The AFR report cited research provided by DFA from our household surveys.

Australia is becoming a nation of landlords as record-high real estate prices force house-hunters into buying and renting investment properties rather than becoming owner-occupiers, analysis of purchases reveals.

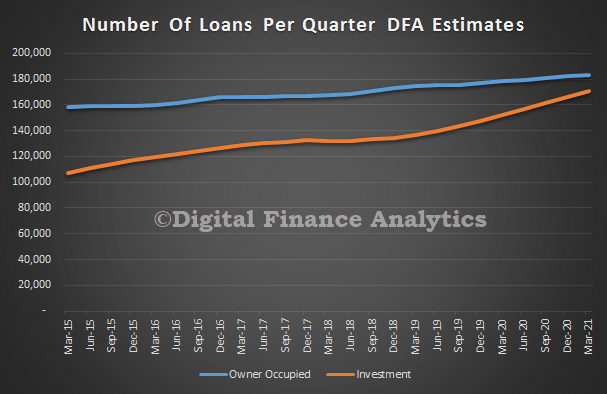

Property investors are also becoming younger and more likely to own several rental properties, with the number of investors with more than five properties having increased by 35 per cent in the past 12 months, from 175,000 to 272,000, according to research by Digital Financial Analytics.

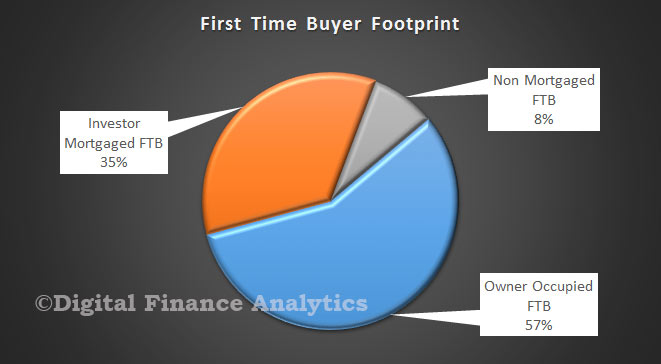

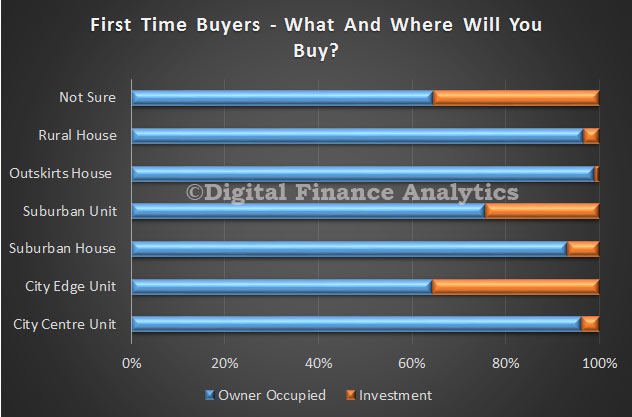

For the first time since records began, more first-time buyers are expected to be investors rather than owner-occupiers by the end of this year, heralding a major change in the nation’s home-owning culture, the research reveals.

The big increase in property investment is “a tower of dominoes”, said Martin North, principal of Digital Financial Analytics, a research firm that works for big banks and financial services companies.

“The question is whether fundamentals like a shortage of supply being soaked up by tenant demand will get us out of jail,” he said. “I think we probably have enough disequilibrium between supply and demand to support the market for the next couple of years.”

Mr North’s research highlights the number of first-time property buyers who rent the property and then remain at home with their parents or live in a communal arrangement with friends.

