According to the Fed, they will conduct another $75 billion worth of repurchase operations on Friday to help keep the federal funds rate within the target of 1 3/4 to 2.0 per cent. So things are still looking out of kilter – perhaps because of the Fed’s earlier balance sheet reduction?

In accordance with the FOMC Directive issued September 18, 2019, the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York will conduct an overnight repurchase agreement (repo) operation from 8:15 AM ET to 8:30 AM ET tomorrow, Friday, September 20, 2019, in order to help maintain the federal funds rate within the target range of 1-3/4 to 2 percent.

This repo operation will be conducted with Primary Dealers for up to an aggregate amount of $75 billion. Securities eligible as collateral in the repo include Treasury, agency debt, and agency mortgage-backed securities. Primary Dealers will be permitted to submit up to two propositions per security type. There will be a limit of $10 billion per proposition submitted in this operation. Propositions will be awarded based on their attractiveness relative to a benchmark rate for each collateral type, and are subject to a minimum bid rate of 1.80 percent.

In the latest RBA Bulletin there is an article on the Committed Liquidity Facility, which is a facility designed to support some of our major banks. Under the CLF, the Reserve Bank will provide an ADI with liquidity via repurchase agreements (repos), for a fee. Since the CLF was introduced in 2015, the number of ADIs that have applied to APRA to have a facility has risen from 13 to 15.

Under the Basel liquidity standard, the liquidity coverage ratio (LCR) requires authorised deposit-taking institutions (ADIs) to have enough high-quality liquid assets (HQLA) to cover their net cash outflows in a 30-day liquidity stress scenario. Jurisdictions with a clear shortage of domestic currency HQLA can use alternative approaches to enable financial institutions to satisfy the LCR – hence the CLF in Australia.

The RBA says the CLF has been in operation for five years and continues to be required given the still relatively low level of government debt in Australia. However, because the volume of HQLA securities has increased over recent years and they appear to have become more available for trading in secondary and repo markets, the Reserve Bank has assessed that the CLF ADIs should be able to raise their holdings to 30 per cent of the stock of HQLA securities. This increase will occur at a pace of 1 percentage point each year, commencing with an increase to 26 per cent in 2020. Taking into account how the CLF ADIs have responded to the framework between 2015 and 2019, the Reserve Bank has also concluded that the CLF fee should be increased from 15 basis points to 20 basis points by 2021; this is to proceed in two steps, with the fee rising to 17 basis points on 1 January 2020 and to 20 basis point on 1 January 2021.

These pricing changes will have only a minor impact on the CLF Banks in terms of their net interest margins, at a time when many other factors are in play, such as reductions in the RBA’s cash rate, competition for mortgages and the yield curve driving pricing in the 2-5 years portion of banks treasury portfolios.

But there are two bigger questions to ask and answer. First, given the size of Government debt now, and the flow of bonds available, why do we still need this facility at all?

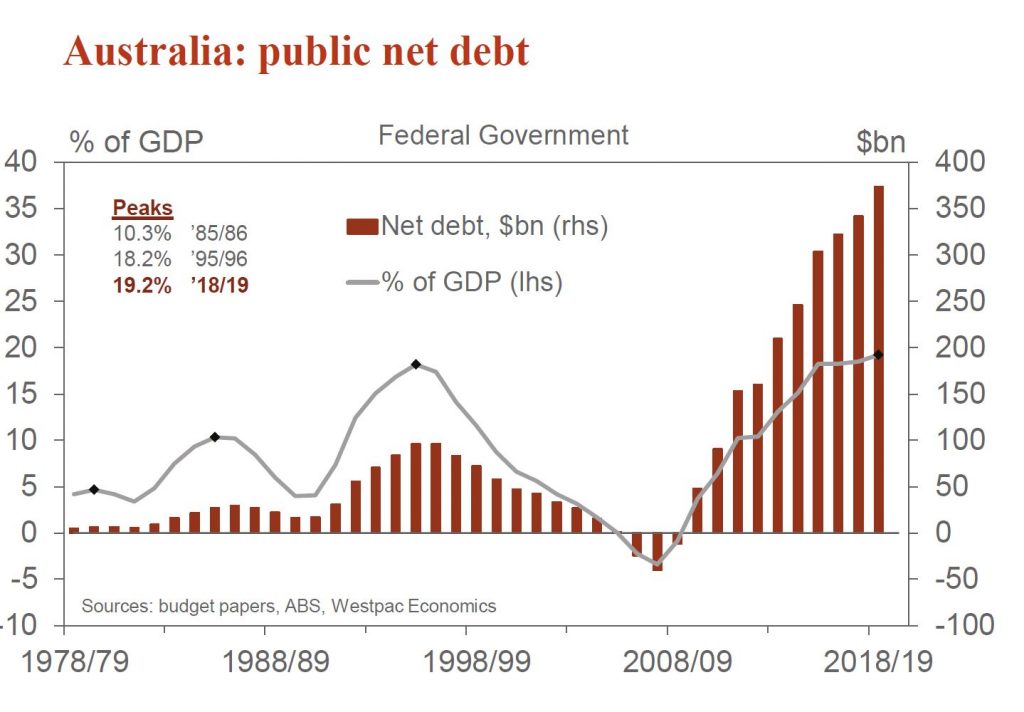

Net general government debt at June 2019 is $374bn (19.2% of GDP), some $12.5bn higher than forecast in the April 2019 Budget

The answer to that, and the second point is the CLF is essentially a back-door QE measure. If international liquidity became an issue, or if rate decreases triggered a capital flight, the CLF allows the RBA to step in and fund the banks’ funding shortfall from a loss of international investors, at rates below the banks’ international funding rates. Thus, high cost international funding by the banks can easily be replaced by cheap RBA funding through a form of QE or money printing subsidising bank profits and banker bonuses – for a short period.

