Last Thursday, the Basel Committee for Banking Supervision (BCBS) finalized its market risk capital framework, known as the Fundamental Review of the Trading Book. The final rule, which updates the Basel II and 2.5 approaches and takes effect January 2019 will increase the transparency and consistency of reporting risk-weighted assets (RWA) and capital metrics, which is a key goal of the BCBS agenda for 2016.

Under the new standards, banks’ reported market risk capital measures will be more comparable because of consistent risk factor identification, a more rigorous model approval process, and an enhanced standardized capital calculation serving as a capital floor to the internal models-approach calculation. The revised market risk capital framework enhances both the standardized and models-based approaches of calculating market risk exposure, recognizing that model variability is one of the key drivers of differing riskweighting and capital treatment for similar exposures across banks. Under the revised framework, internal models-approach banks will need to calculate market RWA under both methods, at trading desk level. Also, as the model validation process is reinforced under the framework, coverage of risks by the internal models approach could be narrowed – for example, they would be moved to the standardized approach.

These final rules will especially affect our rated universe of global investment banks (GIBs), which generally have significant trading operations, use internal models to calculate capital requirements, and have the largest share of market RWA as a percent of total RWA. We estimate that our rated GIBs’ market RWA account for about 10% of total RWA on average. It is unclear how the new market risk capital rules will specifically affect the capital requirements of the GIBs after the GIBs take mitigating actions, however, the BCBS estimated that in aggregate, banks would have a 40% higher market risk capital requirement on a weighted average basis and 22% higher on median basis under the new market risk standard versus the existing one. We expect that the finalization of these rules, which GIBs anticipated, will motivate them to further reduce and/or exit more capital-intensive trading activities. Although market risk has generally been smaller relative to credit and operational risk in bank capital requirements, the potential capital increase comes on top of other capital requirements that will start being phased in and will be material for some banks.

Key aspects of the internal models-approach include shifting the measure of stress loss risk or tail risk to an expected-shortfall measure from a value-at-risk measure to better capture the potential magnitude of tail losses, and including a stressed capital add-on for risk factors that cannot be modeled. The capital floor (capital charge under the internal-models approach relative to capital under the standardized approach) is set at 100%, meaning that banks have no incentive to move to the internal models-approach and suggesting that the BCBS believes that model-risk remains high despite the improvements in the new framework. The revised standardized approach uses an expanded factor sensitivities-based method, so that risks are evaluated more extensively and consistently across jurisdictions. Capital charges for risk factor sensitivities (i.e., delta, vega, and curvature risk) are applied to a broad group of risk classes, including interest rate risk, foreign-exchange risk and credit-spread risk.

