I caught up with Mark Jones, Chief Executive Officer of SocietyOne, Australia’s first and only marketplace lender to reach $500 million in loan originations across its personal loan, agri lending and marketplace business. And now its setting its sights on reaching $1 billion by the end of calendar year 2019.

I wanted to know how he had been able to grab the $500m of the $100 billion market, and specifically whether it was the appetite for P2P which was growing, or whether there were particular elements which had made the difference, given the 60 people working in the business, plus the external technology platform provider.

He argued that in the past 3-6 months SocietyOne had made a number of improvements to its business, and combined this had made a significant difference to their momentum. First, they have improved their algorithms around risk assessment and pricing. He explained that their underwriting algorithm had been tuned and improved, but that loans were still reviewed by a credit officer. They are sending data to, and expect to benefit from the new comprehensive reporting regime which is coming in October.

Next they are clear on their target market, with a focus on good quality borrowers, often stable homeowners aged 35-50, with loan interest rate tailoring between 7.5% and 18% depending on individual risk profiles. The typical loan would be in the region of $22k, over 3 or 5 years, though they are able to offer facilities between $5k and $50k. Average loan duration is around 4 years, and funds are offered on a principal and interest, straight line repayment basis.

Finally, they have invested in new technology, designed to offer customers a better online experience. They will shortly be launching a new application form, built from the ground up for mobile devices. Loans via these devices make up more than half of the loan applications now, and are growing quickly. This is a substantial change from the previous front end which was PC/Web based primarily. Mobile is the future.

They offer unsecured loans, and also credit to agribusiness sector – for example for the purchase of cattle and sheep. Momentum has accelerated thanks to the development of the broker channel, which they started in June 2018. They wrote $100k in June/July via this channel, $1.4m in August and are on track for $2m in September. This is proving to a significant venture. Most of this business related to unsecured personal credit, where around half of loans are refinancing of existing facilities, debt consolidation and credit cards. More than half of the loans are written below 13% interest rate, which is significantly lower than many credit cards. Brokers often advise their clients about managing their debt, Mark said. Other reasons to borrow include car loans and holidays.

Ahead they are considering offering secured loans including motor vehicle finance among others. They will continue their focus on the Australian market, which remains a significant opportunity.

Their portfolio is quite concentrated in the Sydney and Melbourne metropolitan areas, because they have been targeting their marketing and advertising there. That said it is a national business. In terms of portfolio losses, Mark said he was satisfied with these, making the point that all applicants were effectively “new to bank” so there was no customer history. But on a like-for-like basis the loss ratios were quite similar if not better than what a typical bank might see.

Finally, I asked about the funding source for the business. Around a quarter comes from high-net worth “sophisticated” individual investors, with the remaining coming from a range of institutions, including mutual banks and institutional investors. These channels are growing more quickly, as shown by the relative fall in the proportion from high net worth sources, which was 30-35% a year ago.

The recipe of good risk profiling, target markets, and a focus on customer experience is clearly paying off, and the $1 billion target certainly looks achievable, ahead.

SocietyOne says it has today become Australia’s first and only marketplace lender to reach $500 million in loan originations across its personal loan, agri lending and marketplace business, and is now setting its sights on reaching $1 billion by the end of calendar year 2019.

The milestone follows a record August and the recent appointment of ex-Westpac and Citibank exec, Mark Jones, to the top job of CEO.

“We’re delighted to have reached this significant milestone as we deliver an even better deal for our borrowers and investor funders,” said Mr. Jones.

“We’ve been growing steadily over the past 12 months while we continued to transform our business and build new capabilities for our customers. As a result, we’re now seeing real momentum in the business that we expect to continue, and which should see us achieve breakeven by the end of March 2019 and reach $1 billion in loan originations by the end of 2019.”

We had a record August month for personal lending with $14 million in originations, up 46% on August 2017, and well above the monthly average for the past 12 months. September is now also shaping up to be another record month, with volumes expected to further increase into the fourth quarter of the calendar year.