This also distorts the markets because there are many lenders unable to get the CLF, creating a two-tier banking system with the “blessed” 15 supported by the CLF.

This is what the RBA says:

The Reserve Bank provides the Committed Liquidity Facility (CLF) as part of Australia’s

implementation of the Basel III liquidity standard.[1] This framework has been designed to improve the

banking system’s resilience to periods of liquidity stress. In particular, the liquidity coverage

ratio (LCR) requires authorised deposit-taking institutions (ADIs) to have enough high-quality liquid

assets (HQLA) to cover their net cash outflows in a 30-day liquidity stress scenario. Under the Basel

liquidity standard, jurisdictions with a clear shortage of domestic currency HQLA can use alternative

approaches to enable financial institutions to satisfy the LCR. These include the central bank offering a

CLF. This is a commitment by the central bank to provide funds secured by high-quality collateral through

the period of liquidity stress. This commitment can then be counted by the ADI towards meeting its LCR

requirement given the scarcity of HQLA. The Australian Prudential Regulation Authority (APRA) has

implemented the LCR in Australia, incorporating a CLF provided by the Reserve Bank.[2]

The CLF Is Required Due to the Low Level of Government Debt in Australia

The Australian dollar securities that have been assessed by APRA to be HQLA are Australian Government

Securities (AGS) and securities issued by the central borrowing authorities of the states and territories

(semis). All other forms of HQLA available in Australian dollars are liabilities of the Reserve Bank,

namely banknotes and Exchange Settlement Account (ESA) balances. For securities to be considered HQLA,

the Basel liquidity standard requires that they have a low risk profile and be traded in an active and

sizeable market. AGS and semis satisfy these requirements since they are issued by governments in

Australia and are actively traded in financial markets. In contrast, there is relatively little trading

in other key types of Australian dollar securities, such as those issued by supranationals and foreign

governments (supras), covered bonds, ADI-issued paper and asset-backed securities (Graph 1). Given

this, these securities are not classified as HQLA.

Graph 1

The supply of AGS and semis is not sufficient to meet the liquidity needs of the Australian banking

system. This reflects the relatively low levels of government debt in Australia (Graph 2). When the

CLF was first introduced in 2015, ADIs would have needed to hold around two-thirds of the stock of HQLA

securities to be able to cover their LCR requirements. Such a high share of ownership by the ADIs would

have reduced the liquidity of these securities, defeating the purpose of them being counted on as

HQLA.

Graph 2

Jurisdictions with low government debt have used a range of approaches to address the resulting shortage

of domestic currency HQLA. Australia is one of three countries that have put in place a CLF, along with

Russia and South Africa. Some other jurisdictions have allowed financial institutions to hold HQLA in

foreign currencies to cover their liquidity needs in domestic currency. The main downsides of the latter

approach is that it relies on foreign exchange markets to be functioning smoothly in a time of stress and

increases the foreign currency exposures in the banking system. Some jurisdictions have classified a

broader range of domestic currency securities as HQLA. However, this approach has not been taken in

Australia due to the low liquidity of Australian dollar securities other than AGS and semis.

The Conditions for Accessing the CLF

APRA determines which ADIs can establish a CLF with the Reserve Bank. Access is limited to those ADIs

domiciled in Australia that are subject to the LCR requirement.[3] Before establishing a CLF, these ADIs must

apply to APRA for approval. In these applications, the ADIs have to demonstrate that they are making

every reasonable effort to manage their liquidity risk independently rather than relying on the CLF. APRA

also sets the size of the CLF, both in aggregate and for each ADI.

The Reserve Bank makes a commitment under the CLF to provide a set amount of liquidity against eligible

securities as collateral, subject to the ADI having satisfied several conditions.[4] The ADI is

required to pay a CLF fee to the Reserve Bank that is charged on the entire committed amount (not just

the amount drawn). To access liquidity through the CLF, an ADI must make a formal request to the Reserve

Bank that includes an attestation from its CEO that the institution has positive net worth. The ADI must

also have positive net worth in the opinion of the Reserve Bank.

Under the CLF, the Reserve Bank will provide an ADI with liquidity via repurchase agreements (repos). In

a repo, funds are exchanged for high-quality securities as collateral until the funds are repaid. These

securities must meet criteria set by the Reserve Bank. The types of securities that the ADIs can hold for

the CLF include self-securitised residential mortgage backed securities (RMBS), ADI-issued securities,

supras, and other asset-backed securities. To protect against a decline in the value of these securities

should an ADI not meet its obligation to repay, the Reserve Bank requires the value of the securities to

exceed the amount of liquidity provided by a certain margin. These margins are set by the Reserve Bank to

manage the risks associated with holding these securities.[5] If the CLF is drawn upon, the ADI must also pay

interest to the Reserve Bank for the term of the repo at a rate set 25 basis points above the cash

rate.

The First Five Years of the CLF

Since the CLF was introduced in 2015, the number of ADIs that have applied to APRA to have a facility

has risen from 13 to 15.[6] Each year, APRA sets the total size of the CLF by taking the difference between the

Australian dollar liquidity requirements of the ADIs and the amount of HQLA securities that the Reserve

Bank assesses can be reasonably held by these ADIs (the CLF ADIs) without unduly affecting market

functioning.

