Mckinsey says that Consumer adoption of digital banking channels is growing steadily across Asia–Pacific, making digital increasingly important for driving new sales and reducing costs. The branch-centric model is gradually but unmistakably giving way to the mobile-centric one.

Deferring the development and refinement of a digital offering leaves a bank exposed to the risk of weakened relationships and lower profitability. Now is a critical moment to draw retail-banking customers toward Internet and mobile-banking channels, regardless of the general level of network connectivity in a given market.

Our annual study, the Asia–Pacific Digital and Multichannel Banking Benchmark 2016, was led by Finalta, a McKinsey Solution, and examined digital consumer-banking data collected between July 2015 and July 2016 from 41 banks. This article focuses on our findings from Australia and New Zealand, Hong Kong, Malaysia, Singapore, and Taiwan, examining consumer digital engagement, user adoption, and traffic and sales via Internet secure sites, public sites, and mobile applications.1 We detail three counterintuitive findings, and make suggestions for how banks should move forward.

Three counterintuitive findings

Consumer use of digital banking is growing steadily across all five markets (Exhibit 1). In the more developed markets of Australia and New Zealand, Hong Kong, and Singapore, growth in recent years has been concentrated in the mobile channel. Indeed, among some banks use of the secure-site channel has begun to shrink, as some customers enthusiastically shift most of their interactions to mobile banking. In emerging markets, growth is strong in both secure-site and mobile channels.

Exhibit 1

Three counterintuitive findings point to the need for banks to act aggressively to improve their use of digital channels to strengthen customer relationships.

First, banks can excel in their digital offering despite limitations in the digital maturity of the markets they serve. One measure of digital maturity is the Networked Readiness Index (NRI), published annually by the World Economic Forum. This scorecard rates how well economies are using information and communication technology. It examines 139 countries using 53 indicators, including the robustness of mobile networks, international Internet bandwidth, household and business use of digital technology, and the adequacy of legal frameworks to support and regulate digital commerce. Comparison of digital-banking adoption with the level of networked readiness reveals that a country’s level of digital maturity does not necessarily promote or inhibit the growth of a bank’s digital channels.

Singapore, for example, has the most highly developed infrastructure for digital commerce in the world. However, when it comes to digital banking, Singaporean banks trail their peers from the less-networked markets of Australia and New Zealand, where banks have been able to draw consumers to digital channels despite gaps or weaknesses in digital connectivity.

Some banks have also been successful in pushing mobile banking regardless of network limitations (Exhibit 2). While Australia and New Zealand have moderately high levels of third-generation (3G) and smartphone penetration (trailing both Hong Kong and Singapore), the banks surveyed have achieved much stronger consumer adoption of mobile channels than their peers in other markets.

Exhibit 2

The second key finding is that having a relatively small base of active users does not necessarily mean low traffic (Exhibit 3). Among all participating banks in our survey, banks in Malaysia report among the smallest share of customers using the secure-site channel; however, these customers tend to log on many times a month, and the typical secure-site customer interacts with the bank more than twice as often as the secure-site banking customers of participating banks in Hong Kong and Singapore.

Exhibit 3

Third, the survey data reveal wide variations in performance across key metrics by country. In Australia and New Zealand, for example, there is wide variation in digital-channel traffic, with customers logging on with 32 percent more frequency at participating banks in the upper quartile than those in the lower quartile. In Hong Kong, digital adoption among upper quartile peers exceeds that of the lower quartile peers by ten percentage points. Participants in Singapore observe a sixteen-percentage-point gap between the upper and lower quartile peers in the proportion of sales through digital channels.2 The wide gap between best and worst in class in multiple markets points to a significant opportunity for banks to beat the competition with compelling digital offers.

What banks should do

Banks in emerging markets have an opportunity to leapfrog to digital banking. Despite gaps in technology and smartphone penetration, a number of banks have tapped into consumer segments eager to adopt digital channels. Banks in emerging markets should prepare for rapid consumer adoption of digital channels. The digital evolution in emerging markets will differ considerably from the trajectory of banks in more developed markets.

Banks in highly developed markets have room to grow their active user base and digital sales. Indeed, the cost and revenue position of banks that do not act to improve their digital offering may weaken relative to peers that shift more business to digital channels. Banks in all markets should plan for this transition, especially through the integration of diverse technology platforms, the consolidation of customer data across multiple channels, and the continuous analysis of customer behavior to identify real-time needs. It is important to build services rapidly and to go live with minimally viable prototypes in order to attract early adopters—these digital enthusiasts eagerly experiment with new features and provide valuable feedback to help developers.

The significant variation of performance among countries shows great potential for banks to boost digital engagement with a dual emphasis on enrollment and cross-selling. Banks should carefully consider four best practices that often bring immediate gains by streamlining the customer’s digital experience:

Deliver credentials instantaneously upon in-app enrollment. The global best practice shows that banks that issue credentials instantaneously through in-app enrollment see their mobile activity rise on average 1.5 times faster. Of the banks that provided data on functionality, more than 50 percent do not have in-app enrollment. This presents a significant value-creation opportunity.