“The seasonal increase in consumer credit heading into the festive season will combine with the rollout and expansion of a number of new initiatives, including continued expansion of our broker distribution offering, the launch of our new brand campaign, and the release of the first phase of our new technology platform,” continued Mr. Jones.

“We’ve also launched our new “When it happens” brand campaign this past weekend, bolstered by support from our shareholders. The campaign is an honest reflection of the way that even joyful moments can sometimes present financial stress to otherwise financially-fit people, as a result of unexpected costs.

“‘It’ can happen to any of us, but there’s no need to add extra stress by racking up high-interest credit card debt when a low rate personal loan from SocietyOne is often a far better solution.

“Looking ahead, the impending introduction of comprehensive credit reporting and open banking, ASIC’s proposed regulatory changes to credit cards, a robust economic backdrop, and a push for a better deal following the royal commission into banking all bode well for a highly prosperous 2019,” concluded Mr. Jones.

Online retailer Kogan is expanding into the finance sector, with home loan’s first off the rank in 2019 via Kogan Money offering products through agreements with Pepper Money and Adelaide Bank. Kogan Money Home Loans will be the first of a suite of products and services set to be rolled out under the new brand.

More evidence of the distribution of financial services enabled by digital.

The company’s active customer base is now 1,388,000, up by 433,000 or 45.3% and last month they posted a 277% rise in full year profit to $14.11 million, up more than $10 million from last year’s $3.74 million, driven by the pure play online retailer’s portfolio strategy. The result came as revenue jumped by $122.79 million or 42.4% to $412.31 million.

According to their announcement:

Kogan Money will focus on simplifying credit and financial services for all Australians and making them more affordable through digital efficiency.

Under the agreement with the two lenders, Adelaide Bank will make available competitively priced conforming or prime home loans. Pepper will make available competitive near prime, non-conforming or specialist, home loan.

Details such as the level of interest rates have not yet been released, but are expected much closer to the launch date.

David Shafer, executive director of Kogan.com, said the partnerships will help Australian homeowners.

Kogan is excited to partner with Adelaide Bank and Pepper to enable us to offer Aussies a range of competitively priced home loans available online.

Adelaide Bank has a long history of partnering with innovative brands and business that bring greater choice and diversity to consumers.

Pepper is the leader in alternative lending in Australia and, since 2001, has been helping Aussies who may not tick all the traditional boxes for home loans to get financing.

With well over a million active customers, Kogan.com is proud to be able to form partnerships like these that form a genuine win-win-win for both Adelaide Bank and Pepper, for Kogan’s shareholders, and most importantly, for Kogan.com customers.

Adelaide Bank’s head of strategic partnerships, Damian Percy, said, Kogan.com is a leader in the online retail space and Adelaide Bank has a long tradition of partnering with like-minded businesses to bring greater choice and competition to the Australian home loan market.

Together we believe we can make a real difference to the emerging community of Australian online shoppers by delivering simple, great value housing solutions through Kogan Money.

Mario Rehayem, CEO Australia at Pepper Money, said, Pepper Money is delighted to be partnering with Kogan.com on the Kogan Money Home loans opportunity.

They are a company who clearly anticipates their customer needs and looks for innovative ways to solve them.

Through our experience and depth of product offerings, we look forward to helping more of their customers succeed in finding the home loan finance they need.

Fintech, GetCapital, one of the most interesting SME business lenders here in Australia, recently announced a distribution agreement with aggregator PLAN. So I took the opportunity to discuss the growth of the business with GetCapitals’ COO Frank Sterle in our occasional Fintech Spotlight series.

Frank Sterle COO GetCapital

GetCapital is a specialist lender to the SME sector. It was founded in 2013, and really hit the market in earnest in 2015, offering finance to businesses with an annual turnover of typically between $200k and $2m, though they have written deals for much bigger firms too. Their focus is the Australian and New Zealand Markets. They have lent more than $250 million in loans so far, and this is still growing, with a team now topping 100.

