The latest edition of our weekly finance and property news digest with a distinctively Australian flavour.

Contents:

0:23 Introduction

1:18 US

2:21 US Retail

3:15 US Markets

4:10 China’s Growth

5:10 Brexit and UK Markets

07:05 Germany

09:00 Australia

09:05 Latitude Failed Float

10:10 Bank of Queensland Result

10:42 Regionals Under Pressure

11:10 Unemployment

11:32 RBA Comments

12:40 Property Auctions and Prices

14:05 Mascot Tower defects

14:35 Local Market

Here is a show about my submission to the Senate Inquiry into Audit in Australia, where I focus in on the key issues, show some of the gaps in the current system and suggest reform. Submission close on 28th October if you want to have your say!

Submissions close on 28 October 2019. DFA has made a submission.

Introduction.

We welcome the current inquiry and note the similar

initiatives underway in several other jurisdictions. This is an important

issue.

We believe there is a need to refocus the auditing practices

which are currently deployed by the “big four” firms in particular and the

industry more widely. We reach these conclusions, having analysed the financial

sector for more than 30 years, as a consultant, financial firm employee and a

partner within Arthur Andersen before its dissolution.

There are many threads to the argument, but, these large

audit firms are in our opinion too close to management of large companies, as

they both advise them on strategy and tax minimisation, and separately provide

audit services. In addition, these big four firms are responsible for the

evolution of accounting standards, including off-balance sheet minimisation, as

well as providing advisory services to companies and Government, and they also offer

auditing capabilities. Conflicts abound.

Whilst in theory audit practices should be separated from

other commercial and advisory operations of the big four, I have seen examples

when company account planning sessions have included cross discipline

discussions, from advisory, consulting, services AND audit, to craft strategies

to maximise the commercial benefits to the audit and consulting firm. This

happened regularly at AA.

In addition, the audit of large companies are executed in a

formulaic and superficial way, where the main test is the need to meet relevant

accounting standards, not separately confirming independently that the business

is functioning as advertised from a financial and compliance perspective. Who audits the auditors?

Remember that in 2008 several banks failed, despite having

been given an unqualified audit in the months prior. Others required

substantial Government bail-out or were absorbed by other industry players.

Nothing has changed (other than the quantum of debt and other exposures have

increased substantially) since then.

A Financial Services Example.

To illustrate the limitations of audit, I will highlight

four areas, where from my research and experience current banking sector audits

are deficient.

Financial Derivatives Exposure.

According to recent RBA data Australian banks have some $48

trillion of gross derivatives exposures. This will include services to client,

but also position taking on a trading basis within the bank’s treasury

operations. Recent BIS research highlighted that in a low interest rate

environment, banks will tend to lend less and trade more to try to bolster

profits[i]. Plus, some window-dress their books for

quarter end.[ii]

Derivatives gross exposures dwarf the capital and assets

held within banks. This gross exposure is not reported clearly within the

accounts, because most is held off balance sheet. Moreover, the true

net-exposure which a bank may face will be determined by market movements and

relative trading positions. But even net exposures are not adequately reported.

We only get a glimpse of the true positions (and risks) when capital is applied

under the Basel rules, but this does not tell the full story, yet are within

current accounting standards, and off-balance sheet rules. We see no evidence

of auditors picking through the derivatives book and validating or reporting

these gross exposures. In a crisis this may well hit the financial position of

an individual bank, and trigger the need for a restructure, bail-in or

bail-out. Current audit rules and

approaches are designed to minimise disclosure and obscure the true risks. APRA does not provide an alternative route to

disclose such risks.

Internal Risk Models

Major banks can use their own “internal risk models” to

estimate the amount of capital applied to the business, under the Basel rules.

These models are complex and “tuned” by the institutions to enables

institutions’ to maximise their use of capital. However, we are not convinced

these models are functioning as intended, and they are not subject to regular

audit, either by external auditors, or APRA. Thus, the data is taken as

accurate from the “black-box” and this may lead to higher risks in the business

than are disclosed. Again, the true

position will not be exposed until a crisis hits.

Property Portfolio Revaluations

Large financial companies hold significant portfolios of

mortgages backed by residential property. An initial valuation is used in the

underwriting process. However, unless there is a material refinancing event,

subsequent portfolio adjustments, (because for example property prices move

down) are applied only at an aggregate level (for example state level). As a result,

there is a significant risk the property portfolio is overstating the real

current value of the underlying security, and this may translate to bigger

risks in a downturn. In addition, the amount of capital held under Basel rules could

well be understated. There may be offsetting benefits in a rising market, but

the standard portfolio analysis is not very accurate. But once again external

auditors will be not examining the operation practices of portfolio valuations

yet will sign off on the accounts as true and accurate.

Household versus Loan Risks

Households often hold multiple loans across a lender or

lenders. APRA only considers the status of individual loans. Reporting for

audit purposes will be at a loan, not household level. Indeed, there are cases when loans are

deliberately split to reduce the overall loan to value results. Once again this

is an area where auditors will not tread, but the risks in the system are

higher than those reported in the accounts. Again, the true position will not

be exposed until a crisis hits.

These are just examples of pain points which the current

audit processes will not adequately examine. There are many others.

Final Observations

The role of an auditor should be more than just checking

with the accounting standards and signing off. They should be seeking out

material issues, independently from management. But in the four cases above the

results are wanting.

The solution would be to create an independent audit

function, perhaps within the Auditor General’s domain, to provide accurate and

independent analysis of large financial players. In addition, we believe that

the audit functions of major firms should operate as separate service businesses

and should NOT be also be allowed to offer creative accounting and off-balance

sheet techniques as part of their service suite. The conflicts and limitations

are obvious and concerning.

However, the true impact of such deficiencies would only be

revealed in a crisis, mirroring 2008, by which time it is too late. Changing

management and audit practices as suggested would place our important financial

sector companies on a firming footing. Such changes could well benefit other

industry sectors as well.

Changes to audit practice and structure are essential!