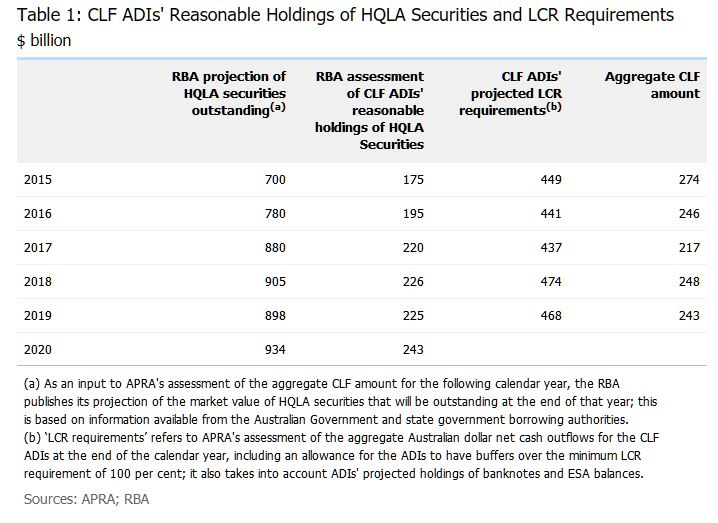

For 2015-19, the Reserve Bank assessed that the CLF ADIs could reasonably hold 25 per cent of

the stock of HQLA securities. In determining this, the Reserve Bank took into account the impact of the

CLF ADIs’ holdings on the liquidity of HQLA securities in secondary markets, along with the

holdings of other market participants. The volume of HQLA securities that the CLF ADIs could reasonably

hold increased from $175 billion in 2015 to $225 billion in 2019, reflecting growth in the stock of HQLA

securities (Table 1). Over the period, the CLF ADIs held a significantly higher share of the stock

of HQLA securities than in the years leading up to the introduction of the LCR (Graph 3). The CLF

ADIs have been holding a larger share of the stock of semis compared to AGS.

Graph 3

The CLF ADIs’ projected LCR requirements, which were used in calculating the CLF, increased

modestly in aggregate from $449 billion in 2015 to $468 billion in 2019. This increase can be entirely

explained by the CLF ADIs seeking to raise their liquidity buffers over time to be well above the minimum

LCR requirement of 100. Reflecting this, the aggregate LCR for these ADIs increased from around

120 per cent in 2015 to around 130 per cent in 2019; this was the case for their

Australian dollar liquidity requirements as well as for their requirements across all currencies

(Graph 4).[7]

Graph 4

The aggregate CLF amount is the CLF ADIs’ projected LCR requirements less the RBA’s

assessment of their reasonable holdings of HQLA securities. APRA reduced the aggregate size of the CLF

from $274 billion in 2015 to $243 billion in 2019. This reflected that the volume of HQLA securities that

the CLF ADIs could reasonably hold increased by more than their projected liquidity requirements over

this period.

From 2015 to 2019, the Reserve Bank charged a CLF fee of 15 basis points per annum on the

commitment to each ADI. The fee is set so that ADIs face similar financial incentives to meet their

liquidity requirements through the CLF or by holding HQLA. The amount of CLF fee paid by the CLF ADIs to

the Reserve Bank declined from $413 million in 2015 to $365 million in 2019, which is in line with the

reduction in the size of the CLF. Since the CLF was established, no ADI has drawn on the facility in

response to a period of financial stress.[8]

Assessing ADIs’ Reasonable Holdings of HQLA Securities

When assessing the volume of HQLA securities that the CLF ADIs can reasonably hold, the Reserve Bank

seeks to ensure that these holdings are not so large that they impair market functioning or liquidity.

For the period from 2015 to 2019, the Reserve Bank assessed that the CLF ADIs could reasonably hold

25 per cent of HQLA securities without materially reducing their liquidity. This was informed

by the fact that a large proportion of HQLA securities were owned by ‘buy and hold’

investors. These investors were price inelastic and generally did not lend these securities back to the

market, reducing the free float of HQLA securities. Many of these investors were non-residents (such as

sovereign wealth funds), which were holding nearly 60 per cent of the stock of HQLA securities

earlier in the decade (Graph 5). So overall, the Reserve Bank concluded that these bond holdings

were not contributing significantly to liquidity in the market.

Graph 5

Over recent years, the volume of HQLA securities has risen and they have become more readily available

in bond and repo markets (Table 1). The Australian repo market has grown considerably, driven by

more HQLA securities being sold under repo. Since 2015, non-residents have emerged as significant lenders

of AGS and semis (and borrowers of cash) in the domestic market (Graph 6). Over the same period,

repo rates at the Reserve Bank’s open market operations have risen relative to unsecured funding

rates (Graph 7). This is consistent with market participants financing a larger volume of HQLA

securities on a short-term basis through the repo market. For this assessment, the increased availability

of HQLA securities in the market suggests that the CLF ADIs should be able to hold a higher share of

these securities without impairing market functioning.

Graph 6

Graph 7

Analysis of transactions in the bond and repo markets using data from 2015–17 suggests that most

HQLA securities were being actively traded.[9] Monthly turnover ratios for AGS bond lines were well above

zero, and much higher than turnover ratios for other Australian dollar securities such as asset-backed

securities, covered bonds, ADI-issued paper and supras (Graph 1). Although semis bond lines were

traded less frequently than AGS, relatively few semis had low turnover ratios (Graph 8). As such,

some increase in ADIs’ holdings of AGS and semis would appear unlikely to jeopardise liquidity in

these markets.

Graph 8

Earlier in the decade, a ‘scarcity premium’ had emerged in the pricing of HQLA securities.

Australia’s relatively strong economic performance and AAA sovereign rating have been of

considerable appeal to investors with a preference for highly rated securities. Higher yields compared to

other AAA-rated sovereigns also contributed to strong demand from foreign investors, particularly for

AGS. The scarcity premium was most prominent before 2015, when the yield on 3-year AGS was well below the

expected cash rate over the equivalent horizon (as measured by overnight indexed swaps (OIS);

Graph 9). However, the scarcity premium has dissipated alongside an increase in the stock of AGS on

issue. This suggests that there is scope for the CLF ADIs to hold more HQLA securities without impairing

market functioning.