Frank, who by the way previously worked at Deutsche Bank within the Fixed Income, Currencies and Commodities (FICC) division of its Investment Bank, highlighted that they will consider deals across all sectors, and they offer loans for a range of business purposes from vehicle purchase, working capital, equipment finance and import lines of credit, with the proviso that borrowers will need to provide a personal guarantee as a minimum. They operate in the “Prime” to “Near-Prime” credit space.

Around one third of leads come via their direct channel – using an on-line application, one third from strategic partnerships, and one third from a portfolio of aggregators, including AFG, CFG, Fast, Plan, and others. In fact, this is the channel which is expanding fastest and they expect to announce additional aggregator partnerships soon.

Their underwriting processes are interesting, as they have invested big in technology at the back end, for example to be able to capture bank statement data using tools from Proviso and this supports quick assessments of deals by their dedicated Relationship Managers, who will also consider credit history, and serviceability. Although a portion of loans with a low “expected loss” are fully automated, GetCapital still used a final human overlay by an experienced credit officer for larger and more complex underwrites. This also enables a broker to transparently workshop a deal with their Relationship Manger rather than being advised of a black box “computer says ‘no’ response”. They can approve finance in under 24 hours, often much less. They have three price tiers, with the lower value one typical of the sector, averaging around $40,000, but the average is much higher in the stronger credit tiers, with different pricing structures above. Frank was at pains to underscore the prime quality of the loans they write thanks to their specialist capabilities, and that their loss rates are very low, across the country. They claim to be “sharp on price” as well, though the price will depend on how long the business has been trading, their credit score and the assets backing the deal.

They are funded by a couple of institutional investors, including NAB, who provides their wholesale funding, so no crowd funding in sight here!

The experienced team also includes CEO, Jamie Osborn, ex. Managing Director at Macquarie Capital; Chief Commercial Officer Renata Cihelka, ex. ANZ, AMP, Morgan Stanley and CBA; Head of Sales, Cristian Fedrigo, ex. AFG, CBA; Head of Customer Operations, Brad Kinna, ex. ING Direct and Rabobank and Chief Risk Officer, David Hurford, ex. Westpac Institutional Bank.

Looking ahead, Frank believes the SME funding market is set to grow, but in so doing, there will be a bifurcation in the target market, with some focussing on the higher more sophisticated end of the sector, while others will battle it out at the lower end. He thinks they are well positioned for the former, and sees the prospect of further expansion in Australia ahead.

My sense is that GetCapital is indeed well positioned to disrupt core prime lending to SME’s in Australia, and as such are becoming a force to be reckoned with. Highly relevant given the feedback from our latest SME surveys which shows again that the incumbent lenders are forcing SME’s to jump though ever higher hoops to get a loan.

Further evidence of the digital disruption of finance ahead!

Australian fintech Tic:Toc, has today announced a reduction in its fixed home loan (live-in) rates by up to 0.10%, bringing their headline 1-year fixed rate to 3.59% (comparison rate 3.64%).

Tic:Toc’s 2-year fixed home loan (live-in) will match their standard variable rate at 3.64% (comparison rate 3.65%).

The rate cut increases Tic:Toc’s standing as holding the lowest 1 and 2 year fixed rates in the market (27 August, https://www.finder.com.au/home-loans/fixed-rate-home-loans), possible due to the cost efficiencies in Tic:Toc’s automated assessment and approval platform.

Tic:Toc founder and CEO, Anthony Baum, said the decision to reduce fixed rates was great news for home loan customers and new home buyers looking for stability for the foreseeable future.

“We recognised there is a lot of confusion in today’s market; with slumps in house prices; out of cycle rate changes; and erratic predictions around interest rate rises.

“Helping Australians better manage their home loan repayments, or move into home ownership, is our priority, and we want to do so with full transparency.”

Since its launch, Tic:Toc has received over $1.3billion in value of submitted home loan applications.

The home loans originated by Tic:Toc and backed by Australia’s fifth largest retail bank, Bendigo and Adelaide Bank, are available throughout Australia at tictochomeloans.com; with the latest fixed rates advertised at www.tictochomeloans.com/instant-fix.

