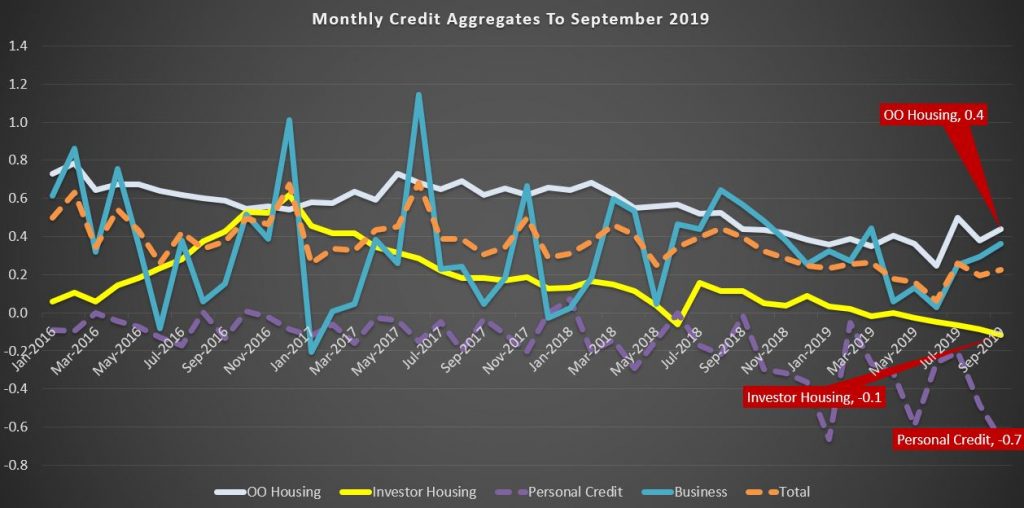

We are getting to the rub now with the RBA releasing its Credit Aggregate data to end September 2019. This is loan stock data, reflecting the net effect of new loans coming on, old loans repaid, refinancing, and any reclassification which occurred in the month.

Over the month of September, total credit grew by 0.2%, with housing also at 0.2%, business at 0.4% and personal credit down another 0.7%. Owner occupied lending was a little firmer, but investment lending faded again.

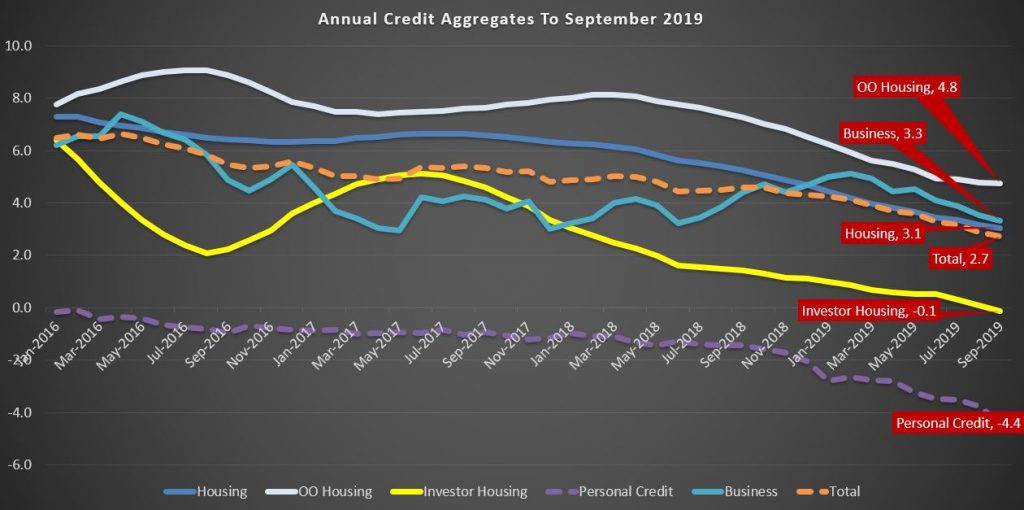

For the year ending, total credit grew by 2.7%, the lowest since June 2011, Housing at 3.1%, the lowest at least since 1977, and business at 3.3%. Personal credit fell 4.4% over the year.

