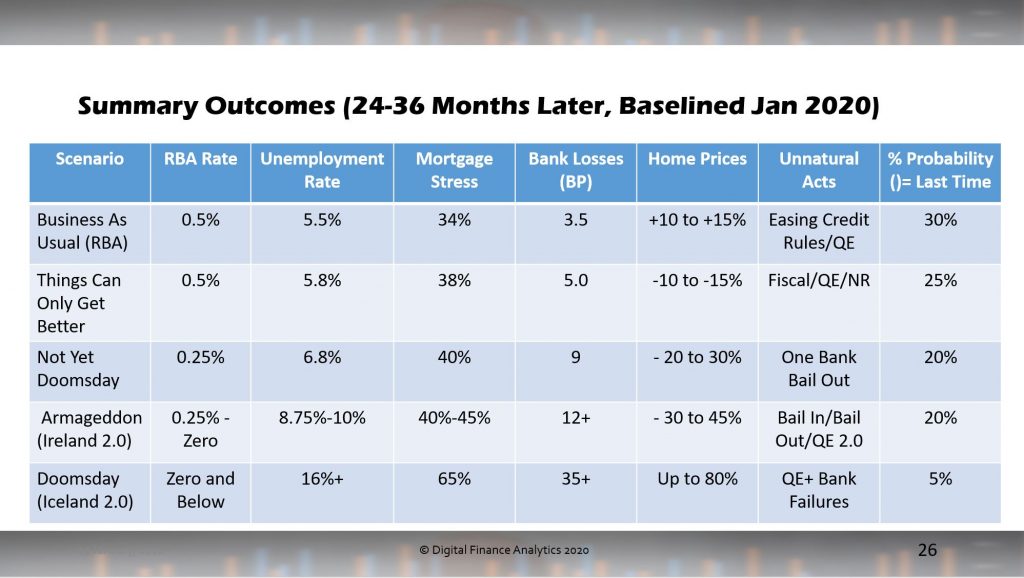

Here is the edited version of our live stream event for January. In the show we update our property and finance scenarios, and answer a range of questions from viewers. We ran out of time, so I plan to make a future show covering those I missed. Here are our current scenarios:

The original live recording, with the embedded live chat is also available. You will need to watch on YouTube to follow the interactions:

Our next live show will be at 20:00 Tuesday 18th February.

When the world’s

largest fund manager tells its clients that it plans to swiftly exit its

thermal coal investments over the next six months, this should tell us

something important.

BlackRock

manages around USD$7 trillion of funds on behalf of investors and up to now has

been cautious in its response to climate change and slow to participate in

investor campaigns. But that just

changed, for good economic reasons. Recent analysis published by the Institute

for Energy Economics and Financial Analysis (IEEFA), estimated that BlackRock

lost as much as USD$90 billion in investment value due to poor investments in

fossil fuel companies in 2019. The IEEFA

assessment also found that investments in just four fossil fuel companies,

ExxonMobil, Chevron, Royal Dutch Shell and BP accounted for around

three-quarters of the USD$90 billion loss.