Simplify authentication processes to make them both secure and user friendly. Approximately three in five banks surveyed lack the ability to authenticate a user’s mobile device. In our experience, banks that store device information and allow users to log on simply by entering a personal identification number or fingerprint see three times more digital interaction than banks that require users to enter data via alphanumeric digits each time they log on.

Implement ‘click to call’ routing to improve response times. Instead of using a voice-response system, where customers must listen to a long list of options before selecting the relevant service choice, an increasing number of mobile apps are adopting click-to-call options for each segment, enabling customers to bypass the voice-response menus. Of the banks that provided data on capability, only 30 percent in our Asia–Pacific survey offer authenticated click-to-call options. The improvement in customer service is significant, with global banks able to improve the speed of answering customer calls by up to 40 percent.

Make digital sales processes intuitive and simple. Take credit cards as an example: best-practice global banks achieve average conversion rates (the ratio of page visits to applications) some 1.6 times those of Asia–Pacific banks. They do this by presenting products and features for which a customer has been prequalified through an intuitive, easy-to-read dashboard display or via tailored messages. Application forms are prefilled automatically with customer data. With intuitive and simple applications, banks in the Asia–Pacific region could increase the rate of completed applications by 22 percent, to come up to par with global best-practice banks.

Across the five markets we focused on, the branch-centric model is gradually but unmistakably giving way to the mobile-centric one. Looking at how digital-channel adoption and usage is evolving, along with the diversity of scenarios, banks have ample room to win in their target markets with a carefully tailored digital offering. Digital-savvy consumers warm quickly to well-designed and easy-to-use digital-banking channels, often shifting to the new channel in a matter of days. Banks need to act quickly to improve their customers’ digital experience or risk being left behind.

Cryptocurrencies such as bitcoin may have captured the public’s fancy – and also engendered a healthy dose of skepticism — but it is their underlying technology that is proving to be of practical benefit to organizations: the blockchain. Many industries are exploring its benefits and testing its limitations, with financial services leading the way as firms eye potential windfalls in the blockchain’s ability to improve efficiency in such things as the trading and settlement of securities. The real estate industry also sees potential in the blockchain to make homes — even portions of homes — and other illiquid assets trade and transfer more easily. The blockchain is seen as disrupting global supply chains as well, by boosting transaction speed across borders and improving transparency.

These uses are merely the tip of the proverbial iceberg for a nascent technology whose development stage has been compared to the early years of the internet. “We’re very early in the game,” said Brad Bailey, research director of capital markets at Celent, at a recent Blockchain Opportunity Summit in New York. He likened the blockchain’s current status to the web of the early 1990s, heralding a coming wave of new ideas and uses. “This will impact the world.”

The blockchain technology came about initially as a way to verify bitcoin transactions online and to enable two parties to transact business without having to know or trust each other. It was designed without a central authority in mind, such as a bank or government, to oversee transactions. Essentially, the blockchain is a shared virtual public ledger where encrypted transactions are confirmed by outside parties. In the bitcoin world, these outside parties are called “miners” — computers that solve complex mathematical problems to confirm transactions and earn fees. Confirmed transactions are placed in a “block” and added to the chain. Since the ledger is shared by everyone on the network, it is thought to be nearly impossible to remove or change the data – a premise that turned out to be false in some cases.

Today, the concept of the blockchain has expanded beyond its use by cryptocurrencies. Instead, the benefits of the shared ledger and its seemingly immutable record of transactions accessible to multiple parties are being explored by a variety of industries. Experts said there won’t be a “mother blockchain,” but multiple ledgers with different purposes. Varying versions of blockchains have popped up, too: While the original bitcoin blockchain was open to anyone, some companies’ blockchains are private and “permissioned” — they restrict access to approved parties. The latter approach is preferred by companies fearful of being hit with government fines and lawsuits if they get hacked, said summit participant Sarab Sokhey, chief technology leader of new product innovations at Verizon Wireless. They’ll stay private until the technology matures and industry standards are set.

While the blockchain’s business applications are clear, it has social implications as well. For instance, it can create identities for individuals apart from those sanctioned by governments and not limited by geographic boundaries. The blockchain also allows less-technologically advanced nations to participate in global transactions more easily. “Blockchains are exciting, undoubtedly,” said Saikat Chaudhuri, executive director of the Mack Institute for Innovation Management, which was an official partner for the summit. “It’s much more than about transaction efficiency or flexibility. It’s really beyond that. It could provide an identity to those who don’t have it, or promote financial inclusion. Therein lies the power of this whole thing.”

‘Nervous’ Financial Institutions

According to a survey by the IBM Institute for Business Value and the Economist Intelligence Unit, one in seven companies it calls “trailblazers” expect to have blockchains in production and at commercial scale in 2017. Respondents were interested in taking advantage of the blockchain’s multiple benefits, which include cost reduction, immutability of records, transparency of transactions and the potential to create new business models. For example, the blockchain would eliminate the need for keeping multiple records at banks and other parties doing currency trades. The survey tracked responses of 200 global financial markets institutions.