Given the strong link between home prices and housing credit, this suggests home prices will continue weaker ahead. And this, after all the recent adjustments to lending standards and rates.

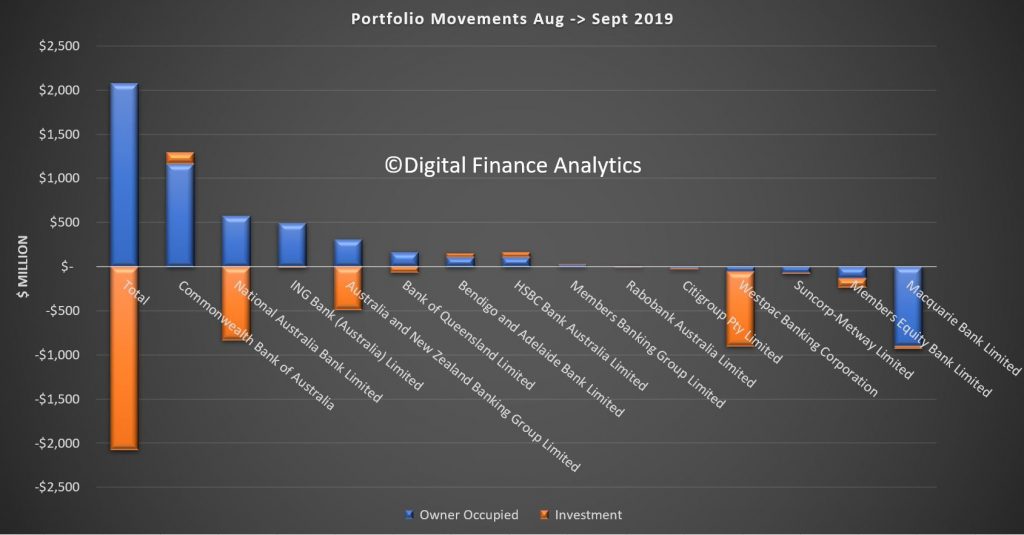

The APRA data also shows some swings between lenders during the month (or reclassification, we cannot tell). NAB, ANZ and Westpac all dropped their investment loan balances, while Macquarie dropped their owner occupied loans.

As expected, the Fed cut rates again following their latest meeting. Its worth noting a slight change of tone, which some suggest this may be the last for some time. Worth reflecting though, if we are not in an economic crisis, just why are rates so low, and what firepower remains if one emerges? Their worry centres on trade and business investment. The “Non-QE” QE continues in parallel. The Dow was higher.

Information received since the Federal Open Market Committee met in September indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a strong pace, business fixed investment and exports remain weak. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In light of the implications of global developments for the economic outlook as well as muted inflation pressures, the Committee decided to lower the target range for the federal funds rate to 1-1/2 to 1-3/4 percent. This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain. The Committee will continue to monitor the implications of incoming information for the economic outlook as it assesses the appropriate path of the target range for the federal funds rate.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; James Bullard; Richard H. Clarida; Charles L. Evans; and Randal K. Quarles. Voting against this action were: Esther L. George and Eric S. Rosengren, who preferred at this meeting to maintain the target range at 1-3/4 percent to 2 percent

