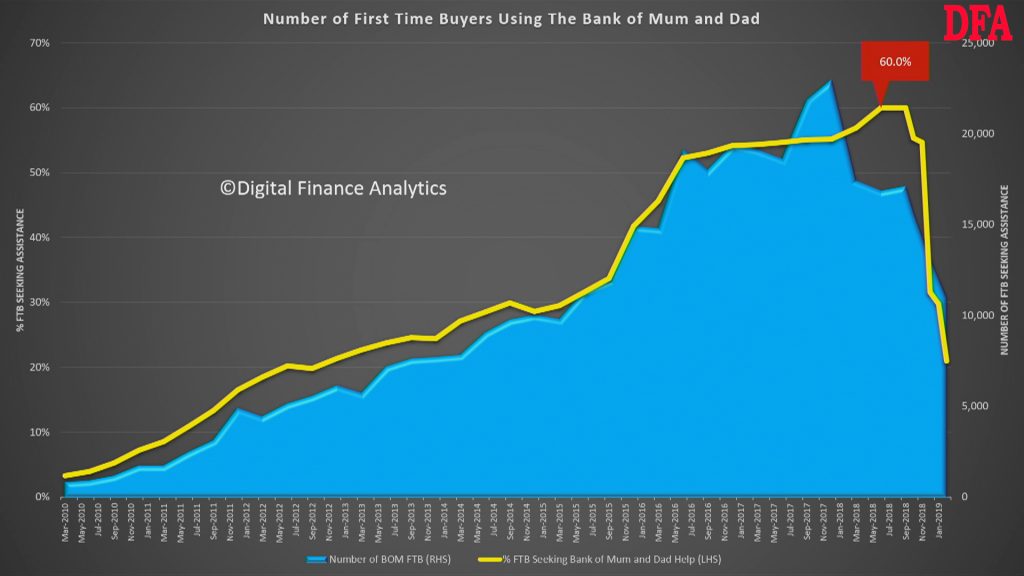

Latest data released today from the DFA household surveys shows that a smaller number of potential first time buyers are now getting help from their parents to buy property.

This video explains what is going on.

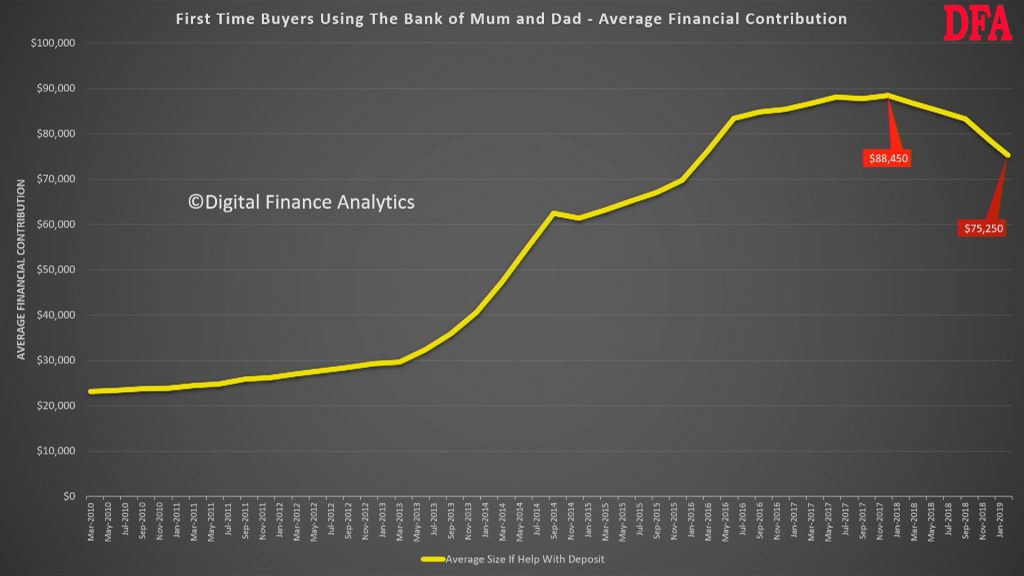

At its height 60% of first time buyers were getting help from their parents, but this has now dropped to 20%. In addition the value of that help has fallen from around $88,000 to around $75,000, on average.