[iii]

Digital Finance Analytics is a boutique research and advisory firm. More

details are available via our Blog. https://digitalfinanceanalytics.com/blog/

We discuss recent development in the proposed cash transaction ban, with the help of a recent Saturday paper article and CBA’s systems failures today. Cash is king!

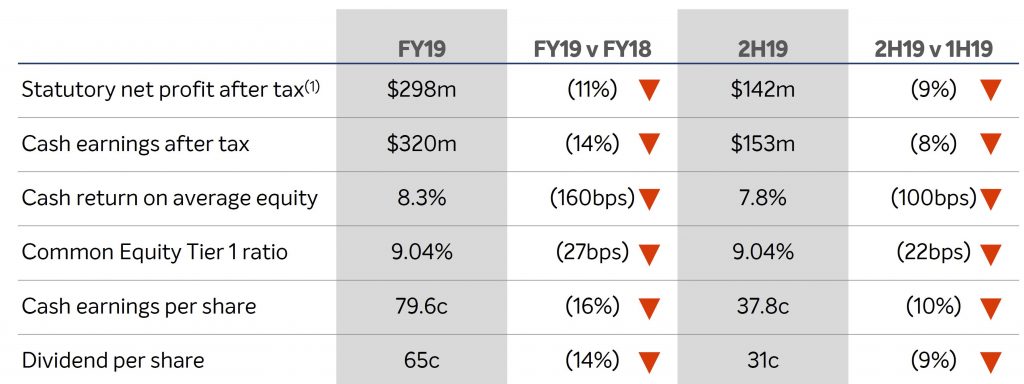

Bank of Queensland today announced FY19 cash earnings after tax of $320 million, down 14 per cent on FY18. Statutory net profit after tax decreased by 11 per cent to $298 million. Basic cash earnings per share was down 16 per cent to 79.6 cents per share. We expect many banks to report a similar story ahead.

The Board has announced a final dividend of 31 cents per share, for a full year dividend of 65 cents per share. This is a reduction of 11 cents per share from FY18. The final dividend payout ratio of 82% was consistent with the interim dividend payout ratio.

They described this as “Disappointing results reflect challenging operating environment”, reflecting a challenging operating environment characterised by slowing credit demand, lower interest rates, a rise in regulatory costs and changes impacting non-interest income.

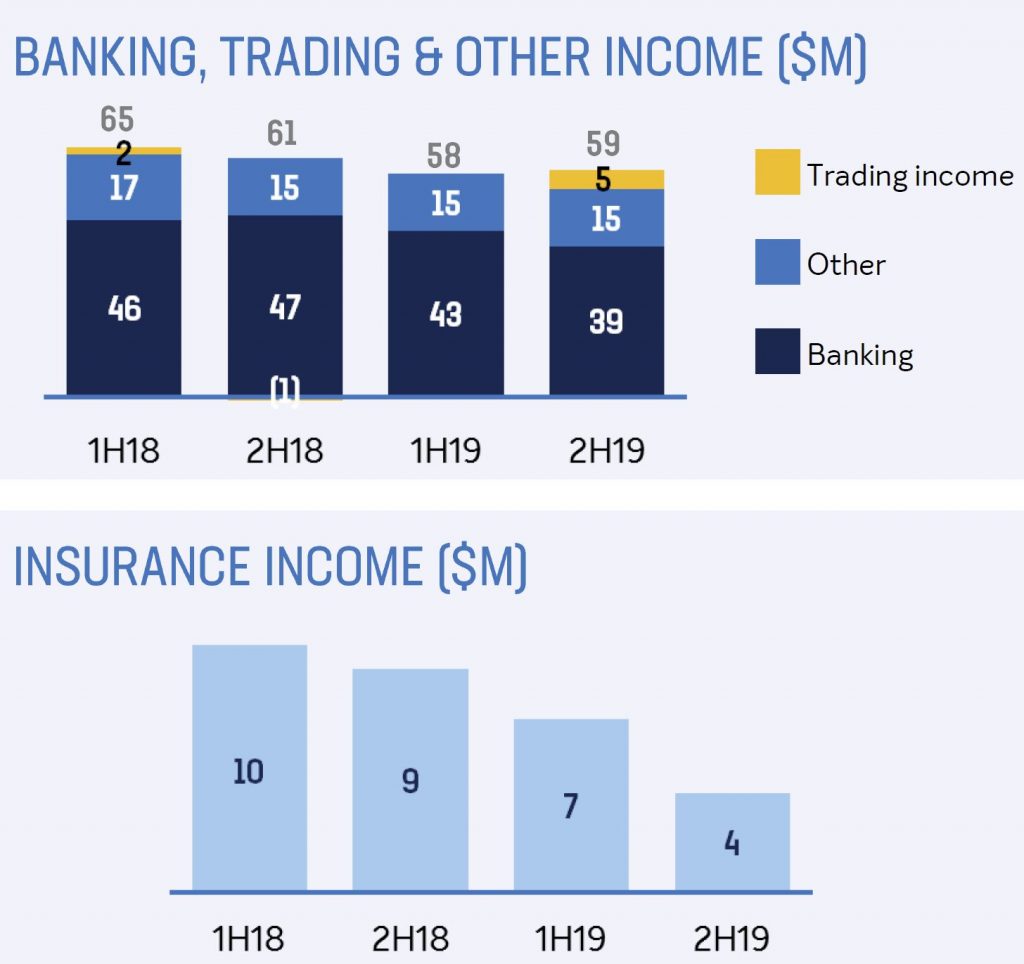

Total income decreased by $21 million or two per cent from FY18.

Net interest income decreased $4 million, driven primarily by a five basis point reduction in net interest margin to 1.93 per cent. This reduction is attributable to the declining interest rate environment and continued strong competition for loans and deposits.

