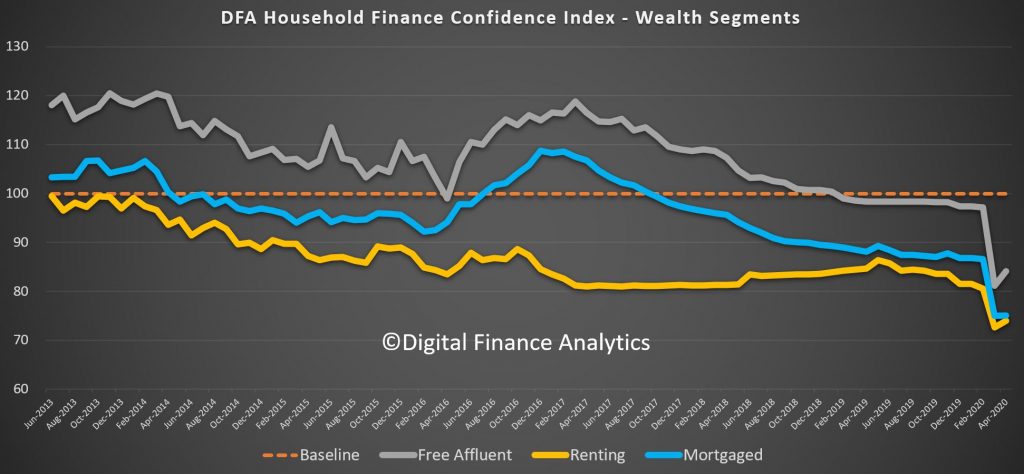

Across our wealth segments, those free affluent households recovered the most mainly thanks to the recovery in stock markets over the past month. Those renting are benefiting from falling rents (though many have income shocks to deal with) while those with a mortgage showed little evidence of a recovery in confidence, thanks to rising debt concerns.

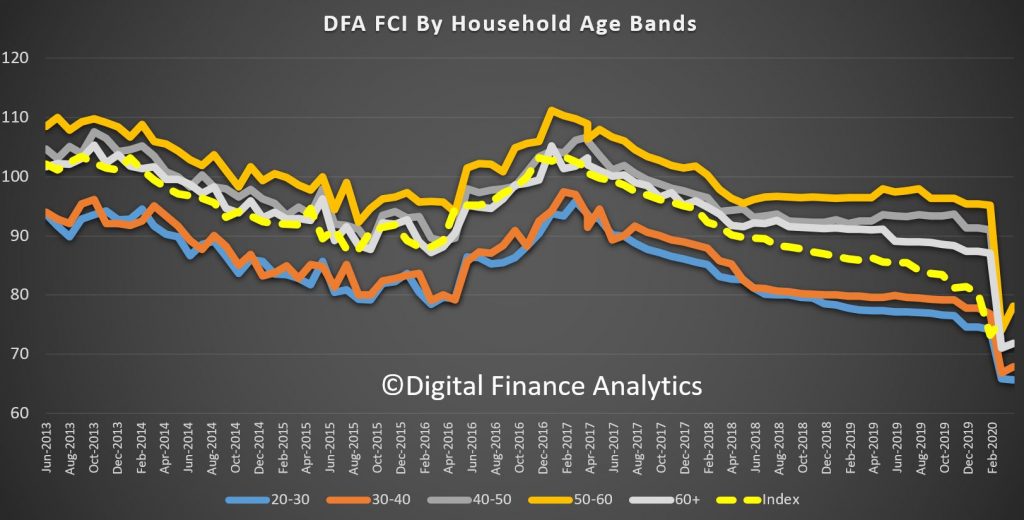

Across the age bands, those aged 50-60 showed the strongest bounce, while those aged 20-30 reported a further fall – not least because younger households tend to be more exposed to zero hour contracts, and part time employment not supported by JobKeeper.

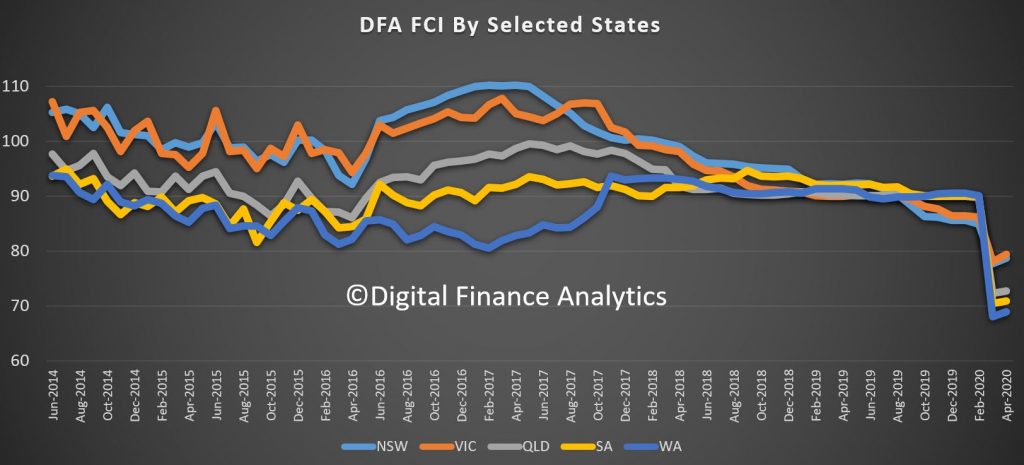

The recovery in confidence was evident across all the states, with NSW and VIC on average more positive relatively speaking than SA and WA.

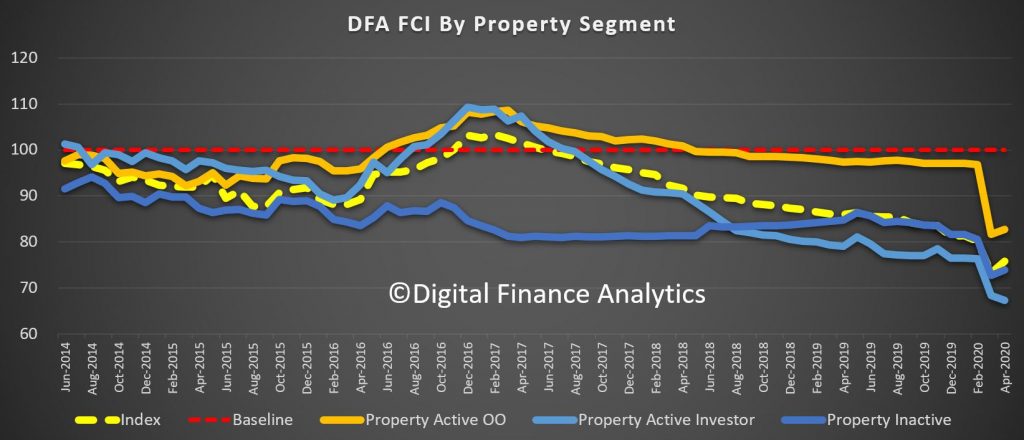

Across our property segmentation, owner occupied households improved, as did those not holding property, but property investors fell again, thanks to less support from banks in terms of mortgage repayment holidays and falling rents and occupancy. Around 8% of property investors are seriously looking to sell their property if they can. More on that in a future post.

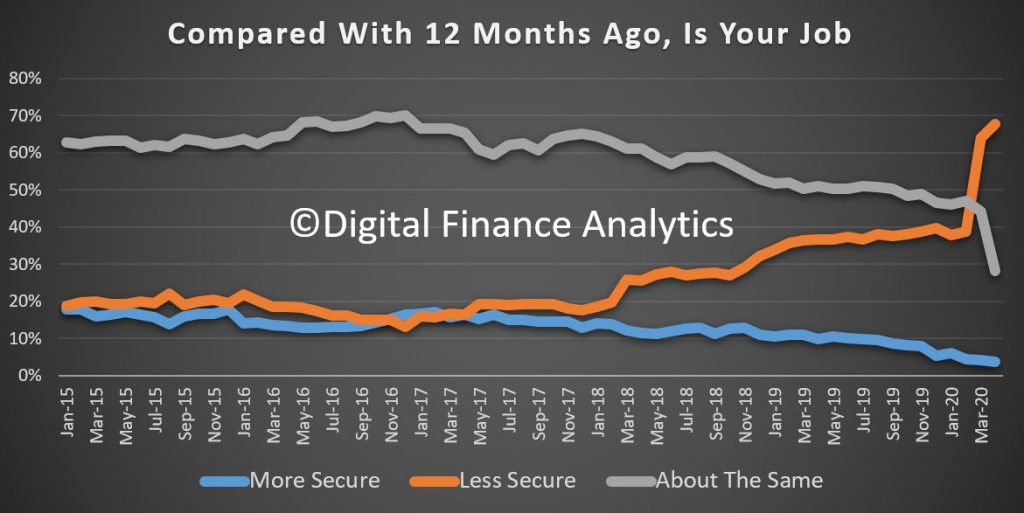

The true state of play is best shown when we look at the moving parts of the index. 67% of households now feel less secure regarding their job prospects than a year ago, a rise of 28% from last month.

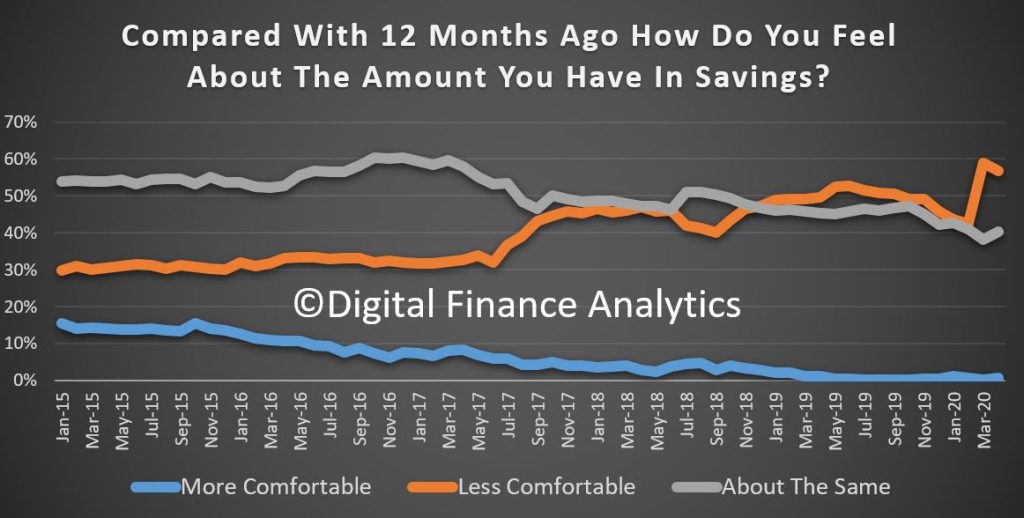

There was a 14% rise in those feeling less comfortable with their savings, to 56% of households. There was a clear intent to try to save more in the months ahead, given current economic uncertainties.

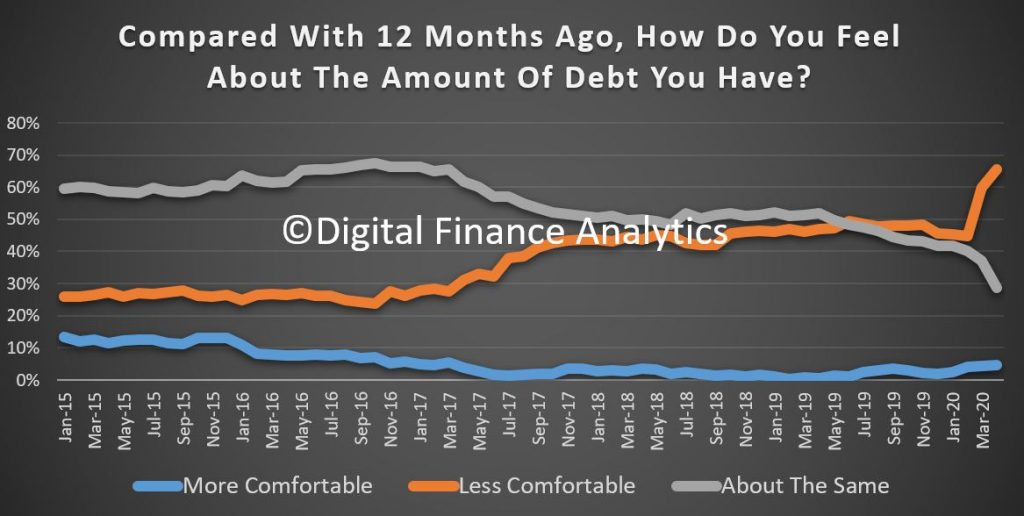

65% of households are less comfortable with their ability to service debt, a rise of more than 20% of households, this despite falling interest rates and bank support schemes. Around $160 billion of loans received some leniency from the banks, but that is a small share of the $1.7 trillion mortgage sector and the $280 billion SME sector.

