Using data from our household surveys, we can look at investor loans by our core master household segments. These segments allow us to explore some of the important differences across groups of borrowers. We believe granular analysis is required to see what is really going on.

Today we look at the distribution of these segments by loan to value (LVR) and amount borrowed and also compare the footprint of loans via brokers, and by loan type.

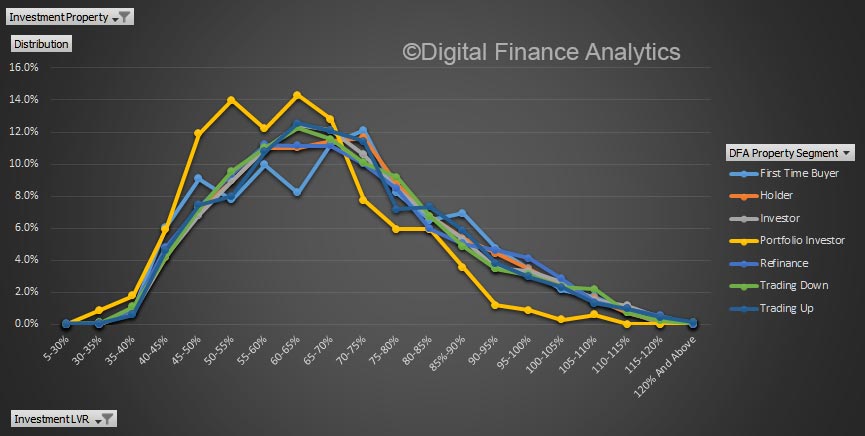

Looking at LVR first, there is a consistent peak in the 60-70% LVR range, with portfolio investors (those with multiple investment properties) below the trend above 70%.

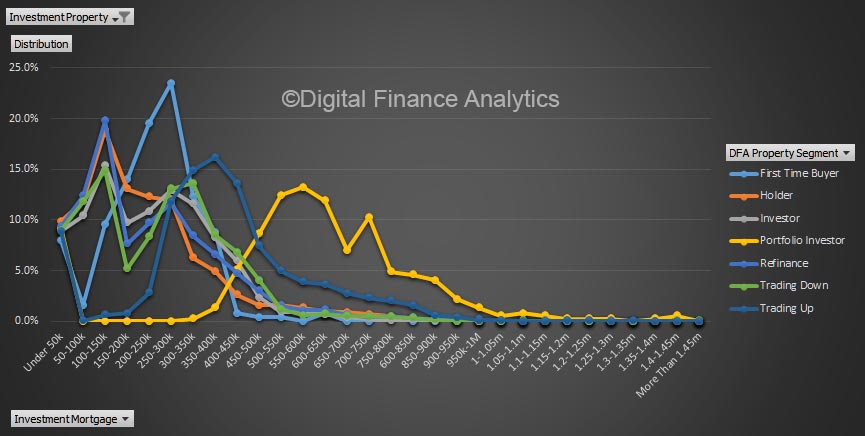

However, the plot of loan values shows that portfolio investors are on average borrowing much more, thanks to the multiple leverage across properties. A small number of portfolios are north of $1.4 million.

However, the plot of loan values shows that portfolio investors are on average borrowing much more, thanks to the multiple leverage across properties. A small number of portfolios are north of $1.4 million.

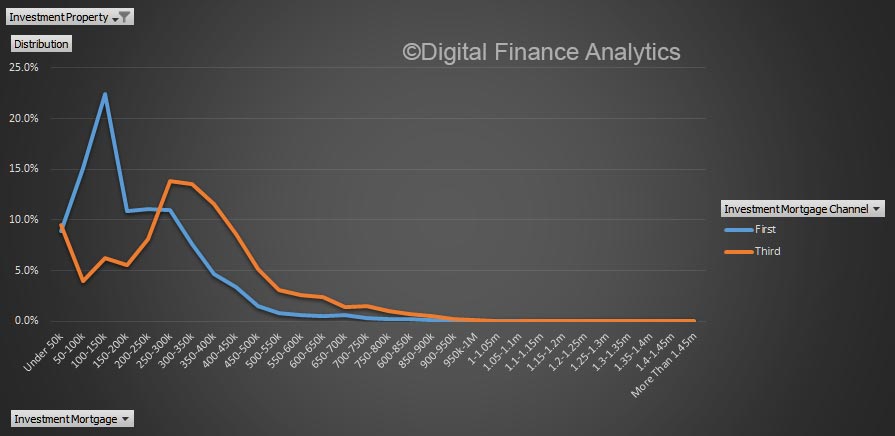

Investors who borrow with the help of a mortgage broker, on average is more likely to get a larger loan.

