Although subscription-based music services have existed for more than a decade, many still wonder whether Apple Music will again revolutionize the music business, like iTunes. The more important question, however, is what Apple’s entry to the music streaming business will mean for underpaid songwriters.

The promise of online streaming

Online streaming offers many benefits. It allows music fans to access content anytime, anywhere. If Apple Music can include a wider variety of music than Pandora and Spotify, it will move us closer to what commentators have referred to as the “celestial jukebox” – the proverbial place where music is always at our fingertips.

On-demand services also respond well to our changing habits of entertainment consumption. Gone were the days when we sat behind the television set every week waiting patiently for the latest episode of our favorite show. Instead, we now binge watch through cable on-demand, Netflix or Amazon.

Although consumers remain reluctant to pay for online content, last year the music industry received, for the first time, more revenue through online streaming than CD sales. When one takes into account the industry’s 18% equity stake in Spotify – worth about $1.5 billion – the revenue-generating potential of online streaming cannot be overlooked.

The music industry’s (relative) well-being

Music business executives remain vocal about the challenge posed by the internet and new communications technologies. The industry, however, seems to have been doing quite well recently.

Taylor Swift’s latest album 1989, for example, sold more than 1 million copies in the first week alone. Top executives also continue to receive compensation packages worth tens of millions of dollars. The problem with online streaming therefore concerns neither Billboard Top 40 artists nor industry executives.

If anything, the arrival of Apple Music will generate more revenue. Although the industry’s total income may initially decline when some iTunes downloaders switch over to the new subscription-based service – causing reduced sales in digital downloads – that amount will return and grow as the subscriber base expands.

Unfortunately, the same cannot be said about professional songwriters.

Consider Spotify. The service claims a distribution of “nearly 70%” of its revenues to rights holders. According to The New York Times, Spotify “generally pays 0.5 to 0.7 cent a stream (or $5,000 to $7,000 per million plays) for its paid tier, and as much as 90% less for its free tier.”

For a song that has been streamed 10 million times in the paid tier, the total royalties will be between $50,000 and $70,000. This arrangement sounds attractive, until the royalties are divvied up among the record label, the performer and the songwriters (including the composers of both the song and its lyric). If the songwriters receive only 10% of the total royalties, their cut will be between $5,000 and $7,000.

That amount will be further reduced if the 10 million streams also include the free tier. For example, on Pandora – a different service that has similarly meager payouts – Pharrell Williams received only $2,700 in publisher and songwriter royalties for 43 million streams of his Grammy-nominated song “Happy”.

The professional songwriters’ oft-overlooked pain

Thus far, musicians have been highly dissatisfied with the royalty payout from online music services.

For professional songwriters who do not perform, few can earn enough money through these services to put food on the table, pay for electricity and equipment and forgo part-time work. Even for those who manage to bring in additional revenue through concerts and tours, the frequent need to perform and travel takes away valuable writing and recording time.

In a recent interview, Björn Ulvaeus of ABBA said he “doubted spending all that time on writing songs would be possible in a world where Spotify is the main source of income … as [his group] would have had to spend much more time touring in order to make a living.”

If professional songwriters are to succeed in the brave new world of online streaming, a new compensation model will have to be developed.

That model could feature a minimum royalty payout or a higher rate for online streaming. It could also include a small cut of profit from the record labels’ equity in streaming services – some of which was reportedly obtained with very limited up-front investment.

Also worth reviewing is the “blackbox” from which royalties for songs from back catalogs have disappeared. Even though the record label may have received only a fixed sum for licensing its whole catalog, a songwriter whose song has yielded 10 million streams deserves some royalty.

Apple could have revolutionized the music business by charting a new course for compensating professional songwriters. Yet nothing reported thus far – other than the lack of a free service – suggests a more generous royalty payout than Pandora or Spotify.

Potential competition concerns

Apple Music will raise additional questions about competition, affecting musicians and consumers alike.

From Pandora to Spotify to Tidal, virtually all existing streaming services are technology start-ups. Apple, by contrast, is the world’s most profitable company with an enormous war chest and reportedly 800 million credit cards on file.

Once Apple enters the market, it is unclear how effectively the existing services will be able to compete or how many new players can still enter the market. It is no coincidence that iTunes remains the most dominant format for digital music. While Google can certainly stay competitive, it is doubtful that the next Pandora or Spotify could emerge.

It is therefore no surprise that the attorneys general in New York and Connecticut have already launched an antitrust investigation into the music streaming business. Although they have yet to target Apple, the timing of the launch is suggestive – not to mention the company’s recent $450 million settlement of its e-book price-fixing lawsuit.

In sum, despite the considerable attention Apple Music has recently caught, it remains to be seen how this new service will improve the lives of underpaid songwriters. If anything, the service has raised more questions than answers.