Category: Economics and Banking

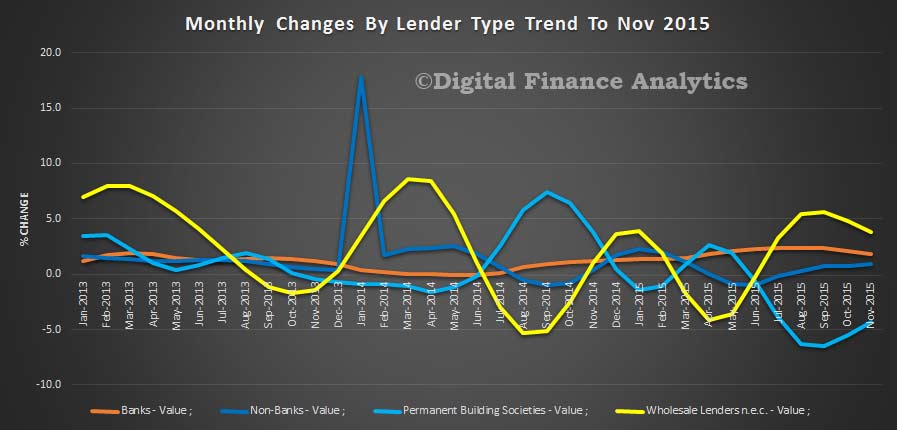

Strong Home Lending Continued In November

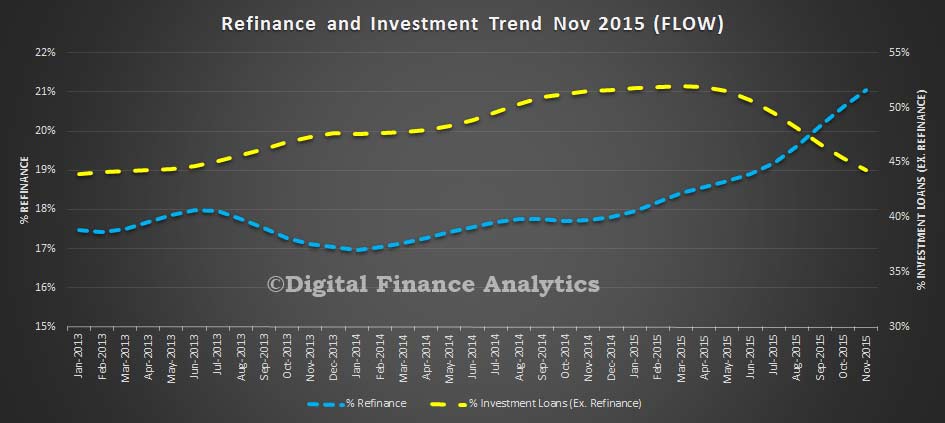

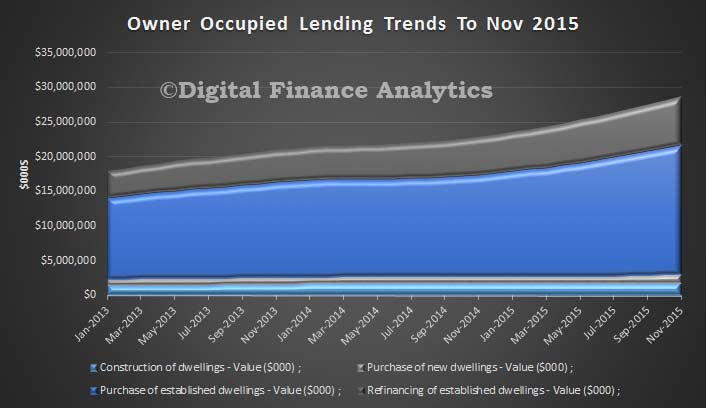

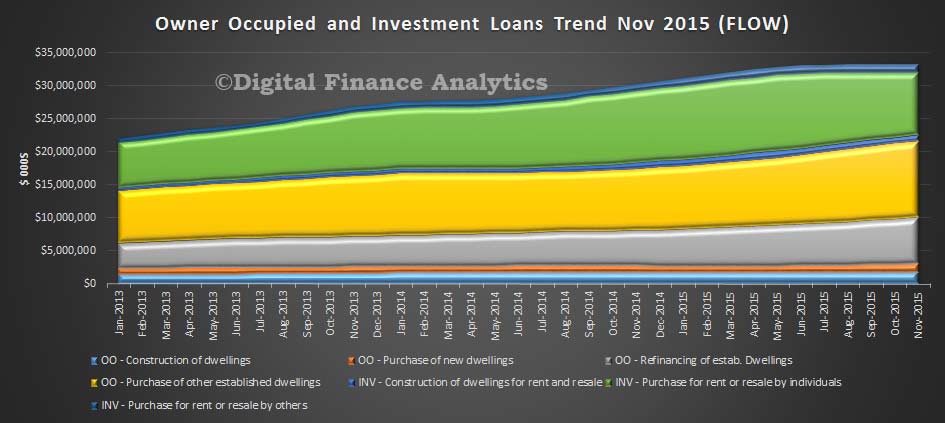

The latest ABS data, on home lending, released today, continues to confirms the strong growth which was reported in the stock data already released by APRA and RBA. The more granular flow data for November shows that owner occupied lending grew by 1.7% from October to $21.6 billion, whilst investment lending fell 2.9% to $11.6 billion. Refinancing accounted for more than 21% of all loans, whilst investment loans fell to 44.3% of new loans (still a big number, but below the 50% peak we saw in early 2015).

We note that by value, loans for construction rose 1.8% ($1.83 bn), whilst purchase of new dwellings lifted 1.6% ($1.24 bn) and purchase of existing dwellings rose 1.7% to $18.6 bn.

We note that by value, loans for construction rose 1.8% ($1.83 bn), whilst purchase of new dwellings lifted 1.6% ($1.24 bn) and purchase of existing dwellings rose 1.7% to $18.6 bn.

Refinanced loans rose 2.3% to $7.0 billion, and confirms the current focus of lenders trying to get existing borrowers to switch.

Refinanced loans rose 2.3% to $7.0 billion, and confirms the current focus of lenders trying to get existing borrowers to switch.