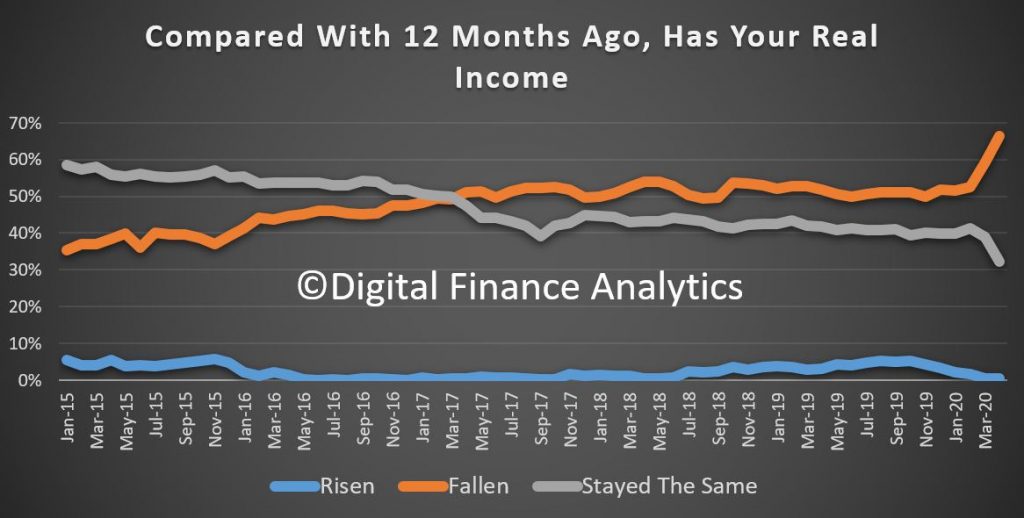

Income pressures are mounting, with 14% saying their incomes had fallen – to 66% of households, while under 1% saw any rise in income – including some who will benefit from higher incomes under JobKeeper than they would normally receive.

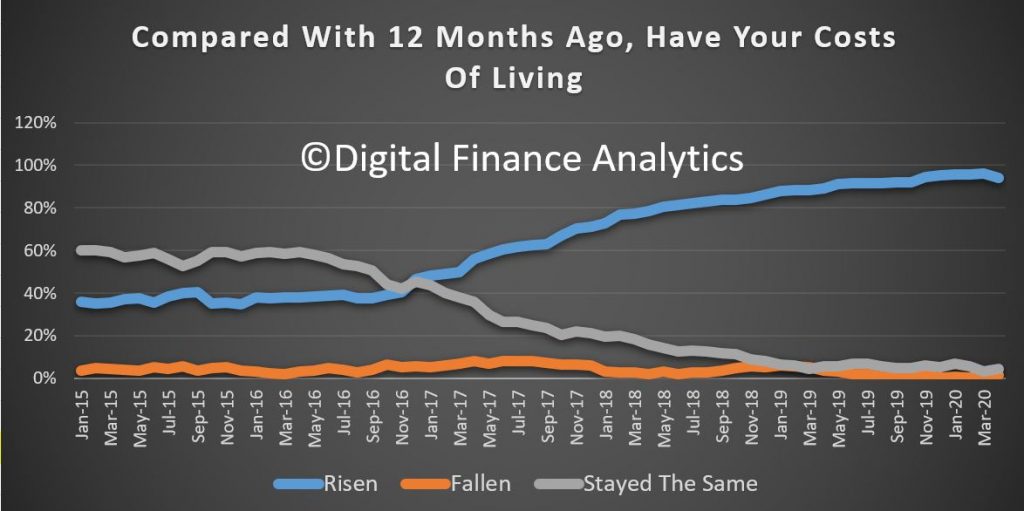

Costs of living continue to drive higher – despite the fall in oil prices – with many households incurring greater costs because they are spending more time at home. 94% said their costs were higher than a year ago.

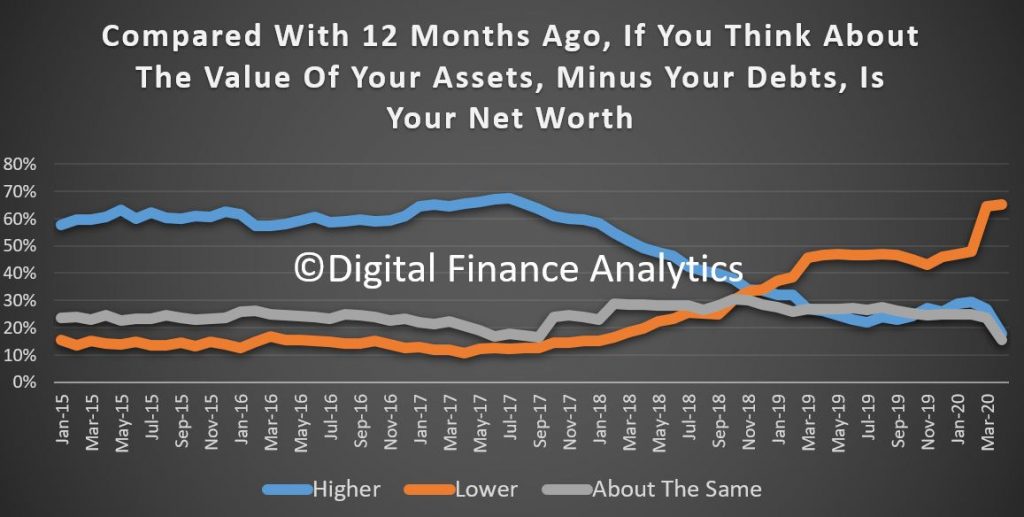

Finally, household net worth was lower for 65% of households, reflecting stock market and property price adjustments, and rising debt levels. There was a drop of 11% in households claiming net worth had risen over the past year to 18%.

So we think the longer terms impacts on households are yet to be fully understood. Certainly, our data suggests households will be cautious, as income pressures, costs of living and rising debts bite. If home prices slide further as we expect they will, then household net worth will put a further brake on the wealth effect and will also adversely impact many households. This does not suggest a V shaped recovery to me.

We started to run some additional questions in our household surveys from January, and have been tracking the spreading impact of the economic shutdown as it spread in response to the virus. Last night we ran a live event where we discussed the main findings and answered questions, but we are also posting some of the analysis today. First here is the show:

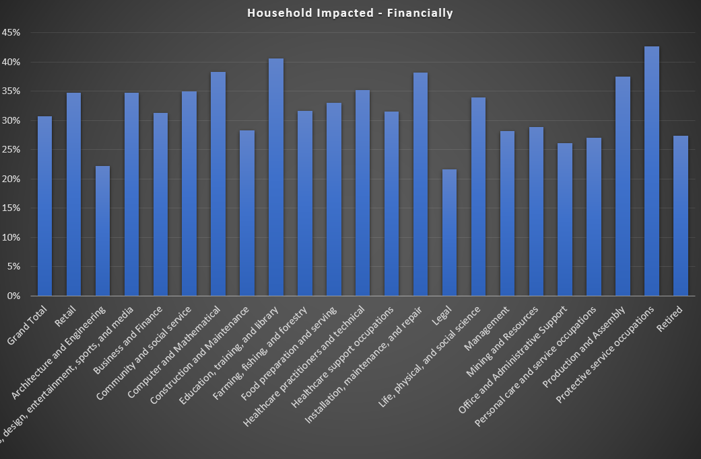

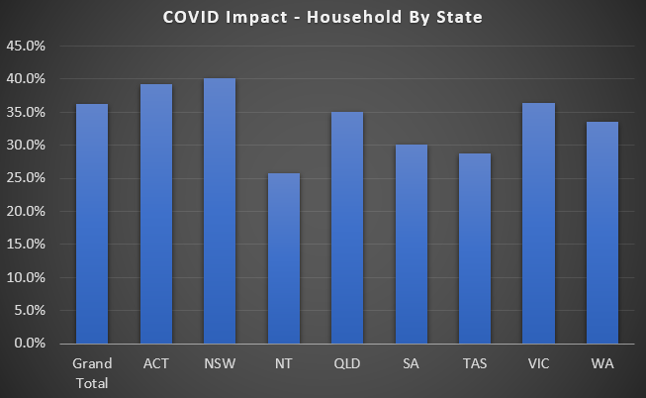

In our surveys we asked two questions. First, have household finances been impacted by the virus/economic slow down, and second, how. Overall 36% of households have been adversely impacted by COVID from a finance perspective. However this does vary by industry, for example, more than 40% of those in education have taken a hit, whereas those in the legal profession are at 20%. Protective services was high, thanks to the closure of transport hubs and other public spaces.

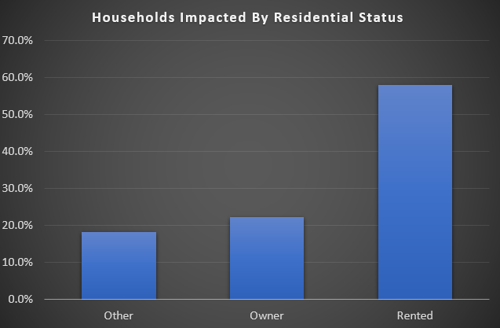

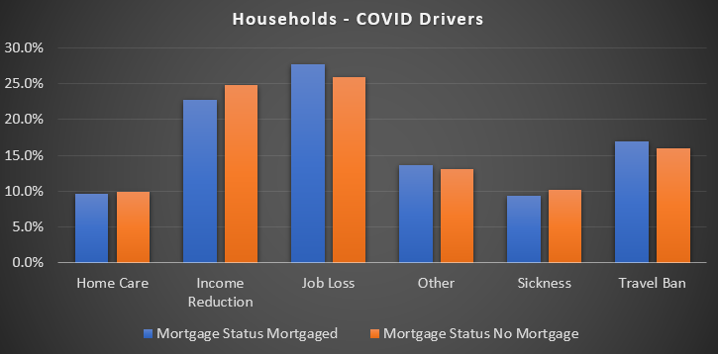

60% of households in rental accommodation have been adversely impacted, compared with 22% of property owners.

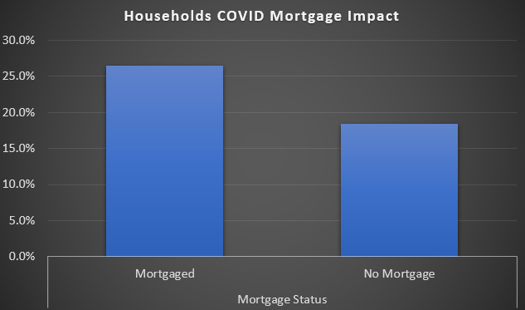

27% of those with a mortgage are impacted compared with 18% of those who are property owners without a mortgage.

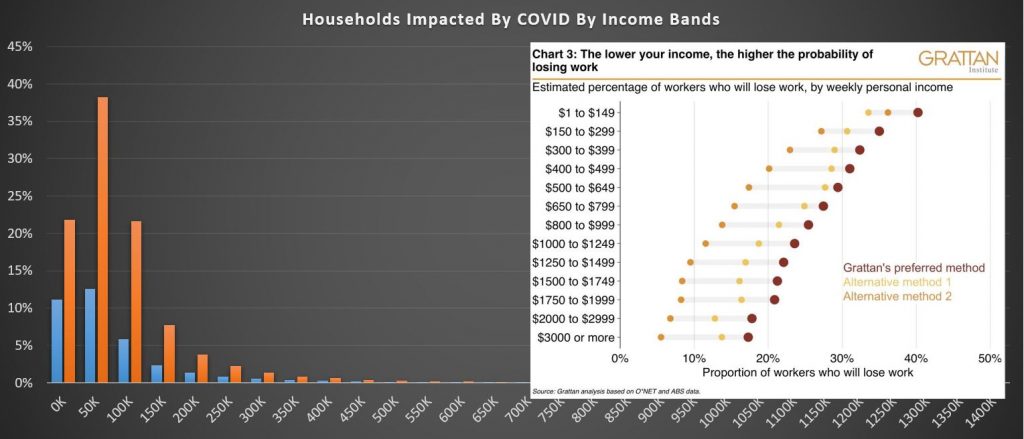

Lower income households are more adversely impacted. Half of those earning less than $50k a year and one third earning between $50-100k are impacted. This is also consistent with Grattan research. This is because many of these jobs are part-time, gig, or zero hours, and lower paid.

There are some state variations, with 40% of households in NSW adversely impacted, compared with 26% in NT. 35% of households in QLD and 37% in VIC are hit, and ACT was above WA, just.

When we examine the nature of the impact, we found that job losses were driving more than 25% of those with a mortgage, followed by income reduction due to less hours, or less pay. There were some differences between those holding a mortgage and those not (though at the margin).