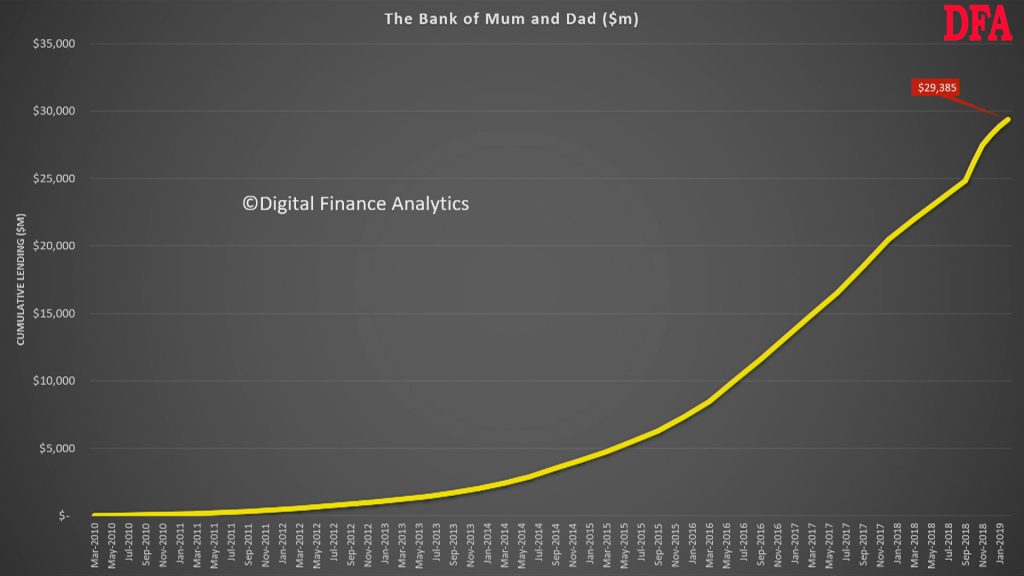

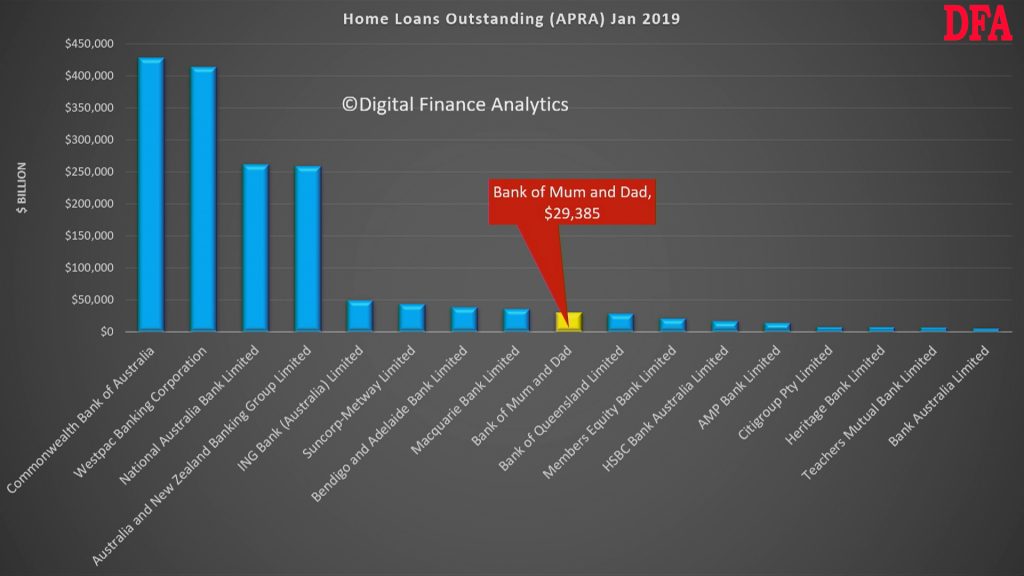

That said the total amount lent by the Bank of Mum and Dad is approaching $30 billion.