Looking at first time buyers, there was a 3.37% lift in the number of owner occupied borrowers (8,945) but there was a small fall in the relative proportion of borrowers, with first time buyers sitting at 14.9% (down 0.1%). Using data from our surveys, we overlay the first time buyers going direct to the investment sector, we see an additional 3,778 purchasers, down 1.3% from last month. Overall then, first time buyers are still active, despite high prices.

Looking at first time buyers, there was a 3.37% lift in the number of owner occupied borrowers (8,945) but there was a small fall in the relative proportion of borrowers, with first time buyers sitting at 14.9% (down 0.1%). Using data from our surveys, we overlay the first time buyers going direct to the investment sector, we see an additional 3,778 purchasers, down 1.3% from last month. Overall then, first time buyers are still active, despite high prices.

![]()

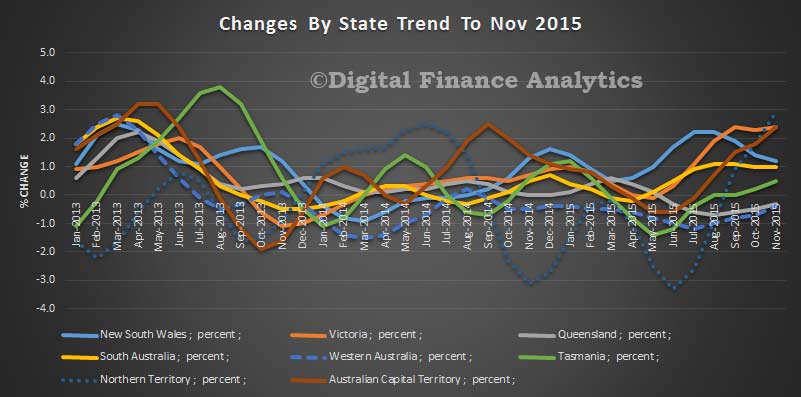

![]() Turning to the state changes, we see that momentum is slowing in NSW, thanks to falls in investment lending, but VIC is growing still, along with ACT and NT. Growth in QLD and WA is slower down 0.3% and 0.4% respectively. Looking specifically at new home lending to owner occupiers, most were higher with NSW up 9.7%, VIC 8.2%, QLD 2.3% and SA 6.3%. Significantly though new home lending to owner occupiers was lower in Western Australia down 15.9% and Tasmania down 10.7%.

Turning to the state changes, we see that momentum is slowing in NSW, thanks to falls in investment lending, but VIC is growing still, along with ACT and NT. Growth in QLD and WA is slower down 0.3% and 0.4% respectively. Looking specifically at new home lending to owner occupiers, most were higher with NSW up 9.7%, VIC 8.2%, QLD 2.3% and SA 6.3%. Significantly though new home lending to owner occupiers was lower in Western Australia down 15.9% and Tasmania down 10.7%.

Finally, it is worth noting that we have seen momentum in the wholesale lending sector (up 3.8%), and non-bank sectors (up 0.9%), whilst the banks have seen growth slowing slightly at around 1.8%. Building Societies appears to be performing less well, although there is a small improvement, with a fall of 4.3%.

Finally, it is worth noting that we have seen momentum in the wholesale lending sector (up 3.8%), and non-bank sectors (up 0.9%), whilst the banks have seen growth slowing slightly at around 1.8%. Building Societies appears to be performing less well, although there is a small improvement, with a fall of 4.3%.

Standing back, momentum across the sector continues, and given that demand for property remains strong (especially in the light of recent stock market volatility) we expect lending to continue to move higher – indeed we have seen a number of lenders reduce their rates for new owner occupied and lending business, in an attempt to gain share. The property story is far from over, despite some falls in prices.

Standing back, momentum across the sector continues, and given that demand for property remains strong (especially in the light of recent stock market volatility) we expect lending to continue to move higher – indeed we have seen a number of lenders reduce their rates for new owner occupied and lending business, in an attempt to gain share. The property story is far from over, despite some falls in prices.

AMP Bank reduces variable and fixed rate loans

AMP Bank has announced will reduce interest rates across a number of variable and fixed rate loans for new customers, effective Monday 18 January 2016.

The AMP Essential variable rate loan will be reduced by 30 basis points to 4.08 per cent

per annum (comparison rate 4.10 per cent per annum).

The Basic 3 year fixed rate will drop by 27 basis points to 4.28 per cent per annum (comparison rate 4.32 per cent per annum).

The variable rate on new investor property loans for the Basic loan will reduce by 40 basis points to 4.57 per cent per annum (comparison rate 4.61 per cent per annum).

The Basic 3 year fixed rate for new investor property loans is reducing by 45 basis points to 4.57 per cent per annum (comparison rate 4.61 per cent per annum).