Non-interest income decreased 12 per cent or $17 million, driven by declines in Banking, Insurance and Other income but partially offset by improved Trading income. Banking income reduced $11 million due to lower fee income and a change in arrangements related to BOQ’s merchant offering. Insurance income reduced $8 million or 42 per cent due to changes in the insurance sector which ultimately impacted distribution of St Andrew’s consumer credit insurance through its corporate partners.

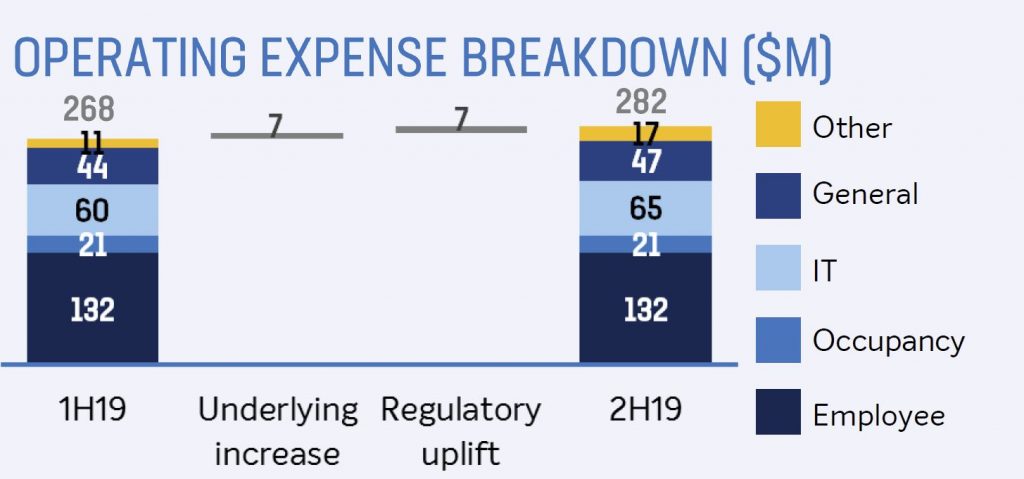

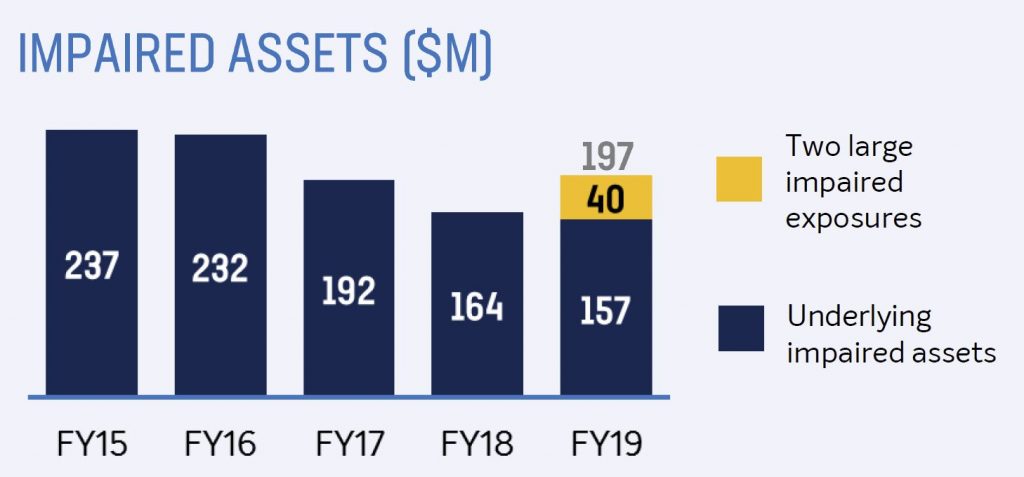

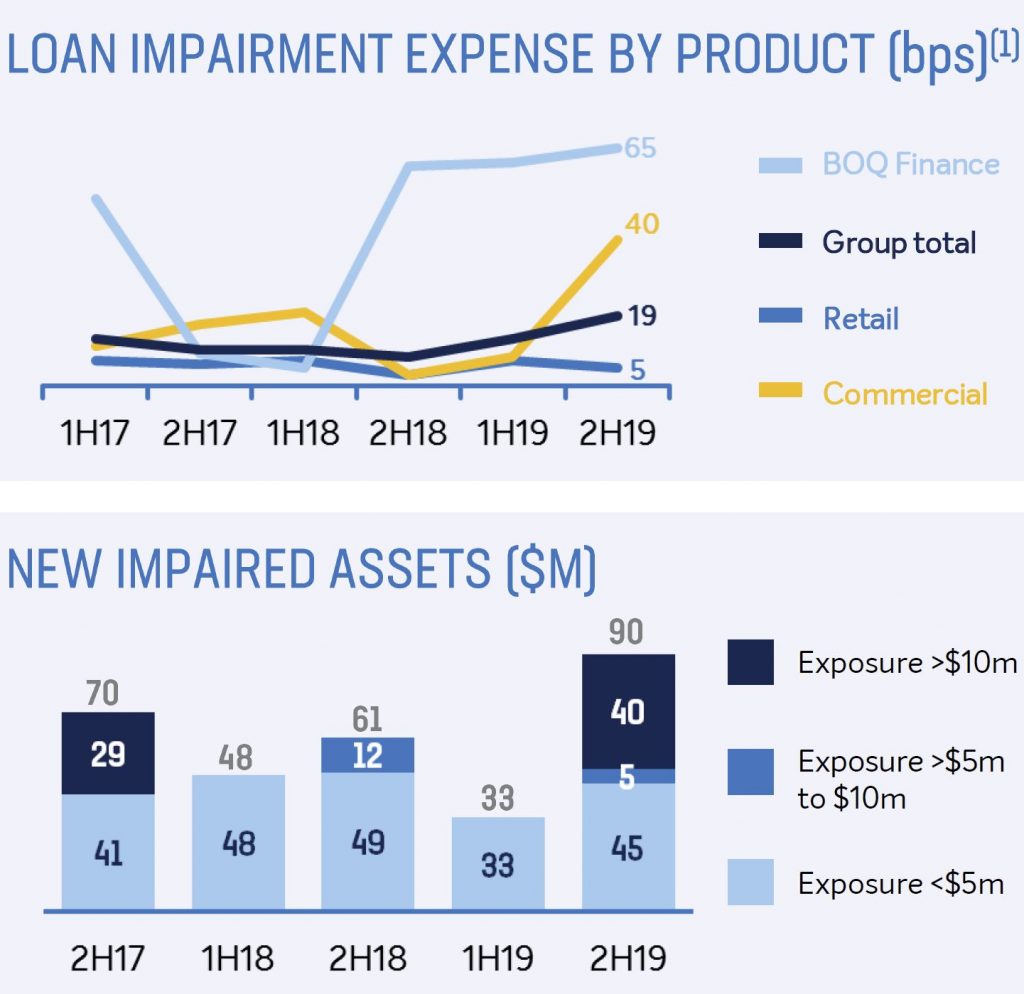

In line with the guidance provided at the 1H19 result, operating expenses increased by $23 million or four per cent from FY18. The increase in expenses was more pronounced in the second half, due to an increase in business deliverables addressing regulatory and compliance requirements. While loan impairment expense increased $33 million to $74 million, equivalent to 16 basis points of gross loans, underlying asset quality remains sound with impairments and arrears remaining at low levels.

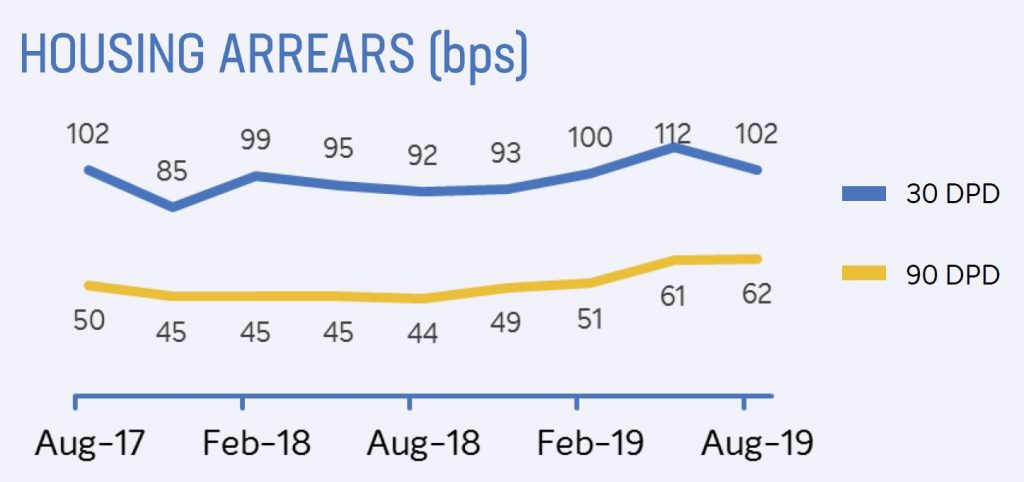

Housing loan arrears over 90 days rose, while 30 day fell.

Implementation of BOQ’s new AASB 9 collective provision model drove an increase in collective provisions due to changes in BOQ’s portfolio and a weaker economic outlook. The increase in collective provisions contributed $22 million of the loan impairment expense uplift.

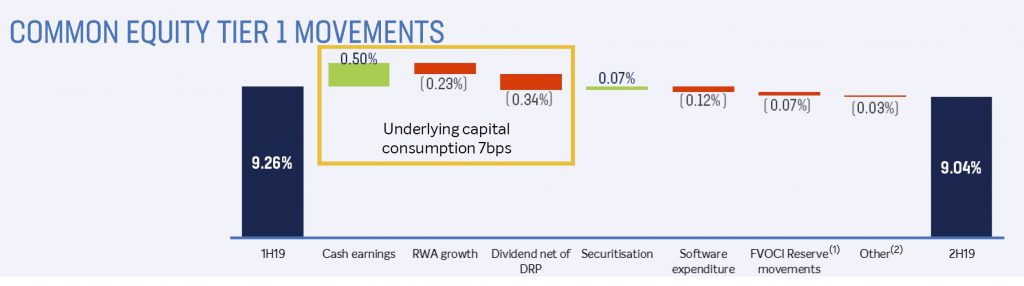