Graph 9

Given these developments, the Reserve Bank has assessed that the CLF ADIs should be able to increase

their holdings to 30 per cent of the stock of HQLA securities.[10] To

ensure a smooth transition and thereby minimise the effect on market functioning, the increase in the CLF

ADIs’ reasonable holdings of HQLA securities will occur at a pace of 1 percentage point per

year until 2024, commencing with an increase to 26 per cent in 2020.

The CLF Fee

The Reserve Bank sets the level of the CLF fee such that ADIs face similar financial incentives when

holding additional HQLA securities or applying for a higher CLF in order to satisfy their liquidity

requirements. A useful starting point to assess the appropriate CLF fee is to compare the yields on the

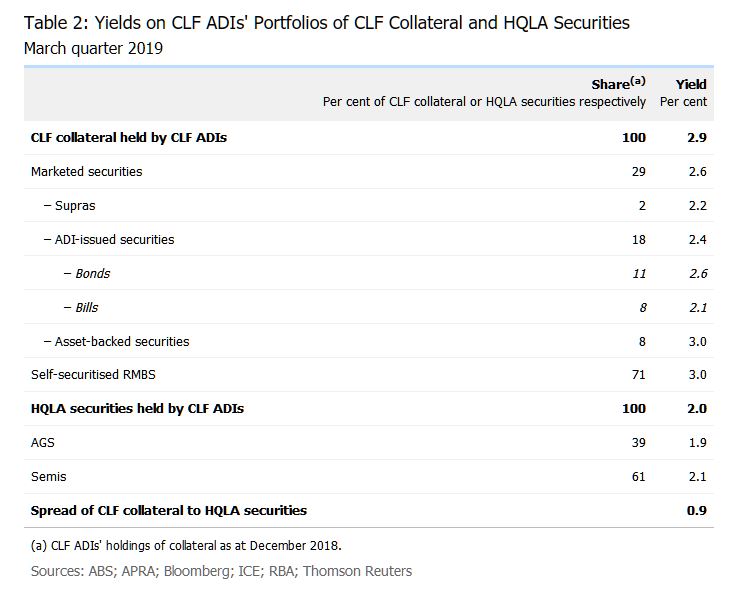

CLF collateral and the HQLA securities held by the relevant ADIs.[11] The Reserve Bank estimated that the

weighted average yield differential between the CLF collateral and the HQLA securities was around

90 basis points in the March quarter 2019 (Table 2). This includes the compensation required by

ADIs to account for the higher credit risk associated with holding CLF collateral rather than HQLA

securities, which would be a sizeable share of the spread. However, it is only the additional liquidity

risk associated with holding CLF collateral that should be reflected in the CLF fee. In practice,

adjusting the spread between CLF collateral and HQLA securities to remove the credit risk component is

not straightforward.

When the Reserve Bank set the CLF fee earlier this decade, it looked at repo rates on some CLF-eligible

securities to gauge how much a one-month liquidity premium might be worth. Before late 2013, it was

possible to separately identify repo rates on government securities (AGS and semis) and private

securities (such as ADI-issued securities) in the Reserve Bank’s market operations. Based on these

data, it was estimated that the one-month liquidity premium for private securities was less than

10 basis points in normal circumstances. However, given that part of the purpose of the liquidity

reforms was to recognise that the market had under-priced liquidity in the past, it was judged to have

been appropriate to set the fee at 15 basis points.

It has since become more difficult to gauge a liquidity premium by using repo rates. In particular, in

late 2013 the Reserve Bank ceased to charge different repo rates for government and private securities.

Instead, the Bank revised its margin schedule to manage the credit risk on different types of collateral

accepted under repo. Moreover, most of the collateral now being purchased by the Reserve Bank under repo

is HQLA securities. This suggests that repo rates mostly reflect the price for converting HQLA securities

into ESA balances, rather than CLF collateral into HQLA.

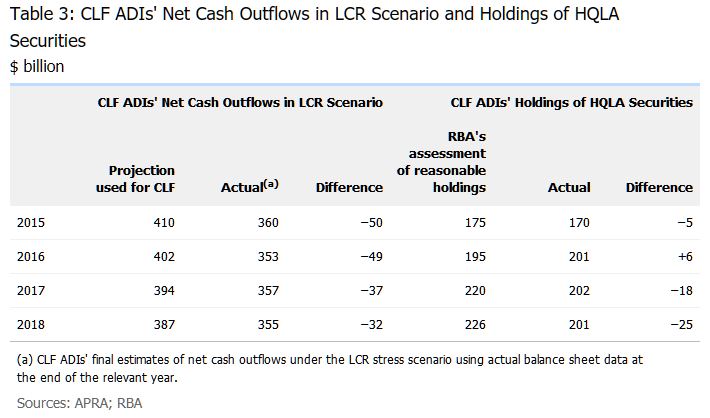

At the same time, it is now possible to take into account how the CLF ADIs have responded to the

existing framework when setting the future CLF fee. Since the CLF was introduced, the CLF ADIs (in

aggregate) have consistently overestimated their liquidity requirements (Table 3). This has resulted

in the CLF ADIs being granted larger CLF amounts, which they have mainly used to hold larger buffers

above the minimum required LCR of 100 (Graph 4).[12] In recent years, the CLF ADIs have also been

holding fewer HQLA securities than the Reserve Bank had judged could be reasonably held without impairing

the market for HQLA securities. Taken together, these two observations suggest that the CLF fee should be

set at a higher level in future.

However, there is uncertainty about the exact level of the fee that would make ADIs indifferent between

holding more HQLA or applying for a larger CLF. If the CLF fee is set too high, this could trigger a

disruptive shift away from using the facility and distort the markets that use HQLA. This has potential

implications for the implementation of monetary policy, since the market that underpins the cash rate

involves the trading of ESA balances, which are also HQLA.[13] The remuneration on ESA balances is purposefully

set at a rate of 25 basis points below the cash rate target in order to encourage ADIs to recycle

their surplus ESA balances rather than holding them. There are scenarios where holding ESA balances could

be a cheaper way to satisfy the LCR than holding HQLA securities. For instance, earlier in the decade,

the yield on AGS was at or below the expected return from holding ESA balances (Graph 9). In this

context, the CLF fee should be set such that ADIs would not have an incentive to meet their LCR

requirements by holding excessive ESA balances.