Macroprudential, Capital and LVR Controls

A newly released IMF working paper examines the impact of macroprudential controls, including lifting capital ratios, and reducing allowable loan to value (LVR) ratios. They find that first, monetary policy and macroprudential policies related to bank capital are likely to be transmitted through the same channels in the banking system as they both affect the cost of loans. So, they should be expected to reinforce each other. Second, capital buffers or liquidity ratios targeting specific sectoral exposures are likely to be effective in slowing down credit growth in the mortgage market. Third, macro-prudential instruments affecting the cost of capital or the liquidity position could usefully be complemented by instruments related to non-price dimensions of mortgage loans such as limits on LTVs. The evidence also suggests that tightening of LTVs is more effective in slowing down credit growth and house price appreciation when monetary policy is too loose.

The design of a macro-prudential framework and its interaction with monetary policy has been at the forefront of the policy agenda since the global financial crisis. However, most advanced economies (AEs) have little experience using macroprudential policies, while there is, by contrast, more evidence about macro-prudential instruments aimed at moderating the volatility of capital flows in emerging markets. As a result, relatively little is known empirically about macroprudential instruments’ effectiveness in mitigating systemic risks in these countries, about their channels of transmission, and about how these instruments would interact with monetary policy.

Many countries publish bank lending surveys that provide very useful information on how banks modify the price and non-price terms of loans to the private sector, and on the drivers of these lending conditions. Some of the terms of loans (such as actual loan-to-value ratios (LTVs)) or some of the drivers of the lending standards (such as the cost of bank capital or the liquidity position of a bank) are directly related to macro-prudential instruments considered to be key in the policy toolkit of many jurisdictions. In this paper, we make use of the European Central Bank Lending Survey to develop a methodology and estimate empirically the likely effectiveness of some of these macro-prudential policies, their channel of transmissions and their interactions with monetary policy.

There is thus far little knowledge about how (policy driven) changes in the cost of bank capital (which could be the result of the implementation of a countercyclical capital buffer, of time contingent or sectoral risk weights, or more generally of bank specific changes in the capital adequacy ratio) or in the bank liquidity position would be transmitted to credit supply. Specifically, would such policy actions be transmitted through non-price factors (such as LTVs, collateral requirements, or maturity) or through price factors (such as price margins or fees)? There is also relatively little knowledge about whether limits on LTVs could significantly slow down house price appreciation and/or mortgage loan growth. Should measures affecting capitalization be complemented by non-price measures constraining lending standards? Can some of these macro-prudential policies be effective during housing booms when traditional monetary policy is typically too loose? Assessing such interactions and the transmission channel of macro-prudential instruments, with a specific focus on the real estate market, is important, as shocks to the real estate market have been a key source of systemic risk during the recent financial crisis.

The Euro-system Bank Lending Survey (BLS) contains information on overall changes in lending standards, or net tightening of lending standards and changes in lending standards related to non-price factors (LTVs, collateral requirements, maturity), price factors (such as margins) and factors contributing to the changes in lending standards, including balance sheet characteristics (such as capital and liquidity ratios) which can be mapped to specific macroprudential targets set by national regulators. However, identification of the impact of macro-prudential policies requires addressing specific challenges. The BLS does not require banks to specify the exact nature of the shocks that cause a change in lending standards or in the cost of capital, even though it provides information on perceptions of risks, economic activity, and competition pressures, and their contribution to the change. Hence, our approach is potentially subject to omitted variable bias, reverse causality and measurement bias (as expectations about house prices and credit growth may be mis-measured). Moreover, our observable variables (lending standard, and the contribution of balance sheet factors to lending standard) are not policy variables, which in our case are unobserved shocks affecting our observables. To address these issues, we develop methodologies relying upon instrumental variables and GMM estimators; our study also includes various control variables such as growth prospects, financial conditions, perception of risks and monetary policy cycle. Still, a potential advantage of our approach is that we would be able to capture the impact of the announcement of macro-prudential measures on lending standards, even before the actual implementation of the policy.

Our main findings are the following. First, our estimates suggest that measures that increase the cost of bank capital are effective in slowing down credit growth and house price appreciation. Second, changes in LTV also impact credit growth and house price appreciation but their impact tends to be more moderate. Third, macro-prudential policies affecting the cost of capital are transmitted mainly through price margins, with very little impact on LTV ratios or other non-price characteristics of mortgage loans. The evidence also suggests that tightening of LTVs is more effective in slowing down credit growth and house price appreciation when monetary policy is too loose.