BOQ remains appropriately capitalised with a Common Equity Tier 1 ratio of 9.04 per cent, which is a decrease of 27 basis points from FY18. The reduction was driven by a combination of asset growth being tilted to more capital intensive business lines, increased capitalised investment, reduced earnings and lower participation in the dividend reinvestment plan.

Overall lending growth of two per cent was achieved over the year.

Continued growth momentum was evident in BOQ’s niche business segments. The BOQ Finance portfolio achieved growth of $667 million or 15%, while BOQ Specialist grew lending balances by $756 million across its commercial and housing loan portfolios which are focused on the medical segment. Virgin Money also delivered a consistently strong level of housing loan growth, with the portfolio growing by $914 million to over $2.5 billion.

A key imperative remains rebuilding the foundation for growth in BOQ’s retail bank, which saw a further contraction of $1.4 billion in its residential housing loan book.

Solid progress has also been made across a number of key foundational investments during the year. BOQ’s core technology infrastructure modernisation program has continued to track to plan, with implementation continuing through FY20. This will deliver a more modern, cloud-based technology environment which will allow for improved change capability.

During the year, work began on development of a new mobile banking application for BOQ customers, with a launch expected in 2020. Lending process improvements have also been a key focus to improve customer experience, particularly for home loan applications. A number of regulatory projects have also progressed during the year to address various regulatory and industry changes. These are all critical investments that will support BOQ’s transformation and future aspirations.