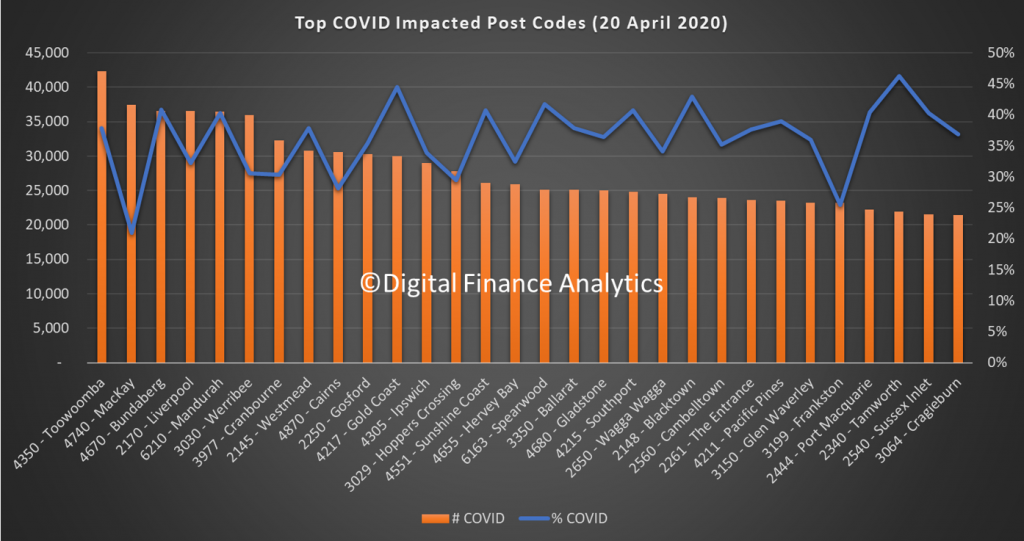

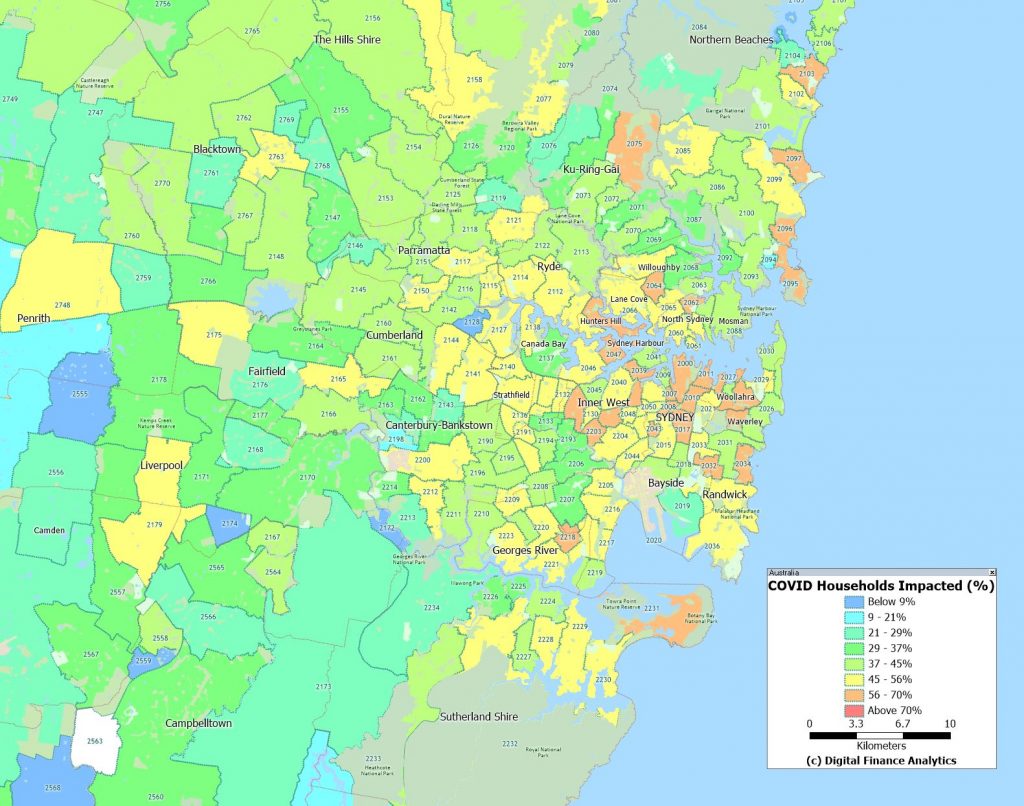

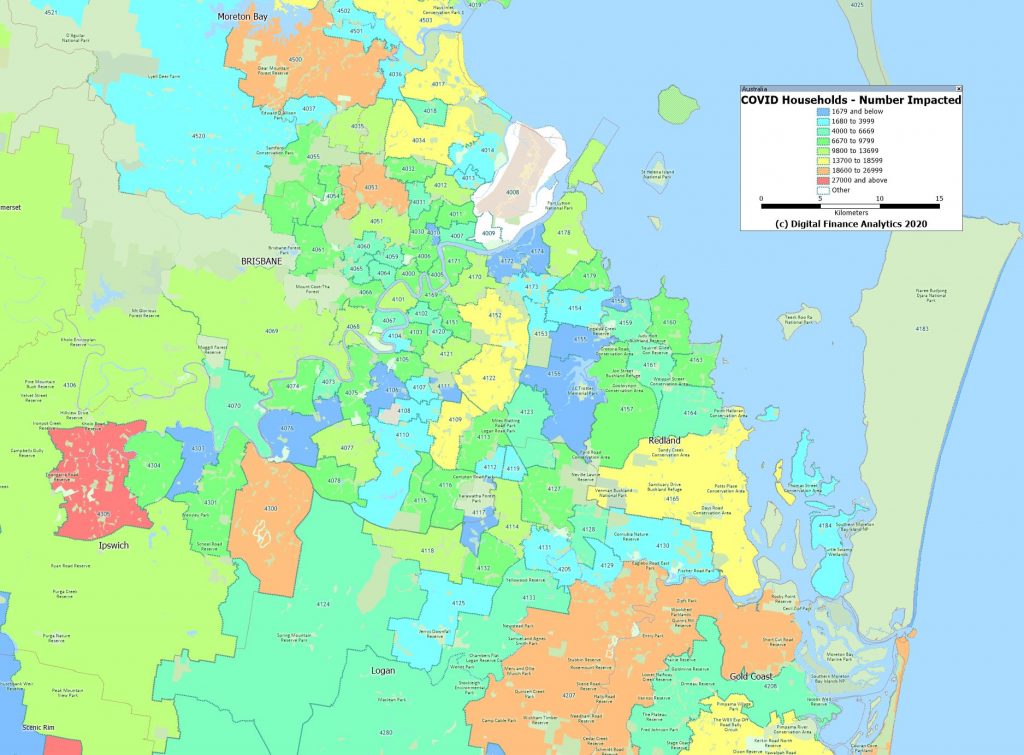

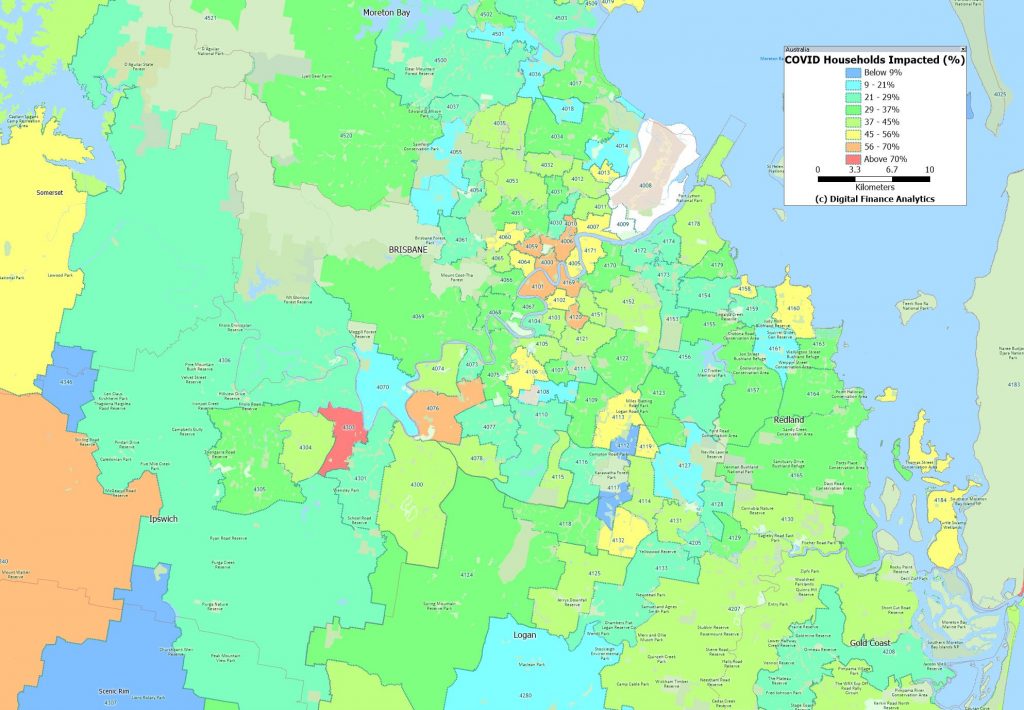

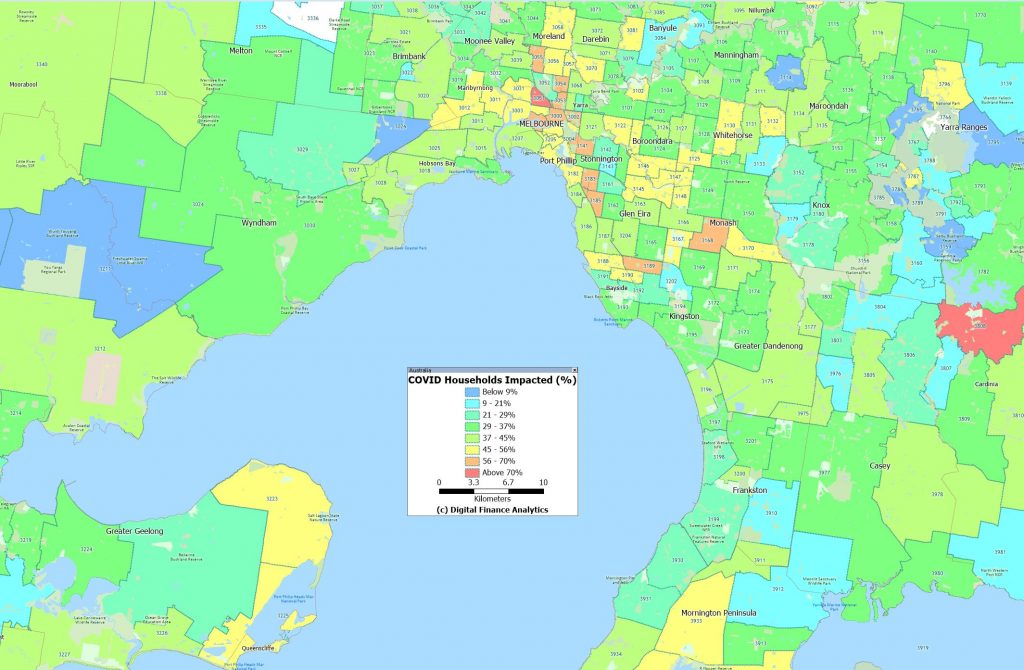

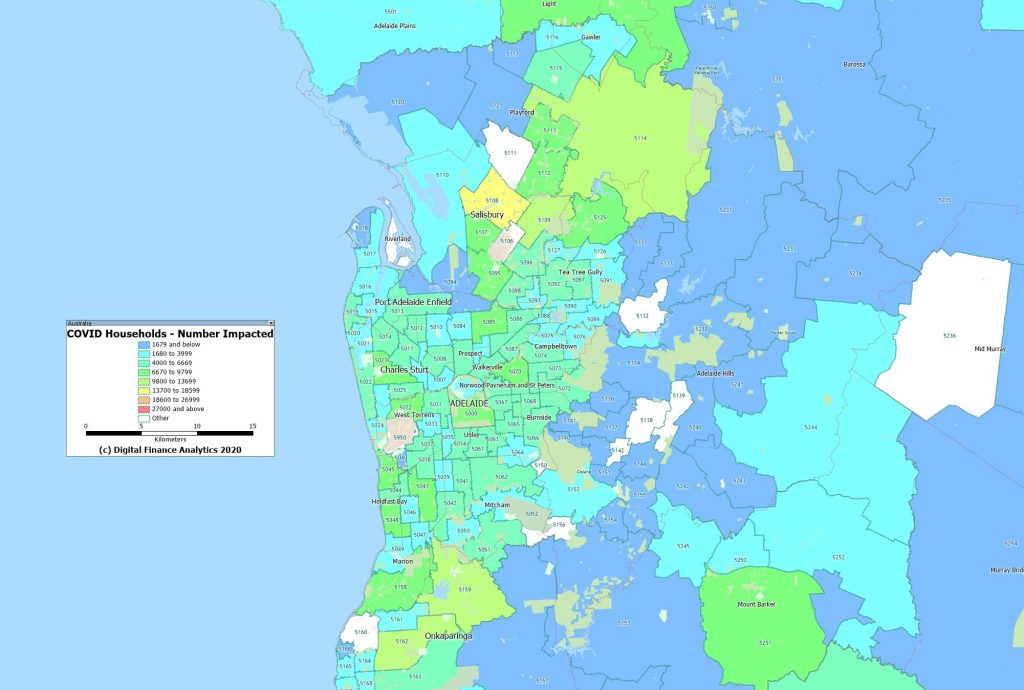

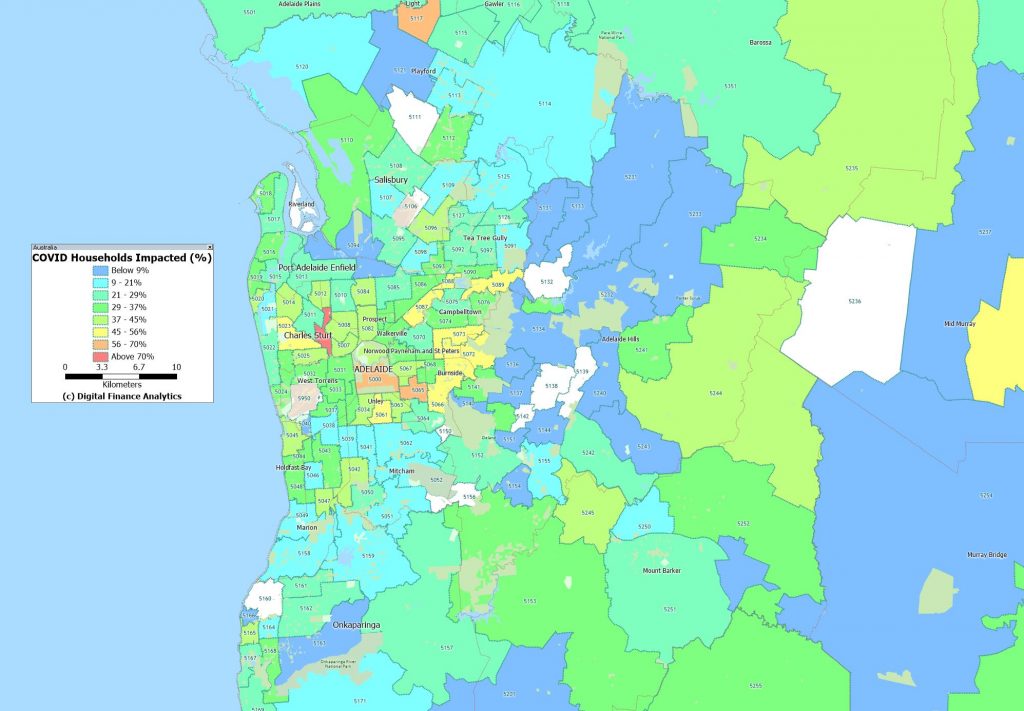

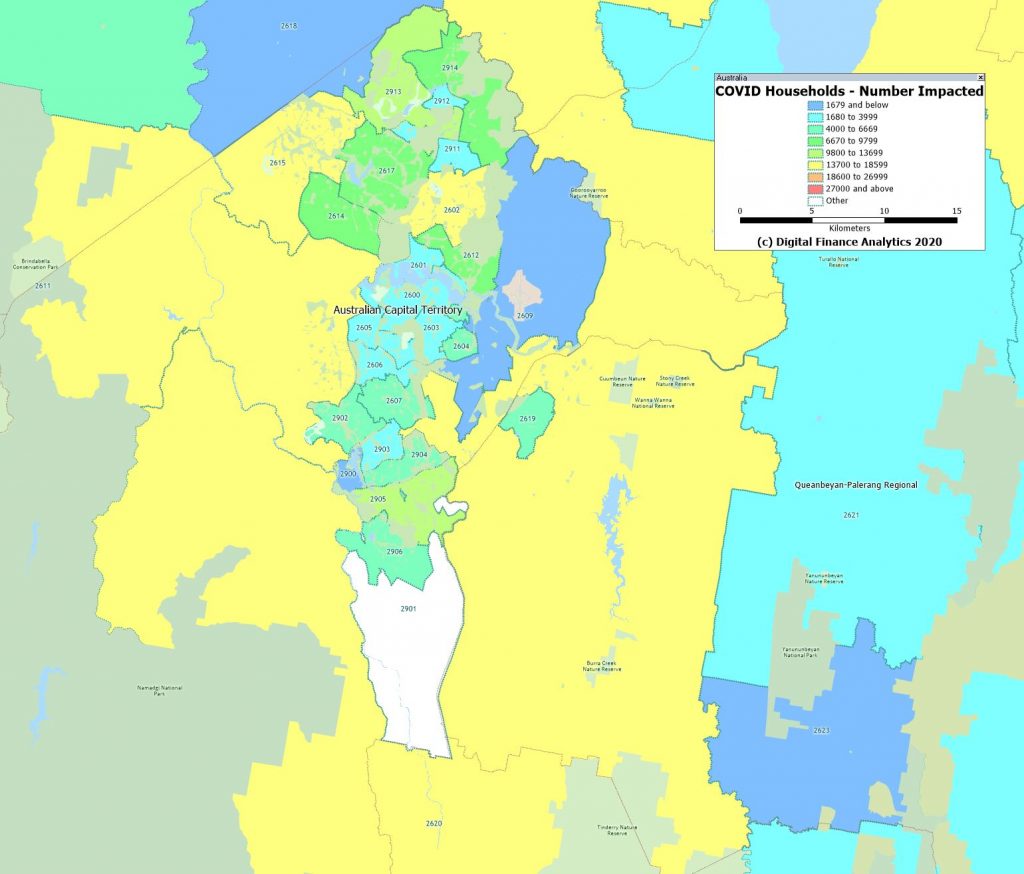

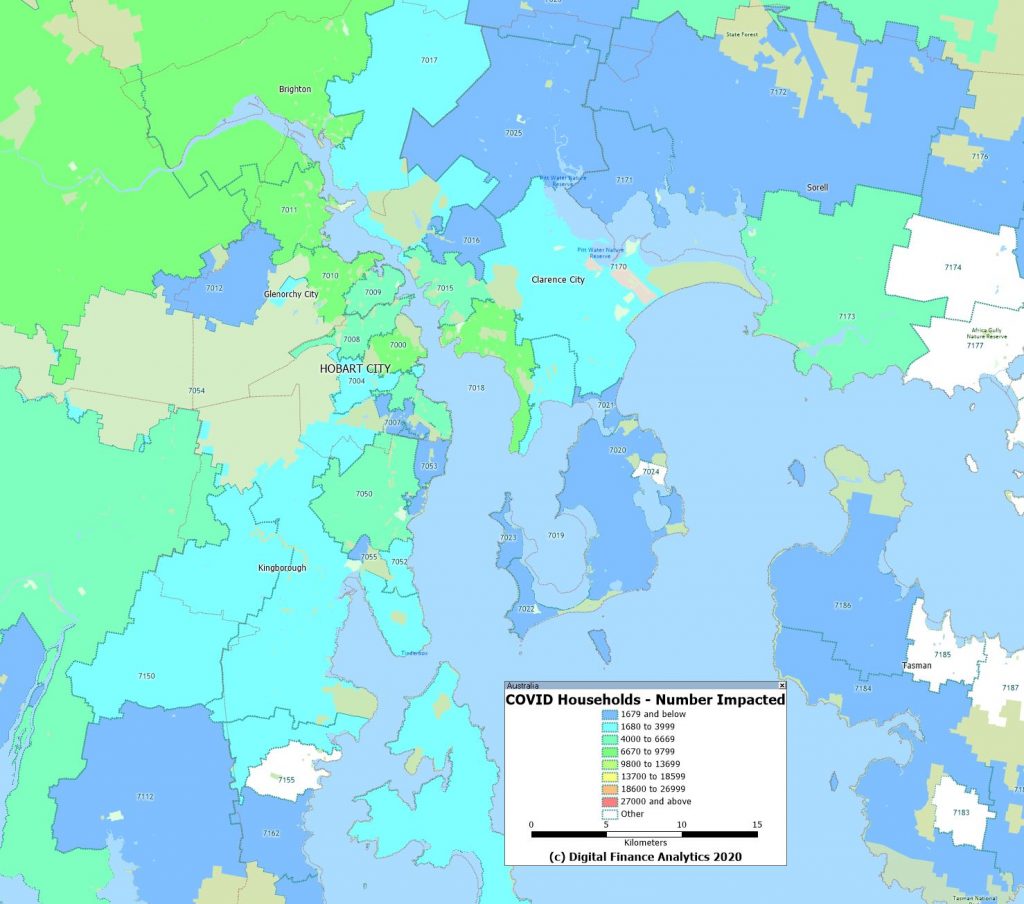

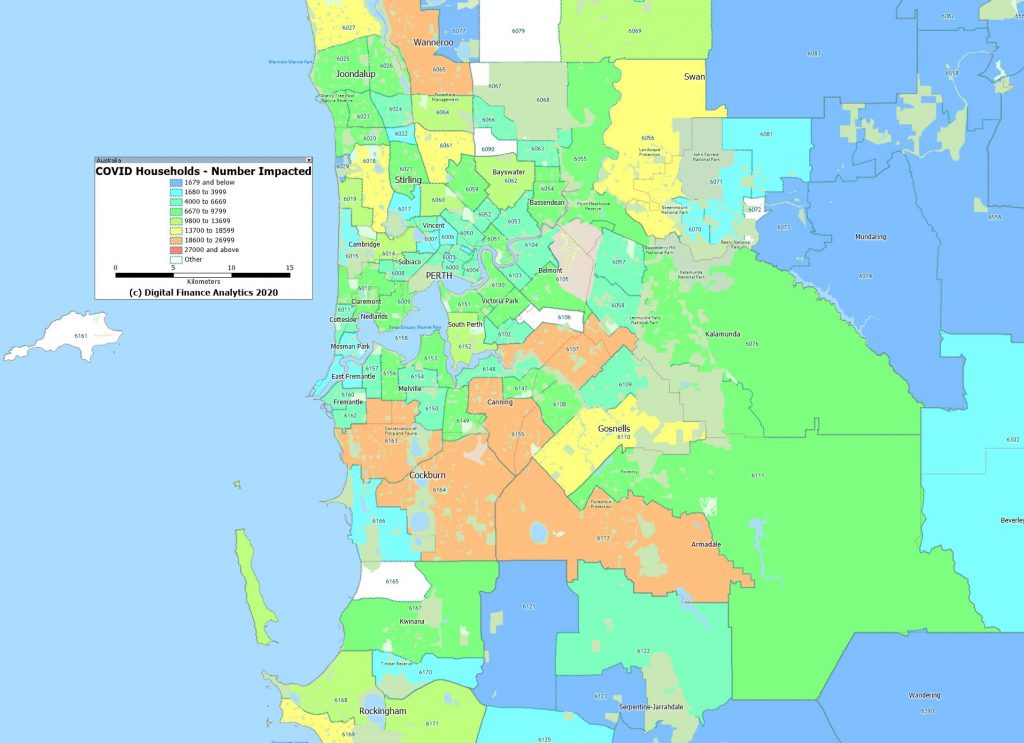

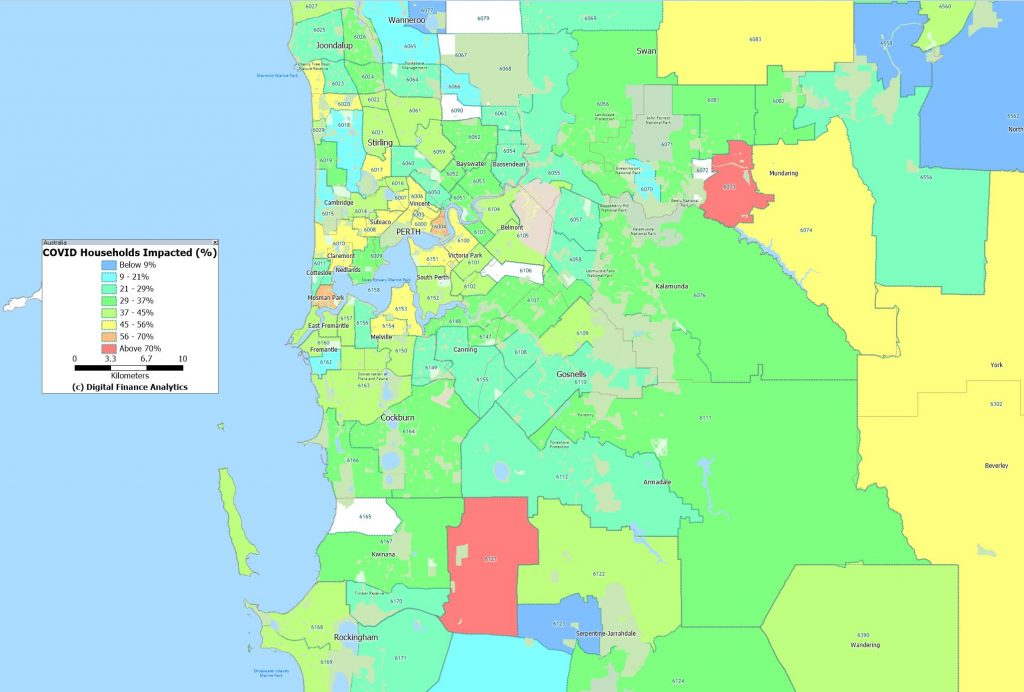

Because of the nature of the DFA survey, which is run to a post code level, we were able to identify those post codes with the largest counts of households impacted by COVID, financially speaking. We found that Toowoomba 4350 has the largest number of households impacted in the country, followed by Mackay 4740, Bundaberg 4670, Liverpool 2170, Mandurah 6210, Werribee 3030 and Cranbourne 3977. This underscores that COVID is hitting household finances areas across the country, not just in the main urban centres. Or to put it another way, even areas with low infection rates are being severely financially impacted.