Note: IMF Working Papers describe research in progress by the author(s) and are published to elicit comments and to encourage debate. The views expressed in IMF Working Papers are those of the author(s) and do not necessarily represent the views of the IMF, its Executive Board, or IMF management.

Is the January barometer providing an early warning for 2016 equity returns?

So far, it has not been a happy new year for equity market investors. The Australian equity market lost A$100 billion in market value in the first week of trading, mirroring a dire global trend.

If we are are to believe the “January barometer”, things may be about to get worse. The January barometer is based on the belief that when the equity market ends in the black for the month of January, the subsequent year will be prosperous for equity markets, while a negative equity market return in January signals a bearish year for stocks.

The barometer was first devised in 1972 by the editor of the Stock Trader’s Almanac, Yale Hirsch. Hirsch claimed that January returns could accurately predict subsequent equity market returns in 91.1% of years, with the rare failures of this indicator being explained by extreme events such as wars.

If the January barometer were as accurate as has been suggested then this indicator would provide a boon to investors who could use the signal to make asset allocation decisions for the subsequent year. Unfortunately financial markets are like discount airlines; there are no free lunches. Competitive market forces result in investors exploiting, and therefore eliminating, any opportunities to make risk-free abnormal profits.

The weight of academic evidence now shows that the evidence used to justify the January barometer was a statistical anomaly. The result does not appear to hold when a longer sample of years are analysed and there does not appear to be any evidence to support the January barometer outside of the US.

An examination of returns on the Australian equity market from 1974 to the present provides a further rebuttal to January barometer. The figure below provides annual average returns across the subsequent eleven months for years in which the return in January is positive and negative respectively.

As shown in this figure, the average equity market return in years following a negative January return (5.8%) is actually marginally higher than average returns in years following positive January returns (5.6%).

Recent history is also informative. In 2014 investors had a similarly unhappy start to the year, yet the market subsequently rebounded and ended the year in the black. Last year the market was up 3.2% in January, yet fell by 6.5% over the subsequent eleven months.

It is therefore clear that January returns are not a magic bullet that can be used to forecast stock market performance and make investment decisions. Financial markets are too sophisticated for individual monthly returns to be informative about the future. To borrow a quote from Mark Twain:

“October. This is one of the peculiarly dangerous months to speculate in stocks. The others are July, January, September, April, November, May, March, June, December, August, and February.”

Given the January barometer does not have merit as a forecasting tool, many investors will be anxious to know what lies ahead. Recent stock market declines can be attributed to structural problems across global economies. Chinese growth is continuing to weaken and global debt has increased significantly following a sustained period of low interest rates.

Ongoing global security threats were also identified as a potential limit to economic growth at the G20 summit last year. While predicting the direction of stock market returns across 2016 is fraught with danger, the current uncertainty across global markets appears to indicate that whatever the end result, investors are likely to be in for a volatile ride.

Author: , Senior Lecturer, Newcastle Business School, University of Newcastle.

Banks May Need More Capital to Cover Basel Step-In Risk

The Basel Committee on Banking Supervision’s proposals concerning step-in risk are most likely to have an impact on banks with large asset and wealth management, investment fund, and securitisation origination and sponsorship activities, says Fitch Ratings.

The Basel Committee launched a consultation on 17 December 2015 to assess whether banks should hold capital specifically to cover the risk that they may be required to step in and provide financial support to non-bank financial entities at a time of financial stress, even in the absence of clear contractual obligations to do so.

These additional capital requirements could prove onerous. This increases the likelihood that affected banks could lobby and resist the proposals.

Banks with discretion over the assets they manage in their wealth management units would incur a capital charge because they might encounter higher step-in risks. Under the proposals, a credit conversion factor, which could be as high as 100%, should be applied to the volume of discretionary assets under management. Large asset and wealth managers could potentially face high additional capital charges if the proposals are adopted, even if only a fraction of assets under management were classed as discretionary.

Fitch says this could reduce the attractiveness of asset and wealth management as a business line, especially if banks are unable to pass on additional capital costs by increasing fees. The Basel Committee also highlighted step-in risk arising from structured note special purpose vehicle platforms, such as the ones used by investment banks and wealth managers to create bespoke investment products for institutional and high net worth investors.

Step-in risk is not new. During the 2008 financial crisis, several banks supported entities which had been shifted off-balance sheet because they were heavily invested in the entities, were the entities’ sole source of liquidity or failure to provide support would lead to considerable reputation damage. Accounting consolidation standards were tightened and regulatory reforms, such as the Basel Committee’s Pillar 2 reputational and implicit support risk guidelines, have tried to tackle step-in risks. And on 14 December 2015, the European Banking Authority issued guidelines regarding limits on banks’ exposures to shadow banking entities.