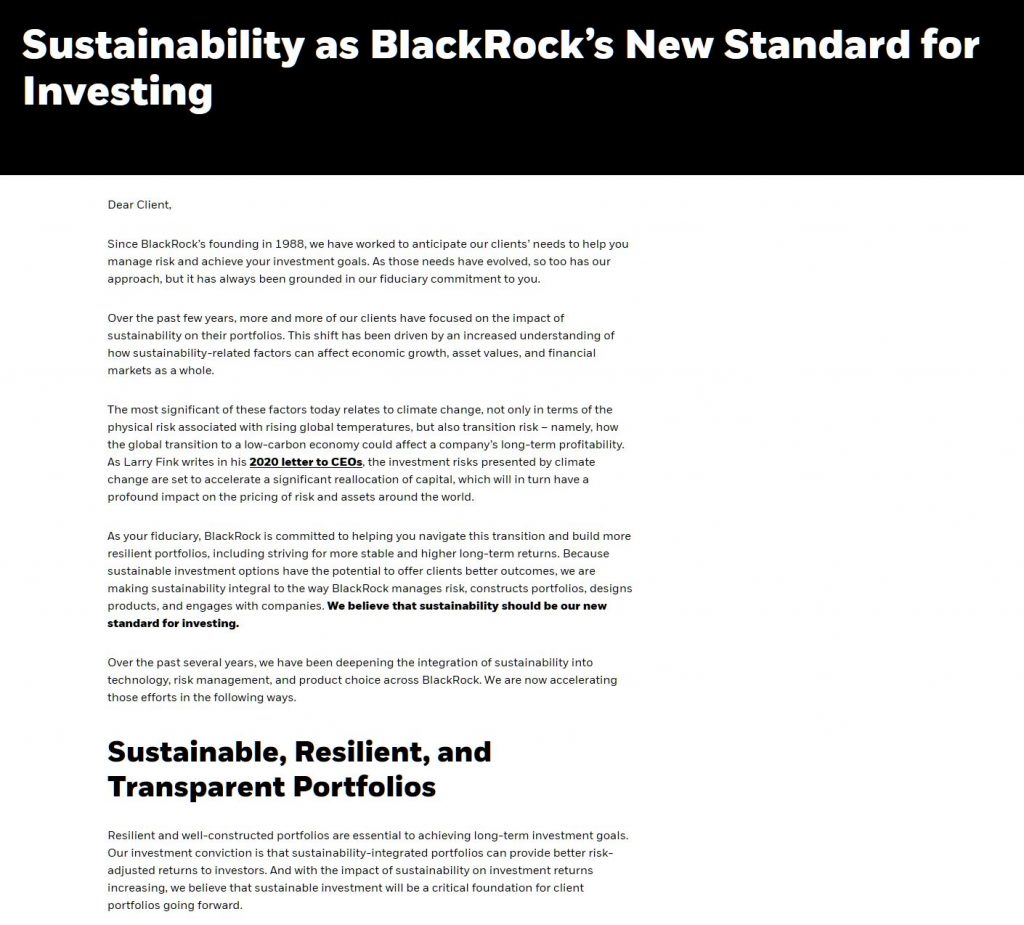

Now, in a

letter to clients, BlackRock’s Global Executive Committee, led by company

founder and CEO Laurence Fink, explained that the company would be withdrawing

its investments in thermal coal producers, including any company that sources

more than a quarter of its revenue from thermal coal production.