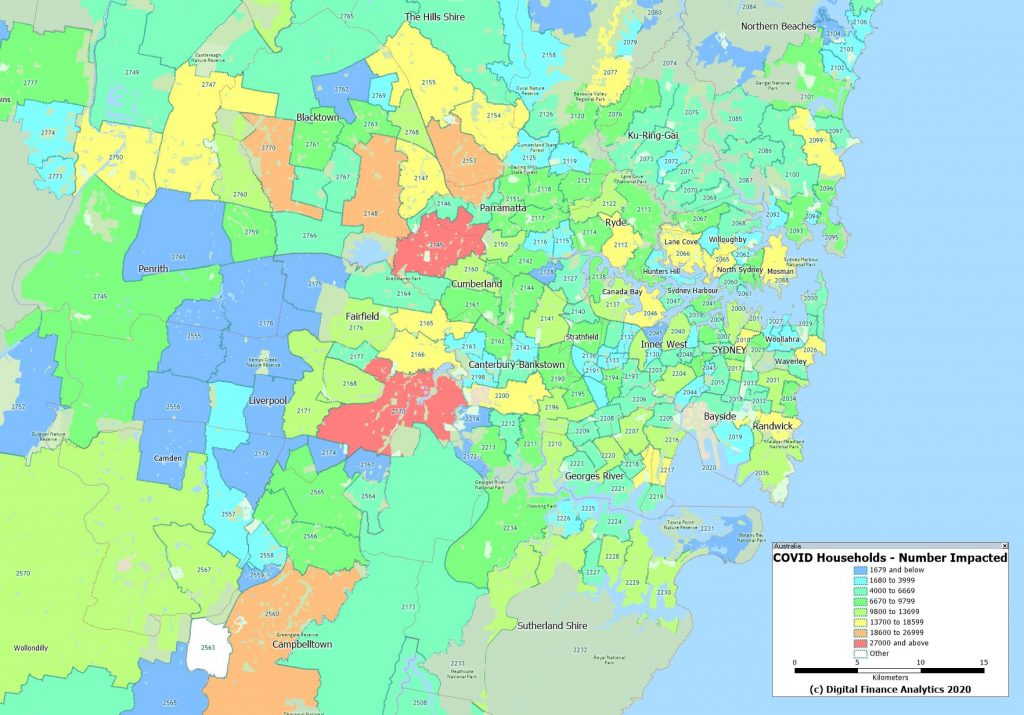

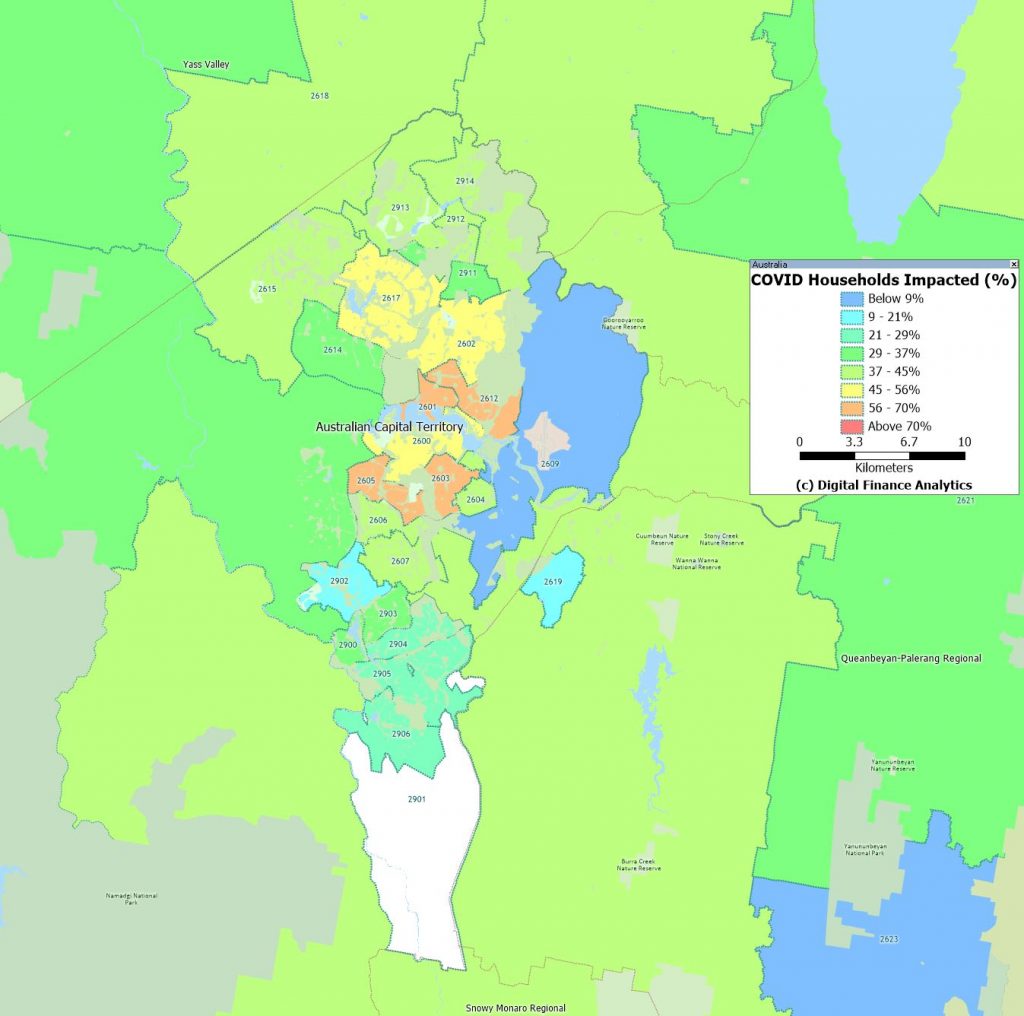

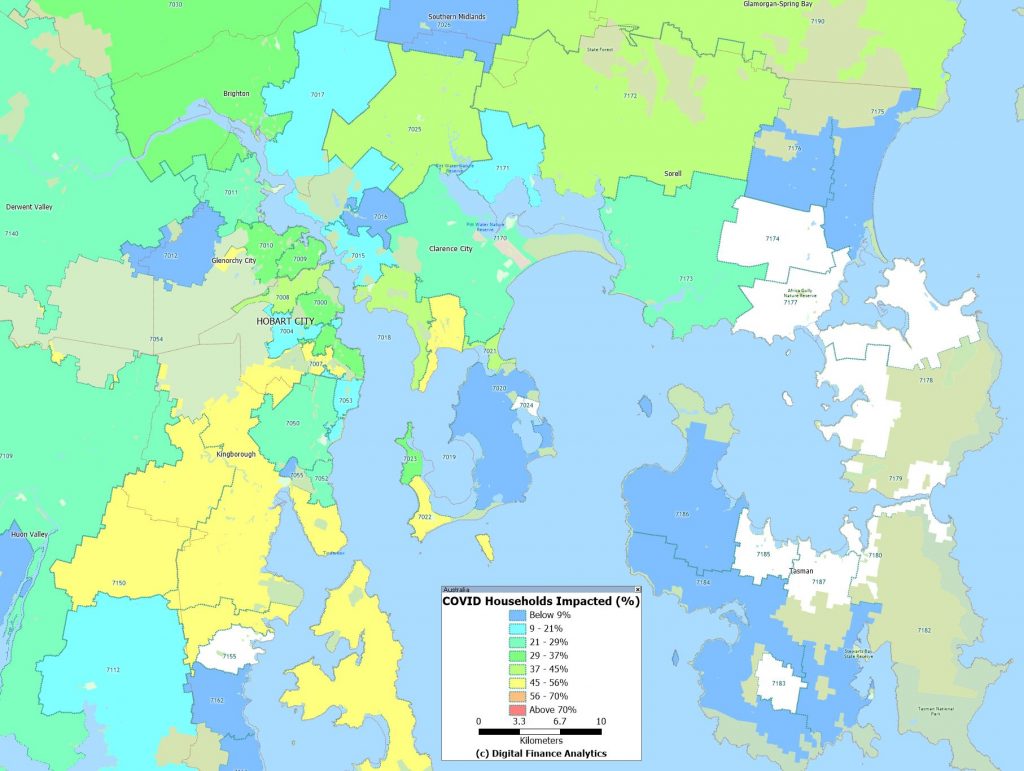

We have mapped both the number of households in each post code, and the percentage of households in each post code adversely impacted financially. There are some important differences. For example, in Sydney, post codes in western Sydney have higher absolute counts, but the relative proportion of households hit is higher in the more affluent eastern suburbs, despite having lower densities.

We completed similar mapping for the other major centres. Brisbane

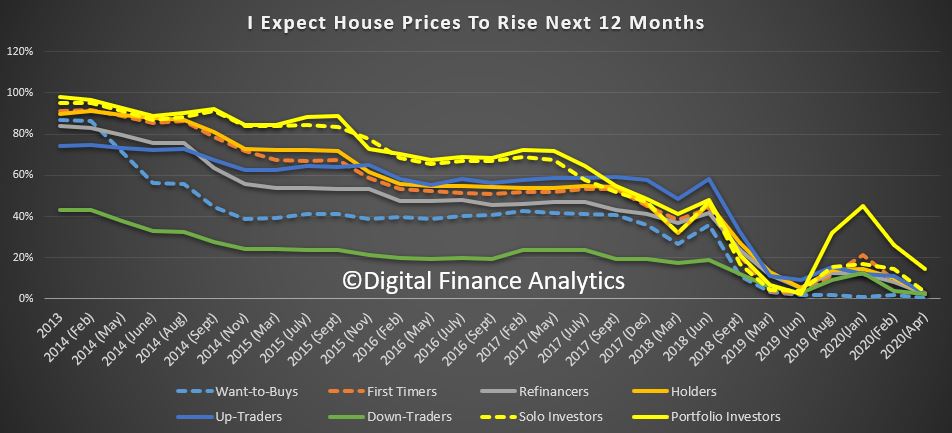

The latest results from the DFA household surveys examining property sentiment, reveals how much things have changed in the past month, from a pre-COVID to a COVID world.

These results are from our rolling 52,000 survey database, and we are able to track sentiment across our various household segments, and across owner occupier and investor cohorts. And I should note that although we run the analysis down to a post code level, the shifts are pretty uniform across the country.

First, we see that the intention to transact has dropped, across all property segments, and there are significant shifts among those seeking to trade downwards in order to to release equity, as fears of equity reduction rise. That said, some here are still seeking to exit now, fearing greater falls later. We covered this in our recent forced sales analysis. Property investors are also stepping back – no real surprise given the fall in rents, and the rises in listings we are seeing. First time buyers are also backing off. Thus sales volume will drop, significantly.

Property price expectations are shifting down, with a massive drop in those expecting any rise in the next 12 months (we may need to change the question to falls in the months ahead!). Portfolio investors remain a little more bullish, but it is all relative.

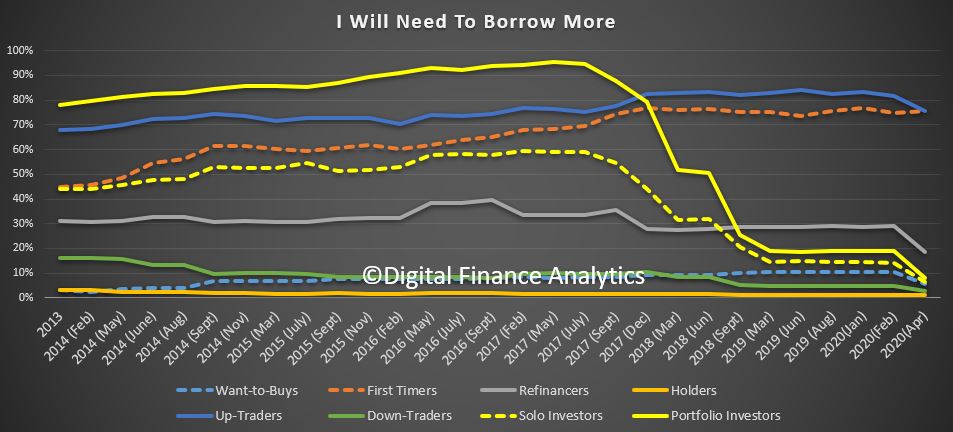

Demand for credit for property purchase also fell, though those seeking to refinance to gain rate discounts are still evident. In two segments, those seeking to trade up, and first time buyers, will still need to borrow more – if they were to transact. As above though the number borrowing is low for now.

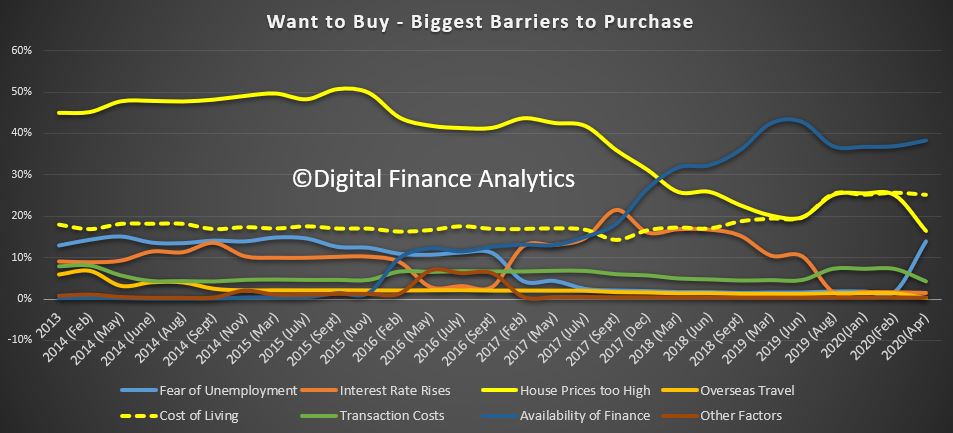

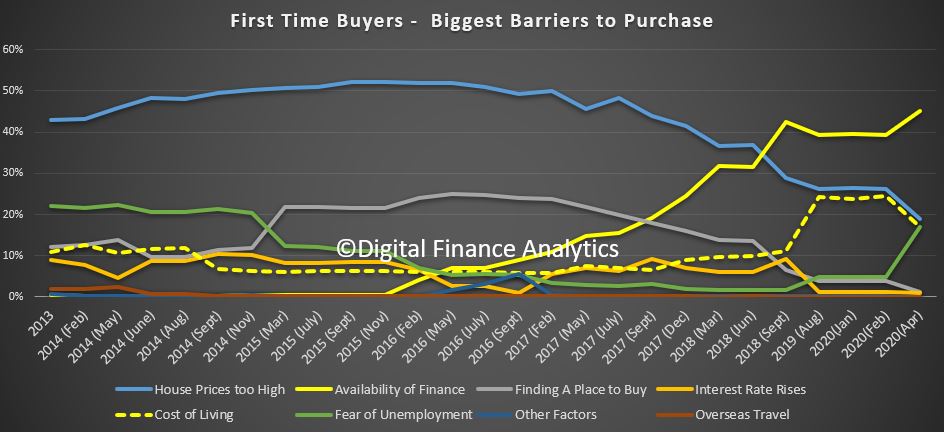

Across the segments, those wanting to buy saw a significant acceleration of concerns about the fear of unemployment – no surprise there.