But the Basel Committee is now proposing that banks should capture potential step-in risk using a quantitative approach either under Pillar 1 or 2 capital requirements. Regulatory drives to ensure banks hold sufficient capital in advance of a stress can be positive for ratings. But we think the proposed step-in capital charge could include an element of double counting.

The Basel Committee’s Liquidity Coverage Ratio already forces banks to determine the liquidity impact of non-contractual contingent funding obligations and asking banks to hold additional capital for step-in liquidity risks could prove too onerous. The proposed step-in risk capital charges could, however, add value when banks calculate their leverage ratios because step-in contingencies go beyond the off-balance sheet liabilities included in leverage calculations.

Fitch already considers potential step-in risks as part of its rating process. Highly opaque or complex organisational structures might be a negative ratings factor. Off-balance sheet risks are analysed when we assess a bank’s financial profile and reputational risks are closely reviewed, particularly when we assess a bank’s propensity to support subsidiaries and affiliates. Branding, entity sponsorship, liquidity provision and the ability to influence management, which the Basel Committee identifies as key potential step-in risk triggers, are factored into our bank ratings.

The Basel Committee’s consultation period on step-in risk closes in March 2016.

Should Banks Be Able To Create Money?

Banks today have the power to extend their reach by multiplying the value of loans against deposits and shareholder capital held. Indeed, all the recent regulatory work has been to try and lift the capital ratios, to protect the financial system and to try to ensure in event of failure, tax payers are be protected. We have highlighted how highly leveraged the main Australian Banks are. And this morning we discussed the risks associated with a credit boom.

Last year the Bank of England suggested that banks have the capacity to create UNLIMITED amounts of credit, in fact creating money, unrelated to deposits.

In this light, a working paper from the IMF in 2012 (note this is a research document, not the views of the IMF), “The Chicago Plan Revisited“, is worth reading.

The decade following the onset of the Great Depression was a time of great intellectual ferment in economics, as the leading thinkers of the time tried to understand the apparent failures of the existing economic system. This intellectual struggle extended to many domains, but arguably the most important was the field of monetary economics, given the key roles of private bank behavior and of central bank policies in triggering and prolonging the crisis.

During this time a large number of leading U.S. macroeconomists supported a fundamental proposal for monetary reform that later became known as the Chicago Plan, after its strongest proponent, professor Henry Simons of the University of Chicago. It was also supported, and brilliantly summarized, by Irving Fisher of Yale University, in Fisher (1936). The key feature of this plan was that it called for the separation of the monetary and credit functions of the banking system, first by requiring 100% backing of deposits by government-issued money, and second by ensuring that the financing of new bank credit can only take place through earnings that have been retained in the form of government-issued money, or through the borrowing of existing government-issued money from non-banks, but not through the creation of new deposits, ex nihilo, by banks.

Fisher (1936) claimed four major advantages for this plan. First, preventing banks from creating their own funds during credit booms, and then destroying these funds during subsequent contractions, would allow for a much better control of credit cycles, which were perceived to be the major source of business cycle fluctuations. Second, 100% reserve backing would completely eliminate bank runs. Third, allowing the government to issue money directly at zero interest, rather than borrowing that same money from banks at interest, would lead to a reduction in the interest burden on government finances and to a dramatic reduction of (net) government debt, given that irredeemable government-issued money represents equity in the commonwealth rather than debt. Fourth, given that money creation would no longer require the simultaneous creation of mostly private debts on bank balance sheets, the economy could see a dramatic reduction not only of government debt but also of private debt levels.

We take it as self-evident that if these claims can be verified, the Chicago Plan would indeed represent a highly desirable policy. Profound thinkers like Fisher, and many of his most illustrious peers, based their insights on historical experience and common sense, and were hardly deterred by the fact that they might not have had complete economic models that could formally derive the welfare gains of avoiding credit-driven boom-bust cycles, bank runs, and high debt levels. We do in fact believe that this made them better, not worse, thinkers about issues of the greatest importance for the common good. But we can say more than this. The recent empirical evidence of Reinhart and Rogoff (2009) documents the high costs of boom-bust credit cycles and bank runs throughout history. And the recent empirical evidence of Schularick and Taylor (2012) is supportive of Fisher’s view that high debt levels are a very important predictor of major crises. The latter finding is also consistent with the theoretical work of Kumhof and Rancière (2010), who show how very high debt levels, such as those observed just prior to the Great Depression and the Great Recession, can lead to a higher probability of financial and real crises.