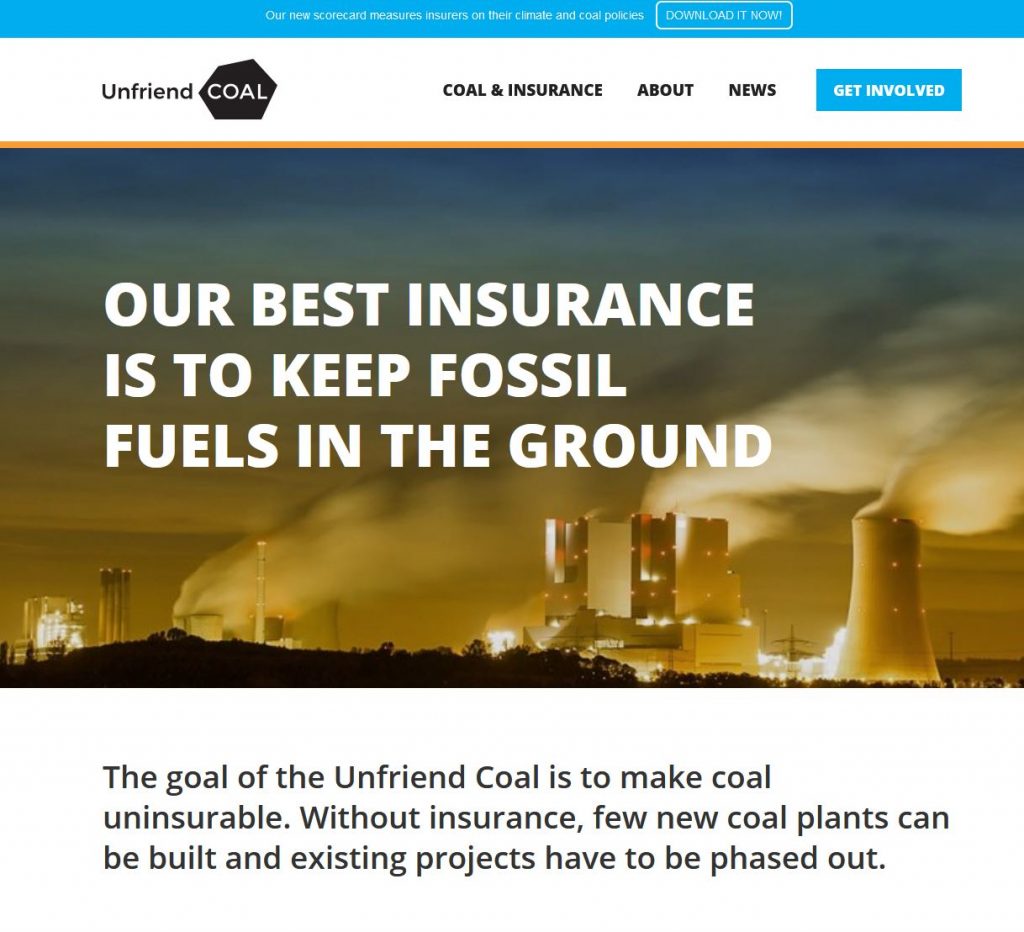

Announcements

of this kind have come out steadily over the past couple of years. Virtually

all the major Australian and European banks and insurers, and many other global

institutions, have already announced such policies. According to the Unfriend

Coal Campaign, insurance companies have stopped covering roughly US$8.9

trillion of coal investments – more than one-third (37%) of the coal industry’s

global assets, and stopped offering reinsurance to 46% of them.