The survey also said “trailblazers” were focusing their efforts on the following business areas: clearing and settlements, wholesale payments, equity and debt issuance and reference data. The report added that in recent years, financial institutions have “swarmed to blockchain pilots and proofs of concept” — opening innovation labs, holding hackathons, partnering with financial technology startups, joining consortia and collaborating with regulators.

To be sure, banks have a vested interest in participating. “Banks provide essentially escrow services for the transfer of value, and here comes a technology that threatens to eliminate that service,” said Chris Ballinger, global chief officer of strategic innovation at Toyota Financial Services. “So they are nervous about that, because it’s a huge revenue stream” that could be taken away. How? “With the blockchain, you can run a network that transfers value among untrusted nodes, and therefore you can eliminate the middle man and you can eliminate all the costs associated with the middle man,” he said. “You’re essentially turning assets into something like cash that you can hand to somebody and they will accept. That makes the transfer of assets extremely efficient.”

Another unique benefit of the blockchain is that it separates someone’s identity from the transaction they’re making. In general, a blockchain uses a digital signature – not real names and other personal information – that is activated by a private key or secret code held by the one doing the transaction. Compare that to current credit card or bank transactions, which tie one’s personal information such as a name and address to purchases and other financial activities. This separation improves the security of one’s data. “Today, the payments information and identity are [bound] together. The combined is a tempting honey pot for hackers,” Ballinger said. “By separating the financial information from the identity, there’s no honey pot, no central place to hack, no incentive to go after.”

In December 2015, Nasdaq executed its first trade on a blockchain, through its Linq ledger. The exchange said the blockchain promises to expedite trade clearing and settlement – all the steps needed to transfer the asset from seller to buyer including recording the transaction — from three days to as little as 10 minutes. That’s because the trades remove many manual processes and bypass third parties. As such, “settlement risk exposure can be reduced by over 99%, dramatically lowering capital costs and systemic risk,” according to Nasdaq. Other stock exchanges tinkering with the blockchain include ones in Australia, Myanmar, Germany, Japan, Korea, London and Toronto.

Overstock.com is on the cusp of issuing its first security using the blockchain. “We are in the process of proving out the first public trading of a blockchain security,” said Ralph Daiuto, Jr., general counsel of tØ, a subsidiary of the e-commerce retailer. While the company has kept its clearing firm, it is using digital wallets for the actual transfer of assets in settlement of the trade. “The goal is to shorten the settlement cycle and [avoid] all the ills that can go wrong with that cycle.” He added that the company can cut its equity trading costs by 70% using the blockchain.

Overstock got regulatory approval for its blockchain trade by taking “incremental steps in proving out the technology in use cases and demonstrating we have real-world application for this blockchain technology,” Daiuto said. “It literally has been a monthly, if not a weekly, education process with our core regulators.” It has taken nearly two years of laying the groundwork for Overstock to get to this point.

Real Estate and Smart Contracts

An area of particular promise for the blockchain is the real estate market. “The blockchain solves pretty much every problem in real estate that we have” in terms of fraud, middleman fees and friction, opaque due diligence, slow price discovery, complex transaction process and other ills, said Ragnar Lifthrasir, president of the International Blockchain Real Estate Association. “In many ways, our technology is still in the 17th century – notaries still use seals.” The blockchain promises to simplify and speed up the process while adding transparency to the records.

For example, in selling a house, people still sign paper deeds over to the new owner. It has to be entered into the public record, which means someone physically has to go to the local government office. “It’s a paper-based system that is ripe for fraud,” Lifthrasir said. The blockchain solution is fairly straightforward, using digital deeds. “When I want to transfer the property, I simply transfer it from my wallet to the buyer’s wallet.”

As for putting the property ownership on the public record, he said the list is already on the blockchain so recording it won’t be hard. Lifthrasir added that validation of ownership would be strengthened. “It’s very difficult to deny who owns the property when it’s on a public network.” His startup, Velox, is working with Cook County in Chicago to use the blockchain for transferring and recording property titles. It is also working on a way to show liens on titles on the blockchain.

Within a blockchain, so-called “smart” contracts could be revolutionary. “They programmatically represent a contract,” said Mark Smith, CEO of Symbiont and co-chair of the Smart Contract Council. For example, a smart contract on an auto loan could be linked in real time to payments made by the car buyer. If he misses payments, the contract gets wind of the violation and starts the repossession process. In Delaware, Smith’s company is working with the state to create “smart” records of its public archives to do such things as being able to sunset themselves.

EY’s Australian operations piloted a real estate blockchain ecosystem that is now being used in the market to trade full, and even fractional, ownership of properties. Real estate and financial institutions approved by EY all liked the idea of using a blockchain, but when it came to actual implementation, “fear and uncertainty crept in,” said James Roberts, partner and Australian blockchain leader. EY had to essentially guarantee verification of participants and transactions to build trust. “We decided we would solve the identity problem [of people and institutions]. We would build trust into the system and prove recordkeeping is true and accurate and can be used to transact financial instruments like property or debt.”