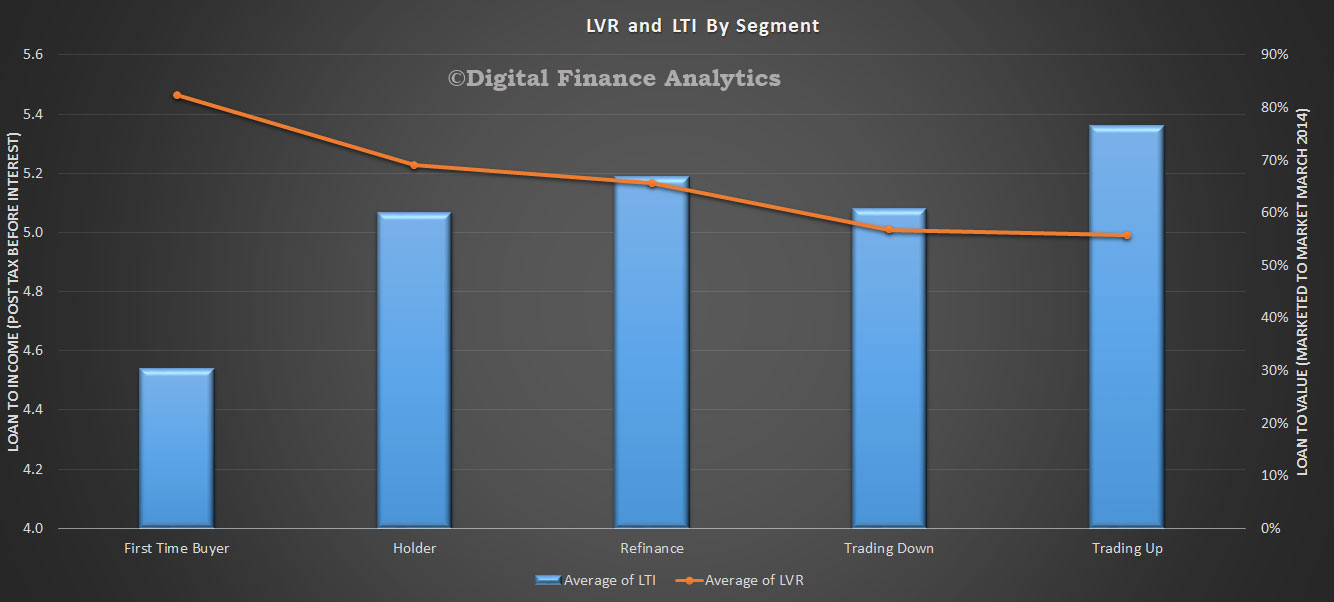

During the same period, the number of want-to-buys, first-time buyers, refinancers, up-traders and down-traders remained about the same.

The number of loans to first-time buyers fell in all states and territories except Tasmania during the March quarter, according to government statistics.

Loan spruiking widespread

Financial advisers are routinely being offered commissions of between 5 per cent and 10 per cent, or fees of $25,000, to encourage investors to take out limited-recourse loans to buy apartments.

Alternatively, finance brokers, who often work with developers, have been encouraging the widespread use of non-bank interest-only loans using the equity in the investor’s home as security and borrowing about 20 per cent of the value of the investment property to cover the deposit and purchase.

Rental income from the investment property is expected to cover all costs and any capital growth is then leveraged to buy the next property.

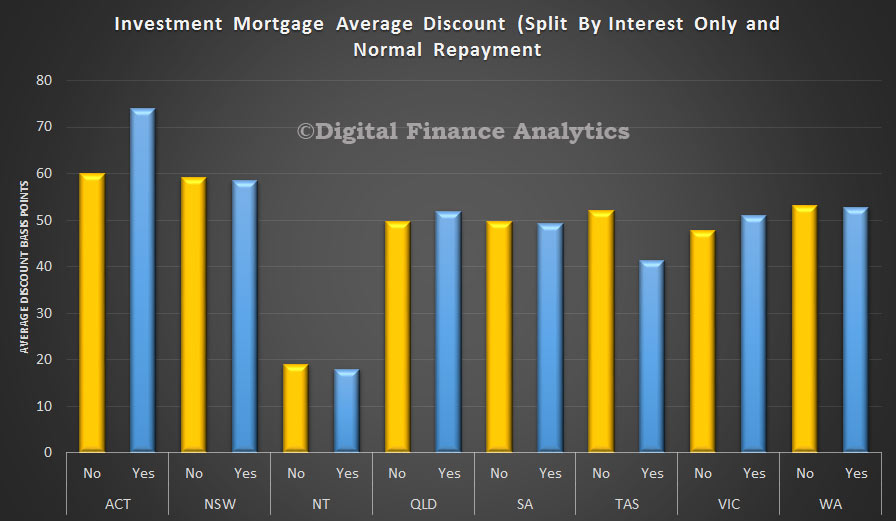

Interest-only loans only require repayment of the interest on the loan over the rolling five-year borrowing term.

Mario Borg , a finance strategist at Melbourne-based Strategic Finance who owns 10 properties and estimates his worth at more than $10 million, disagrees that portfolio investors are exposed to excessive risk.