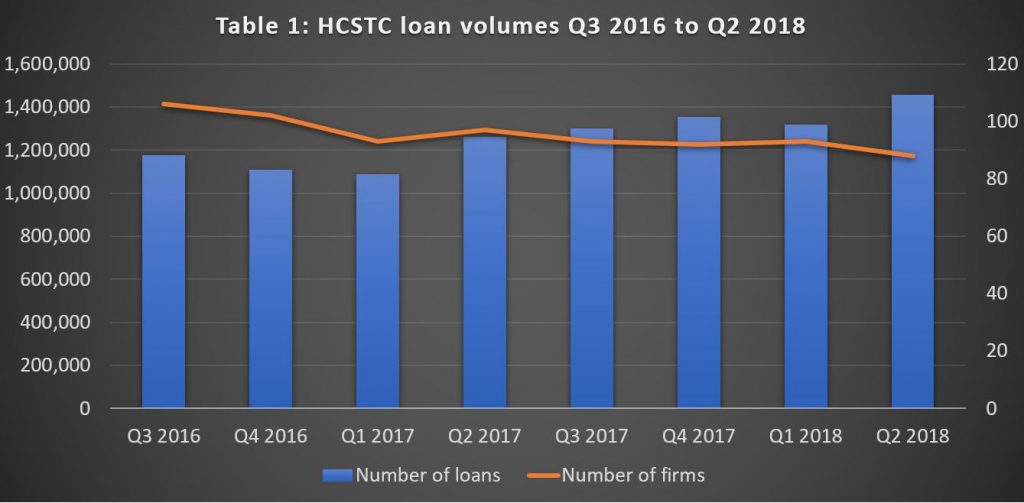

There have been some interesting developments in the short-term lending market in the UK recently. The Financial Conduct Authority in the UK recently published data on the so called high-cost short-term credit (HCSTC) market. HCSTC loans are unsecured loans with an annual percentage interest rate (APR) of 100% or more and where the credit is due to be repaid, or substantially repaid, within 12 months. In January 2015, The FCA introduced rules capping charges for HCSTC loans.

Just over 5.4 million loans originated in the year to 30

June 2018, and that lending volumes have been on an upward trend over the last

2 years. Despite some recovery, current lending volumes remain well down on the

previous peak for this market. Lending volumes in 2013, before FCA regulation,

were estimated at around 10 million per year.

These data reflect the aggregate number of loans made in a

period but not the number of borrowers, as a borrower may take out more than

one loan. They estimate that for the year to 30 June 2018 there were around 1.7

million borrowers (taking out 5.4 million loans).

The market is concentrated with 10 firms accounting for

around 85% of new loans. Many of the remaining firms carry out a small amount

of business – two thirds of the firms reported making fewer than 1,000 loans

each in Q2 2018.

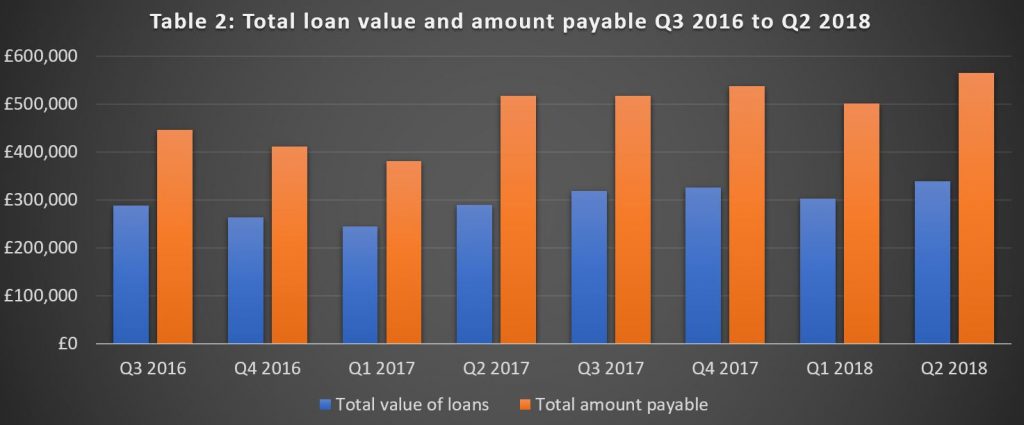

For the year to 30 June 2018, the total value of loans

originated was just under £1.3 billion and the total amount payable was £2.1

billion. Figure 2 shows that the Q2 2018 loan value and amount payable mirrored

the jump in the volume of loans with loan value up by 12% and amount payable

13% on Q1 2018.

The average loan value in the year to 30 June 2018 was £250.

The average amount payable was £413 which is 1.65 times the average amount

borrowed. This ratio has been fairly stable over the past 2 years. A price cap

introduced in 2015 stipulates that the amount repaid by the borrower (including

all charges) should not exceed twice the amount borrowed.

Over the past 2 years the average Annual Percentage Rate (APR) charged for HCSTC has been consistent, hovering around 1,250% (mean value). The median APR value is slightly higher at around 1,300%. Within this there will be variations of APR depending on the features of the loan. For example, the loans repayable by installments over a longer period may typically have lower APRs than single installment payday loans.