EY’s blockchain ecosystem goes through several stages. First, individuals using the blockchain have to be validated using identity checks and even biometrics. They create records on the blockchain using randomly generated unique keys that let EY do further checking against various databases from the government and elsewhere. Next, the transaction is traded on a blockchain exchange. The assets being traded are verified. The entire ecosystem is private and permissioned. Also, EY stores individuals’ unique keys offline for security. Moreover, EY built back-system administrative functions – despite the premise of the blockchain as not having a central authority – to make participants more comfortable in using the system. But to be a viable ecosystem, it needs to scale. “We need millions and millions of people in our system, and that’s going to take a lot of effort,” Roberts said.

Challenges and Risks

Security is still the biggest challenge confronting the blockchain. “The truth is, once you give someone access to a network, many times, more often than not, they can end up very easily getting blanket access to that network,” said Joe Ventura, CEO of AlphaPoint. “This is a huge security problem.” However, if one ends up building many protections to prevent hacks, then it bogs down the blockchain and defeats its purpose in the first place. “Basically, you have to jump through so many hoops simply to pass the message from some party to another party.”

And while blockchain records theoretically can’t be changed, there are ways around that. Smith cited a recent controversial decision by the Ethereum Foundation – the organization behind the open-source cryptocurrency Ethereum – after a hacker exploited a software flaw and took funds. The foundation decided to roll back the clock to give people their money back and created two versions of the ledger. “Imagine if you’re a business and they roll back a day,” Ventura said. “That’s completely unacceptable.” Moreover, by creating two versions, some people were able to exploit it. “People were able to double their money,” Smith said.

As for compliance, at least regulators could have a node on the blockchain itself in which companies define their access to data, said Sandeep Kumar, managing director of Synechron. As such, regulators wouldn’t have to wait days for a bank to hand over documents for compliance. “They can see it as it is happening.”

In the end, each company has to figure out whether a blockchain is suitable. “Is it a blockchain use case or is it a database use case?” said Tyler Mulvihill, director of Consensys. “If you are a company that has a lot of information internally and you don’t transact like a lot of vendors, and not a lot of people need to use your information or do business with you, a database can be fine for a lot of things. It’s when you have a lot of parties that need trust, need access to certain information and need to be audited – that’s where I see the biggest use cases.”

Governments across the globe are experimenting with the blockchain, the technology behind Bitcoin, as a way to reduce costs and provide more accountability to the public. In Europe alone, the United Kingdom, Ukraine and Estonia are experimenting with blockchains to fight corruption and deliver public services.

Rather than siloing our data in government agencies, we could create a single source of information. This would speed up our interactions with government, while reducing errors and fraud.

What is a blockchain?

The blockchain is a kind of public database, one stored simultaneously on a bunch of different computers. When a new transaction occurs it is verified (otherwise known as “mining” or “consensus”), encrypted and added to the database.

For the government’s purposes, the killer feature of the blockchain is that it is a way to record transactions so that they are transparent and cannot be altered or tampered with. When used to track fish through a supply chain, for instance, it allows customers and restaurants to follow where the fish has been and have confidence in the data.

When applied to a government context, these capabilities could be useful for collecting tax, delivering benefits, or regulating business. From the public’s point of view, this could enable us to track government spending, eliminate fraudulent transactions, reduce errors in data processing and speed up service delivery to almost real time. It could be useful almost anywhere records are kept.

All the while the public could be more confident about the accuracy and integrity of the data being held.

In practice

The Australian government makes benefit payments and provides support services through Medicare, Centrelink and Child Support services. It also collects information through numerous other agencies, such as the Australian Tax Office. A government blockchain could record the transactions about a citizen and link together information about health, welfare and child support.

The information would be entered only once into the blockchain by any one of these agencies. There would be no need for the data to be re-entered or matched again. Thus errors that occur in data processing as information is passed on down the line will be eliminated, avoiding some of the issues with the current Centrelink system.

Further, once data is entered it cannot be altered or changed in any way without proper authentication. Any authorised officer within the government could then access the information in the blockchain, avoiding a paper-pushing exercise between government departments. All of your data would be in one place.

We could go even further, as the blockchain would also allow other services to be processed through an app, as the UK is trialling with welfare payments.

The overall cost savings, reduction in bureaucracy and increased responsiveness to helping people in need could be immense. All we need is the government to invest in its own blockchain.

The challenge is making it legitimate

The essence of a blockchain is to reduce the reliance on centralised systems (such as the government), replacing it with a system with inherent accountability, transparency and trust. The original blockchain concept achieved this by being open, like the internet (also known as unpermissioned), relying on independent, anonymous “miners” to validate transactions. This guarantees the integrity of the data as no-one knows who the miners are to bribe or bully them into underhanded actions.

However, some might view a government-run, “permissioned” blockchain with suspicion. The trust of the public would need to be gained. A government blockchain would not be open, and we would have to rely on the government to approve all of the transactions. This negates some of the benefit offered by a blockchain. The legitimacy and trust would have to come from the government itself.