But this is more than a theoretical discussion, because Switzerland will hold a referendum to decide whether to ban commercial banks from creating money, after more than 110,000 people signed a petition calling for the central bank to be given sole power to create money in the financial system. Its been led by the Swiss Sovereign Money movement – known as the Vollgeld initiative – and is designed to limit financial speculation by requiring private banks to hold 100% reserves against their deposits.

“Banks won’t be able to create money for themselves any more, they’ll only be able to lend money that they have from savers or other banks,” said the campaign group.

If successful, the sovereign money bill would give the Swiss National Bank a monopoly on physical and electronic money creation, “while the decision concerning how new money is introduced into the economy would reside with the government,” says Vollgeld.

In the aftermath of the 2008 financial crisis, Iceland commissioned a report “Monetary Reform – A better monetary system for Iceland” which was published in 2015, and suggests that money creation is too important to be left to bankers alone.

Consider the impact if banks had to back loans with deposits. Credit would be expensive, and hard to get. Depositors would be better rewarded, and eventually households would deleverage, whilst property prices normalised. It might just reverse the “financialisation” of society. If it happened, banks would be very different beasts.

Financialisation is a term sometimes used in discussions of the financial capitalism that has developed over the decades between 1980 and 2010, in which financial leverage tended to override capital (equity), and financial markets tended to dominate over the traditional industrial economy and agricultural economics.

Fed December Minutes Signal Further Rate Rises … Later

The minutes of the December 2015 Federal Open Market Committee have been published, and outlines the discussions which underpinned the decision to lift the US federal funds rate. Here is an extract:

Regarding the medium-term outlook, inflation was projected to increase gradually as energy prices and prices of non-energy imports stabilized and the labor market strengthened. Overall, taking into account economic developments and the outlook for economic activity and the labor market, the Committee was now reasonably confident in its expectation that inflation would rise, over the medium term, to its 2 percent objective. However, for some members, the risks attending their inflation forecasts remained considerable. Among those risks was the possibility that additional downward shocks to prices of oil and other commodities or a sustained rise in the exchange value of the dollar could delay or diminish the expected upturn in inflation. A couple also worried that a further strengthening of the labor market might not prove sufficient to offset the downward pressures from global disinflationary forces. And several expressed unease with indications that inflation expectations may have moved down slightly. In view of these risks and the shortfall of inflation from 2 percent, members expressed their intention to carefully monitor actual and expected progress toward the Committee’s inflation goal.

After assessing the outlook for economic activity, the labor market, and inflation and weighing the uncertainties associated with the outlook, members agreed to raise the target range for the federal funds rate to ¼ to ½ percent at this meeting. A number of members commented that it was appropriate to begin policy normalization in response to the substantial progress in the labor market toward achieving the Committee’s objective of maximum employment and their reasonable confidence that inflation would move to 2 percent over the medium term. Members agreed that the post meeting statement should report that the Committee’s decision reflected both the economic outlook and the time it takes for policy actions to affect future economic outcomes. If the Committee waited to begin removing accommodation until it was closer to achieving its dual-mandate objectives, it might need to tighten policy abruptly, which could risk disrupting economic activity. Members observed that after this initial increase in the federal funds rate, the stance of monetary policy would remain accommodative.

However, some members said that their decision to raise the target range was a close call, particularly given the uncertainty about inflation dynamics, and emphasized the need to monitor the progress of inflation closely.

Members also discussed their expectations for the size and timing of adjustments in the target range for the federal funds rate going forward. Based on their current forecasts for economic activity, the labor market, and inflation, as well as their expectation that the neutral shortterm real interest rate will rise slowly over the next few years, members expected economic conditions would evolve in a manner that would warrant only gradual increases in the federal funds rate. However, they also recognized that the appropriate path for the federal funds rate would depend on the economic outlook as informed by incoming data. Members stressed the potential need to accelerate or slow the pace of normalization as the economic outlook evolved. In the current situation, because of their significant concern about still-low readings on actual inflation and the uncertainty and risks present in the inflation outlook, they agreed to indicate that the Committee would carefully monitor actual and expected progress toward its inflation goal. In determining the size and timing of further adjustments to monetary policy, some members emphasized the importance of confirming that inflation would rise as projected and of maintaining the credibility of the Committee’s inflation objective. Based on their current economic outlook, they continued to anticipate that the federal funds rate was likely to remain, for some time, below levels that the

Committee expected to prevail in the longer run.The Committee also maintained its policy of reinvesting principal payments from agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction. In view of members’ outlook for moderate growth in economic activity, inflation moving toward its target only gradually, and the asymmetric risks posed by the continued proximity of short-term interest rates to their effective lower bound, the Committee anticipated retaining this policy until normalization of the level of the federal funds rate was well under way. This policy, by keeping the Committee’s holdings of longer term securities at sizable levels, should help maintain accommodative

financial conditions.