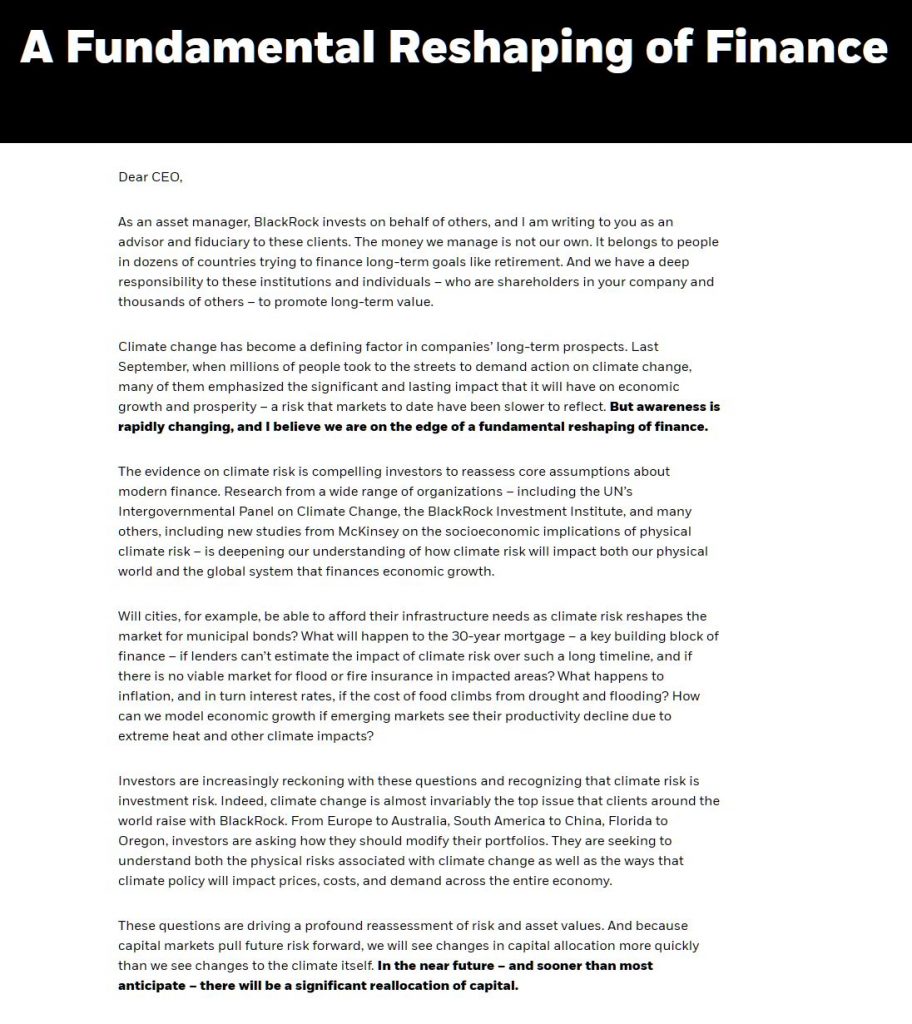

A

separate letter to CEO’s starts with a clear reference to BlackRock’s

‘fiduciary duty’ to its investors. BlackRock’s own analysis shows global

financial markets will be materially impacted by climate change, reflected in

the Bank of England’s analysis of $20 trillion at risk. “BlackRock concludes

that this stranded asset risk is not yet priced into the market, so as a

fiduciary, BlackRock really has no choice but to act.”

“Thermal

coal is significantly carbon intensive, becoming less and less economically

viable, and highly exposed to regulation because of its environmental impacts.

With the acceleration of the global energy transition, we do not believe that

the long-term economic or investment rationale justifies continued investment

in this sector,” the letter says.

“As a

result, we are in the process of removing from our discretionary active

investment portfolios the public securities (both debt and equity) of companies

that generate more than 25% of their revenues from thermal coal production,

which we aim to accomplish by the middle of 2020.

Environmental,

Social, and Governance (ESG) Criteria are coming to the fore – Environmental –

a set of standards for a company’s operations that consider how a company

performs as a steward of nature. Social – examines how a company manages

relationships with employees, suppliers, customers, and the communities where

it operates. Governance – how its deals with a company’s leadership, executive

pay, audits, internal controls, and shareholder rights.

“As part

of our process of evaluating sectors with high ESG risk, we will also closely

scrutinize other businesses that are heavily reliant on thermal coal as an

input, in order to understand whether they are effectively transitioning away

from this reliance.”

The move

will see the investment giant dump around USD$500 million (A$725 million) in

thermal coal investments.

And firms

should note that Blackrock is going to flex its influence. “Given the groundwork we have already laid

engaging on disclosure, and the growing investment risks surrounding

sustainability, we will be increasingly disposed to vote against management and

board directors when companies are not making sufficient progress on

sustainability-related disclosures and the business practices and plans

underlying them,” Fink said.

So,

Blackrock’s Fink seems to have figured out the huge impact that climate change

will have on not just money, but the world.

“Will

cities, for example, be able to afford their infrastructure needs as climate

risk reshapes the market for municipal bonds?” Mr Fink wrote in his letter to

CEOs.

“What

will happen to the 30-year mortgage – a key building block of finance – if

lenders can’t estimate the impact of climate risk over such a long timeline,

and if there is no viable market for flood or fire insurance in impacted areas?

What happens to inflation, and in turn interest rates, if the cost of food

climbs from drought and flooding? How can we model economic growth if emerging

markets see their productivity decline due to extreme heat and other climate impacts?”

he said.

BlackRock

also announced that it would join the Climate Action 100+ initiative, that

supports investors to actively engage with the companies they are invested in

to assess, disclose and address the risk that climate change and the energy transition

poses to the company and the value of investments. The Climate Action 100+

initiative includes the Australian based Investor Group on Climate Change,

which supports Australian institutional

In 2019,

the UK-based think tank InfluenceMap released a report that showed

BlackRock was the leader of the asset management pack in terms of fossil fuel

ownership. As at June 2018, the oil, gas and thermal coal reserves controlled

by fossil fuel producers it holds represented an aggregated 9.5 gigatonnes of

carbon dioxide emissions equivalent, with just under half of these emissions in

thermal coal and equivalent to 30 per cent of total global energy-related

carbon emissions in 2017.