Thus a government-run blockchain would not be without its challenges. But if an Australian government blockchain is developed and allowed to succeed, then the potential benefits could be enormous. Society as we know it will be disrupted!

Author: Christine Helliar, Professor School of Commerce, University of South Australia

ANZ today announced its customers can continue to use their digital wallets when they report their card as lost or stolen with a new service that automatically updates their replacement card details.

As soon as a customer calls to report their debit or credit card as missing, ANZ puts a stop on the original card and automatically uploads the new virtual card details to the customer’s digital wallet.

ANZ Managing Director Products Australia, Katherine Bray said: “Our customers report about 670,000 cards as lost or stolen each year and we know waiting for a new card to arrive can be a real inconvenience.

“Now our customers can keep using their digital wallet, whether it’s Apple Pay or Android Pay, to make purchases while they wait for the new physical card to arrive in the mail.

“For many customers their smartphone is now the primary way they do their banking, including making purchases, so we’re working hard to keep improving their mobile experience with changes like this.”

ANZ has also made it possible for customers to keep their existing Personal Identification Number (PIN), provided it hasn’t been compromised, meaning less change with the same high level of security.

ANZ is the only major Australian bank to offer both Apple Pay and Android Pay with about 8.3 million transactions made across the bank’s digital wallets last year.

Mckinsey in a new report “A brave new world for global banking“, says three formidable forces—a weak global economy, digitization, and regulation—threaten to significantly lower profits for the global banking industry over the next three years. Developed-market banks are most affected, with $90 billion, or 25 percent, of profits at risk, but emerging-market banks are also vulnerable, especially to the credit cycle. Countering these forces will require most banks to undertake a fundamental transformation centered on resilience, reorientation, and renewal.

Our report, A brave new world for global banking: McKinsey global banking annual review 2016, finds that of the major developed markets, the United States banking industry seems to be best positioned to face these headwinds, and the outcome of the recent presidential election has raised industry hopes of a more benign regulatory environment. Japanese and US banks have between $1 billion and $45 billion in profits at risk by 2020, depending on the extent of digital disruption. Yet after mitigation, their profitability would drop by only one percentage point to 8 percent for US banks and 5 percent in Japan. Banks in Europe and the United Kingdom have $35 billion, or 31 percent, of profits at risk; more severe digital disruption could further cut their profits from $110 billion today to $50 billion in 2020, and slice returns on equity (ROEs) in half to 1 to 2 percent by 2020, even after some mitigation efforts (see exhibit for how digitization may reduce fees and margins across different businesses).

Exhibit

Emerging-market banks face a different challenge. They are structurally more profitable than their developed-market counterparts, with ROEs well above the 10 percent cost of capital in most cases but vulnerable to the credit cycle. Brazil, China, and Russia could have $50 billion in profits at risk, with China comprising $47 billion. A slower growth scenario could result in additional credit losses of up to $250 billion, of which $220 billion would be in China, our report finds, but with their current high profitability of $320 billion, Chinese banks should be able to withstand these losses.

Three formidable challenges

Banks must adapt to the reality of a macroeconomic environment that offers a number of risks and limited upside potential. Along with stagnating growth, banks face enormous challenges to digest the wave of postfinancial-crisis regulation, despite industry hopes of a more benign regulatory environment in the United States. Control costs in risk, finance, legal, and compliance have shot up in recent years. And additional proposals, termed “Basel IV,” are likely to include stricter capital requirements, more stress testing, and new guidelines for conduct and compliance risk.

Meanwhile the pressures of digitization, which boosts competition and compresses margins, are growing. Some emerging-market banks are managing well, offering innovative mobile services to customers. But our report finds that in the largest emerging markets, China and India, banks are losing ground to digital-commerce firms that have moved rapidly into banking.

In developed economies, digitization is impacting banks in three major ways. First, regulators, who were initially more conservative about the entry of nonbanks into financial services, are now gradually opening up. Over time, huge tech companies may be able to insert themselves between banks and their customers, capturing the vital customer relationship and presenting an existential threat. On the positive front, a number of banks are teaming up with fintech and digital firms, using big data and analytics to sharpen risk assessment and drive revenue growth. Lastly, many banks have been able to digitize processes and dramatically lower costs in their middle and back offices (although digitization can sometimes add costs).

A fundamental transformation

Countering the headwinds now gathering force means most banks will need to embark on a fundamental transformation that exceeds their previous efforts. Tinkering around the edges, as many banks have done for years, is not adequate to the scale of the task and will only exacerbate the sense of fatigue that comes from years of one-off restructurings.

This transformation is centered on three themes:

Resilience. Banks must ensure the short-term viability of their business through tactical measures to restore revenues, cut costs, and improve the health of the balance sheet. They need to protect revenues through repricing and greater intermediation, reduce short-term costs, manage capital and risk, and protect core business assets. Our report found that digitization is only the start of the answer on costs, with radical reductions in functional costs needed to fundamentally rebase the cost structure.