The barriers for first time buyers include the availability of finance (we know some lenders are asking more questions about employment, and income than a month back). Again we see the fear of unemployment lifting consistent with other segments.

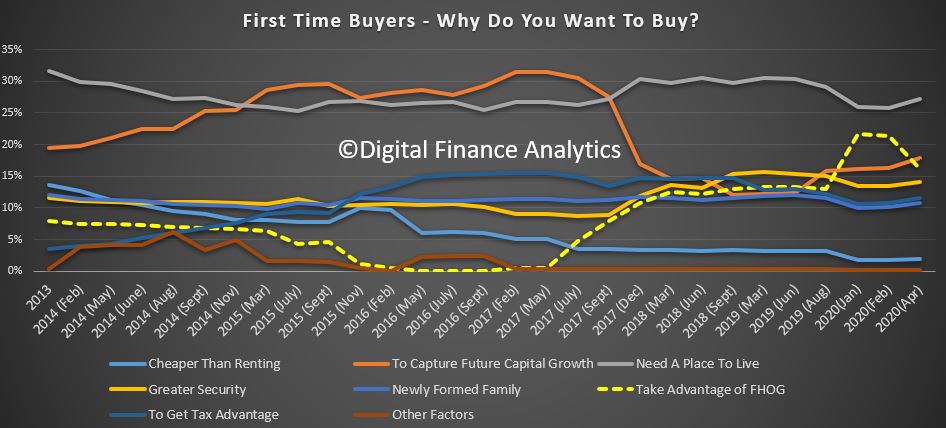

First time buyer motivations show that the attractiveness of the First Owner Grants tailed off, and there was a slight uptick in future capital growth expectations.

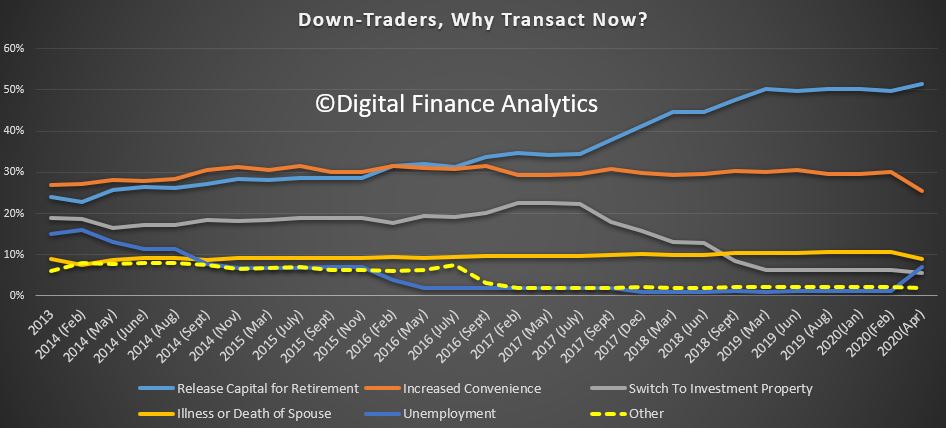

Down traders are driven mainly by a need to release capital for retirement (good luck with that!) and again we see the uptick in unemployment driving the decision to transact.

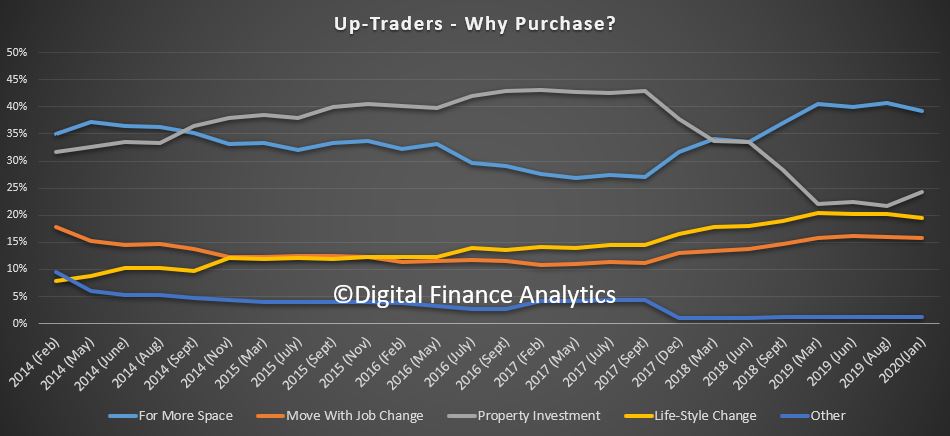

Those seeking to trade up still have the same basic motivations.

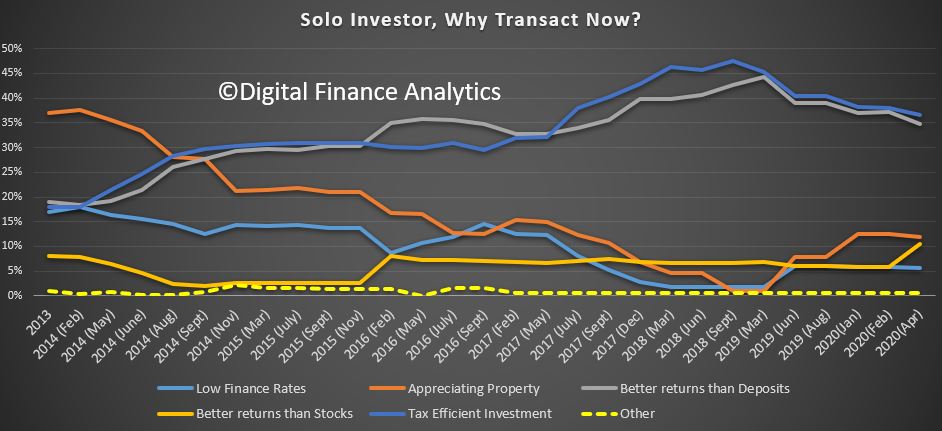

Property Investors are swinging a little towards equity investments, and under 20% are expecting future capital gains for now. Low finance rates, and prospective better returns than deposits remain the stronger themes, though as I have highlighted before, many property investors would be disappointment if they did but calculate the real returns on property. They are overstated, especially if capital values continue to fall.

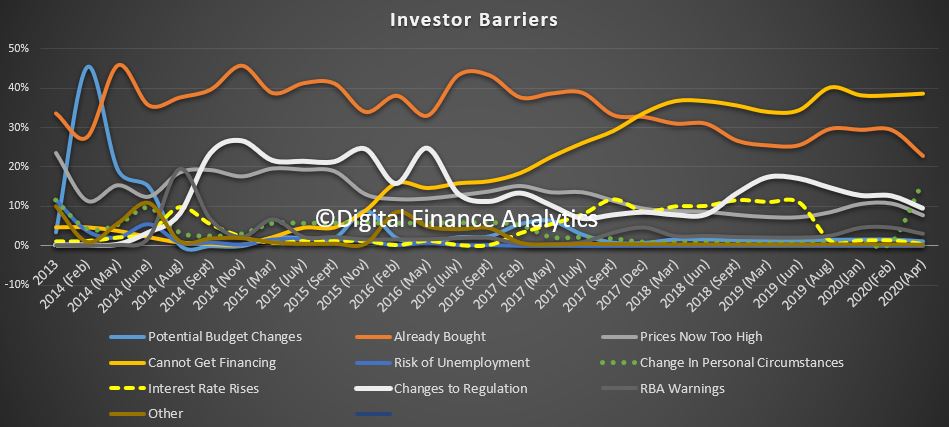

On the other hand, the barriers for investment reveals difficulty in getting financing, and changes in personal circumstances as significant risk factors.

I should caution we may see sentiment swing back in the weeks ahead as things play out, but in summary for now, demand for property is sinking, availability of finance is tightening, and the spectre of unemployment is rising. Property prices are likely to fall, now its a question of how far!

