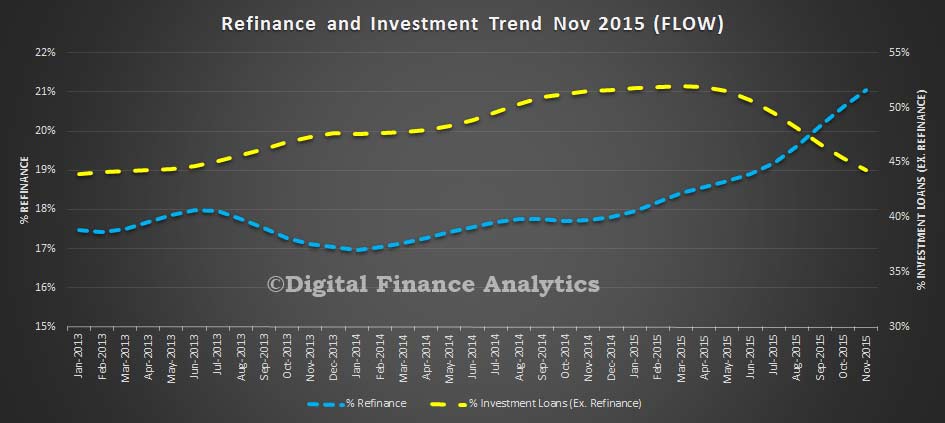

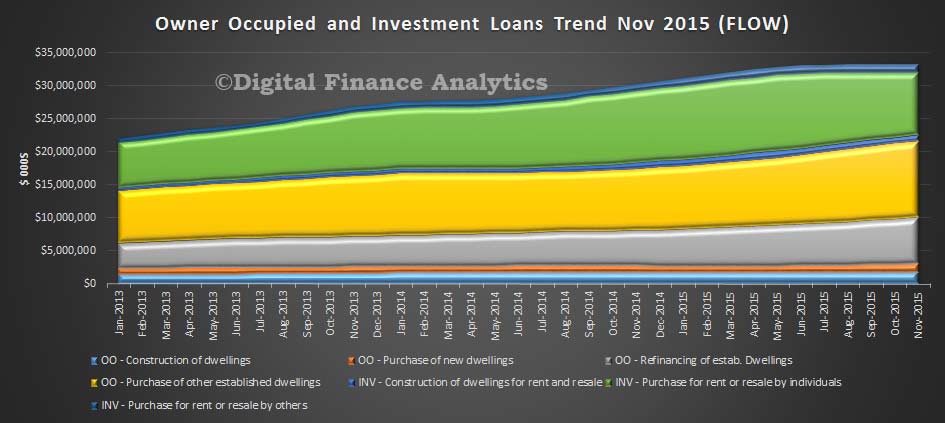

The latest ABS data, on home lending, released today, continues to confirms the strong growth which was reported in the stock data already released by APRA and RBA. The more granular flow data for November shows that owner occupied lending grew by 1.7% from October to $21.6 billion, whilst investment lending fell 2.9% to $11.6 billion. Refinancing accounted for more than 21% of all loans, whilst investment loans fell to 44.3% of new loans (still a big number, but below the 50% peak we saw in early 2015).

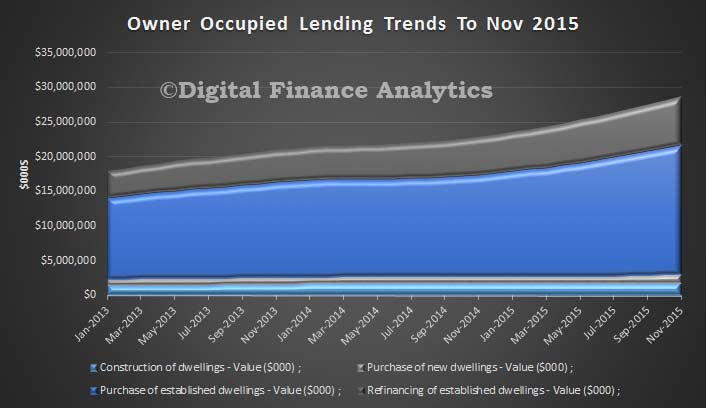

We note that by value, loans for construction rose 1.8% ($1.83 bn), whilst purchase of new dwellings lifted 1.6% ($1.24 bn) and purchase of existing dwellings rose 1.7% to $18.6 bn.

We note that by value, loans for construction rose 1.8% ($1.83 bn), whilst purchase of new dwellings lifted 1.6% ($1.24 bn) and purchase of existing dwellings rose 1.7% to $18.6 bn.

Refinanced loans rose 2.3% to $7.0 billion, and confirms the current focus of lenders trying to get existing borrowers to switch.

Refinanced loans rose 2.3% to $7.0 billion, and confirms the current focus of lenders trying to get existing borrowers to switch.

Looking at first time buyers, there was a 3.37% lift in the number of owner occupied borrowers (8,945) but there was a small fall in the relative proportion of borrowers, with first time buyers sitting at 14.9% (down 0.1%). Using data from our surveys, we overlay the first time buyers going direct to the investment sector, we see an additional 3,778 purchasers, down 1.3% from last month. Overall then, first time buyers are still active, despite high prices.