As a result of these considerations, the RBA has concluded that the CLF fee should be increased

moderately. This should ensure that ADIs have strong incentives to manage their liquidity risk

appropriately, without generating unwarranted distortions in the markets that use HQLA. To ensure a

smooth transition by minimising the effect on market functioning, the increase will occur in two steps,

with the CLF fee rising to 17 basis points on 1 January 2020 and to 20 basis points on 1

January 2021.[14]

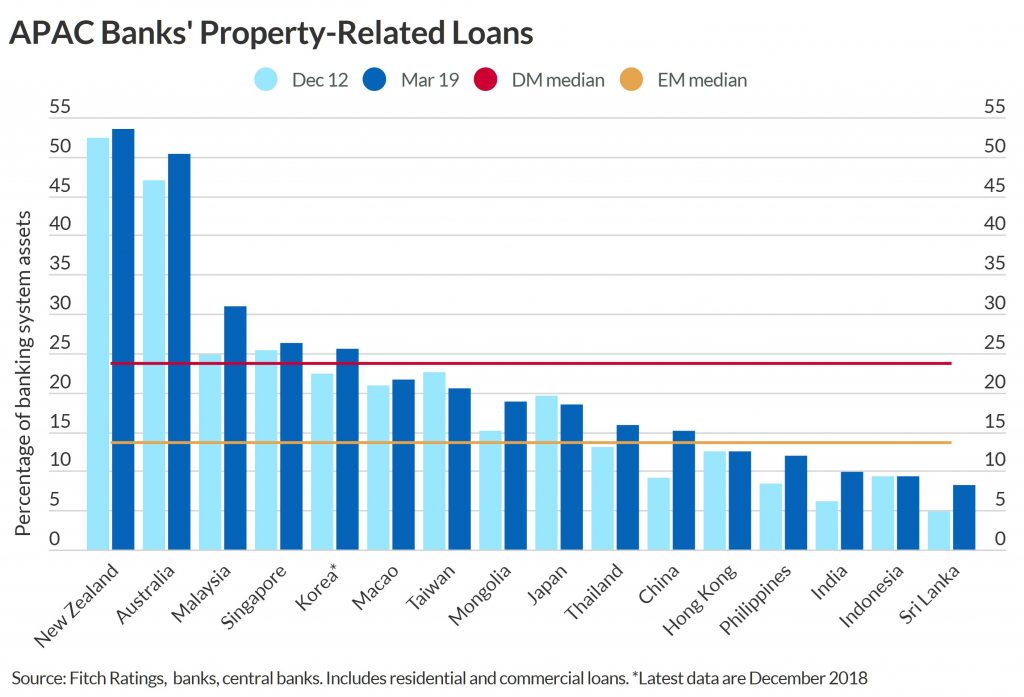

Banks in the Asia-Pacific region are increasingly exposed to property-related risks, Fitch Ratings says in a new report. The Australian and New Zealand banking sectors have the greatest exposure to property market stress, while banks in Sri Lanka, Mongolia and Vietnam have the least protection from loss-absorption buffers. We believe that regulatory oversight and macro-prudential policies should contain the direct effect of a residential property downturn on banks, especially in developed markets where loss-absorption buffers tend to be higher. However, accommodative monetary and economic policies could aggravate leverage.

Rising household debt increases risks for banks as borrowers’ debt-servicing capacity becomes more sensitive to economic factors, and a high reliance on property to collateralise loans exposes banks in a property market downturn. Regulators in most of the region’s developed markets have introduced macro-prudential measures to stem property-sector risks and to strengthen banking-sector resilience to potential property stress. We believe that policymakers will remain focused on measures that support stability and prevent risks of overheating, despite recent macro-prudential loosening in Australia, New Zealand and Taiwan to support their economies. We expect Hong Kong, Singapore and South Korea to maintain the tighter bias in their policy settings.

In general, developed economies in Asia have higher banking-sector exposure to property and more indebted household sectors than emerging countries. Australia and New Zealand are two stand-out cases, with household debt-to-GDP ratios of 129% and 94%, respectively, at end-2018. However, banking systems in developed markets have more experience of managing property cycles and stronger loss-absorption buffers, and the authorities’ proactive approach should cushion the impact on banks from a property market stress.

In emerging countries, banks’ exposure to the property sector tends to be lower, but risks are building in light of their strong property lending in recent years, due in part to governments relying increasingly on property to support their economies. Rapid credit growth often masks asset-quality issues, and rising property exposure makes banks more vulnerable to a property downturn, particularly where loss-absorption buffers are lowest (Mongolia, Sri Lanka and Vietnam). Property-related risks in India and Sri Lanka may be understated due to indirect exposures and limited data transparency.

Vietnamese banks appear susceptible in light of rapid consumer loan growth coupled with large legacy bad-debt issues and thin capital buffers. That said, a significant deterioration in Vietnam’s property market seems remote amid strong economic prospects.

In China, banks’ property

exposure has increased significantly over the past decade, but only to

15% of banking sector assets at end-March 2019, while household

debt-to-GDP had risen to 53% by end-2018 from 30% at end-2012. The risks

may be partly mitigated by macro-prudential and other measures, but the

Chinese authorities frequently intervene to manage the housing sector.

However, rising household debt adds to the challenges for domestic

consumption and the financial sector.

Superfund-owned bank ME has shelved plans to launch new credit cards after witnessing the success of “buy now, pay later” players like Afterpay and Zip, via Investor Daily.