Investment in the implementation of a new Virgin Money digital bank has also progressed during the year, with a customer launch planned for 2020. This will require $30 million of capitalised investment during FY20 to complete the phase one build which will deliver a transaction and savings account offering to customers. This is an investment in long term value creation for this iconic brand which has demonstrated success in attracting customers across its existing product suite. It is also anticipated that this investment in a new digital banking platform will be leveraged across the Group in the years ahead.

Commenting on the results and outlook for BOQ, new Managing Director & CEO George Frazis said that there are challenges ahead, however fundamentally, BOQ is a good business.

“Our capital is well positioned for ‘unquestionably strong’, we have a good funding position and our underlying asset quality is sound. “There are numerous opportunities ahead for a revamped BOQ and I will be working closely with the executive leadership team to complete our strategic and productivity review, with a market update on our plans in February 2020,”

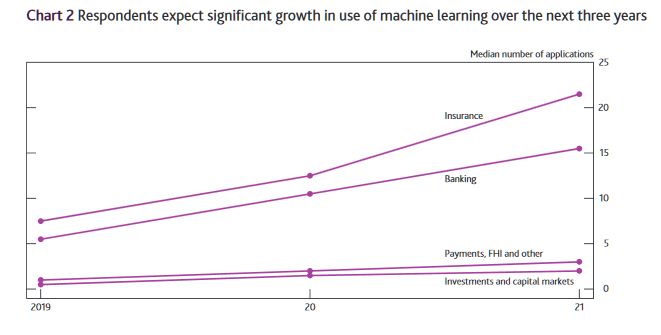

The Bank of England (BoE) and Financial Conduct Authority (FCA) have a keen interest in the way that ML is being deployed by financial institutions.

They conducted a joint survey in 2019 to better understand the current use of ML in UK financial services. The survey was sent to almost 300 firms, including banks, credit brokers, e-money institutions, financial market infrastructure firms, investment managers, insurers, non-bank lenders and principal trading firms, with a total of 106 responses received.

In the financial services industry, the application of machine

learning (ML) methods has the potential to improve outcomes for both

businesses and consumers. In recent years, improved software and

hardware as well as increasing volumes of data have accelerated the pace

of ML development. The UK financial sector is beginning to take

advantage of this. The promise of ML is to make financial services and

markets more efficient, accessible and tailored to consumer needs. At

the same time, existing risks may be amplified if governance and

controls do not keep pace with technological developments. More broadly,

ML also raises profound questions around the use of data, complexity of

techniques and the automation of processes, systems and

decision-making.

The survey asked about the nature of deployment of ML, the business

areas where it is used and the maturity of applications. It also

collected information on the technical characteristics of specific ML

use cases. Those included how the models were tested and validated, the

safeguards built into the software, the types of data and methods used,

as well as considerations around benefits, risks, complexity and

governance.

Although the survey findings cannot be considered to be statistically

representative of the entire UK financial system, they do provide

interesting insights.

The key findings of the survey are:

ML is increasingly being used in UK financial services. Two thirds of respondents report they already use it in some form. The median firm uses live ML applications in two business areas and this is expected to more than double within the next three years.

In many cases, ML development has passed the initial development phase, and is entering more advanced stages of deployment. One third of ML applications are used for a considerable share of activities in a specific business area. Deployment is most advanced in the banking and insurance sectors.

From front-office to back-office, ML is now used across a range of business areas. ML is most commonly used in anti-money laundering (AML) and fraud detection as well as in customer-facing applications (eg customer services and marketing). Some firms also use ML in areas such as credit risk management, trade pricing and execution, as well as general insurance pricing and underwriting.

Regulation is not seen as a barrier but some firms stress the need for additional guidance on how to interpret current regulation. Firms do not think regulation is a barrier to ML deployment. The biggest reported constraints are internal to firms, such as legacy IT systems and data limitations. However, firms stressed that additional guidance around how to interpret current regulation could serve as an enabler for ML deployment.

Firms thought that ML does not necessarily create new risks, but could be an amplifier of existing ones. Such risks, for instance ML applications not working as intended, may occur if model validation and governance frameworks do not keep pace with technological developments.

Firms use a variety of safeguards to manage the risks associated with ML. The most common safeguards are alert systems and so-called ‘human-in-the-loop’ mechanisms. These can be useful for flagging if the model does not work as intended (eg. in the case of model drift, which can occur as ML applications are continuously updated and make decisions that are outside their original parameters).

Firms validate ML applications before and after deployment. The most common validation methods are outcome-focused monitoring and testing against benchmarks. However, many firms note that ML validation frameworks still need to evolve in line with the nature, scale and complexity of ML applications.

Firms mostly design and develop ML applications in-house. However, they sometimes rely on third-party providers for the underlying platforms and infrastructure, such as cloud computing.

The majority of users apply their existing model risk management framework to ML applications. But many highlight that these frameworks might have to evolve in line with increasing maturity and sophistication of ML techniques. This was also highlighted in the BoE’s response to the Future of Finance report. In order to foster further conversation around ML innovation, the BoE and the FCA have announced plans to establish a public-private group to explore some of the questions and technical areas covered in this report.

The major capital cities are seeing

property prices shoot back up thanks to interest rate cuts and an easing

of lending buffers. With auction clearance rates back near all time

highs, is the property downturn now well or truly over or will a new

round of frenzied bidding result in more debt-fuelled instability.

In this episode, Adam Creighton, economics editor of The Australian pits noted bear Martin North, who believes property prices could fall as much as 40 per cent, against Nerida Conisbee, chief economist of realestate.com.au.

The RBA minutes for October are decidedly bearish, clearly the battery in their rose-tinted specs as run down, revealing the mounting risks in the economy. Probably more risks ahead, more cuts and the proverbial QE in some form…

International Economic Conditions

Members commenced their discussion of global economic conditions by noting that heightened policy

uncertainty was affecting international trade and business investment. This had continued to be

apparent

in a range of indicators, including new export orders and investment intentions. Conditions in

the

manufacturing sector had remained subdued, partly because of ongoing US–China trade

tensions.

