The Treasurer has announced a second stimulus plan as Australia fights to contain the economic impact of the coronavirus.

Hours

after the emergency rate cut by the Reserve Bank, the Prime Minister

and Treasurer addressed Australia announcing a further $15 billion

investment to enable smaller lenders to continue supporting Australian

consumers and small businesses.

This

funding will complement the Reserve Bank of Australia’s (RBA’s)

announcement of a $90 billion term funding facility for authorised

deposit-taking institutions (ADIs) that is also expected to support

lending to small and medium enterprises.

The

government’s latest action is aimed to enable customers of smaller

lenders to continue to access affordable credit as the world deals with

the significant challenges presented by the spread of coronavirus.

“Small

lenders are critical to Australia’s lending markets, often driving

innovation and providing competition for larger lenders,” said the

Treasurer Josh Frydenberg.

“Combined,

these measures will support the continued ability of lenders to support

their customers and in doing so the Australian economy,” the Treasurer

added.

The Treasurer confirmed that

the Australian Office of Financial Management (AOFM) will be provided

with an investment capacity of $15 billion to invest in wholesale

funding markets used by small ADIs and non-ADI lenders.

The

$15 billion capacity would allow the AOFM to support a substantial

volume of expected issuance by these lenders over a 12 month period.

“Importantly the assets being purchased by the AOFM will not be limited to residential mortgage backed securities.

“The

AOFM will also be able to invest in a range of other asset backed

securities and warehouse facilities. The Government will provide the

AOFM with investment guidelines that will outline the basis on which the

AOFM is to undertake these investments,” the Treasurer added.

Enabling

legislation will be introduced in the week commencing Monday, 23 March

2020. The AOFM is expected to be able to begin investing by April.

RBA said: The coronavirus is first and foremost a public health issue, but it is also having a very major impact on the economy and the financial system. As the virus has spread, countries have restricted the movement of people across borders and have implemented social distancing measures, including restricting movements within countries and within cities. The result has been major disruptions to economic activity across the world. This is likely to remain the case for some time yet as efforts continue to contain the virus.

Financial market volatility has been very high. Equity prices have experienced large declines.

Government bond yields have declined to historic lows. However, the functioning of major government bond

markets has been impaired, which has disrupted other markets given their important role as a financial

benchmark. Funding markets are open to only the highest quality borrowers.

The primary response to the virus is to manage the health of the population, but other arms of policy,

including monetary and fiscal policy, play an important role in reducing the economic and financial

disruption resulting from the virus.

At some point, the virus will be contained and the Australian economy will recover. In the interim, a

priority for the Reserve Bank is to support jobs, incomes and businesses, so that when the health crisis

recedes, the country is well placed to recover strongly.

At a meeting yesterday, the Reserve Bank Board agreed to the following comprehensive package to support

the Australian economy through this challenging period:

A reduction in the cash rate target to 0.25 per cent.

The Board will not increase the cash rate target until progress is being made towards full employment

and it is confident that inflation will be sustainably within the 2–3 per cent target

band.

A target for the yield on 3-year Australian Government bonds of around 0.25 per cent.

This will be achieved through purchases of Government bonds in the secondary market. Purchases of

Government bonds and semi-government securities across the yield curve will be conducted to help

achieve this target as well as to address market dislocations. These purchases will commence tomorrow.

The Bank will work closely with the Australian Office of Financial Management (AOFM) and state

government borrowing authorities to ensure the efficacy of its actions. Further details about the

implementation of this are provided in the accompanying notice.

A term funding facility for the banking system, with particular support for credit to small and

medium-sized businesses.

The Reserve Bank will provide a three-year funding facility to authorised deposit-taking institutions

(ADIs) at a fixed rate of 0.25 per cent. ADIs will be able to obtain initial funding of up to

3 per cent of their existing outstanding credit. They will have access to additional funding

if they increase lending to business, especially to small and medium-sized businesses. This facility is

for at least $90 billion. Further details are available in the accompanying notice.

The Australian Government has also developed a complementary program of support for the non-bank

financial sector, small lenders and the securitisation market, which will be implemented by the

AOFM.

Exchange settlement balances at the Reserve Bank will be remunerated at 10 basis points, rather

than zero as would have been the case under the previous arrangements.

This will mitigate the cost to the banking system associated with the large increase in banks’

settlement balances at the Reserve Bank that will occur following these policy actions.

The Reserve Bank will also continue to provide liquidity to Australian financial markets by

conducting one-month and three-month repo operations in its daily market operations until further

notice. In addition, the Bank will conduct longer-term repo operations of six-month maturity or longer

at least weekly, as long as market conditions warrant.