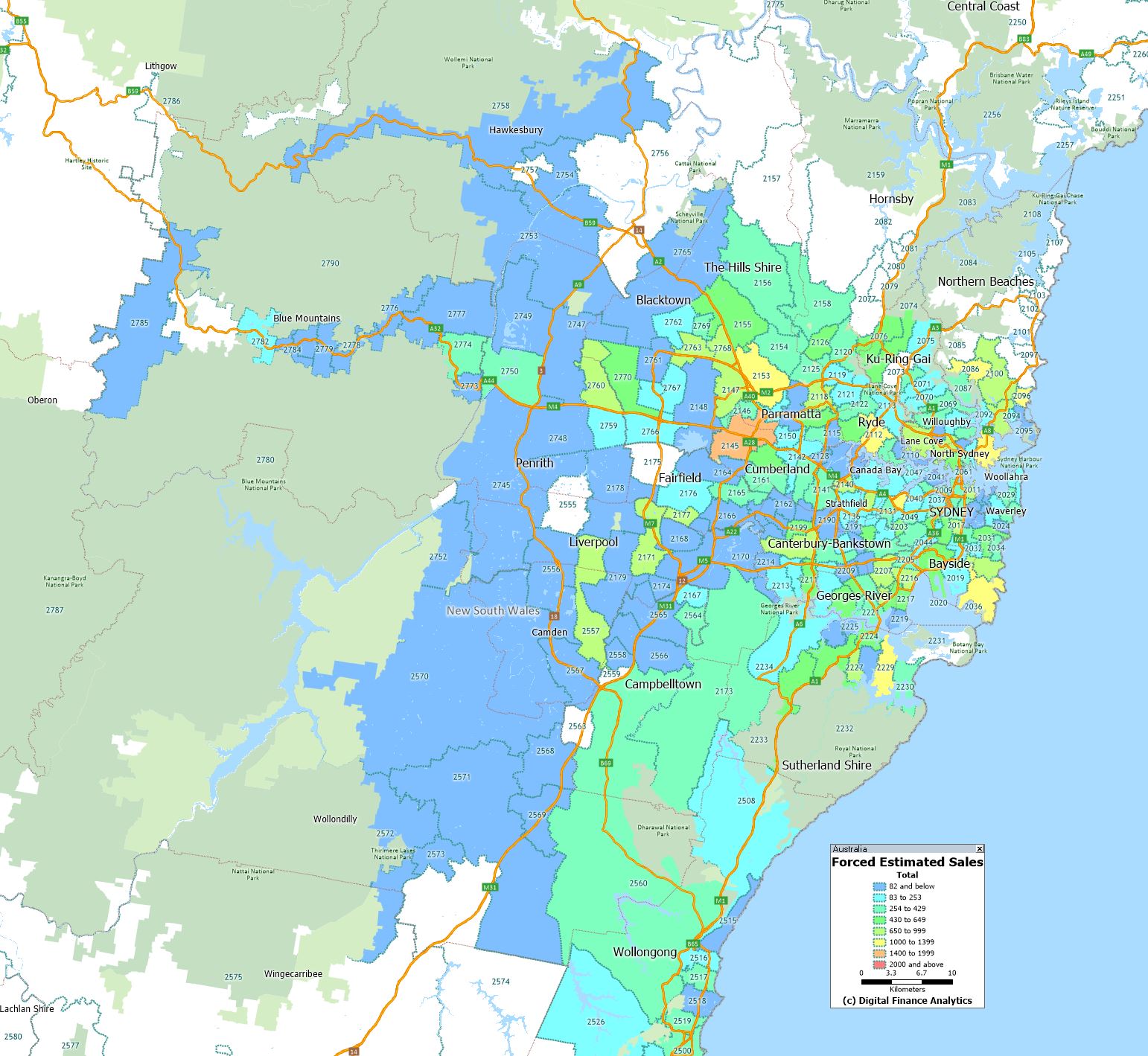

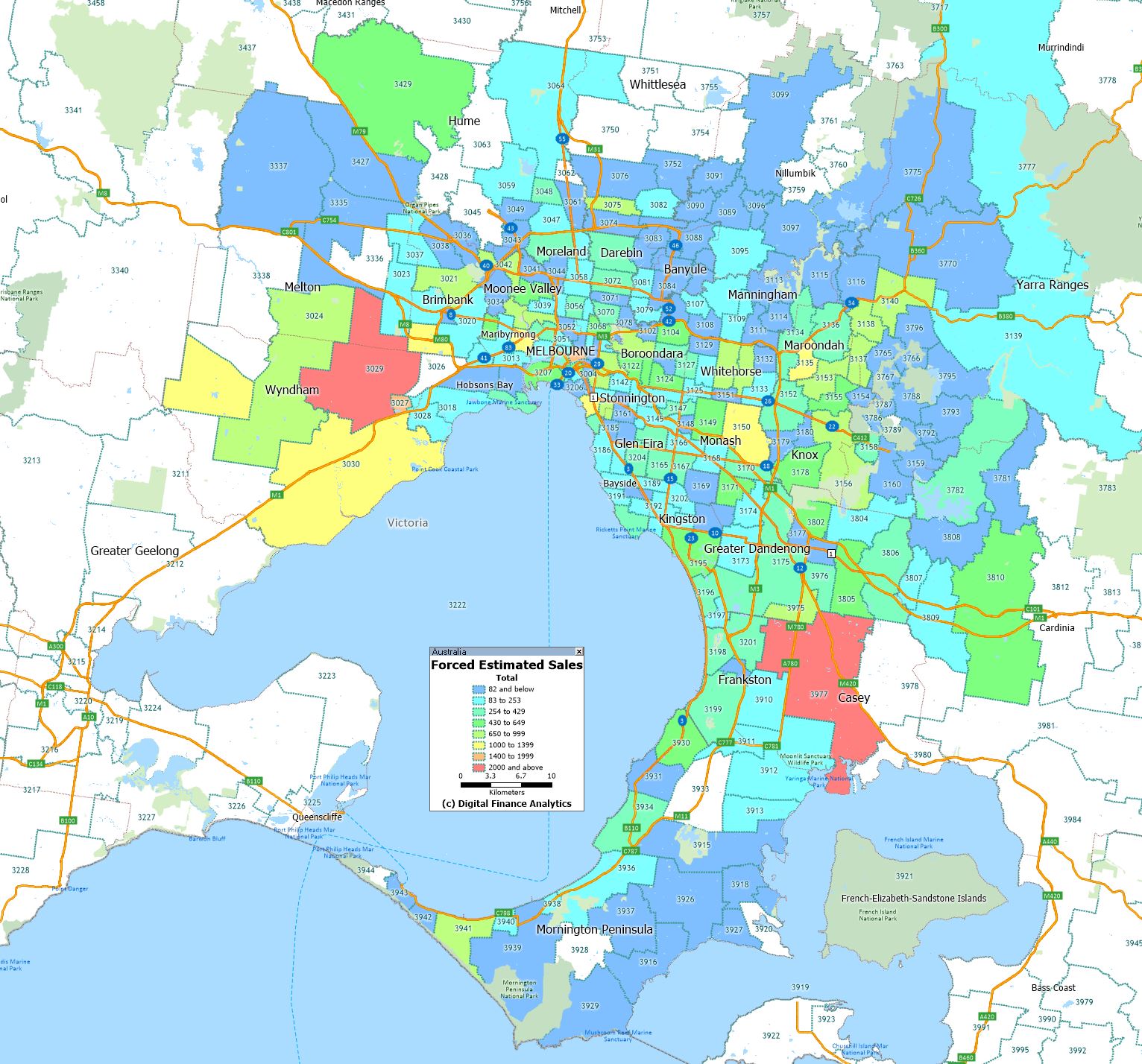

Nine News asked me to run some analysis on potential forced property sales, which they ran in Perth, Melbourne and Sydney yesterday. Today I wanted to add some extra detail from our analysis and explain how we established the baseline and share some heat maps for some of the major urban centres.

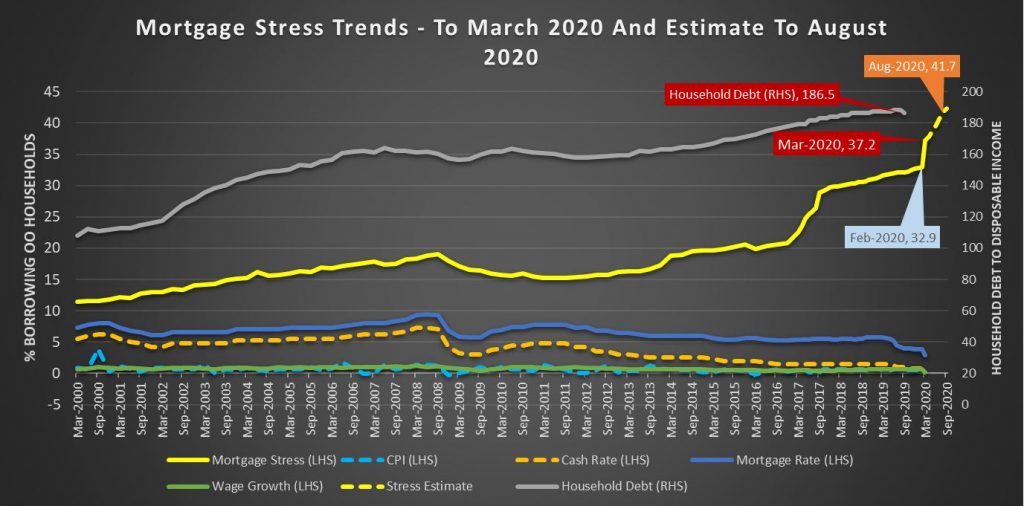

This is not an exact science, but the input data is from our rolling 52,000 surveys. One element in the survey is intention to transact – either to buy or sell, and the reason to transact. We also of course have cash flow analysis which is used for our regular mortgage stress analysis. For the record stress has risen significantly, as another 200,000 households fell into stress since February (even allowing for the various Government support schemes).

Forced sales are often narrowly defined as those initiated by lenders for debt recovery. The good news is that so far only a small number of these are in train. But the forced sales landscape is wider and is centred on the “fear of not getting out”

Property investors have had issues for a long time with real rentals falling, greater rental supply, and the recent shutting of Airbnb type lets. So for many, they are facing at least significant falls in receipts, or worse vacant property. They are also still dealing with the change of finance arrangements (though these are undone to more lose assessments it seems) and the need to have a repayment plan for the loan. The saving grace was the more recent rises in values, in some areas with houses doing better than units. But the expectation now is for significant property value drops, raising the risk of negative equity, or worse. Our surveys also suggest that some investors are unable, at least so far, to get repayment holidays from lenders. Thus the imperative to sell, even into a falling market explains the reason why we estimate around 8% of property investors are seeking to exit and quickly before values fall further. And some of these do not have mortgages, but simply want to save appreciated paper capital values.

Owner occupied property owners can access the banks’ schemes for repayment deferral more easily, though this appears subject to specific terms and conditions and some need to provide evidence of the health crisis impacting their finances. Many are going to ride out the current property cycle fall, though those with higher mortgages (including the 95% first time buyer schemes) will face the real prospect of the negative equity trap. But only about 2% of households are looking to sell under the current duress.

We are already seeing a rise in property listings across the country.