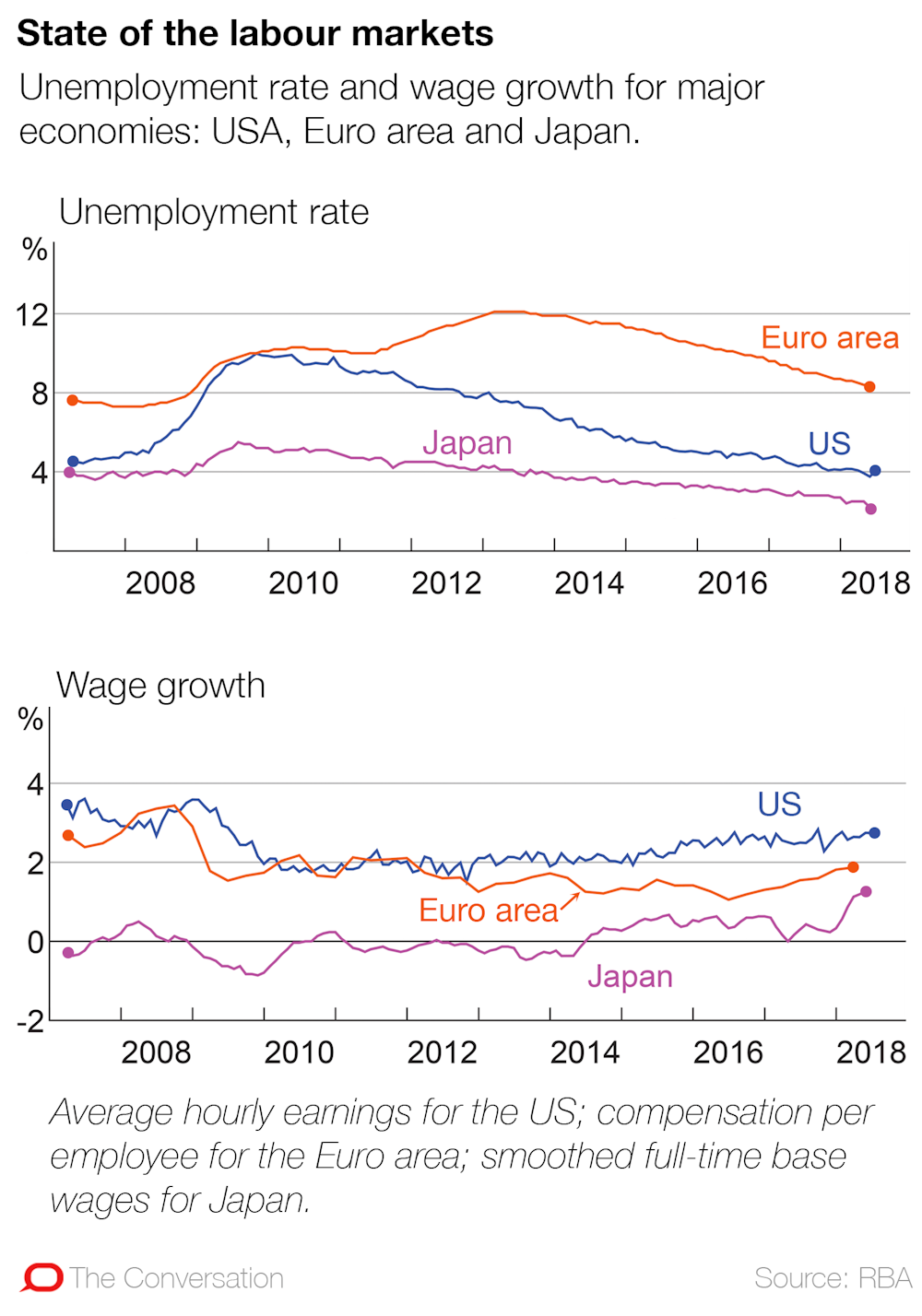

Increased inequality and low wage growth are constraining economic growth. But why is wage growth so low? And how should policymakers respond?

Income inequality has increased significantly in most advanced economies since the early 1980s. In particular, very low rates of wage increase are widely blamed for the weak growth in aggregate demand this century and secular stagnation since the Global Financial Crisis. The GFC was itself brought on by the rise in consumer debt that was used at first to support demand in an attempt to offset the impact of weak wage growth.