The

bank posted its full-year results this week, which showed that

statutory net profit after tax fell by nearly 25 per cent to $67.1

million, down from $89.1 million the previous year. The lender recorded

$14.4 million of impairment losses in its credit card business.

ME

CEO Jamie McPhee said the bank halted its work in bringing more credit

cards to market after recognising a structural shift away from cards and

was therefore focusing its work on digital wallets.

He

explained: “Our work on digital wallets is progressing. We wanted to

bring that forward, and we’ve taken the opportunity to relook at the

credit card market, and what we’ve been seeing is that the number of

credit cards are in decline, while we’ve seen a significant increase in

the buy now, pay later entrants Afterpay, Zip, Flexi,” he said.

“We

think that the credit card market is being structurally disrupted, so

we’ve decided that we don’t think that is the right environment for the

bank to go forward in.”

Mr McPhee added that while the bank will

continue to have its low-rate credit card, it has revised its strategy

regarding a wider product range.

“We were thinking of coming to

market with a broader range of credit cards, including reward cards,

etc. but having had a look at the market, we don’t think that is the

right thing to do, strategically, going forward,” he said.

“So, that has obviously impacted the statutory earnings this time around.

“There

is no way we will be diverting our attention away from building out the

customer digital ecosystem like the digital wallets, NPP (national

payments platform), until we get that right up to a very, very market

competitive offerings.

“That will be our focus for the foreseeable focus. Anything else would be a distraction.”

It is expected that ME will be releasing its “digital ecosystem” progressively from 2020.

We look at today’s data, the Fed cut, the repo issue, and locally the

engineered balanced budget and higher unemployment. Many echos of a

decade back, is history repeating?

Latest on the cash ban, which was presented in Parliament today, with Robbie Barwick from the CEC.

On 19 September 2019, the Senate referred the provisions of

the Currency (Restrictions on the Use of Cash) Bill 2019 [Provisions] to the Economics Legislation Committee for inquiry and report by 7 February 2020.

If you’d like to be part of a delegation to visit your local MP, call the CEC on 1-800 636 432 to be put in touch with others in your area.

Use and share these links for finding MPs and Senators. Click the link, and find the heading State/Territory in the box titled Refine Search on the right hand side of the page. Click on your state and call as many MPs and Senators as you can, on their Parliament House numbers, starting with 02-6.

If today’s second consecutive repo was supposed to calm the stress in the secured lending market and ease the funding shortfall in the interbank market, it appears to have failed says Zerohedge.

As the WSJ said on Tuesday:

For the first time in more than a decade, the Federal Reserve injected cash into money markets Tuesday to pull down interest rates and said it would do so again Wednesday after technical factors led to a sudden shortfall of cash.

The pressures relate to shortages of funds banks face resulting from an increase in federal borrowing and the central bank’s decision to shrink the size of its securities holdings in recent years. It reduced these holdings by not buying new ones when they matured, effectively taking money out of the financial system.

Bloomberg said while the spike wasn’t evidence of any sort of imminent financial crisis, it highlighted how the Fed was losing control over short-term lending, one of its key tools for implementing monetary policy. It also indicated Wall Street is struggling to absorb record sales of Treasury debt to fund a swelling U.S. budget deficit. What’s more, many dealers have curtailed trading because of safeguards implemented after the 2008 crisis, making these markets more prone to volatility.

The Federal Reserve made crystal clear that it doesn’t want U.S. money market rates to spike again like they did early this week, announcing it will — for the third day in a row — inject cash into this vital corner of finance.

On Thursday, the New York Fed will offer up to $75 billion in a so-called overnight repurchase agreement operation, adding another dose of temporary liquidity to restore order in the banking system. It made the same offer Tuesday and Wednesday, deploying a tool it hadn’t used in a decade. This latest action follows the Fed’s reduction in the interest rate on excess reserves, or IOER, another attempt to quell money-market stresses.

The prior operations have calmed markets, with repo rates declining Wednesday to more normal levels after jumping to 10% on Tuesday, four times where it was last week.

In addition, as Credit Swiss points out, Basel changed the rules:

The longer term issue is that the definition of “excess reserves” has changed in a Basel III environment. Previously excess reserves were defined by the Fed’s standard. If banks held more in the Federal Reserve accounts than they needed to settle transactions with one another, they had excess reserves. Now, under Basel III, excess reserves are defined by a global standard. Banks not only need enough reserves to settle accounts with one another at the end of each day – they also need to hold enough reserves for liquidity and capital buffer purposes. Indeed, reserves are better “high quality liquid assets” (HQLA) than even US Treasuries. In this context, at the beginning of 2017 (when Basel III really kicked in), banks found themselves with excess reserves by Fed standards, but deficient reserves by Basel III standards. Making matters worse for a little while were the Fed’s balance sheet reduction efforts, draining reserves from the system

This could be a signal of a potential liquidity crisis (echoes of 2007?).