Reorientation. While the resilience agenda is defensive in nature, in reorientation, banks go on offense. They must reorient their business models to the customer and the new digital environment by establishing the bank as a platform for data and digital analytics and processes, and aggressively linking up with fintechs, platform providers, and other banks to share costs through industry utilities. They also need to streamline their operating models and IT structure and move toward a proactive regulatory strategy.

Renewal. The industry must move beyond traditional restructuring and renew the bank via new technological capabilities, as well as new organizational structures. Any new business model that banks design will likely require new technology and data skills, a different form of organization to support the frenetic pace of innovation, and shared vision and values across the organization to motivate, support, and enable this profound transformation.

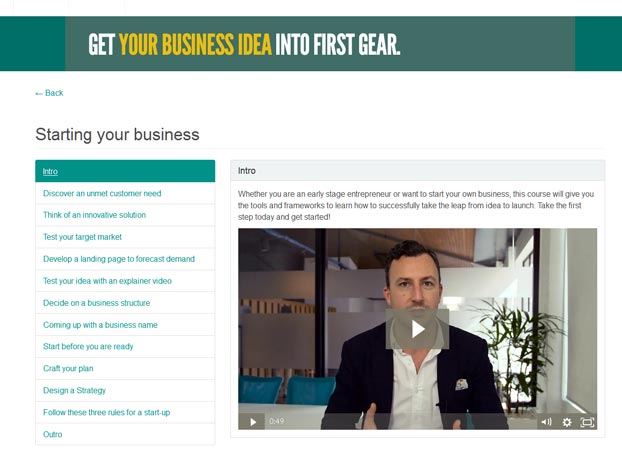

Suncorp Start Company, a new online platform, brings together a diverse range of services and solutions to create a user-friendly guide for aspiring entrepreneurs.

Suncorp Customer Platforms Chief Executive Officer Gary Dransfield said the website connects customers with resources like legal and accountancy documents, business name registration forms and website development tools, which are essential to starting a business.

“It also provides access to educational tutorials, tips and plans to help recently established and trading businesses to take the next step,” Mr Dransfield said.

“Our research tells us that small businesses want to spend more time on building their business, not completing paperwork – early access to the right tools and information can set them up for faster success.

“With Suncorp Start Company we consolidated solutions from our partner companies and insights from customer feedback to develop a product which solves problems and helps to meet their needs.”

The new platform follows Suncorp’s partnership with 9 Spokes to bring to the market ‘Suncorp Business Toolbox’ – a business dashboard that enables customers to gain insights across their business.

“We know small businesses are busy. Suncorp is committed to making it easier for them to achieve their financial goals through solutions and services which are easily available as part of our new Marketplace strategy,” Mr Dransfield said.

The 10th anniversary of the Apple iPhone reminds us that while it was not the first smartphone, it was the first to achieve mass-market appeal. Since then the iPhone has defined the approach that other smartphone manufacturers have taken.

Smartphones have transformed our lives, essentially giving us an internet-connected computer in our pocket. But while we’re distracted by Candy Crush or Pokemon Go, we are losing freedoms. We are losing control of our own devices, and losing access to the information they contain – in the very same devices that are increasingly important in our life.

To see how far we’ve come, consider that personal desktop computers only became widespread with the IBM PC. By designing the PC with an open architecture, an enormous industry of PC-compatible products from other manufacturers sprang up. It’s the same today: when you purchase a computer, you’ll have (if you wish) the ability and the right to add or remove, swap or upgrade any element of the system hardware, install or remove any software you wish, including the operating system, and access to any information stored on it.

However, today the smartphone or tablet have in many cases effectively replaced the desktop or laptop computer. In parts of the developing world, smartphones are the first experience many have of computing and internet access. The fact that they are small and portable and work wirelessly means they are put to many other uses, such as receiving guidance from navigation systems, listening to music while exercising, or playing games in waiting rooms.

Yet doing something that’s very simple on a computer – such as listing your files – is impossible on an iPhone. iPhone users can change their background image, their ring-tone, the time of their alarm. But the iPhone guards what files it contains jealously. Your phone that is carried everywhere with you, which knows your precise location, which records the websites you visit – has all of its files completely inaccessible to you. If you care about privacy this should sound disturbing.

We have always had the right to govern our own computers, to do with them as we wished. But the smartphones and tablets we’re buying today come without administrator rights: we are merely users in the hands of the big tech companies, and these firms effectively rule the machines we live with.

Information and freedom

Of course, the iPhone does allow access to some information, such as photos, emails or documents. But it is often difficult to get that data off the phone. The way the iPhone communicates with your computer is a closed, proprietary protocol, and Apple changes this protocol each time it updates the phone. So if you use neither Microsoft Windows or Apple Mac computers you will have a hard time even to get your own photos out of your own phone.