Fairfax columnist Ross Gittins recently noted that “many economists were disappointed by this week’s news … that consumer prices rose only 2.1%”. That was because low inflation is “usually a symptom of weak growth in economic activity and, in particular, of weak growth in wages”.

Thus, today it is widely agreed that wages need to increase faster. The OECD, the IMF, leading US scholars, former US Treasury Secretary Larry Summers, Nobel prize winner Joseph Stiglitz and most recently Stephen Bell and I in our book, Fair Share, have all argued that increasing inequality is bad for economic growth.

To solve this problem, the critical issue for policymakers is what is causing this rising inequality and weak wage growth? Unless we better understand the causes, we are unlikely to achieve an effective policy solution.

First, we can quickly dismiss the explanation offered by federal Treasurer Scott Morrison, whose so-called “economic plan” assumes present low wage growth will respond positively to higher company profits. According to Morrison, a company tax cut will lead to more investment and thus more jobs, so eventually the benefits will trickle down and increase wages.

Unfortunately, this logic is the reverse of reality. It ignores the evidence that slow wage growth across all the developed economies has been a problem over a couple of decades now.

Slow wage growth is a continuing long-term problem in the developed economies.CC BY-ND

In fact, the evidence strongly suggests higher profits will not drive higher wages. The benefits of a company tax cut will largely be returned to shareholders, while the only wages that increase will be those of senior management.

Instead, higher investment will require increased consumer demand. And that in turn depends on stronger wage growth. In short, aggregate demand in a flat economy, like ours, is wages-led. Wages drive investment, not the other way around.

Broadly speaking, there are two serious schools of thought about what is causing weak wage growth and rising inequality.

One explanation puts most of the blame on a weakening of trade-union power.

The other explanation emphasises the impacts of technological change and, to a lesser extent, globalisation on the labour market. Together technology and globalisation are said to have changed job structures and demands for skills. They have reduced the share of middle-level jobs, which has directly increased income inequality, and they can depress the demand for labour more generally and thus wages in developed countries, but especially for less skilled labour.

These two explanations are not mutually exclusive – both may have played a role. However, I want to consider their relative significance as the basis for arguing which policy responses should be given priority.

Trade union power in Australia and its impact

A very distinguished professor of labour economics and former Industrial Relations Commission deputy president, Joe Isaac, recently argued persuasively that an important explanation of slow wage growth is “to be found in the change in the balance of power in favour of employers and against workers and unions”.

Isaac starts by noting that union membership in Australia has fallen from about 50% of all employees in the 1970s to the present 15%. This is one of the lowest rates in the OECD.

Isaac also finds some correlation between income inequality (measured by the Gini coefficient) and trade union density for 11 OECD countries. More relevant, though, would be the change in inequality relative to the change in union membership, especially as Australia has always had a relatively high Gini coefficient.

Isaac argues that this loss of membership and the reduced authority of the Fair Work Commission has weakened the bargaining power of organised labour in Australia. Employers are now able “to determine no wage increase or an increase less than their profits would warrant, with less resistance from workers and unions”. Although Isaac admits that “this conclusion is based on the association over time of union power decline and slow wages growth”, he concludes that “it seems reasonable to claim, at least prima facie, a causal connection between them”.

I am more sceptical. While I wouldn’t rule out any impact on wages and employee conditions from a decline in trade union membership and the possibly associated changes in the power of the Fair Work Commission, I question Isaac’s analysis for the following reasons.

First, it is uncertain how much trade union power has declined as a result of loss of membership. Another test of trade union power is the proportion of wages determined by awards and collective agreements – as Isaac shows, this proportion has largely remained the same in Australia. Indeed, in some countries, such as France, trade union membership has always been very low, but they have a highly centralised system of wage determination, which allows the unions a lot of influence.