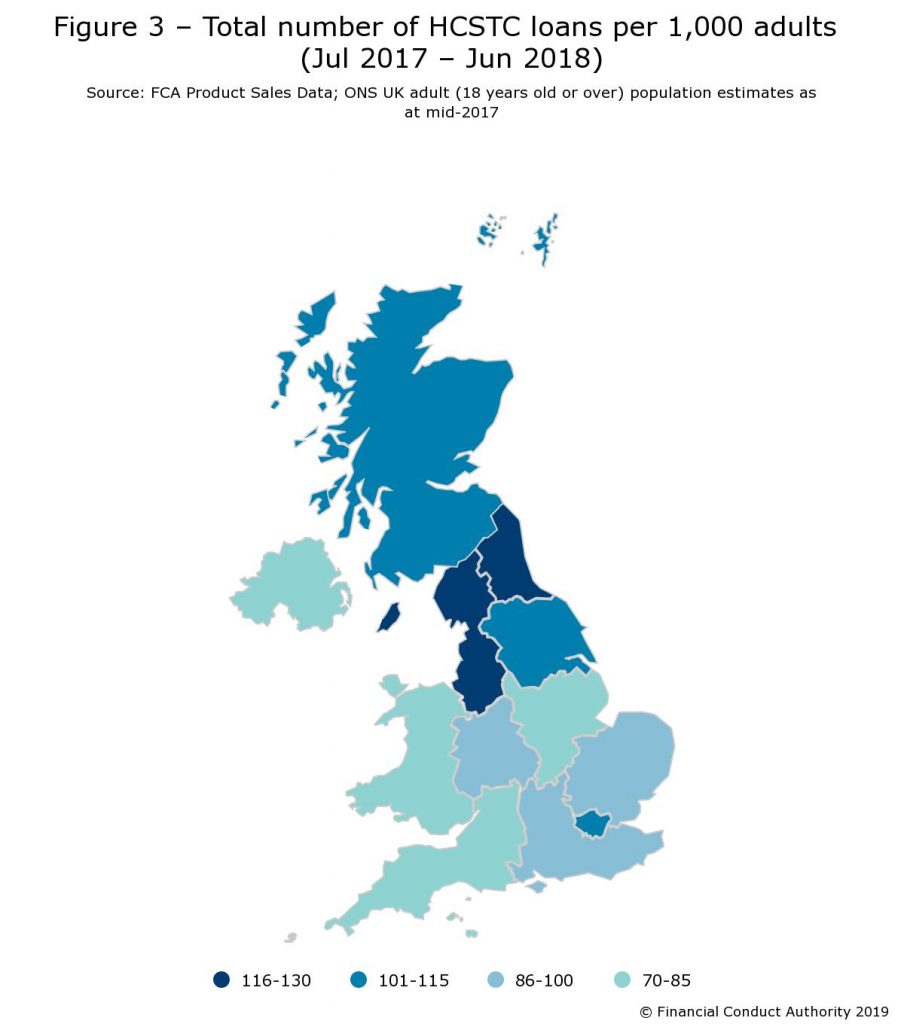

In the UK, the North West has the largest number of loans

originated per 1,000 adult population (125 loans), followed by the North East

(118 loans). In contrast, Northern Ireland has the lowest (74 loans).