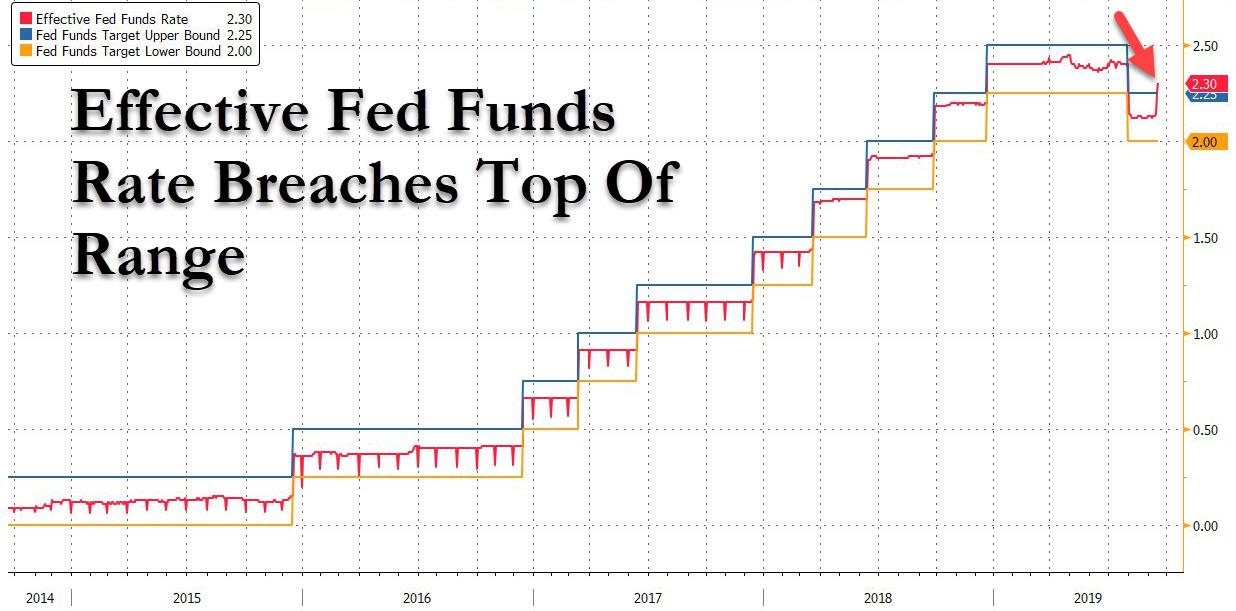

Zerohedge says not only did O/N general collateral print at 2.25-2.60% after the repo operation, confirming that repo rates remain inexplicably elevated even though everyone who had funding needs supposedly met them thanks to the Fed, but in a more troubling development, the Effective Fed Funds rate printed at 2.30% at 9am this morning, breaching the Fed’s target range of 2.00%-2.25% for the first time.

Source: Bloomberg, Zerohedge

And yes, it is quite ironic that on the day the Fed is cutting rates,

the Fed Funds was just “pushed” above the top end of the target range

for the first time ever.

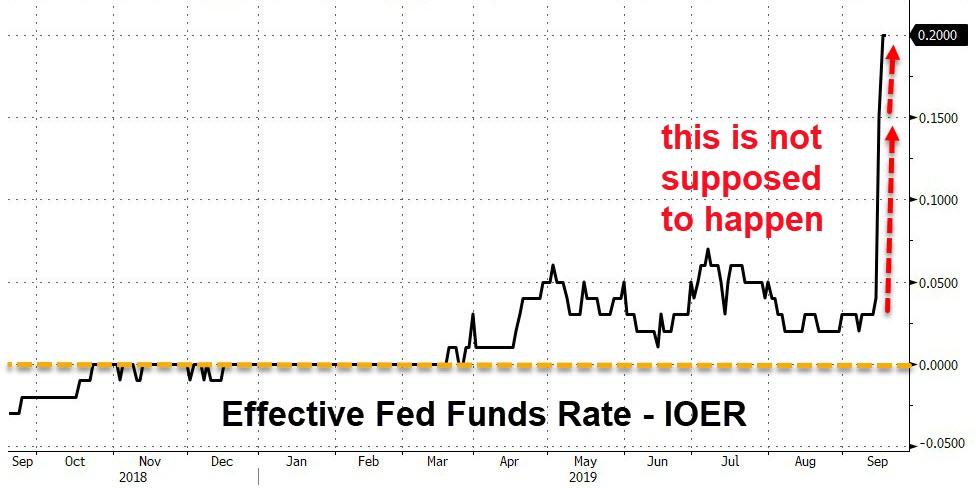

This also means that the EFF-IOER spread has now blown out to an

unprecedented 20bps, yet another indication that the Fed has lost

control of the rates corridor.

Source: Bloomberg, Zerohedge

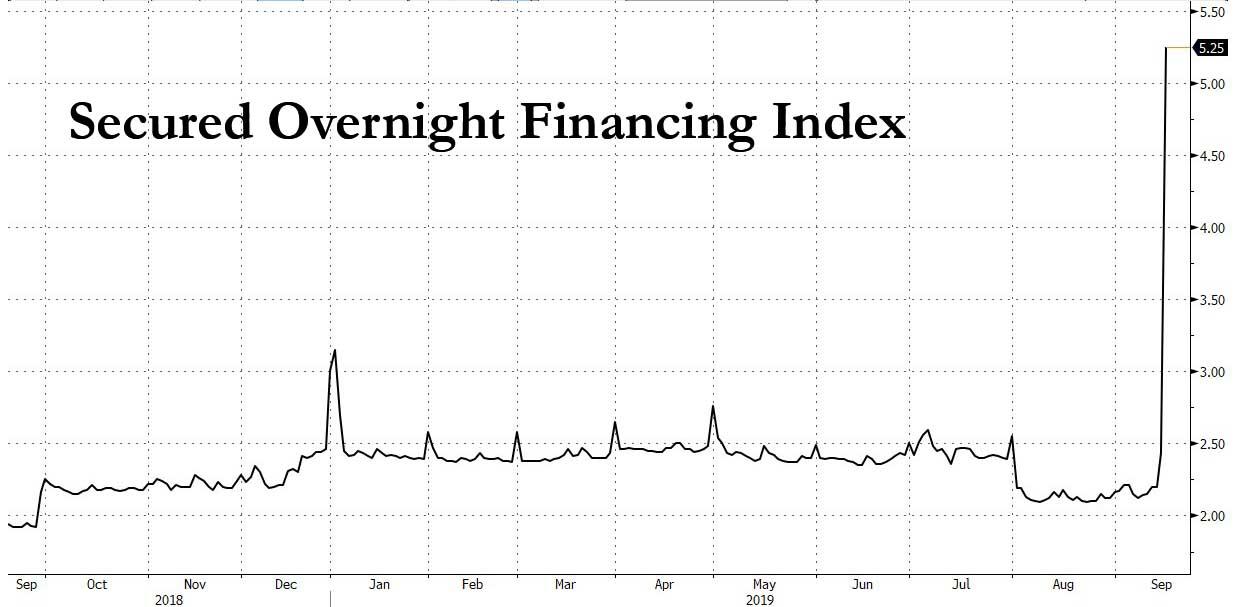

But in what may be the most concerning move, today’s print for the

Secured Overnight Financing Index (SOFR), which is widely expected to be

Libor’s replacement, exploded higher by 282bps to a record 5.25%.