Apple also restricts what information can be stored on the device. For example, iPhone users are obliged to transfer any music files on the phone through Apple iTunes software. If you cannot or do not wish to run iTunes – no music for you. Additionally, iTunes will automatically delete all the music tracks on your phone if you try to transfer files from more than one computer, due to digital rights management software that assumes that access from more than one computer means that the file has been shared illegally. It’s a bit like buying spectacles that control the conditions under which you’re allowed to read books. Or a backpack that will destroy all its contents if you attempt to carry items bought from different stores.

The same issue also affects which applications can be installed. If you learn how write code, you can develop your own applications to solve your own unique problems. But the iPhone doesn’t allow you to run those programs: only software authorised by Apple and distributed via the Apple Store is permitted.

Open alternatives

Why so tightly control what we can do with our devices? Some may argue that these restrictions are necessary in favour of security. If we look again at computers, however, we find that Linux, an open source non-commercial operating system, is also the most secure. It’s true that the Android mobile phone operating system, which is more open, is not as secure as the iOS operating system that runs Apple’s iPhone. But it shows that it is possible to have a system that is both secure and open.

In fact, iOS is built around several open source software projects – those whose internal workings are open to anyone to view or modify, for free. But while elements of iOS are open source, they are used as part of a tightly closed system. Android, an open source mobile phone operating system originally created by Google, is the chief alternative to the iPhone. But Android phones too have many closed source components, and Google is constantly replacing open components with closed source ones.

Another alternative comes in the form of Ubuntu Touch, a recent version of the popular Ubuntu Linux for phones and tablets, although it is not yet widely used. The fact remains that ten years on, the mobile revolution kicked-off by the iPhone has taken us several steps forward and several steps back; leaving us uncertain of whether some day we will actually fully own our devices.

Author: Leandro Soriano Marcolino, Lecturer in Data Engineering, Lancaster University

The impact technology is having on the financial services industry is immense and getting caught up in the hype surrounding new technologies is all too easy, writes SuiteBox’s Ian Dunbar.

The list of buzzwords that dominate the landscape of tech innovation in financial services grows by the day (and yes, they all have to come with a hashtag). But so what?

It is easy to get swept up in the hype of the industry and forget what the point of all this innovation is.

What defines innovation that changes the shape of an industry and, more importantly, makes a difference to real peoples lives?

I have been to many Fintech innovators conferences and have organised two of them through the Afiniation Fintech Network.

I must have seen more than 500 ‘innovators’ presenting their carefully crafted wares to the eager (or cynical) audience.

But again, so what?

Here is an example of how big a difference technology innovation can make in the convenience of life.

The ‘old banking’ in the story is a big lumbering Australian bank and Visa. The ‘new banking’ is Apple and American Express.

I really wish I had been able to say the star of this story was a super exciting start-up operating from a garage somewhere, but yes, it is Apple and Amex (and how often do you read about Amex in a Fintech blog?)

I was travelling in the UK earlier this year and I managed to lose my wallet.

That is a horrible experience at the best of time, but absolutely the worst experience when sitting at a train station outside of London, heading to Heathrow to catch a flight to Zurich.

Hmm, little money (about 5 quid in change), no cards, no drivers licence. What does one do?

The ‘old bank’ financial services provider:

Emergency phone call to Visa and the bank in Australia – Absolutely no way I can get an emergency card quickly in London, but I can arrange an emergency funds transfer to Western Union in 48 hours.

No worries, I will walk from Zurich Airport to the Airbnb and eat nothing for 2 days!

I borrow 200 pounds from a friend in London (phew) and get on my way.

The problem, no confirmation ever arrives of the emergency funds. I phone Visa and the bank a grand total of seven times. Each time I get one step closer to my emergency funds.

The final hurdle, the bank won’t release the funds because Visa has spelled my address with ‘St’, rather than ‘Street’. Seriously!

Later, when I get back from Zurich to London, I get my emergency card via courier, but my unbranded Visa card comes with no pin and no bank in London has any idea what to do with it.

Four more calls to the bank in Australia and I give up.

The ‘new bank’ financial services innovator:

Wondering how I survived? Straight after the first call with Visa and the bank in Australia, I called American Express to cancel my Amex card and order the new one.

Within 2 hours I received an alert on my Apple Pay Wallet on my iPhone that my new Amex card had been loaded and activated.

No more calls, no need for a pin, no courier.

I survived for the next seven days on the cash I had borrowed and using Apple Pay on my phone absolutely everywhere.

The Tube in London, supermarkets, cafes, shops and Uber – I became the walking example of the cashless society.

The point of this story is not to promote Apple or Amex; they are well and truly big enough to do that without me.

The point of recounting my story is to highlight that technology needs to make a difference, not just a little difference but a big difference.

Combine that with good marketing and excellent management and you have a winner.

So, how to cut through the hype of Fintech? The ‘difference’ can come in a number of ways:

Deliver convenience

Technology should make peoples’ lives easier, much easier. It should cut out the friction in the way we interact with financial services.

By reducing wait times, cutting out painful steps in a process, eliminate repeated identity verifications, eliminate paper, printing and postage, offer services when the client is free, not when you are.

The story above, while being an infrequent occurrence, is all about convenience.