This puts the Bank of Mum and Dad among the top-10 lenders in Australia, based on the latest APRA data, in terms of loan stock.

Three drivers explain these changes. First parents are more concerned in a falling market about the equity in their property, when facing into retirement. The “ATM” has run dry. They cannot afford to pass money down the generation now.

Second despite some incentives, such as those in the Northern Territories, announced recently, many first time buyers are preferring to wait, rather than buy into a falling market and risk loosing their deposits. Plus we know that those who get help from parents are twice a likely to default in the subsequent 5 years compared with those who saved.

Third, banks are reluctant to lend, and a seagull payment is not regarded well, compared with a record of regular savings. Some lenders have stopped lending to borrowers with a Bank of Mum and Dad deposit.

Thus we think the momentum we saw last year is slowing and the Bank of Mum and Dad may be a less important factor ahead.

Some parents may decided to help pay monthly mortgage payments instead as this is a more flexible alternative and does not risk capital.

Excellent insights from Steen Jakobsen at Saxobank, who has declared that monetary policy is dead, as Fed has thrown in the towel, and central banks are committed to defying the business cycle.

Current chair Jerome Powell saw himself as a new Volcker, but last night he cemented his panicky shift since the December FOMC meeting, and instead cut the figure of Alan “the Maestro” Greenspan, who set our whole sorry era of central bank serial bubble blowing in motion.

The Fed’s mission ever since has been a determined exercise in defying the business cycle, and replacing it with an ever-expanding credit cycle.

This latest FOMC meeting has set in motion a race to the bottom, with the European Central bank currently in the lead, but the Fed and the Bank of England are gaining fast.

I am presently in London, and on my way to China and Hong Kong with Saxo’s Gateway to China events. I am joined at these events by the impressive Dr. Charles Su of CIB Research, China. He and I agree on many things, but one in particular:

Monetary policy is dead.

My view has long been that monetary policy is misguided and unproductive, but the difference now is that we are reaching the most major inflection point since the global financial crisis as central bank policy medicine rapidly loses what little potency it had. In the meantime, the harm to the patient has only been adding up: the economic system is suffering fatigue from QE-driven inequality, malinvestment, a lack of productivity, never-ending cheap money and a total lack of accountability.

The next policy steps will see central banks operating as mere auxiliaries to governments’ fiscal impulse. The policy framework is dressed up as “Modern Monetary Theory”, and it will be arriving soon and in force, perhaps after a summer of non-improvement or worse to the current economic landscape. What would this mean? No real improvement in data, a credit impulse too weak and small to do anything but to stabilise said data and a geopolitical agenda that continues to move away from a multilateral framework and devolves into a range of haphazard nationalistic agendas.

For the record, MMT is neither modern, monetary nor a theory. It is a the political narrative for use by central bankers and politicians alike. The orthodox version of MMT aims to maintain full employment as its prime policy objective, with tax rates modulated to cool off any inflation threat that comes from spending beyond revenue constraints (in MMT, a government doesn’t have to worry about balanced budgets, as the central bank is merely there to maintain targeted interest rates all along the curve if necessary).

Most importantly, however, MMT is the natural policy response to the imbalances of QE and to the cries of populists. Given the rise of Trumpism and democratic socialism in the US and populist revolts of all stripes across Europe, we know that when budget talks start in May (in Europe, after the Parliamentary elections) and October (in the US), governments around the world will be talking up the MMT agenda: infrastructure investment, reducing inequality, and reforming the tax code to favour more employment at the low end.

We also know that the labour market is very tight as it is and if there is another push on fiscal spending, the supply of labour and resources will come up short. Tor Svelland of Svelland Capital, who joins Charles and I at the Gateway to China event, has made exactly this point. The assumption of a continuous flow of resources stands at odds with the reality of massive underinvestment.