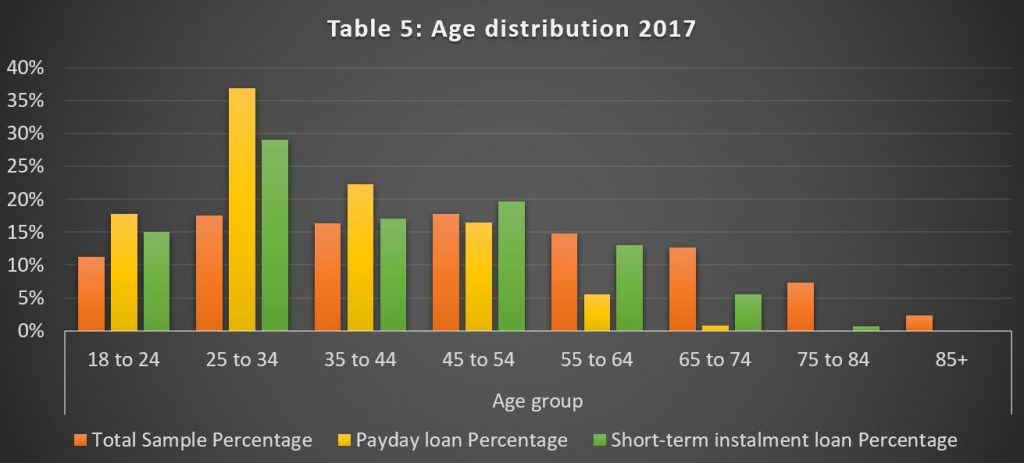

Borrowers between 25 to 34 years old holding HCSTC loans (33.4%) were particularly over-represented compared to the UK adults within that age range (17.5%). Similarly, borrowers over 55 years old were significantly less likely to have HCSTC loans (12.2%) compared to the UK population within that age group (34.8%). The survey also found that 60% of payday loan borrowers and 45% for short-term installment loans were female, compared with 51% of the UK population being female.

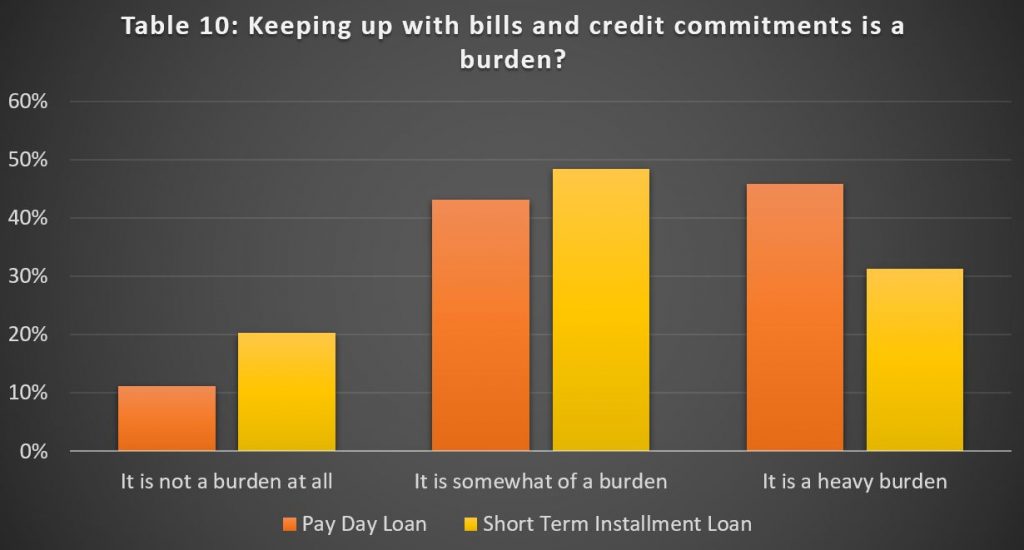

61% of consumers with a payday loan and 41% of borrowers with a short-term installment loan have low confidence in managing their money, compared with 24% of all UK adults. In addition, 56% of consumers with a payday loan and 48% of borrowers with a short-term installment loan rated themselves as having low levels of knowledge about financial matters. These compare with 46% of all UK adults reporting similar levels of knowledge about financial matters.

But now the top PayDay lenders are out of business. In August 2018, Wonga, once the biggest payday lender in the UK collapsed and now administrators for the lender have revealed that 389,621 eligible claims have been made since Wonga’s demise. Despite being vilified for its high-cost, short-term loans, seen as targeting the vulnerable, it became a household name and was enormously successful until stricter regulation curtailed its, and other payday loan companies’, lending.

It collapsed in the UK following a surge in compensation

claims from claims management companies acting on behalf of people who felt

they should never have been given these loans. So far, the compensation bill is

£460m, with the average claim £1,181.

Another lender, The Money shop closed earlier this year.