These tensions had led to a contraction in bilateral trade between the United States and China,

which

was resulting in the diversion of some activity to other economies. Members noted that the trade

and

technology disputes continued to pose significant downside risks to the global economic outlook.

In general, conditions in the services sector had been relatively resilient in most advanced

economies,

supported by strong labour market conditions. Employment growth had continued to outpace growth

in

working-age populations, unemployment rates had remained at low levels and wages growth had

risen.

Nevertheless, inflation had remained low, although core inflation had picked up in the United

States in

recent months.

In the United States, GDP growth appeared to have slowed a little further in the September

quarter.

Growth in core capital goods orders and investment intentions had declined, whereas growth in

consumption had remained robust. In the euro area, the weakness in output growth in the June

quarter had

been broadly based. Industrial production had fallen, particularly in Germany, and investment

intentions

had remained below average. In Japan, exports had declined further, although output growth in

the

September quarter had been supported by above-average household spending ahead of an increase in

the

consumption tax in October.

In east Asia, export volumes had been flat for several months. Other indicators of activity, such

as

industrial production and surveys of manufacturing conditions, had shown tentative signs of

stabilising.

Growth in output had also slowed in India, driven by weakness in consumption. Members noted that

the

political unrest in Hong Kong had affected economic activity there to a significant extent.

In China, a range of indicators suggested that the pace of economic activity had slowed since the

start

of the year. Economic indicators remained subdued in August, although they had recovered a

little from

broad-based weakness in July. Growth in industrial production and retail sales had edged higher

in

August, and fixed asset investment growth had been broadly unchanged. Conditions in housing

markets also

appeared to have softened. In response to the slowing in activity, the authorities had announced

further

measures to ease policy in September. Chinese demand for imported iron ore and coal had

increased,

supported by ongoing investment in infrastructure.

The iron ore benchmark price had continued to be volatile since the previous meeting. Members

noted

that supply concerns in the iron ore market had eased somewhat, and ongoing strength in Chinese

steel

demand had been met by an increase in iron ore imports. Oil prices had also been volatile, with

the

attacks on oil infrastructure in Saudi Arabia having disrupted oil supply and exacerbated

uncertainty in

the region.

Domestic Economic Conditions

Members noted that the main domestic economic news over the previous month had been the release

of the

national accounts data for the June quarter and updates on the labour and housing markets. On

balance,

the data had pointed to a continuation of recent trends.

The national accounts reported that the Australian economy had grown by 0.5 per cent in the June quarter. Year-ended growth had slowed to 1.4 per cent, the lowest outcome in a decade. Nevertheless, there had been a pick-up in quarterly GDP growth over the first half of 2019 compared with the second half of 2018. The pick-up had been driven by stronger growth in exports, led by exports of resources and manufacturing goods. Members noted that export demand was being supported by the lower level of the Australian dollar. Public demand had also been growing strongly, partly because of spending on the National Disability Insurance Scheme. Members observed that the drought had continued to affect the rural sector to a significant extent and that, as a result, farm output was expected to remain weak over the following year.

Growth in household disposable income had been subdued. Strong growth in income tax paid by households had been a contributing factor, as had been low growth in non-labour income, partly reflecting the effects of the drought on the farm sector. By contrast, strong employment growth had boosted growth in labour income.

Consistent with the ongoing low growth in household disposable income, household consumption had increased by only 1.4 per cent over the year to the end of June. Members noted that there had not yet been evidence of a pick-up in household spending following the recent reductions in the cash rate and receipt of the tax offset payments, although they acknowledged that it may be too early to expect any signs of a pick-up. Retail sales had remained subdued in July and car sales had decreased in August. Despite weak reported retail sales conditions generally, on a slightly more positive note some contacts in the Bank’s liaison program had reported a mild pick-up in retail sales since July. Responses to consumer surveys in September had suggested that, on average, households planned to spend around half of their lump-sum tax payments, broadly in line with what had been assumed in the Bank’s most recent forecasts.

The residential construction sector had contracted further and this was expected to continue for some time. The decline in dwelling investment in the June quarter was greater than had been expected a few months earlier. Higher-density approvals had declined in July, to be at their lowest level in seven years; detached approvals had also declined in July. The Bank’s liaison program had continued to report weak pre-sales for higher-density developments. Taken together, this information implied that dwelling investment would decline further over coming quarters.

The turnaround in the established housing market had continued in September. Housing prices had increased further in Sydney and Melbourne, and auction clearance rates had remained high in both cities. The pace of growth in housing prices had also picked up in some other capital cities in recent months. However, housing turnover had remained low.

Business investment had decreased a little in the June quarter, driven by a decline in non-residential construction outside the mining sector. Nevertheless, the outlook for non-mining business investment remained favourable, supported by investment in infrastructure. Mining investment had picked up largely as expected. Members noted that mining investment was expected to continue to increase gradually, supported by projects both to sustain and to expand production. Survey measures of business conditions had remained around average in August; members noted that conditions in retailing were reported to have been very weak, while conditions in the mining industry had remained well above average.

Conditions in the labour market had continued to be mixed. Employment growth in August had remained stronger than growth in the working-age population, and the employment-to-population ratio had reached its highest level since late 2008. Employment had increased by 2½ per cent over the preceding year, the third successive year of strong employment growth. The participation rate had also increased to another record high. Members noted that the strong demand for labour had been met by an equally strong increase in supply. The unemployment rate had been around 5¼ per cent since April and the underemployment rate had remained above its recent low point. Looking ahead, job vacancies and advertisements had declined, suggesting that employment growth would probably moderate over the subsequent few quarters. Members noted that the ongoing subdued growth in wages implied that there continued to be spare capacity in the labour market.

Financial Markets

Members noted that financial conditions remained accommodative internationally and in Australia.

Several major central banks had eased policy in September and market pricing implied that market

participants expected the global economic expansion to be sustained by an extended period of

policy

stimulus. Expectations of further monetary easing had been partially scaled back in response to

tentative signs of progress in the trade and technology negotiations between the United States

and China

and some better-than-expected US economic data. These developments had also supported the prices

of

equities and corporate bonds.