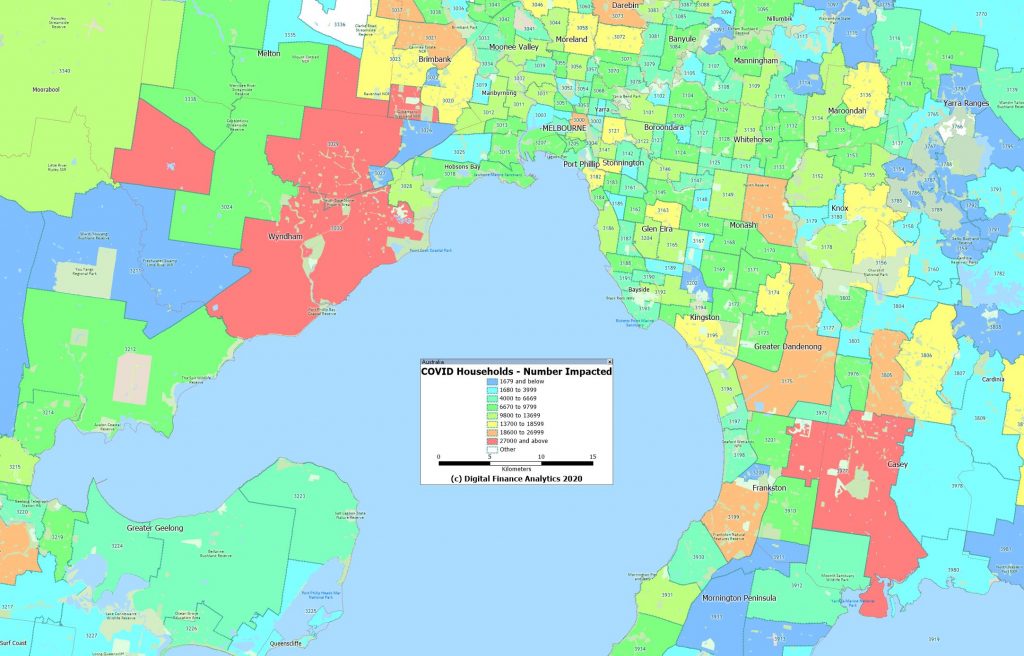

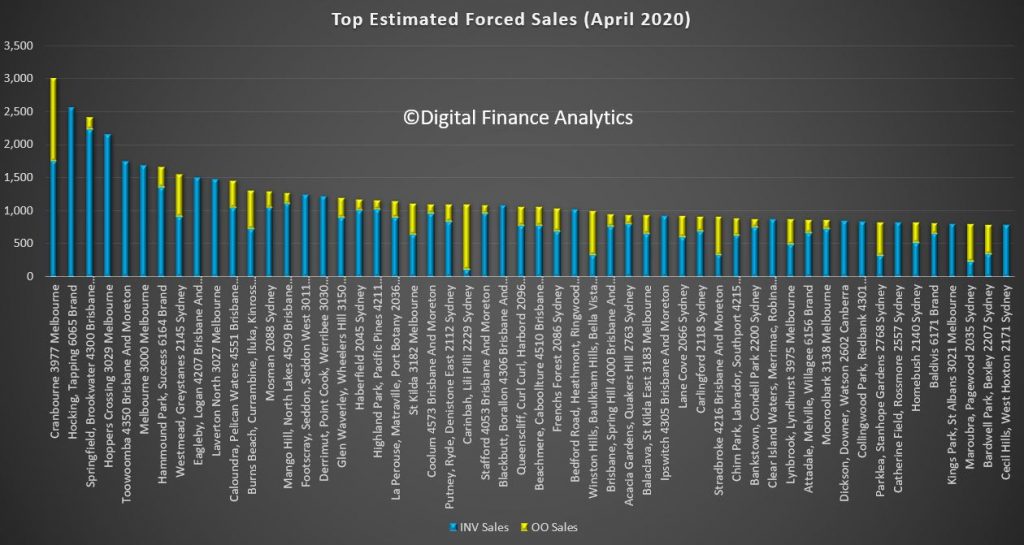

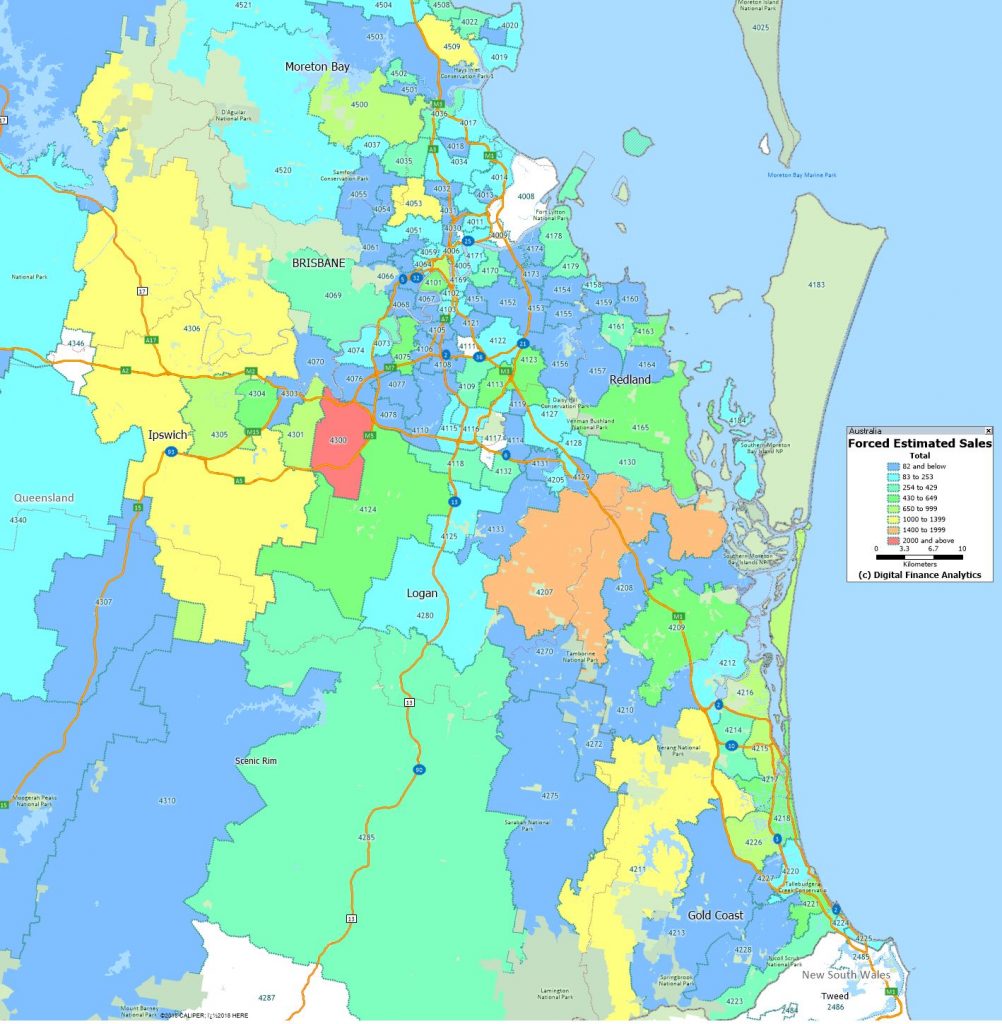

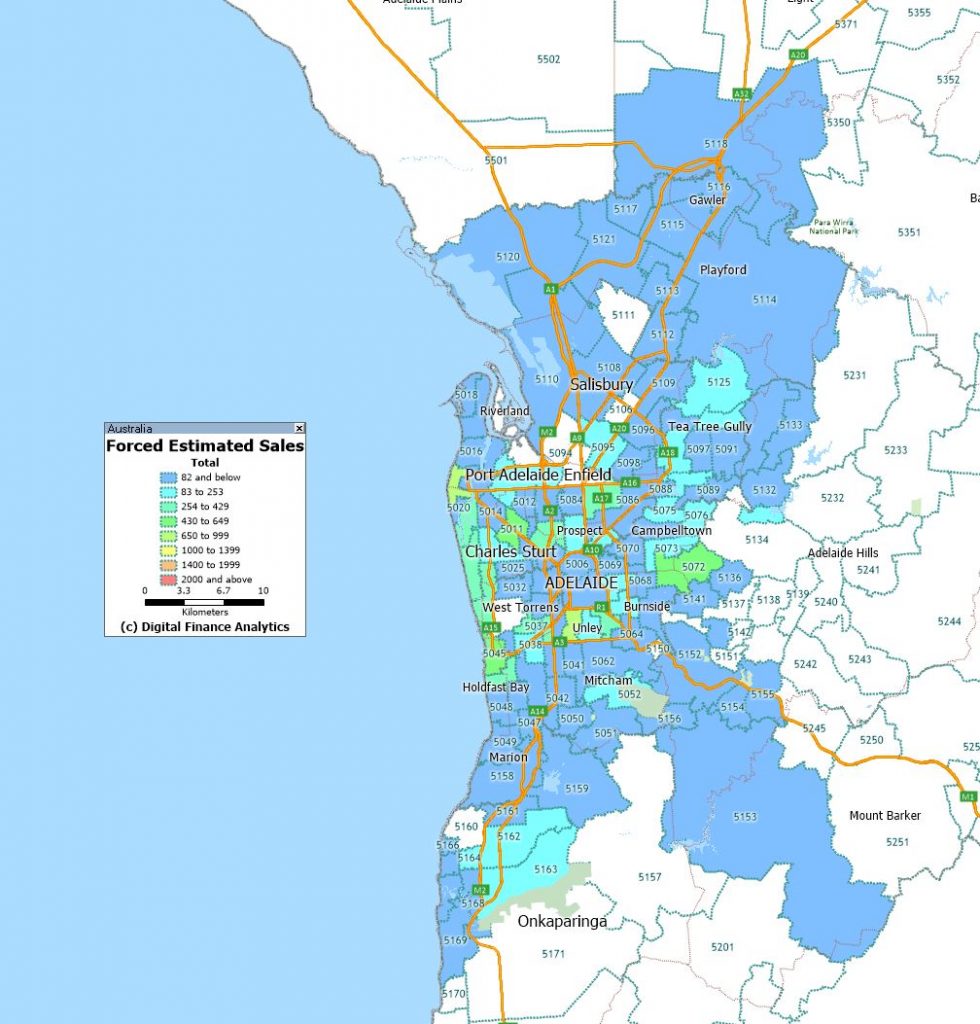

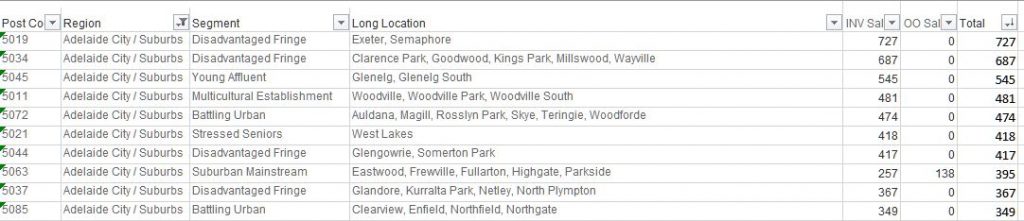

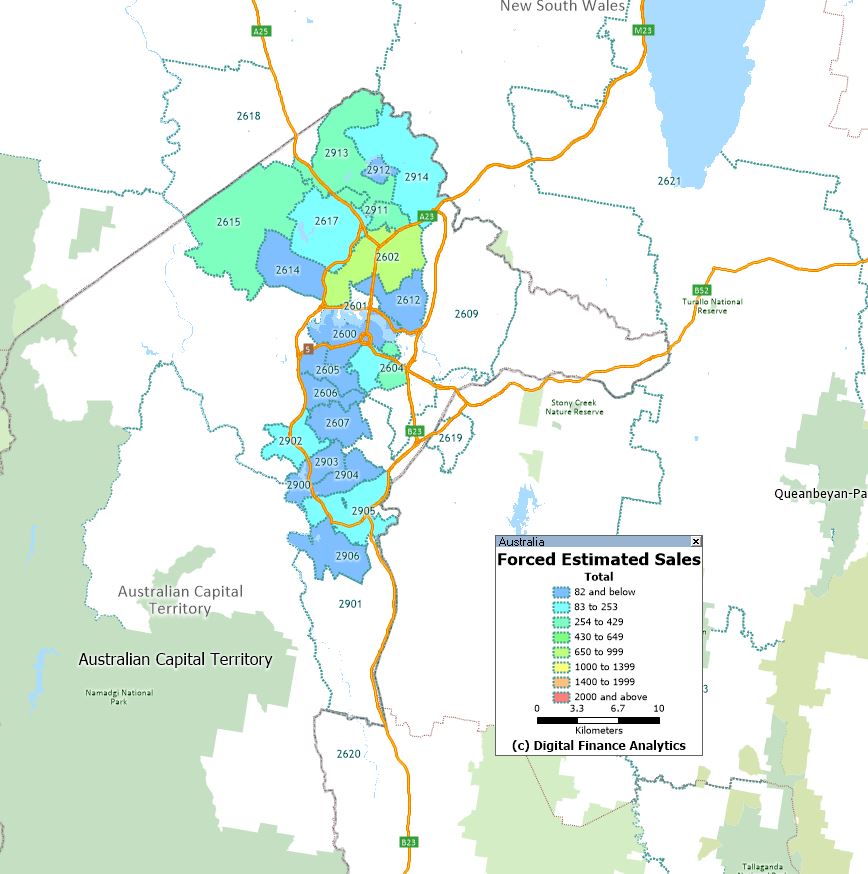

We have completed the analysis for some of the major urban centres, and the results are revealing. The post code with the largest number of potential forced sales in 3977, Cranbourne in Victoria. Here around 3,000 households are caught, with around 1,750 being property investors and 1,258 owner occupiers. Those following our modelling will recognise this post code as one of our most stressed, driven by high levels of new developments and recent purchases, by households who had above average incomes. Many new migrants live in the areas too.

Another new development area on the outskirts of Perth is second post code, 6065, which includes Hocking and Tapping, are next, with 2,500 investment properties likely to be up for forced sale.

Third on the list is Brisbane postcode 4300, which includes Brookwater and Springfield, with 2,220 investors seeking to exit and 190 owner occupiers.

Next is 4350, around Toowoomba, another high stress district, 1,780 property investors now looking to get out.

Fifth is central Melbourne 3000, with 1,690 property investors, almost exclusively in the high-rise sector of the market.

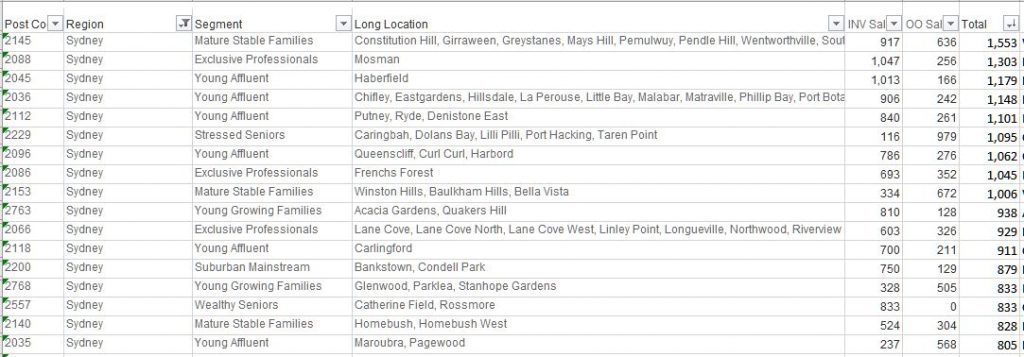

Sixth is 6164, in Perth, covering the areas around Success and Hammond Park, with 1,360 property investors and 309 owner occupied; and seventh is Sydney post code 2145, which includes Westmead and Greystanes with 920 property investors and 640 owner occupiers.

We have mapped each of the main geographies, and listed the top post codes in each state.

We will run the analysis again next month and see what trends are emerging.

We are running an extra live stream event tonight at 20:00 Sydney, covering the latest finance and property news, and our latest analysis via our surveys. Here is the YouTube link:

You can ask a question in real time via the YT chat, or sent a question to me beforehand by the DFA Blog message facility. Note, I will not be monitoring the Blog channel once the show begins.

I already have questions on MMT, property price movements, investment property, mortgage stress and forced sales and others….

I look forward to seeing you on the Chat later tonight.

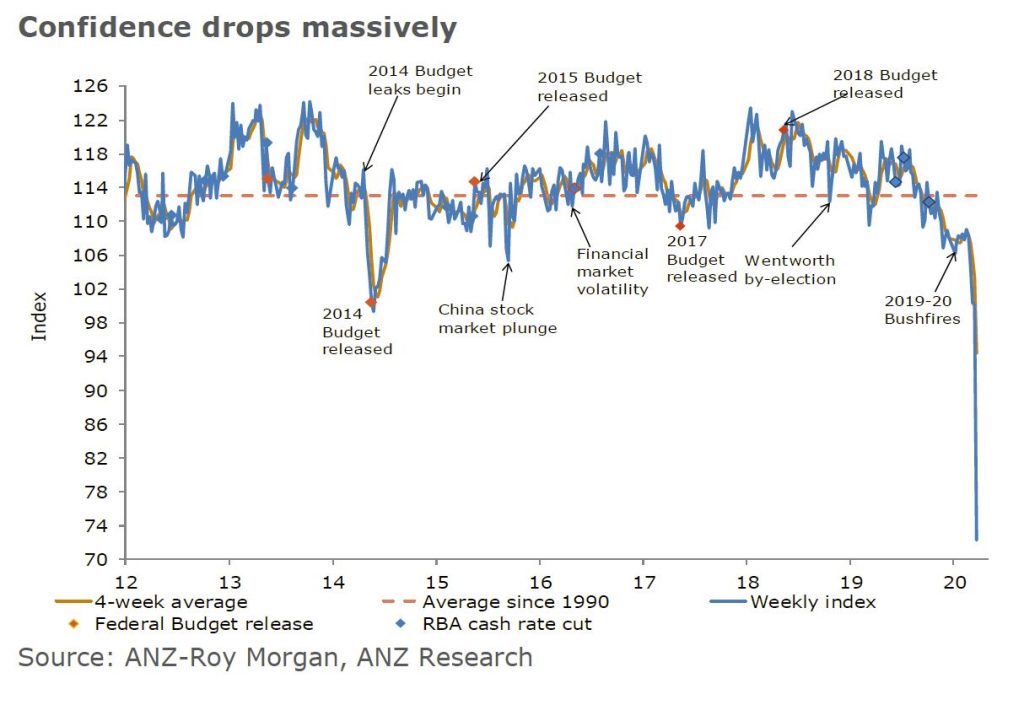

The ANZ-Roy Morgan Consumer Confidence index fell by a massive 27.8% last week. This fall has bought the headline index to just above the all-time lows recorded in 1990. Confidence is 17% below the lowest point seen during the global financial crisis (Oct 2008).

All the sub-components of the survey plunged. ‘Current financial conditions’ fell 23.9% while ‘future financial conditions’ dropped 25.8%.

The economic conditions subindices were also down sharply, with ‘current economic conditions’ falling 37.1% and ‘future economic conditions’ declining by 19.1%.

‘Time to buy a major household item’ fell the most, dropping by 37.2%. The four-week moving average for ‘inflation expectations’ was stable at 4.0%.

They do warn that they made a change in the survey methodology, away from face-to-face to phone and online interviews. It is possible that this impacted the results, though the consistency of the responses suggests this is unlikely.