Second, other countries have also experienced increases in inequality – much greater than in Australia in most cases – but don’t seem to have experienced any notable loss of union power. For example, some of the biggest increases in inequality over the last 30 years, as measured by the Gini coefficient for final disposable income, have occurred in countries like Sweden, Finland and Germany, which are not associated with any loss of trade union power.

Third, Isaac’s analysis of wage inequality focuses entirely on a decline in the wage share of total factor income. This ignores changes within the distribution of earnings. These latter changes are more important in many countries, and certainly for Australia.

While the wage share in Australia has declined since the 1970s and early 1980s, this was at least partly a result of deliberate policy under the Hawke/Keating governments’ Accord with the trade unions, when it was accepted that the wage share had been too high. Even today the wage share is still higher than in 1960, when the economy was generally considered to be performing exceptionally well.

Fourth, the changes in the distribution of earnings largely reflect changes in the structure of occupations rather than changes in relative wage rates. But trade unions seek to influence wage rates, and it is difficult to see how they can exert much direct influence over the structure of jobs.

For these various reasons, I don’t think the loss, if any, of trade union power can explain much of the increase in inequality in most countries over the last 30 years. It is necessary to look elsewhere for the explanation, and the main driver seems to have been the impact of technological change.

Impacts of technology and globalisation

In Fair Share, Stephen Bell and I examine the causes of increased inequality over the last 30 years in most of the advanced economies. A critical starting point is to distinguish between changes in the job structure and changes in relative wage rates. As we note:

Even if there were no change in relative wage rates, but employment increased faster for both high-paid and low-paid jobs, the earnings distribution would show up as more unequal. What would have happened is that the composition of the top and lowest deciles of earnings would have altered, which would increase the median income of the top decile and reduce the median income of the lowest decile, which would in turn be reported as an increase in the inequality of earnings.

The consensus in the studies we reviewed is that increased inequality of earnings largely reflects the impact of technological change. Globalisation and increased participation in global value chains may also have played a role, but less so in Australia, which we attribute to Australia having a more flexible labour market than, say, America.

We also surmise that increased financialisation and the capture of rents generated by technological change may help explain the very large increase in remuneration for the top 1%.

Interestingly, the OECD specifically rejected the hypothesis that regulatory changes have helped drive any significant increase in inequality. It found that “the net effect of regulatory reforms on trends in ‘overall earnings inequality’ remains indeterminant in most cases”.

Technological change has also driven the fall in the relative price of capital goods. This has led to some substitution of capital for labour. Again, this is “particularly pronounced in industries with a high predominance of routine tasks”, as the OECD notes.

These changes in job structure and the relative decline in the middle-level jobs have been the most important cause of increasing inequality in many countries, including Australia. Technological progress has also led to an increase in the demand for skills. In some countries that has increased the premium paid for skilled labour, but the extent of this depends upon the policy response affecting the supply of skills.

In Australia’s case, Bell and I find that the premium for skills, and consequently relative wage rates, did not change much because of the increase in education and training effort. Accordingly, much of the increase in earnings inequality in Australia reflects changes in the job structure rather than changes in relative wage rates (see also Keating and Coelli & Borland).

So what does this mean for policy?

Consistent with his view that a weakening of trade union power has driven the increase in inequality, Isaac recommends changing the Fair Work Act to rectify “the unbalanced industrial power in the labour market”. I can support most of Isaac’s recommended changes, and especially greater rights of union entry, which should help better police adherence to awards and wage agreements.

I also agree that Isaac’s recommended legislative changes are unlikely to result in unions abusing their increased power. This is because, as he puts it, “there are now prevailing forces, such as global competition and structural changes, which will continue to keep union power in check”.

However, these “prevailing forces” are what really caused most of the increase in inequality, as discussed above. I therefore doubt that these legislative changes will do much to reverse the increase in earnings inequality.

Instead, the best way to respond to the impact of technological change on the job structure and possible associated changes in wage premiums is to improve education and training. Enhanced education, training and labour market policies will help workers adjust to the challenges posed by new technologies and will also spur the adoption of those technologies.

In addition, if the supply of skills thereby increases in line with the increase in their demand, there should not need to be any change in relative wage rates. Although these types of reforms take time, in the end they can boost both aggregate demand and potential output, with benefits all round.