As expected, the US Federal Reserve had reduced its policy rate again by 25 basis points in

September. The Federal Reserve had noted that, although the US economy had remained strong,

easier

policy was warranted given muted domestic inflation pressures, a weakening in global activity

and

persistent downside risks. Members of the Federal Open Market Committee did not anticipate a

prolonged

easing cycle, but continued to signal that they were willing to ease policy further if needed to

sustain

growth and meet the Federal Reserve’s inflation objective. Market pricing suggested that

the

federal funds rate was expected to decline by a further 50 basis points or so by mid 2020,

which was a little less than had previously been anticipated.

The European Central Bank (ECB) had delivered a package of stimulus measures in response to

inflation

being persistently below the ECB’s target, protracted weakness in economic growth and

continued

downside risks. The package included cutting the ECB’s policy rate by 10 basis points

to

–0.5 per cent, exempting a portion of banks’ excess reserves from negative

deposit

rates, committing to not lifting rates until inflation returned sustainably to target, renewing

purchases of government and private sector securities, and easing the conditions of the targeted

long-term refinancing operations designed to encourage banks to lend to the private sector.

The People’s Bank of China had provided additional but targeted monetary stimulus, further

cutting

its reserve requirements, with larger adjustments for some smaller banks that are important

providers of

finance to small businesses. Chinese banks had also lowered the benchmark lending rate for

corporate

borrowers slightly.

Government bond yields in major markets had risen a little, with yields in Australia following suit. Nonetheless, bond yields remained very low, with a large portion of bonds in Europe and Japan trading at negative yields. Members noted that a sizeable proportion of the investors holding these negative-yielding bonds were constrained by their mandates or regulatory requirements, including asset managers, banks, insurance companies and pension funds.

Members noted that financing conditions for corporations remained favourable globally. Equity

prices

had remained close to recent peaks, spreads on corporate bonds were low and issuance volumes had

been

strong. In Australia, the cost of capital for corporations had been quite stable for some years,

although more recently it had declined a little. Members also discussed hurdle rates for

business

investment, which had not changed much over recent times.

Major exchange rates had generally been little changed over September, with the US dollar

having

appreciated over the preceding two years or so on a trade-weighted basis. The Chinese renminbi

had

stabilised after its earlier depreciation, while the Japanese yen had depreciated, consistent

with some

easing of concerns about global risks. The Australian dollar had been little changed and

remained around

its lowest level in recent years.

In Australia, borrowing rates for households and businesses, as well as banks’ funding costs, were at historically low levels. Housing loan approvals to both owner-occupiers and investors had increased in the three months to August, consistent with stronger conditions in some established housing markets. However, members noted that this increase in approvals had not yet translated into faster growth in housing credit. The pace of growth in housing credit for owner-occupiers had been fairly steady since the beginning of the year and the stock of housing credit for investors had continued to decline a little.

Financial market pricing indicated that a 25 basis points reduction in the cash rate was

largely

priced in for the October meeting, with a further reduction expected by mid 2020.

Financial Stability

Members were briefed on the Bank’s regular half-yearly assessment of the financial system.

Globally, investors were accepting low rates of compensation for bearing risk, despite the increased chance of significantly weaker economic growth. Members noted that a sharp slowdown in global growth could result from an escalation of the US–China trade and technology disputes or geopolitical tensions in the Middle East, Hong Kong or the Korean peninsula. Central banks had eased monetary policy in response to the potential for weaker growth, and additional easing was expected by markets, leading to falls in long-term government bond yields. Despite the increased uncertainty, risk premiums were low and in some cases had fallen further. The lower risk-free interest rates and low term, credit and liquidity risk premiums had seen many asset prices increase further. Any shock that caused markets to increase risk premiums or revise upwards expectations of future policy rates, such as a pick-up in inflation without accompanying stronger growth, could see a broad range of asset prices fall. Given debt levels were high in some non-financial sectors in some economies, a fall in asset prices could result in financial stress for some businesses and households, which could spill over to financial institutions.

Members observed that there had been strong growth in corporate debt in the United States, France

and

Canada, particularly lower-quality debt. Members noted that borrowers whose credit ratings fell

below

investment grade, and who relied on market-based finance, could face difficulty accessing

funding, given

many investors’ mandates were constrained by credit ratings. The interaction of high

sovereign debt

and less resilient banks in Japan and some European economies was also seen as a risk. However,

in the

United States and the United Kingdom, the resilience of the banking system had increased as

profitability had improved.

Corporate debt in China had increased sharply over the previous decade, although in relation to

GDP it

had declined recently in response to policy measures to promote deleveraging. These measures

included

closing some unprofitable state-owned firms, restructuring some debt, reducing the size of

non-bank

financing and reducing non-banks’ interactions with banks.

In Australia, near-term risks related to the housing market had eased in the preceding few months with a turnaround in housing prices in Sydney and Melbourne. Prices in those cities had fallen by a little under 10 per cent over the preceding 18 months, reducing the housing equity of households and resulting in a small share with negative equity. The recent increase in housing prices in those cities had reduced the risk of large increases in negative equity, which could result in losses for lenders if declines in income reduced households’ ability to meet debt repayments. Half of all loans in negative equity were in Western Australia and the Northern Territory, where housing price declines had persisted over the previous few years. Members noted that the rate of mortgage arrears in Western Australia had increased by more for riskier types of lending, including lending with smaller deposits, higher repayments relative to income, and loans to investors and self-employed borrowers.

Despite the high level of household debt in Australia relative to other countries, the risks from household debt appeared to be mostly contained. While the share of mortgages in arrears had continued to rise, it remained at a low rate relative to many other countries and in absolute terms. In addition, the quality of new lending had increased in recent years. The shares of loans with high loan-to-valuation ratios and with interest-only repayment terms had declined following a focus by regulators on this higher-risk lending. Further, members noted that households continued to have large prepayments on their housing debt. In aggregate, mortgage prepayments were equal to two-and-a-half years of repayments. However, while one-third of borrowers had prepayments exceeding two years of mortgage repayments, a slightly lower share had very little or no buffers. Of these, a little less than half appeared more likely to be vulnerable to shocks to their ability to meet their mortgage payments.