Author: Peter K Yu – Professor of Law and Co-Director of the Center for Law and Intellectual Property at Texas A&M University

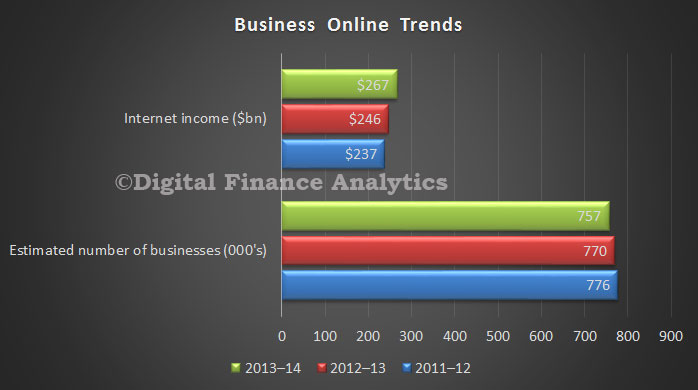

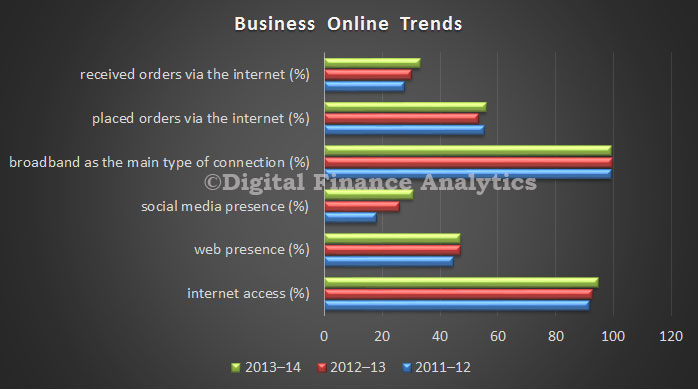

The survey shows a significant rise in a social media presence up 18%, but this compares with a massive 44% increase in the prior year. We also see a rise in orders placed via the internet (up 4%), and fulfilled via the internet (up 10%). Almost all firms have broadband access.

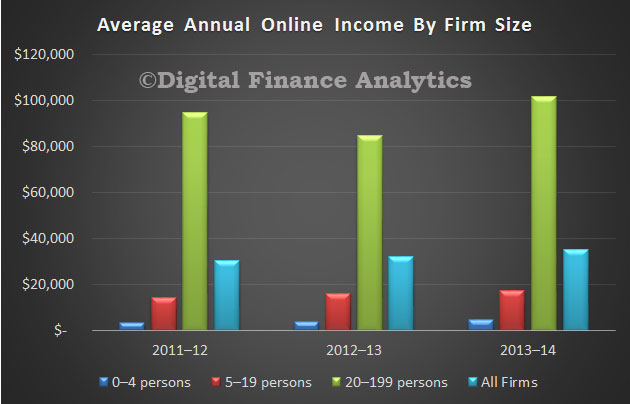

The survey shows a significant rise in a social media presence up 18%, but this compares with a massive 44% increase in the prior year. We also see a rise in orders placed via the internet (up 4%), and fulfilled via the internet (up 10%). Almost all firms have broadband access. Finally, average annual income for a small firm was more than $4,000, compared with a medium firm of $17,000. Larger firms generated more income, and the four largest employers generated on average $3.6 million.

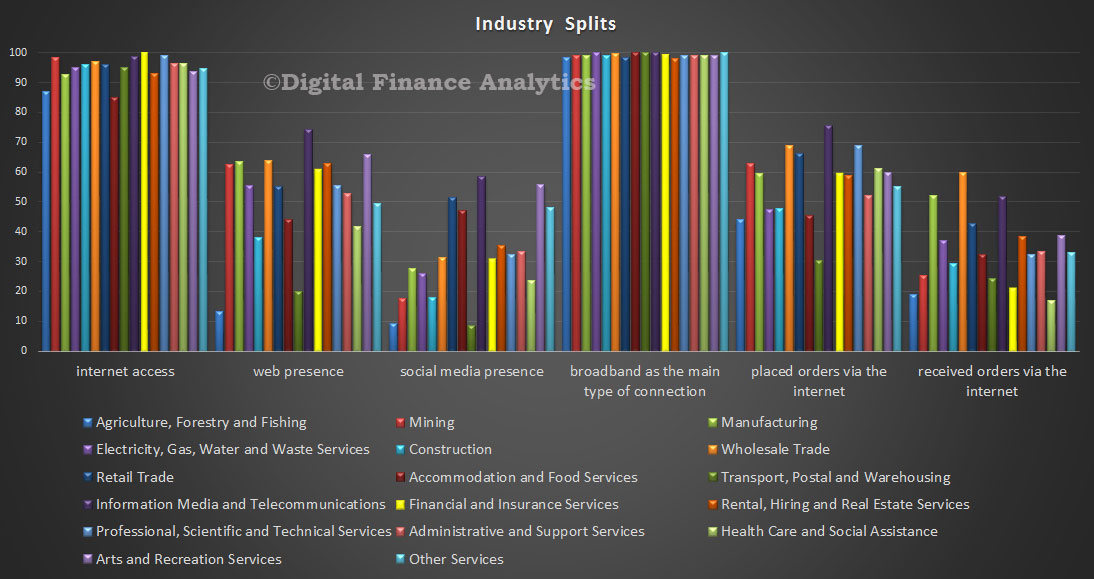

Finally, average annual income for a small firm was more than $4,000, compared with a medium firm of $17,000. Larger firms generated more income, and the four largest employers generated on average $3.6 million. Commerce through the internet is both mainstream, and likely to grow further, supported by the deeper penetration of smart phones and tablets, which enhance customer convenience, and innovation in terms of products and services. See our recent post. Many firms now see online as just another channel to market, but there are industry variations.

Commerce through the internet is both mainstream, and likely to grow further, supported by the deeper penetration of smart phones and tablets, which enhance customer convenience, and innovation in terms of products and services. See our recent post. Many firms now see online as just another channel to market, but there are industry variations. We see, for example that Information, Media and Telecommunications are some of the most active, whilst in finance and insurance, only 60% have a web presence, and 30% have a social media presence.

We see, for example that Information, Media and Telecommunications are some of the most active, whilst in finance and insurance, only 60% have a web presence, and 30% have a social media presence.