Now QuickQuid, UK’s largest payday lending firm is to close with thousands of complaints about its lending still unresolved. QuickQuid’s owner, US-based Enova, says it will leave the UK market “due to regulatory uncertainty”.

QuickQuid is one of the brand names of CashEuroNet UK, which

also runs On Stride – a provider of longer-term, larger loans and previously

known as Pounds to Pocket. The UK’s Financial Ombudsman Service said that it

had received 3,165 cases against CashEuroNet in the first half of the year. It

was the second most-complained about company in the banking and credit sector

during that six months.

Back in 2015, CashEuroNet UK LLC, trading as QuickQuid and

Pounds to Pocket, agreed to redress almost 4,000 customers to the tune of £1.7m

after the regulator raised concerns about the firm’s lending criteria.

More than 2,500 customers had their existing loan balance

written off and more almost 460 also received a cash refund. (The regulator had

said at the time that the firm had also made changes to its lending criteria.)

“Over the past several months, we worked with our UK

regulator to agree upon a sustainable solution to the elevated complaints to

the UK Financial Ombudsman, which would enable us to continue providing access

to credit,” said Enova boss David Fisher.

“While we are disappointed that we could not ultimately

find a path forward, the decision to exit the UK market is the right one for

Enova and our shareholders.”

So this could be the twilight of the PayDay industry in the

UK, as better education, and other lending options, plus tighter regulation

bite.

Given the pressures on households here, we are concerned that

more will reach for short term loans to tide them over, despite the high costs

and risks from repeat borrowing, all made easier still via the proliferation of

online portals. The debt burden on households is high and rising.

APRA is proposing to adjust its capital requirements for authorised deposit-taking institutions (ADIs) to support the Government’s First Home Loan Deposit Scheme (FHLDS). The scheme aims to improve home ownership by first home buyers, through a Government guarantee of eligible mortgage loans for up to 15 per cent of the property purchase price.

Recognising that the Government guarantee is a valuable form of credit risk mitigation, APRA is proposing to reflect this in the capital framework by applying a lower capital requirement to eligible FHLDS loans.

APRA intends to give effect to this lower capital requirement by adjusting the mortgage capital requirements set out in Prudential Standard APS 112 Capital Adequacy: Standardised Approach to Credit Risk (APS 112).

Specifically, recognising both the minimum 5 per cent deposit required of borrowers and the Government guarantee of 15 per cent of the property purchase price, APRA proposes to allow ADIs to treat eligible FHLDS loans in a comparable manner to mortgages with a loan-to-valuation ratio of 80 per cent.

This would allow eligible FHLDS loans to be risk-weighted at 35 per cent under APRA’s current capital requirements. Once the Government guarantee ceases to apply to eligible loans, (this could be because the borrower pays down the loan to below 80 per cent of the property purchase price, refinances or uses the property for a purpose that is not within the scope of the guarantee.) ADIs would revert to applying the relevant risk weights as set out in APS 112.

APRA invites feedback on this proposal, which will be subject to a

two-week public consultation. APRA intends to release its response,

including additional information on implementation for participating

ADIs, as soon as practicable after the consultation period.

Written submissions on the proposal should be sent to ADIpolicy@apra.gov.au by 11 November 2019

The latest edition of our weekly finance and property news digest with a distinctively Australian flavour.

Contents:

0:24 Introduction

0:58 US Markets

3:10 The Feds “Non-QE” QE

5:40 Brexit and UK Markets

6:50 Metro Bank

8:06 ECB

10:20 Australian Segment

10:30 Economic Data

12:30 Cash Transaction Ban

14:20 Property Sales and Prices

16:45 Foreign Buyers

18:45 WA First Time Buyer Incentives

19:40 Bank Profitability

20:30 Interest Only Lending

21:25 Local QE Is Coming

25:30 Local Market Summary

Westpac has said its cash earnings for the second half of 2019 will be reduced by $341 million due to customer remediation programs.

The additional provisions put Westpac’s total remediation costs for 2019 at $1.13 billion.

Of

the $341 million impact on cash earnings in the half, approximately 72

per cent relates to customer payments (including interest) while the

rest relates to costs associated with running these remediation

programs.