The resilience of Australian banks had increased since the financial crisis. Banks had largely

completed their transition to their higher ‘unquestionably strong’ capital ratios.

Banks’ resilience would increase further with the introduction by the Australian Prudential

Regulation Authority of a Loss Absorbing Capacity (LAC) regime, which will require banks to

raise an

additional 3 percentage points of capital by 2024. Members observed that banks were already

issuing

new Tier 2 securities to meet their LAC requirements. Banks’ profitability had

declined a

little over the prior year or two, although banks remained highly profitable. The increase in

housing

arrears had resulted in a small decline in banks’ overall asset quality, although asset

quality

remained high. Rates of non-performing business loans were a little below rates for housing

loans.

Members also discussed non-financial risks facing the financial system. Members noted that cyber

risks,

and IT risks more broadly, were increasing as technology systems become more complex and

embedded in all

operations. Members also noted that climate change presented a risk to financial institutions.

While

extreme weather events were thought unlikely to produce large losses for the financial system as

a

whole, at least at present, losses could be larger in future if financial institutions do not

manage the

risks carefully.

Considerations for Monetary Policy

In considering the policy decision, members observed that the risks to the global growth outlook remained tilted to the downside. The trade and technology disputes between the United States and China were affecting international trade and investment, as businesses scaled back their spending plans in response to increased uncertainty. In China, the authorities had taken further steps to support the economy, while continuing to address risks in the financial system. In most advanced economies, inflation remained subdued despite low unemployment rates and rising wages growth.

In this context, global interest rates had continued to decline, with the central banks in the

United

States and Europe reducing interest rates in the previous month. Further monetary easing was

widely

expected, as central banks continued to respond to the downside risks to the global economy and

subdued

inflation. Long-term government bond yields were close to record lows in many countries,

including in

Australia. Borrowing rates for both businesses and households were at historically low levels,

and the

Australian dollar was at its lowest level in recent years.

Members considered the case for a further easing in monetary policy at the present meeting, to support employment and income growth and to provide greater confidence that inflation would be consistent with the medium-term target. Members noted that the Bank’s most recent forecasts suggested that the unemployment and inflation outcomes over the following couple of years were likely to be short of the Bank’s goals. The most recent run of data had not materially altered this assessment and, on balance, had been on the softer side. The ongoing subdued rate of wages growth also suggested that the economy still had spare capacity. There was therefore a case to respond to the general outlook with a further easing of monetary policy.

Members were mindful, however, that monetary policy was already expansionary and that the lower

exchange rate was also supporting growth. They acknowledged that these factors and the recent

tax cuts

could combine to boost growth by more than their individual effects would imply, especially

given the

context of the mining and established housing sectors seeming to have reached turning points. At

the

same time, members recognised that it was possible that the effects may be smaller than expected

and the

global risks were to the downside.

Members also considered the argument that some monetary stimulus should be kept in reserve to address any future negative shocks. However, that argument requires changes in interest rates to be the key driver of demand, rather than the level of interest rates, which experience has shown to be the more important determinant. Members concluded that the Board could reduce the likelihood of a negative shock leading to outcomes that materially undershot the Bank’s goals by strengthening the starting point for the economy.

The Board’s discussions also focused on the ongoing strength in employment growth. The

period of

strong employment growth had not reduced spare capacity in the labour market significantly.

Almost all

of the strength in employment growth over the preceding three years had been matched by higher

participation, so there had been little progress on reducing unemployment and underemployment.

It was

also possible that participation was rising partly in response to weak growth in incomes.

Moreover,

employment growth was forecast to slow over the period ahead.

Members also discussed the possibility that policy stimulus might be less effective than past experience suggests. They recognised that some transmission channels, such as a pick-up in borrowing or the effect on the home-building sector, may not be operating in the same way as in the past, and that the negative effect of low interest rates on the income and confidence of savers might be more significant. Notwithstanding this, transmission through the exchange rate channel was still considered likely to work effectively, and evidence suggested that the positive effects of lower interest rates on aggregate household cash flows via lower debt repayments was likely to support household spending, given that household interest payments exceed receipts by more than two to one.

Members also noted that the housing market and other asset prices might be overly inflated by lower interest rates. Members acknowledged that asset prices were part of the transmission mechanism of policy, including by encouraging home building. By themselves, higher asset prices were considered unlikely to present a risk to macroeconomic and financial stability. This assessment would need to be reviewed if rapidly increasing asset prices were accompanied by materially faster credit growth, weak lending standards and rising leverage. Although household debt was still considered high, members saw only a limited risk of excessive borrowing at the current juncture: household disposable income growth (and thus borrowing capacity) is weak; the memory of recent housing price falls is still fresh; and banks are still quite cautious in their appetite to lend. Nonetheless, members assessed that close monitoring of this risk was warranted.

Members concluded that these various factors did not outweigh the case for a further easing of

monetary

policy at the present meeting. Taking into account all the available information, including the

reductions in interest rates since the middle of the year, the Board decided to lower the cash

rate by a

further 25 basis points. Members judged that lower interest rates would help reduce spare

capacity

in the economy by supporting employment and income growth and providing greater confidence that

inflation would be consistent with the medium-term target. Members also noted the trend to lower

interest rates globally and the effect this was having on the Australian economy and inflation

outcomes.

Members judged it reasonable to expect that an extended period of low interest rates would be required in Australia to reach full employment and achieve the inflation target. The Board would continue to monitor developments, including in the labour market, and was prepared to ease monetary policy further if needed to support sustainable growth in the economy, full employment and the achievement of the inflation target over time.

The Decision

The Board decided to lower the cash rate by 25 basis points to 0.75 per cent.