Source: Bloomberg, Zerohedge

Commenting on the blow out in the SOFR, Goldman had this to say on

the “extremely volatile” price action in the key funding index:

The SOFR market saw extremely volatile price action over the course

of the day…. Almost 20k in SERU9 blocks printed from 11:15am through

the afternoon, pushing SERFFU9 from -10 to -21.5. Shortly after 4pm the

market was given another jolt of adrenaline as news of a second Fed

operation to be conducted tomorrow morning at 8:15am caused the spot-6mo

curve to go bid into the close.

The problem here is that since SOFR is expected to replace LIBOR as

the reference rate for several hundred trillions in fixed income

securities, a spike such as this one would be perfectly sufficient to

wreak havoc across market if indeed it had been the key reference rate.

Finally, courtesy of BMO’s Jon Hill, here is some commentary on today’s oversubscribed, and clearly insufficient, repo operation by the Fed:

Today’s emergency repo operation was oversubscribed with $51.6 bn in

Treasury and $22.8 bn in MBS collateral accepted. The weighted average

in USTs was 2.215%, with a high rate of 2.36% and a low of 2.10%. This

should help alleviate some stress in USD funding markets, and the fact

that it’s occurring earlier in the morning than Tuesday should help keep

daily averages more subdued than yesterday – SOFR printed at a

remarkable 5.25% (a stunning 282 bp spike) with fed funds still unknown

but scheduled to be released at 9:00 AM ET and likely to print outside

of the target range.

If Powell is successful at guiding the market toward assuming a

mid-cycle adjustment, one specific repricing that will occur is in 2020

forwards, which are still factoring in one and a half 25 bp cuts next

year as shown in the attached (admittedly, precision here is difficult

due to the illiquidity of the Jan ’21 contract). This contrasts with the

FOMC’s desire to execute a more modest drop in overnight rates and the

price response here will be a focal point in determining how markets are

responding to the impending Fed communication. If Powell is effective,

look for that area of the curve to steepen sharply.

The Fed chair Jerome Powell said after the decision ” We don’t see a recession, we’re not expecting a recession, but are are making monetary policy more accommodative”, saying it is a mistake to hold onto your firepower until a downturn has gathered moment. This was seen by the market as “hawkish”, much to Trump’s annoyance! The US dollar was stronger after the announcement.

Information received since the Federal Open Market Committee met in July indicates that the labor market remains strong and that economic activity has been rising at a moderate rate. Job gains have been solid, on average, in recent months, and the unemployment rate has remained low. Although household spending has been rising at a strong pace, business fixed investment and exports have weakened. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In light of the implications of global developments for the economic outlook as well as muted inflation pressures, the Committee decided to lower the target range for the federal funds rate to 1-3/4 to 2 percent. This action supports the Committee’s view that sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective are the most likely outcomes, but uncertainties about this outlook remain. As the Committee contemplates the future path of the target range for the federal funds rate, it will continue to monitor the implications of incoming information for the economic outlook and will act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.

In determining the timing and size of future adjustments to the

target range for the federal funds rate, the Committee will assess

realized and expected economic conditions relative to its maximum

employment objective and its symmetric 2 percent inflation objective.

This assessment will take into account a wide range of information,

including measures of labor market conditions, indicators of inflation

pressures and inflation expectations, and readings on financial and

international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair, John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; Richard H. Clarida; Charles L. Evans; and Randal K. Quarles. Voting against the action were James Bullard, who preferred at this meeting to lower the target range for the federal funds rate to 1-1/2 to 1-3/4 percent; and Esther L. George and Eric S. Rosengren, who preferred to maintain the target range at 2 percent to 2-1/4 percent.

Fitch Ratings says residential mortgage loans in Scandinavia, the Netherlands and Switzerland have seen exceptionally strong performance despite high loan-to-value (LTV) ratios and significant household debt. This reflects generous social security systems and large household wealth, which are a common denominator of these ‘AAA’ rated jurisdictions with strong public finances.

The growth of housing

debt in Scandinavia, the Netherlands and Switzerland can be explained

by a combination of tax deductibility, low interest rates, and unique

features of each respective mortgage market. These include long

contractual tenors and interest-only periods. Limited repayment has made

borrowers more sensitive to house price decreases. However,

macro-prudential requirements in each country are helping to address the

risk that high household debt could jeopardise financial stability.

Macro-prudential

measures were originally focused on maximum LTV and stressed

affordability at origination, but lower mortgage rates continued to

stimulate mortgage growth. Banking authorities therefore imposed minimum

mortgage loan amortisation as well as maximum loan-to-income (LTI) or

debt-to-income ratios. Such restrictions have contributed to the recent

adjustment in Norwegian and Swedish house prices and limited lending

growth in Denmark. Swiss regulators have tightened capital requirements

for banks and promoted self-regulation, which established minimum

amortisation for mortgages above 66% LTV. Gradual changes to tax

incentives and underwriting standards were introduced by the Dutch

authorities, especially since 2013, which have made the mortgage market

more resilient.