Looking at first time buyers, there was a 3.37% lift in the number of owner occupied borrowers (8,945) but there was a small fall in the relative proportion of borrowers, with first time buyers sitting at 14.9% (down 0.1%). Using data from our surveys, we overlay the first time buyers going direct to the investment sector, we see an additional 3,778 purchasers, down 1.3% from last month. Overall then, first time buyers are still active, despite high prices.

![]()

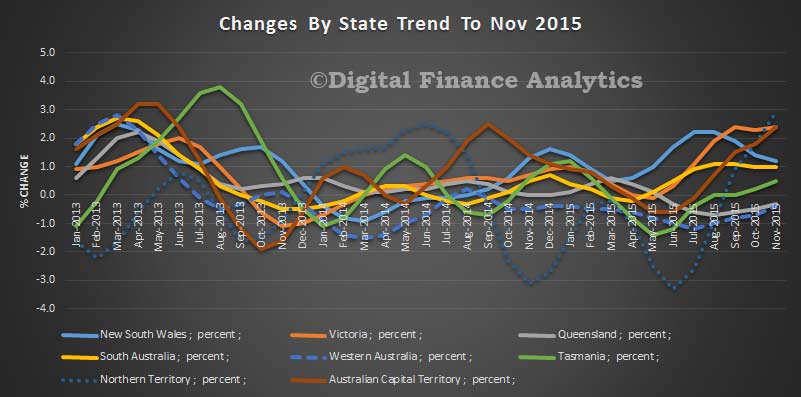

![]() Turning to the state changes, we see that momentum is slowing in NSW, thanks to falls in investment lending, but VIC is growing still, along with ACT and NT. Growth in QLD and WA is slower down 0.3% and 0.4% respectively. Looking specifically at new home lending to owner occupiers, most were higher with NSW up 9.7%, VIC 8.2%, QLD 2.3% and SA 6.3%. Significantly though new home lending to owner occupiers was lower in Western Australia down 15.9% and Tasmania down 10.7%.

Turning to the state changes, we see that momentum is slowing in NSW, thanks to falls in investment lending, but VIC is growing still, along with ACT and NT. Growth in QLD and WA is slower down 0.3% and 0.4% respectively. Looking specifically at new home lending to owner occupiers, most were higher with NSW up 9.7%, VIC 8.2%, QLD 2.3% and SA 6.3%. Significantly though new home lending to owner occupiers was lower in Western Australia down 15.9% and Tasmania down 10.7%.

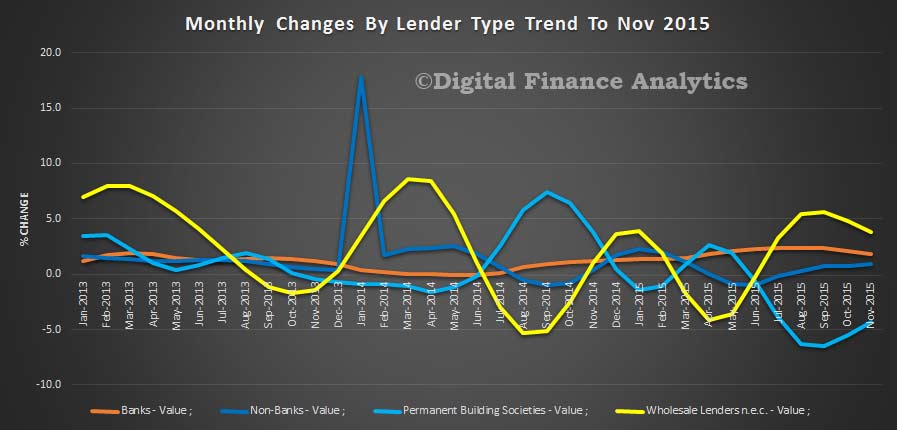

Finally, it is worth noting that we have seen momentum in the wholesale lending sector (up 3.8%), and non-bank sectors (up 0.9%), whilst the banks have seen growth slowing slightly at around 1.8%. Building Societies appears to be performing less well, although there is a small improvement, with a fall of 4.3%.

Finally, it is worth noting that we have seen momentum in the wholesale lending sector (up 3.8%), and non-bank sectors (up 0.9%), whilst the banks have seen growth slowing slightly at around 1.8%. Building Societies appears to be performing less well, although there is a small improvement, with a fall of 4.3%.

Standing back, momentum across the sector continues, and given that demand for property remains strong (especially in the light of recent stock market volatility) we expect lending to continue to move higher – indeed we have seen a number of lenders reduce their rates for new owner occupied and lending business, in an attempt to gain share. The property story is far from over, despite some falls in prices.

Standing back, momentum across the sector continues, and given that demand for property remains strong (especially in the light of recent stock market volatility) we expect lending to continue to move higher – indeed we have seen a number of lenders reduce their rates for new owner occupied and lending business, in an attempt to gain share. The property story is far from over, despite some falls in prices.