SocietyOne, Australia’s pioneering and leading marketplace lender, has celebrated its sixth anniversary of operations as total lending since inception approaches $500 million.

After making its first loan in August 2012, SocietyOne has now helped more than 20,000 customers thanks to more than $480 million provided by its investor funders.

Based on current lending volumes, SocietyOne expects to achieve $500 million in total lending in September – making it the first marketplace lender to achieve this milestone.

Since the beginning of 2016, total lending has grown nearly 6 times and SocietyOne’s loan book now totals over $220 million, up from $41 million at the start of 2016.

“The last 12 months have represented another year of growth, transformation and progress” said interim CEO Mark Jones.

“We have seen continued growth in lending with more than $150 million originated since our fifth birthday. Lending growth, combined with an improvement in margins and disciplined cost management, has translated to a strong improvement in SocietyOne’s financial performance. At the same time, we have continued to transform and simplify our business to focus on our core marketplace lending activities.”

“SocietyOne’s vision is ‘to be Australia’s leading, most trusted, lending marketplace’ and our mission is to achieve this by ‘providing a better deal for borrowers and lenders, one brilliant funding moment at a time’.”

“We have made good progress over the past year towards our vision and goals.” Among many highlights, Mr Jones noted the:

successful completion of the strategic investor capital raise in January 2018;

strengthening of the leadership team ranks with the appointment of Simon Farrell as Chief Technology Officer and Ross Horsburgh as Chief Credit Officer;

expansion of our distribution reach with the development of a new personal loan offering available through mortgage brokers;

successful implementation of systems and credit processes to ensure readiness for Comprehensive Credit Reporting; and

continued recognition for excellence and innovation through numerous industry awards. Most recently, SocietyOne was recognised in The Australian Financial Review Top 100 Most Innovative Companies List for 2018. “We have come a long way over the past 6 years and our success could not have been achieved without the collective effort of our hardworking and passionate team here at SocietyOne, and the backing of our Board, shareholders and key business partners” said Mr Jones.

“SocietyOne has been at the forefront of ‘fintech’ disruption of the financial services industry in Australia for 6 years. We have a real commitment to customer-first innovation and everything we do is guided by our values of being Transparent; Imaginative; Empowering; One Team; and Connected” said Mr Jones.

Looking ahead to the next 6 months, SocietyOne will be focusing on making further improvements to the customer experience; continuing to build its brand profile; developing new solutions for investor funders; broadening out its broker solution and developing new strategic partnerships; and further investing in its technology capabilities and platforms.

“With more than $60 million in committed investor funding at present, and continued interest from a number of institutions, we are in a strong position to further grow lending over the remainder of the year.”

“The next 6 months will be another exciting period of growth and innovation” said Mr Jones. While there is a lot of work to do, the momentum in the business is really pleasing. By the end of 2018, we will be well positioned for the next phase of growth. We remain on track to achieve operating breakeven by March 2019.”

On 10 August, the International Bank for Reconstruction and Development said it has mandated the Commonwealth Bank of Australia (CBA) as the exclusive arranger of the world’s first bond issuance solely using blockchain technology, via Moody’s.

This is credit positive for CBA because it shows the bank is making headway with significant fintech initiatives, which can help improve its operating efficiency and fend off new competition.

CBA will use the private Ethereum blockchain platform to create, allocate, transfer and manage a new debt instrument debt, dubbed “bond-i.” The transaction will provide a platform for future debt-security issuance using blockchain technology. The use of blockchain for bond issuance can offer efficiency benefits for both issuers and arrangers by simplifying the settlement processes. The technology can be used for both registry and payment systems, consolidating payments by investors and title transfers by issuers into single, instant transactions.

Prior to this transaction, CBA experimented blockchain-based bond issuance with government entity Queensland Treasury Corporation (State of Queensland, Aa1 stable). In January 2017, the bank arranged the issuance of a so-called cryptobond for Queensland, by utilizing blockchain technology. It was a trial transaction carrying no debt obligation, with Queensland acting as both the issuer and investor to test the process.