Automated advice tools (whether adviser or consumer led), online FX, virtual meeting rooms, video banking, digital signing, digital mortgages, mobile payments, digital identification and biometrics all fall into the domain of enhancing convenience.

Save people money

Technology shouldn’t save users just a little bit of money – as we consumers don’t generally change our behaviour for a small saving – but offer exceptional value, and that generally means savings.

Innovators in the foreign exchange space are great examples of this.

The large banks are making huge returns on small business and consumer FX, which is now being eroded by new entrants.

Peer-to-peer lending is another example, providing lower cost lending to many individuals that might otherwise be denied credit or use pay-day lenders.

Enhanced security of services:

Cyber-security, identity theft, payments fraud are all huge businesses, and while consumers might not pay for it, businesses will.

In Australia in 2015, some 8.5 per cent of the population experienced some form of online theft, costing over $2.1 billion.

Biometrics (voice, eye, thumb print, facial) are growing rapidly and will make a substantial difference to the security of our online and mobile transactions of the future (forget cards, what will a card be?).

Back the leaders in enhancing the security of our financial transactions.

Create an exceptional customer experience:

The financial services industry is not well known for innovative client facing.

Delivering a mobile app is not enough. A staggering 23 per cent of apps are abandoned after first use and 90 per cent after a month.

Fintech innovators are changing this rapidly, with the use of innovative user experience design, gamification, behavioural psychology and more.

Collate, use and share data to create powerful insights and connected eco-systems

Fintech leaders know how to source and use data. Credit scoring, for example, might use information not just from a credit agency (the majority of the world is not scored in credit bureaus) but also source data from social media.

Wealth platforms may source website search histories and social media to predict consumer behaviours before they occur.

AI engines can assess personality profiles based on written content and social media posts.

Data itself, however, is not enough, but when combined with smart algorithms, powerful and valuable consumer insights are created. These insights are valuable.

Fintech is big and it has the attention of the incumbent financial players globally. Spot the difference that a fintech innovator is making, validate it against objective criteria, and strap in and enjoy the ride.

Ian Dunbar is the chief executive officer of SuiteBox.

Robo-advice platforms’ capacities are expected to continue growing in the coming year, according to Finovate, expanding their functionality to include broader wealth management functions and cater to high-net-worth customers.

The “myriad” financial needs facing Millennials, coupled with increasing longevity risk confronting older investors, has driven change in the robo-advice space, Finovate research analyst David Penn said, with the improving abilities of such services now extending beyond “traditional boundaries”.

“The growing capacity of robo-advisers to help manage other aspects of personal finance supports a more expansive view of wealth management and financial planning,” he said.

“This includes everything from health care planning, insurance, even real estate, education and leisure.”

As robo-advice becomes “both more sophisticated and more accepted”, high-net-worth investors are increasingly making use of these services to manage parts of their finances, Mr Penn said.

“Catering to high-net-worth clients, according to some, involves both greater technological sophistication on the part of robo-advisors as well as more extensive customer service,” he said.

“Specifically, high net worth clients may require access to more complex investment vehicles, including non-equity investments, as well as more advanced rebalancing and tax harvesting than the average investor.”

Fintech services designed to help high-net-worth individuals manage their wealth are already emerging on the market, Mr Penn said, adding that high-net-worth individuals already using these services had increased their investment from 5 per cent to 20 per cent in the last two years alone.

Fintech marketplace operator Cashwerkz has merged with Trustees Australia to create a platform that aims to disrupt the fixed interest investment sector.

According to the companies, the merger helps bring together Trustees Australia’s funds under management with Cashwerkz’s distribution platform to serve retail customers, the financial planning industry, superannuation funds, councils and other entities that are looking to invest large cash balances.

It is hoped the merged companies will allow Australian fixed income investors “to find the best term deposit and fixed income solutions to match their investment criteria and to simultaneously and seamlessly transact term deposits online between banks and buy/sell fixed interest securities, such as small parcel bonds, with or without the involvement of intermediaries”.

The merged platform will enable those seeking a term deposit or a related cash product to access Cashwerkz’s marketplace for cash. It will offer consumers a wider choice of ADIs, including access to regional ADIs such as smaller banks, credit unions and building societies. Likewise, it will offer regional ADIs and smaller banks access to a huge number of potential new consumers.

Brook Adcock, chairman of Adcock Private Equity, the company behind Cashwerkz, commented, “While some incumbents are keen to use the cost and difficulties associated with compliance of cash investments to ‘own’ their clients, consumers in many markets are now empowered by technology to break those compliance shackles and access better deals.

“There is an enormous opportunity to scale the business by expanding into the (before now), too granular and untapped retail market, the up-until-now paper-based middle-market, and the before-now too-time-consuming IFA market.”

Cashwerkz says it aims to expand into new products such as cash management accounts, high interest savings accounts, annuities and bonds.

Further, by retaining its custodial licence, the entity, listed under Trustees Australia, can offer custodial services to small and medium third parties, which it has identified as a gap in the market.