APRA Proposes to Report ADIs Liquidity Data

The Australian Prudential Regulation Authority (APRA) today released a consultation package on the proposed publication of liquidity statistics for authorised deposit-taking institutions (ADIs).

APRA proposes to expand the current statistics published in the Quarterly Authorised Deposit-taking Institutions (ADI) Performance publication to include relevant information on the liquidity of ADIs. APRA proposes to introduce liquidity statistics for banks, and expand the existing liquidity statistics published for credit unions and building societies.

APRA invites submissions on the proposal by 30 March 2016. The consultation package can be found on the APRA website at: www.apra.gov.au/adi/PrudentialFramework/Pages/Consultation-on-the-publication-of-ADI-liquidity-statistics.aspx

Of most interest, and welcome, is the Liquidity Coverage Ratio (LCR).

APRA does not currently publish any statistics on LCR ADIs in QADIP. Under the LCR requirements that came into effect on 1 January 2015, LCR ADIs are required to maintain a sufficient level of unencumbered high quality liquid assets (HQLA) to meet their liquidity needs for a 30 calendar day period under a severe stress scenario. Absent a situation of financial stress for locally-incorporated LCR ADIs, the value of the LCR must not be less than 100 per cent5.

The LCR is calculated as the percentage ratio: Stock of high-quality liquid assets / Total net cash outflows over the next 30 calendar days

APRA proposes to publish aggregate LCR statistics each quarter in QADIP. The statistics would include the components of the LCR: HQLA and other qualifying LCR liquid assets. Expected cash outflows and cash inflows under the LCR stress scenario would also be published.

APRA also proposes to publish statistics at the ADI segment-level for: banks (as well as major banks, other domestic banks and foreign subsidiary banks sub-segments). There are currently no credit unions or building societies subject to the LCR regime, but should this change APRA would include LCR statistics for these segments subject to meeting confidentiality obligations.

APRA proposes to publish statistics on a Level 2 consolidation basis from December 2014 reference period onwards, commencing in the March 2016 edition of QADIP. APRA does not propose to publish statistics for the 30 June 2014 and 30 September 2014 quarters, as the underlying data were submitted on a ‘best endeavours’ basis.

Major banks reduce maximum loan amounts

In the September 2015 edition of the Property Imperative, DFA highlighted the impact of reductions in loan values being offered, as lenders tightened their lending criteria and affordability guidelines. This trend has been confirmed in more recent media reports, and will potentially make it difficult for some refinancing borrowers to get the loans they need, and further dampen property demand and prices. It will also make the on-ramp for first time buyers even steeper.

According to Australian Broker,

“Major banks have significantly reduced the amount they are prepared to lend home buyers, a new analysis by leading brokerage Home Loan Experts has revealed.

A couple with a combined income of $120,000 purchasing an investment property can now borrow up to $80,000 less from a major bank than they could a year ago, according to the calculations published in a report by the Sydney Morning Herald.

Investment property buyers aren’t the only ones affected either. The maximum loan size for the same hypothetical couple buying an owner-occupied home has fallen by up to $65,000, according to the Sydney-based brokerage’s calculations.

According to the Sydney Morning Herald report, the calculations were based on the borrowing power or maximum loan amount for a couple earning $60,000 each, with two children. The comparison compared December 2014 with December 2015 and included Commonwealth Bank, National Australia Bank and Westpac. The broker was not able to access comparative figures for ANZ from 2014.

Commonwealth Bank, for example, would have lent $640,000 as a housing investment loan a year ago, compared with $560,000 now — an $80,000 reduction.

Westpac would have lent the couple buying an owner-occupied home $645,000 a year ago, but this amount has fallen to $580,000 — a $65,000 reduction.

Home Loan Experts mortgage broker Christina Parnham told the Sydney Morning Herald that the maximum loan amount has been reduced because banks are requiring borrowers be tested against how they would cope with higher interest rates.

“You’re going to have to be able to service the loan at about 7.5 to 8%,” she said.

At the same time, Farnham says banks have adopted more conservative assumptions about living expenses”