Central bankers and indirect politicians are hoping/wishing for inflation, and in 2020 they will get it – in spades. Unfortunately, it will be the wrong kind: headline inflation with no real growth or productivity. A repeat of the 1970s, maybe?

Get ready for bigger government and massive policy interventions on a new level and of a new nature. These will be driven by a fiscal impulse to stimulate demand rather than to pump up asset prices. It will lead to stagflation of either the light or even the heavy type, depending on how far MMT is taken.

Last night, a client asked an excellent question: how much of this scenario is already priced in? Here is my take: Saxo’s macro theme since December has been the coming global policy panic, and this has now been fully realised. The Fed proved slower to cave than even the ECB, but last night saw them give up entirely. The US-China trade deal, another key uncertainty, is priced for perfection despite plenty of things that can go wrong.

The Brexit deal, however, is extremely mispriced. The UK’s biggest challenge may not even be the circus act known as Brexit, but rather the collapsing UK credit cycle which our economist Christopher Dembik has put at risking a 2% drop in UK GDP. If nothing changes over the next six to nine months, and nothing will change, the UK economy will be in free fall. Forget Brexit, UK assets are simply mispriced from the lack of credit juice in the pipeline.

The overall China-bound inflow over the next three to five years will exceed $1 trillion China is also misunderstood and mispriced. If our two talks so far with clients on China and its opening up of its markets have taught me anything, it is that the western ‘reservation’ on anything Chinese is entirely built on bias. Governance is the word that keeps coming back in discussions. I am no fan of Chinese-style governance, but… less than 10% of global AUM is currently in China. This year alone will see the inclusion of China’s bonds in global indices like Barclays, Russell, and S&P and the allocation to China in the MSCI’s emerging markets index will quadruple from 5% to 20%. The overall China-bound inflow over the next three to five years will exceed $1 trillion using very conservative estimates.

China is perhaps the country in the world least likely to treat inbound capital poorly. It has transitioned from being a capital exporter to now being an importer. It has a semi-closed capital account, which means little money flows out, but a massive inflow is beginning to stream in as global investors acquire Chinese assets.

China and its growth model now need to share the burden of becoming an industrialised country, and Beijing knows that only the only way keep the capital flowing in 2019 is to treat investors well. On the domestic front, meanwhile, the CPC seems to be signaling that it wants domestic investors to move excess savings from the ‘frothy’ and less productive housing market to the equity market, where capital can flow to more productive enterprises. Foreign investors are more likely to want to participate in the more liquid and familiar equity market.

2019 for China is like 2018 for the US. The first 10 months of 2018 saw the US stock market near-entirely driven by the buy-back programmes fueled by Trump’s tax reform. US companies plowed over $1 trillion into buybacks over the year. This year, the Chinese government is telling its 90 million domestic retail investors to raise their allocation to the stock market while global capital allocators/investors will need to increase their exposure to China as its capital markets are reweighted.

The lending landscape has changed dramatically over the past year, with near-prime lending becoming the fastest-growing sector and lenders beginning to see the rise of “super prime” borrowers; via The Adviser.

Given

the reduced risk appetites from the banks following the banking royal

commission and an increasing trend from the majors to “simplify” their offerings, the non-bank lenders have taken a growing proportion of market share

as more borrowers fall outside of the credit policies and brokers turn

to non-banks for more specialised products for their clients.

Speaking on The Adviser Live webcast yesterday (21 March) for the Leadership Series – the Changing Lending Landscape,

leading non-bank representatives outlined how the lending market was

changing and what brokers can do to ensure they are across all the

changes and offering solutions to their clients.

One

of the themes from the webcast was the rapid rise of near-prime

borrowers, given the reduced number of exceptions that some banks are

willing to accept.

Aaron

Milburn, director of sales and distribution at Pepper, revealed that the

fastest-growing segment of the lending market was near-prime borrowers.