Borg believes attractive properties where people want to live will always find a tenant and is confident the right financing structures will protect portfolios from market corrections. He never allows the loan-to-value ratio to drift above 50 per cent of the portfolio’s value and maintains a credit limit of 80 per cent of the portfolio value to cover any unforseen events.

Christopher Foster-Ramsay, owner of Foster Ramsay Finance, says investors need to be aware of the risks, particularly if prices begin to fall.

“Many want to live the dream without understanding what they are potentially getting into,” he said.

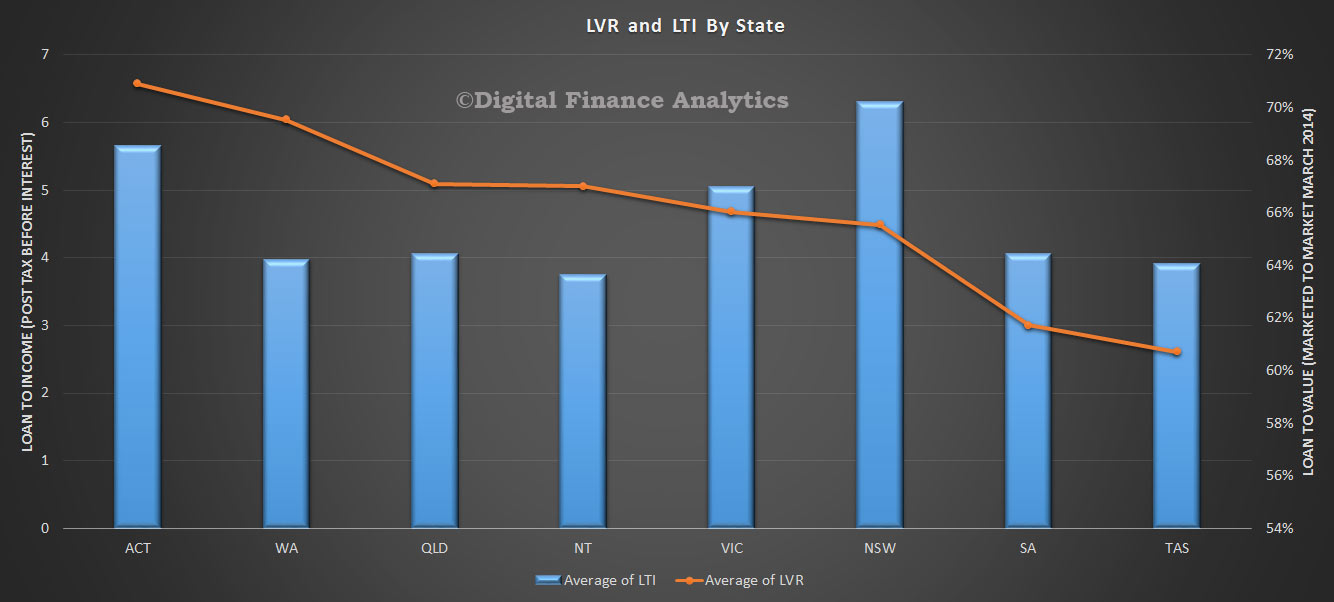

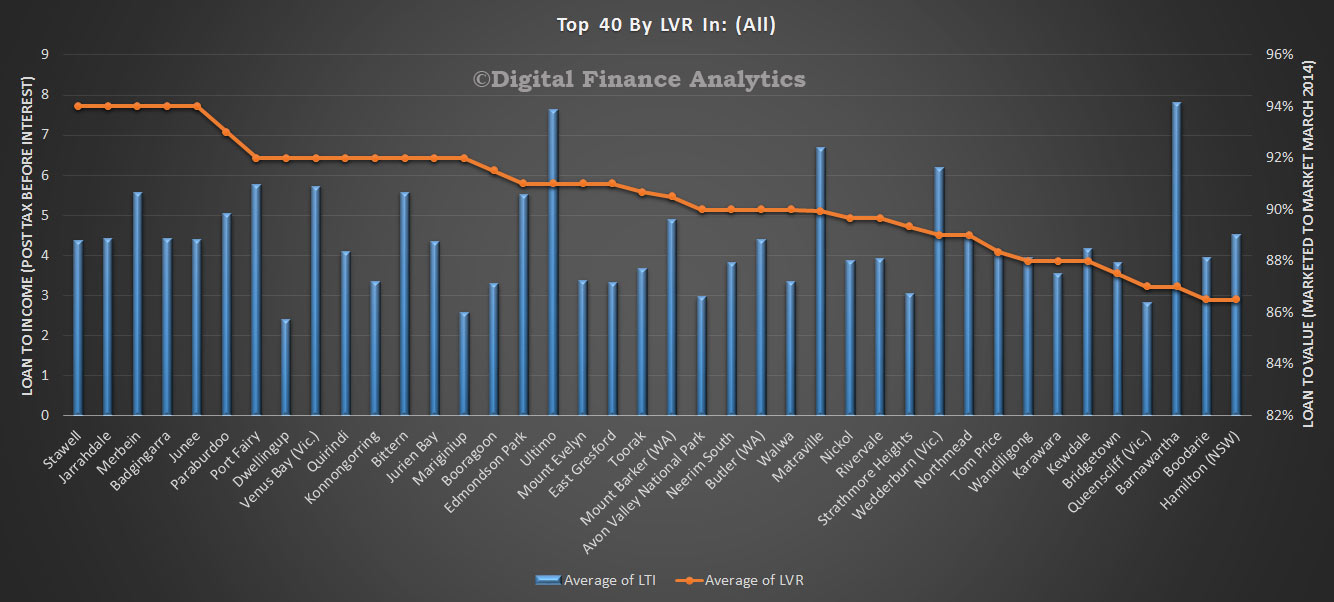

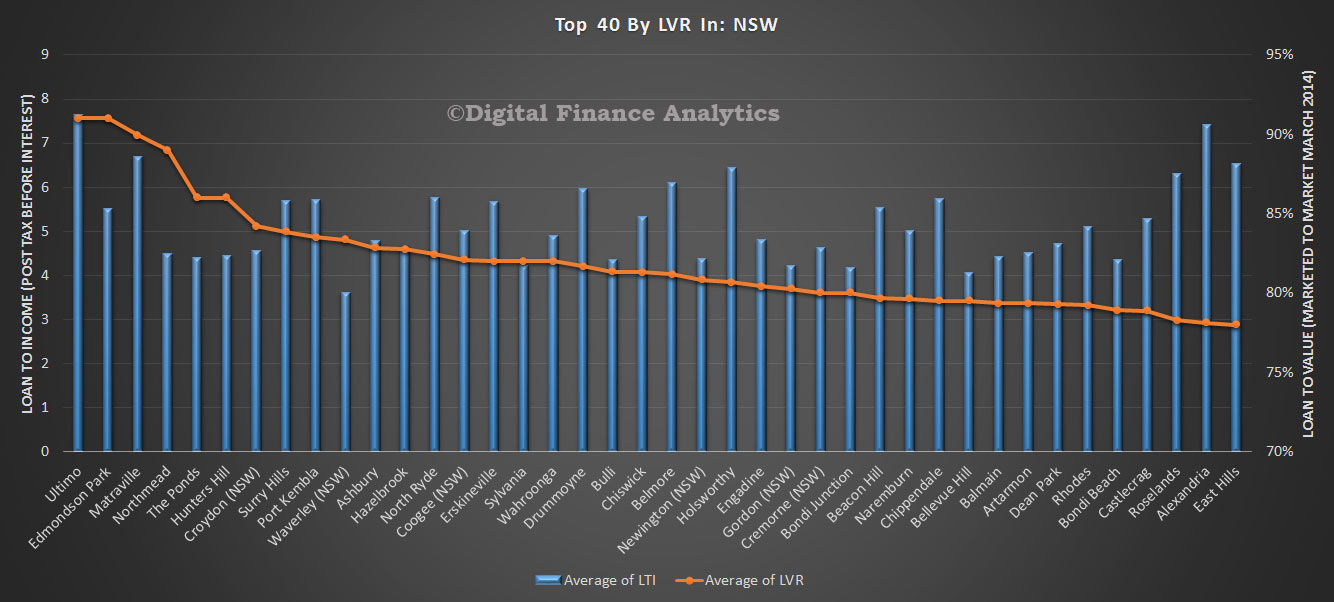

By any international standard, such as loan-to-income ratio or gross domestic product-to-house prices, the nation’s bill for house buying is about 30 per cent above the long-term trend.

Go here to request a copy.

Go here to request a copy.