“Among

the 10 asset management groups with the largest aggregate fund AUM,

BlackRock holds the most coal-intensive portfolios,” the report said. A -100%

indicates full divestment while positive values indicates adding coal to the

portfolio during the period 2011-2016.

“However,

there are key differences between BlackRock’s passively and actively managed

funds,” the report noted. “The group’s passively managed funds show a thermal

coal intensity in 2018 of 680 t/US$m AUM, while its actively managed funds show

a much lower TCI of about 300 tons/$m AUM, well below the global fund

benchmark.”

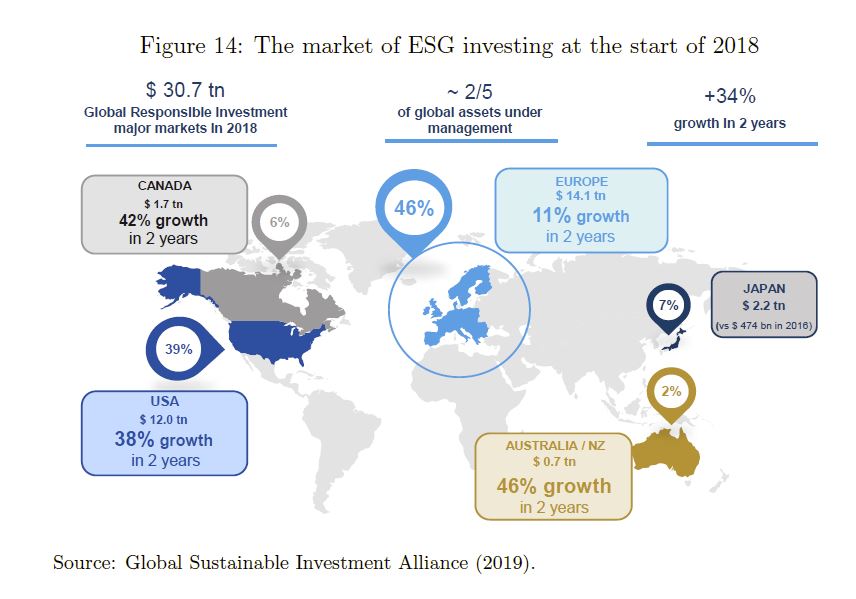

And significantly

ESG investment strategies are growing in profitability, with new geographic

trends adding to their value, according to Amundi Asset Management who analysed

the performance of 1,700 companies across five investment universes. Their

research – ESG investing in recent years: New insights from old challenges

– found that ESG strategies tended to penalise ESG investors between 2010 and

2013, but rewarded investors after 2014. “We have observed a massive

mobilisation of institutional investors on ESG,” they said. The global responsible investment is

estimated to be $30.7 trillion USD, or two fifths of assets under management.

This is a 34% growth in two years.

But here

is the problem. Most of the money that BlackRock manages is wrapped up in

passive investments, which track indexes. Indexes tend to contain the shares of

the sort of companies that BlackRock’s active arm is now divesting from. So, what

exactly BlackRock can do about that? Is this more than greenwash?

Mr Fink

has said that BlackRock will be doubling its offerings of ESG ETFs and will work

with index providers to expand and improve the universe of sustainable indices.

The company will also simplify the process by which investors can integrate ESG

into their existing portfolios by adding a fossil fuel screen and has also

expanded its impact investment strategy.

But the

contradiction between the company’s new activist stance and the passive

replication of an energy-heavy index such as Australia’s is obvious. One

solution might be for large mining companies such as BHP to dump their coal

assets in order to remain part of both Blackrock’s actively managed (stock

picking) and passively managed (all stocks) portfolios. This was discussed in a

recent “The Conversation” article.

Another

might be the development of index funds from which firms reliant on fossil

fuels are excluded. It is even possible that the compilers of stock market

indexes will themselves exclude these firms.