Mr

Milburn said: “Near-prime lending in our industry is the

fastest-growing sector of it. A lot of near-prime [deals] used to be a

major bank deal with a credit exception on it, effectively, [but] that’s

all tightened up now.

“So

the near-prime space is our fastest-growing sector of lending at Pepper

and as an industry. We see that only growing because we see no

relaxation of credit policy at the majors… You think about the gig

economy, you think about people that are Uber drivers, or they do

Airtasker jobs at the weekend and they have been doing that for a

prolonged period of time and they can prove that. Why shouldn’t they use

that income? We see that sort of area growing and that is our

fastest-growing area.”

Mr

Milburn noted that the growing near-prime category was not just

expanding in the residential space but in the commercial space too.

, and Mal Withers has come in to run it for us, and the

near-prime sector of that credit policy, or that product, is growing

substantially fast as well.”

Mr

Milburn elaborated that the near-prime commercial borrower may be a

commercial client who has “a small default” or a “bump in the road in

the past and is trying to get back on their feet”.

“We

think that customer base is bankable, as we do in the near-prime

residential space, and we don’t think they should miss out, so that is

an area of growth for us as well,” he said.

Building

on this, Cory Bannister, VP-chief lending officer at La Trobe

Financial, said that the lender had to “re-categorise” its borrower

segments in the current environment, given the changing borrower

make-up.

He elaborated:

“We’ve even had to re-categorise almost how we determine what’s prime

and near-prime. Now, when we look at it, we look at ‘super prime’, which

we would say is probably what the banks are looking at now.

“Prime,

which is probably the loans that would have been bankable all day,

every day, which have probably slipped out [of major bank’s appetites]

and near-prime is the old traditional space, and specialist sits at the

end of that.”

Mr Bannister

concurred that the near-prime sector was a “growing sector” but added

that these were not necessarily applications that have serious credit

defaults or infringements, but instead borrowers who may have had a

“change of circumstances” such as a variable income or variable

employment.

Looking to the

future, both Mr Milburn and Mr Bannister, as well as Matt Bauld, general

manager, sales and business development at Prospa, agreed that the

non-bank sector would continue to flourish with the support of the

broker space.

Mr Bannister

concluded that he believed broker market share could reach 66 per cent

in the next year, adding: “I think we will see the non-bank market share

continue to grow… I think you’re seeing more of the bank simplification

strategies playing out, more products being exited, [so] non-banks are

doing more of the lifting now to try and provide more solutions.

“The overall credit tightening, I don’t see that being retraced any time soon, that zero exceptions policy is starting to bite.”

“I

think it will be some time before we see the major banks’ credit

policies change. I think it’s going to increase the broker market share

and increase the non-bank market share,” he said.

Mr

Milburn agreed, stating: “I think non-bank share will continue to grow…

the near-prime market, whether that be residential or CRE, is going to

continue to grow out because the major banks aren’t moving their credit

policy in line with the changing world… The number of exceptions to that

major bank policy now are reducing. So near-prime, near near-prime or

super prime, those sections will continue to grow out because the majors

aren’t willing to see individuals as individuals.”

Mr

Milburn continued to suggest that several banks “do not have a

near-prime product, they do not have a specialist product and they are

not there for when customers go into times of hardship. We are. And

that’s the beauty of the non-bank space, we are there for Australians

who are undervalued and underserved by the major banks, and we will

continue to grow that out.”

Speaking

from an SME lender perspective, Mr Bauld added that non-banks would

also grow in this space as brokers continue to diversify into this

space.

Mr Bauld said: “We

have literally scratched the service of a $20-billion-plus market, so

there is massive room for continued growth, that’s why we absolutely

implore brokers to look at this space and think ‘OK, how do we get

involved?’ We will absolutely help them get involved…

“[So],

there is a massive opportunity for the intermediated market, but they

have to seize it. They really have to future-proof their business. And

if they do, there is a huge and massive opportunity ahead,” he said.

Anyone expecting an RBA rate cut to trigger a repeat of the six-year property boom we experienced from 2011 needs to think again, according to one of Australia’s leading forecasters; via InvestorDaily.