Investors who borrow with the help of a mortgage broker, on average is more likely to get a larger loan.

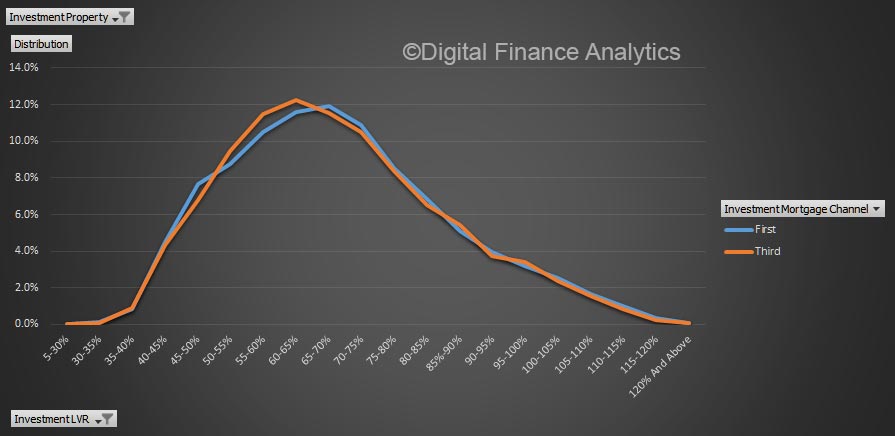

But there is very little difference in the relative LVR by channel.

But there is very little difference in the relative LVR by channel.

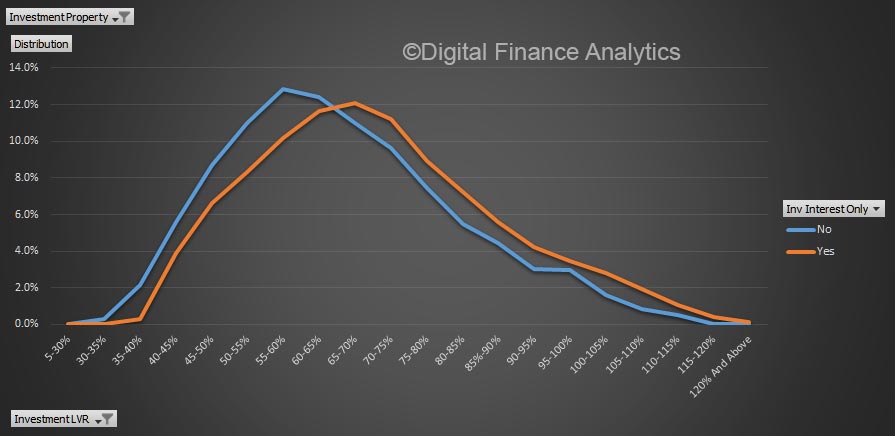

On the other hand, interest only loans will tend to be at a higher LVR.

On the other hand, interest only loans will tend to be at a higher LVR.

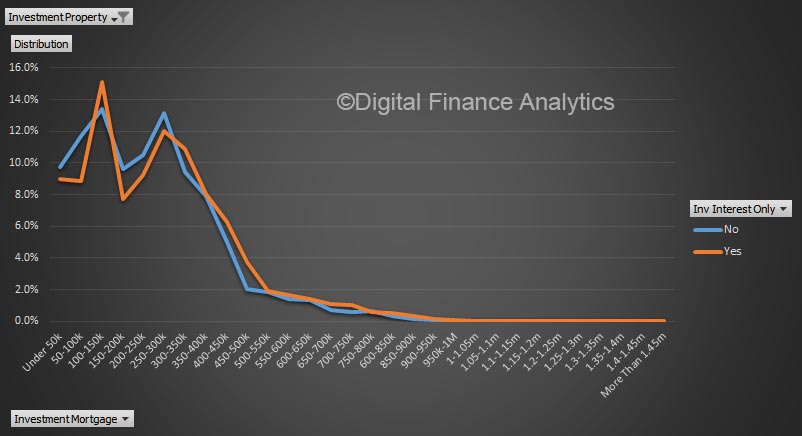

The average balance of interest only loans is also higher, especially in the $400-600k value range.

The average balance of interest only loans is also higher, especially in the $400-600k value range.

Microprudential analysis reveals interesting insights! The loan type and segment are better indicators of relative risk than LVR or origination channel.

Microprudential analysis reveals interesting insights! The loan type and segment are better indicators of relative risk than LVR or origination channel.