The various elements of this package reinforce one another and will help to lower funding costs

across the economy and support the provision of credit, especially to small and medium-sized

businesses.

Australia’s financial system is resilient and well placed to deal with the effects of the

coronavirus. The banking system is well capitalised and is in a strong liquidity position. Substantial

financial buffers are available to be drawn down if required to support the economy. The Reserve Bank is

working closely with the other financial regulators and the Australian Government to help ensure that

Australia’s financial markets continue to operate effectively and that credit is available to

households and businesses.

Today’s policy package from the Reserve Bank complements the welcome fiscal response from

governments in Australia. Together, these measures will support jobs, incomes and businesses through

this difficult period and they will also assist the Australian economy in the recovery.

Growth through 2020 is now estimated at 1.5% with minus 1% in the first half ( minus 0.7% and minus 0.3% respectively in the March and June quarters) and 2.5% in the second half. This is recession territory.

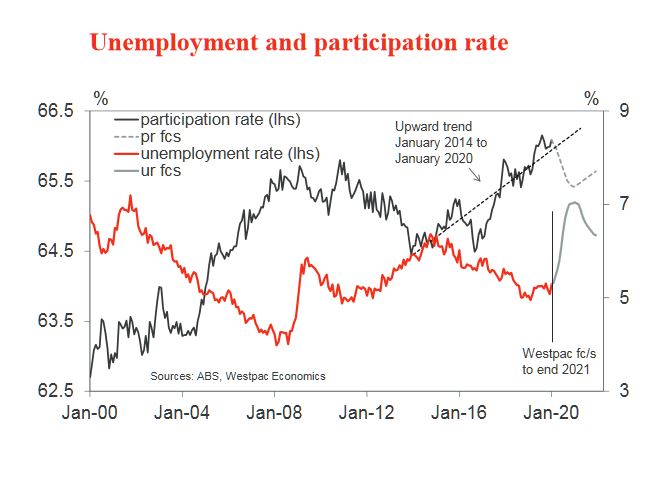

Just last week they had set the forecast peak in the unemployment rate at around 5.8%- 6%, up from the current level of 5.3%.

But now the unemployment rate is now forecast to reach 7% by October 2020 (up from the previous estimate of 5.8%-6.0%) due to the larger negative shocks to the labour intensive sectors such as recreation; tourism; education; renovations and additions; and dwelling construction. This lift in the unemployment rate is despite reducing the participation rate from 66.1% to 65.4% as a discouraged worker effect – that is, as workers respond to a deteriorating labour market the participation rate is likely to decline.

They add: please note that these forecasts are not based on Australia following a European style full lock down. Not surprisingly, the forecasts are subject to downward revision in the event of such an occurrence.