Speaking

to Investor Daily, AMP Capital chief economist Shane Oliver said he

believes Sydney is now about halfway through its correction, with

top-to-bottom house price falls to reach 25 per cent in the nation’s

biggest city.

“Melbourne prices have come down by around 10 per

cent. Like Sydney, I think they will come down by 25 per cent as well,

so they’re not quite halfway through the downturn,” he said. “There is a

wealth effect coming through from the price falls we have already seen

and a wealth effect still to come from further falls in house prices.”

The

property slowdown has also forced lenders like ING and Adelaide Bank to

reduce credit or small businesses borrowing against their residential

property.

ING has banned borrowers from using their homes as

security for business loans amid fears of negative equity as property

prices continue to fall.

A credit squeeze in the small business sector,

coupled with the “wealth effect” of falling property prices, which

curtails household consumption, could have serious implications for the

Australian economy.

RBA assistant governor Michele Bullock gave a

speech in Perth this week in which she stated that the wellbeing of

households and businesses in Australia depends on growth in the

Australian economy.

“And a crucial facilitator of sustained

growth is credit – flows of funds from people who are saving to people

who are investing.”

The Reserve Bank is banking on growth of 3 per

cent by the end of 2019. But AMP Capital’s Mr Oliver believes a

reduction in consumer spending and reduced construction activity related

to housing suggests growth could be closer to 2 per cent.

“If SMEs struggle to get credit, then it could be worse than that,” he said.

“I’m

probably in the more negative camp on the wealth effect and I think the

evidence is there. RBA governor Philip Lowe gave a speech two weeks ago

where he said that a 10 per cent decline in net housing wealth would

reduce consumer spending by 0.75 per cent in the short term and 1.5 per

cent in the longer term.

“A 10 per cent fall in net housing

wealth would be equivalent to a 7 per cent fall in actual house prices,

given a degree of gearing. Net housing wealth is about 75 per cent of

total housing wealth, so if you’ve got a 10 per cent fall in total

housing wealth, it implies a bigger impact of around 2 per cent in

consumer spending.”

Unemployment is a key indicator for measuring

the impact of these effects on the economy. Mr Oliver predicts the

unemployment rate will increase from 4.9 per cent to 5.5 per cent by the

end of the year.

Research released by the Reserve Bank of

Australia shows that the central bank’s decision to begin cutting rates

in November 2011, from 4.75 per cent to 1.5 per cent today, had a direct

influence on booming property prices.

The price of credit has

come down significantly over the last six years, given the 3.25 per cent

reduction in the official cash rate over that time.

House prices

peaked in mid-2017 and have declined by approximately 7 per cent

nationally since then. In Sydney, prices have come down by around 12 per

cent from their peak.

The next rate cut by the Reserve Bank,

which some believe could come as early as May, won’t have the same

impact as it did eight years ago, Mr Oliver said.

“It will

provide some help to stabilise the market. But I don’t think it’s going

to provide the same stimulus as it did in 2011. Household debt-to-income

levels are much higher now. The banks also have much tighter lending

standards than they did in 2011.

Information received since the Federal Open Market Committee met in

January indicates that the labor market remains strong but that growth

of economic activity has slowed from its solid rate in the fourth

quarter. Payroll employment was little changed in February, but job

gains have been solid, on average, in recent months, and the

unemployment rate has remained low. Recent indicators point to slower

growth of household spending and business fixed investment in the first

quarter. On a 12-month basis, overall inflation has declined, largely as

a result of lower energy prices; inflation for items other than food

and energy remains near 2 percent. On balance, market-based measures of

inflation compensation have remained low in recent months, and

survey-based measures of longer-term inflation expectations are little

changed.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. In support of these goals, the Committee decided to maintain the target range for the federal funds rate at 2-1/4 to 2-1/2 percent. The Committee continues to view sustained expansion of economic activity, strong labor market conditions, and inflation near the Committee’s symmetric 2 percent objective as the most likely outcomes. In light of global economic and financial developments and muted inflation pressures, the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate to support these outcomes.