As discussed in our Bank of the Future report, fintech innovations such as these will help traditional banks reduce operating costs and also mitigate the risk of disruption by new fintech firms

HUB24 and Challenger Limited have announced they are working together to provide Challenger annuities to advisers and clients on the market-leading HUB24 platform.

Challenger annuities will be available to advisers and their clients on HUB24 via the innovative technology of ConnectHUB – a collaboration between HUB24 and their subsidiary Agility Applications.

ConnectHUB allows product solutions to be rapidly and seamlessly integrated and provides advisers and their clients with a complete view of their portfolio. Advisers will be able to purchase annuities for their clients as they would any other investment on HUB24.

The teams at Challenger and HUB24 are now working together to build the solution.

Andrew Alcock, Managing Director of HUB24, said: “We are committed to continually enhancing our platform and providing choice for our advisers and their clients.

“We’re delighted to be working with the team at Challenger who are well-known for providing market-leading retirement solutions to deliver their products to our rapidly growing client base.”

Challenger Chief Executive Officer Brian Benari said: “HUB24 is one of the fastest growing platforms in the market and is recognised for its innovation and customer focused approach.

“This relationship further demonstrates superannuation industry leaders moving to meet the needs of retirees as lifetime income stream products become a mainstream option in retirement.”

Challenger is an investment management company that is focused on providing customers with financial security for retirement. It is Australia’s largest provider of annuities.

The Australian Stock Exchange-listed HUB24 connects advisers and their clients through innovative solutions that create opportunities. The business is focussed on the delivery of the HUB24 platform and the growth of its wholly owned subsidiaries Paragem, a financial advice licensee, and Agility Applications which provides data, reporting and software services to Australian stockbroking and wealth management market. HUB24’s award-winning investment and superannuation platform offers broad product choice and an innovative experience for advisers and investors. Its flexible technology allows advisers and licensees to customise their platform solution to fit their individual business, so they can move faster and smarter. It serves a growing number of respected and high profile financial services companies.

Challenger Limited (Challenger) is an investment management firm that is focused on providing customers with financial security for retirement. Challenger operates two core investment businesses, a fiduciary Funds Management division and an APRA-regulated Life division. Challenger Life Company Limited (Challenger Life) is Australia’s largest provider of annuities.

Global, online SME lender OnDeck has reached a new milestone for the value of loans written since it entered the market, just over 10 years ago, via Australian Broker.

With operations across the US, Canada and Australia, the OnDeck Group has lent more than US$9 billion to more than 80,000 small business customers.

Demonstrating the strength of the local market, the group’s Australian business contributed significantly to the total and Australia is now the second largest alternative finance market in the APAC region, behind China.

Cameron Poolman, COE of OnDeck Australia said, “The Australian market is growing at 37% annually. However, while the total size of the alternative finance market in Australia is now 25 times the size it was in 2013, our market is still an emerging on-line lending market,”

OnDeck’s own data shows a number of pain points in the SME finance landscape and the lender has regularly called for better financing options for small and medium sized enterprises.

One in five Australian small businesses are unable to take on new work because of cash flow restrictions and nine out of 10 small businesses report better cash flow could improve revenue by an average of 11.7%.

Despite the challenges, Poolman expects the market will continue its strong growth trajectory and will likely reach maturity in less than six years; a process that took 12 years in the US.

OnDeck was one of six online lenders that signed the new fintech code of lending last month. The code was developed by the Australian Finance Industry Association (AFIA), the Australian Small Business and Family Enterprise Ombudsman (ASBFEO), SME advocate theBankDoctor.org and industry association FinTech Australia.

I wanted to know how he had been able to grab the $500m of the $100 billion market, and specifically whether it was the appetite for P2P which was growing, or whether there were particular elements which had made the difference, given the 60 people working in the business, plus the external technology platform provider.

I wanted to know how he had been able to grab the $500m of the $100 billion market, and specifically whether it was the appetite for P2P which was growing, or whether there were particular elements which had made the difference, given the 60 people working in the business, plus the external technology platform provider.