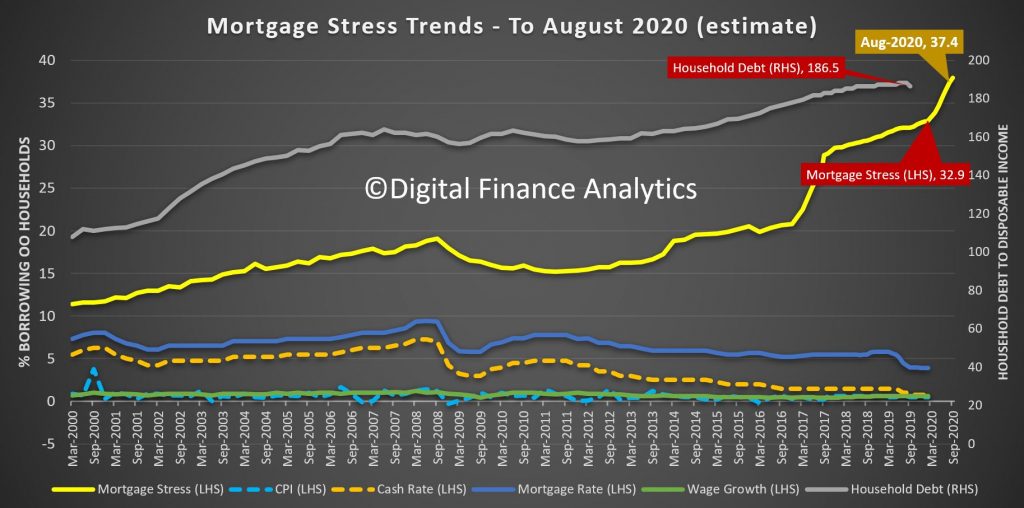

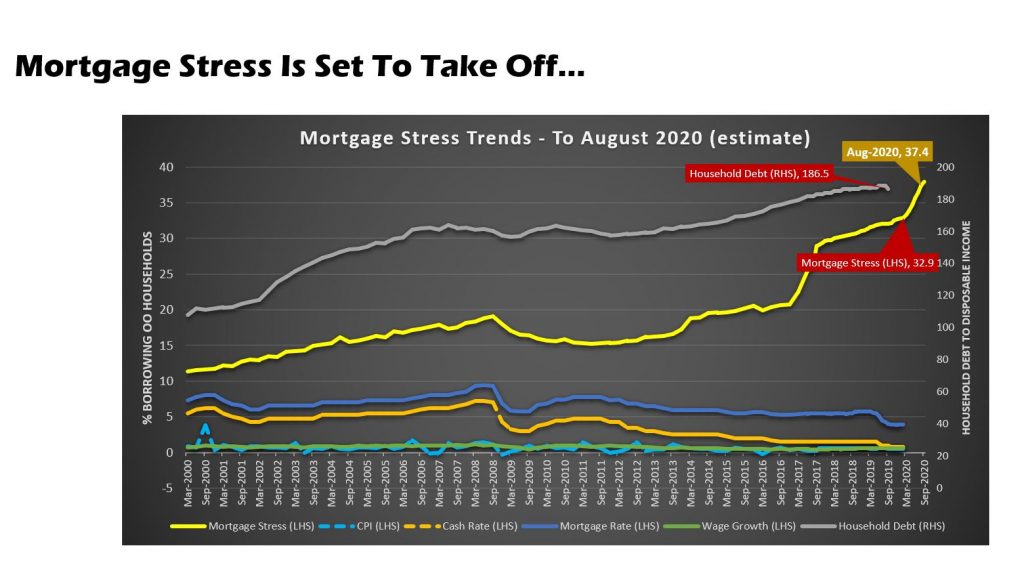

This is consistent with our modelling – mortgage stress will rise in the months ahead as unemployment rises.

Now the question becomes, to what extent with the banks forego mortgage repayments, and not foreclose, and to what extent will the Government supports households directly? The mortgage debt mountain could bite deep and early.

Its also worth noting that we are already seeing a rise in financial stress among those renting – here the protections currently are very limited, and will need to be increased.

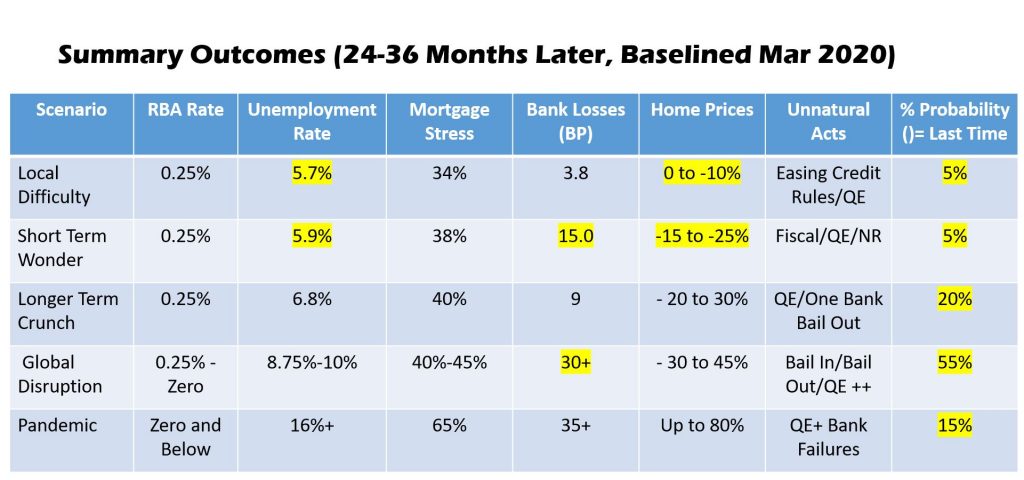

Our own modelling is based on the assumption the crisis will run for at least 6 months. Overnight a UK report suggested 18 months is more likely, given the lead time to a vaccine.

We have updated our scenarios, driven from our core market models.

The drivers are rising unemployment, and business failure thanks to the impact of the virus. We discussed these scenarios in our live stream event last night. This is the full version with live chat. The show starts formally at 32 minutes.

We estimate that mortgage stress is set to rise significantly in the months ahead as household cash-flows are interrupted.

Alternatively we have also released a shorter edited version, without chat here:

Welcome to our latest post covering finance and property news with a distinctively Australian flavour. Given the current market gyrations, we are going to examine the latest critical data each day, because a week is a long time in politics but a lifetime on the markets at the moment…