In determining the timing and size of future adjustments to the

target range for the federal funds rate, the Committee will assess

realized and expected economic conditions relative to its maximum

employment objective and its symmetric 2 percent inflation objective.

This assessment will take into account a wide range of information,

including measures of labor market conditions, indicators of inflation

pressures and inflation expectations, and readings on financial and

international developments.

Troubled wealth giant AMP has admitted it faces a long hard road to recovery. With an increasingly vigilant regulator, conduct remains its greatest risk, via InvestorDaily.

In

its annual report, released on Wednesday (20 March), AMP’s new chief

executive officer, Francesco De Ferrari, told shareholders that 2019

will be a transitional year for the company as it completes the sale of

its wealth protection business and continues work on its hefty

remediation program.

AMP’s 2018 results included a provision of

$430 million (post-tax) for potential advice remediation, inclusive of

program costs, in relation to ASIC reports 499 and 515, which require an

industrywide ‘look back’ of advice provided from 1 July 2008 and 1

January 2009, respectively.

“Our first priority is the separation

of our wealth protection and mature businesses, which will help simplify

and create the basis for a more agile AMP,” Mr De Ferrari said.

“Our

second priority is the delivery of our advice remediation program to

compensate impacted clients. We are focused on doing this as quickly as

possible. Lastly, AMP is focused on getting our risk, governance and

control settings right. This includes placing ethics and risk at the

core of our culture.”

Following the sale of the wealth protection and

mature businesses, AMP will have four core operating businesses – wealth

management in Australia and New Zealand, AMP Bank and AMP Capital.

“Our

wealth management business in Australia has foundational assets and

strong market positions. However, the business model is challenged and

we need to reshape it for the future,” the CEO said. What shape the new

AMP wealth business takes remains to be seen.

“In New Zealand,

our wealth management business continues to deliver resilient earnings

for the group. Our opportunity is to become an advice-led wealth

management business,” Mr De Ferrari said.

AMP Capital has a

strong growth trajectory, particularly internationally. AMP Bank has

performed well and can be further leveraged as part of our wealth

management offer.

In its director’s report, AMP provided extensive

commentary on the key risks to the company, which has faced significant

challenges throughout 2018.

“Given the nature of our business

environment, we continue to face challenges that could have an adverse

impact on the delivery of our strategy,” the company said, adding that

the most significant business challenges include business, employee and

business partner conduct.

“The conduct of financial institutions

is an area of significant focus. There is a risk that business practices

and management, staff or business partner behaviours may not deliver

the outcomes desired by AMP or meet the expectations of regulators and

customers” the company said.

“An actual or perceived shortcoming

in conduct by AMP or its business partners may undermine our reputation

and draw increased attention from regulators. Our code of conduct

outlines AMP’s expectations in relation to minimum standards of

behaviour and decision-making, including how we treat our employees,

customers, business partners and shareholders.”

We often get questions about how to navigate the current choppy financial waters. DFA does not provide financial advice, but we do invite people with different views to share them with our community.

To that end, on Monday March 25th at 12pm AEDT (Sydney) I will discussing the current state of play with Harry Dent.

Note that we are not being paid to send this invite, nor for our time. This is not a sponsored promotion. It is being offered as a service to our community.

During this one-off LIVE broadcast, you will discover:

Harry Dent’s latest research and what it reveals about our economic future, and why it’s SHOCKING!

Harry Dent’s 2 major predictions that could begin to take place as early as the next few months

How to shield yourself from financially devastating stock market and real estate losses by preparing before the carnage begins, so you can feel safe knowing your future

How to profit from specific “decline-related” investments year after year, over the next several years, so you won’t just survive a market crash, you’ll prosper from it…

How to create a “legacy of wealth” by snapping up nearly every investment you can think of, at fire sale prices, allowing you to make more money by spending less…

How to set yourself up for the next long-term “boom cycle”