The larger items over the half related

to provisions associated with financial advice. The majority of new

provisions are related to ongoing advice service fees and changes in how

the time value of money is calculated including extending the forecast

timing over which payments are likely to be made.

Westpac

said the current estimated provision associated with authorised

representatives now represents 32 per cent of the ongoing advice service

fees collected over the period. For salaried planners the estimated

percentage is 26 per cent.

“A key priority in

2019 has been to deal with outstanding remediation issues and refund

customers as quickly as possible,” Westpac CEO Brian Hartzer said.

“The additional provisions announced today are part of that commitment. As part of our ‘get it right put it right’ initiative we are determined to fix these issues and stop these errors occurring. We will continue to review our products and services to ensure they deliver the right outcomes for customers, and if necessary, make further provisions.”

Westpac’s shares were down today, but then most of the major banks were also lower.

Westpac yesterday announced a number of changes to its credit policy, which have also gone into effect across its subsidiaries: BankSA, Bank of Melbourne, and St George Bank. Via Australian Broker.

Investor lending

Effective 22 October, the maximum loan to value ratio for

interest-only investor loans was raised from 80% to 90% – including any

capitalised mortgage insurance premium.

The update applies to new purchases, refinances within Westpac Group

or externally, and loan variations such as switching from P&I

repayments to interest-only.

However, the current switching policy will continue to apply, with

customers only able to switch to interest-only repayments post 12 months

of loan drawdown.

The changes will not apply to interest-only owner occupier loans, which will maintain their maximum LVR at 80%.

HEM calculations

Also effective yesterday, referral to credit will no longer be

required in instances where expenses are greater than 130% of HEM and no

other reason that requires credit assessment is triggered, a change the

group expects to save brokers time and deliver faster outcomes to

customers.

Updated resources

The group also launched an enhanced version of its Assess calculator,

“developed in response to broker feedback.” It crafted the updated tool

to be more intuitive and streamlined, making the completion of

assessments “much quicker” and saving brokers valuable time.

Westpac plans to remain receptive to feedback moving forward,

inviting brokers to “give it a go” and share their thoughts on their

experience.

The older version of the Assess calculator will not be available for use after 15 November 2019.

Over a third of the world’s banks lag on technology and scale, and are unprepared for an economic downturn, according to global consultancy firm McKinsey and Co, via InvestorDaily.

The

firm used its annual banking review to warn banks that they risked

“becoming footnotes to history” if they did not scale up and embrace

technological change.

“About 35 percent of banks globally are both subscale and suffer from operating in unfavorable markets,” the report reads.

“Their business models are flawed, and the sense of urgency is acute.”

According

to the report, banks need to merge with or acquire more companies and

forge new partnerships in order to build scale and weather the financial

storm.

They also need to be prepared for an “arms race on technology”.

“Both

banks and fintechs today spend approximately 7 percent of their

revenues on IT; but while fintechs devote more than 70 percent of their

budget to launching and scaling up innovative solutions, banks end up

spending just 35 percent of their budget on innovation with the rest

spent on legacy architecture,” the report reads.

The report noted

the efforts of Amazon in the US, which offers businesses traditional

banking services while connecting them to the Amazon “ecosystem” of

non-financial products and services, and pointed to blockchain and

artificially intelligent systems as some of the advances banks need to

embrace in order to survive.

Banks could also outsource some

“non-differentiating” activities – activities that do not differentiate

the bank from its competitors, such as “know your customer” and

anti-money laundering compliance, which can represent as much as 7 per

cent and 12 per cent of costs.

However, some factors – like geography – were outside of bank control.

The

report noted that North American banks hit a ROTE of 16 per cent in

2018, while European banks barely managed half of this, with

implications for their performance in the event of downturn.

The report also warned of the potential impact of a downturn on public perception of banks.

“Because

of the special role they play in society, they, perhaps more than other

industries, benefit from society in areas such as deposit protection

and regulation as a means of constraining supply,” the postscript to the

report reads.

“In return, they are particularly accountable in

an era of rising inequality and falling faith in historically trusted

institutions; beyond shareholders to society and the sustainability of

the environment in which they and their clients operate.”