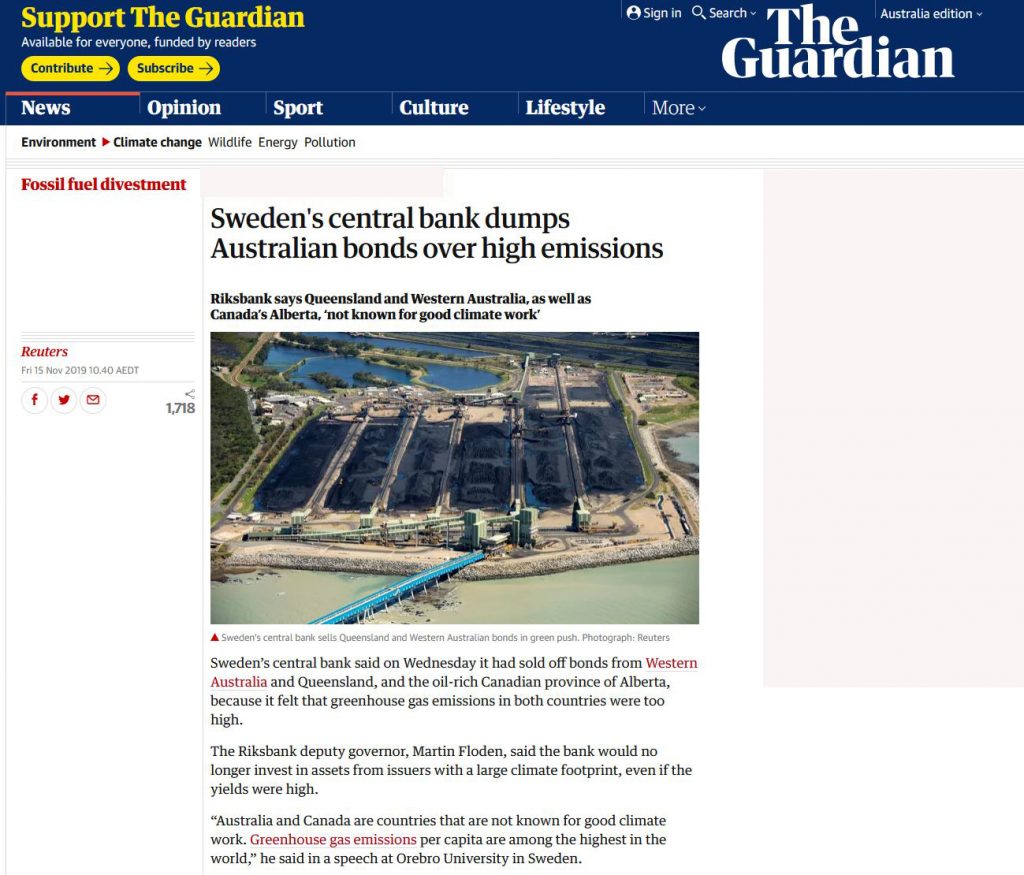

But once

bond investors follow the lead of Blackrock and other financial institutions,

divestment of Australian government bonds will likely follow. This process has

already started, with the decision of Sweden’s central bank to unload its holdings of

Australian government bonds.

Taken in

isolation, Sweden’s move had virtually no effect on Australia’s bond prices and

yields. But the most striking feature of the divestment movement so far is the

speed with which it has grown from symbolic gestures to a severe constraint on

funding for the firms it touches.

The

effects might be felt before large-scale divestment takes place. Ratings

agencies such as Moody’s and Standard and Poors are supposed to anticipate risks

to bondholders before they materialise.

Once

there is a serious threat of large-scale divestment in Australian bonds, the

agencies will be obliged to take this into account in setting Ausralia’s credit

rating. The much-prized AAA rating is likely to be an early casualty.

That

would mean higher interest rates for Australian government bonds which would

flow through the entire economy, including the home mortgage rates mentioned in

the Blackrock statement.

So the government’s case for doing nothing about climate change (other than cashing in on past efforts) has been premised on the “economy-wrecking” costs of serious action. But as investments associated with coal are increasingly seen as toxic, we run an increasing risk that inaction will cause greater damage. So yes, Blackrock’s announcement is a real wake-up call, like it or not.

In this trimmed high quality recording of our live event, we discuss the latest financial and property data, examine our latest scenarios, and discuss the trends ahead. We also answer a range of questions posed by our viewers live. The unedited original stream with live chat, is available to view (starting at 0:30) below: