To address temporary disruptions

in the market for Treasury securities, the Open Market Trading Desk

(the Desk) at the Federal Reserve Bank of New York has updated the

current monthly schedule of Treasury purchase operations.

Today, the Desk will conduct purchases

in each of five maturity sectors below at the times indicated, subject

to reasonable prices.

20 to 30 year sector at 10:30 – 10:45 am and 2:15 to 2:45 pm for around $4 billion each

7 to 20 year sector at 11:15 – 11:30 am for around $5 billion

4.5 to 7 year sector at 12:00 – 12:15 pm for around $8 billion

2.25 to 4.5 year sector at 12:45 – 1:00 pm for around $8 billion

0 to 2.25 year sector at 1:30 – 1:45 pm for around $8 billion

These purchases are intended to address highly unusual disruptions in the market for Treasury securities associated with the coronavirus outbreak. These purchases are part of the $80 billion of planned monthly purchases, including both $60 billion of reserve management purchases and $20 billion of reinvestments of principal payments received from the Federal Reserve’s holdings of agency debt and agency mortgage-backed securities. In these purchases, the Desk will include securities that are cheapest to deliver into active Treasury futures contracts as eligible securities for purchase. The Desk intends to further bring forward remaining purchases for this monthly calendar and adjust terms of operations as needed to foster smooth Treasury market functioning and efficient and effective policy implementation. A revised schedule will be posted.

The Dow plunged to its biggest-one day

percentage loss since October 1987 as fears the spread of the novel

coronavirus will pick up pace and usher in a global recession

overshadowed the Federal Reserve’s bold new stimulus measures to calm

funding markets.

The Dow Jones Industrial Average

fell nearly 10%, or 2,352 points, it worst one-day percentage drop

since Black Monday when it lost 22.6%. It was the fourth-largest

percentage drop for the blue chip index in history, rivaling those seen

in 1929.

The rout on Wall Street for the second-straight day comes as investors upped their bearish bets on stocks despite the Federal Reserve unveiling $1.5 trillion in fresh liquidity to combat “temporary disruptions” in funding markets.

The short-term pause in selling following the Fed announcement proved short-lived as investor sentiment on stocks continued to be swayed by the latest updates on the spread of Covid-19, which has killed nearly 5,000 people, with infections topping 133,000 worldwide.

In the U.S., where infections are feared

to increase in the coming weeks, state-wide bans on large gatherings to

limit the virus impact continued, with New York announcing announce a

ban on gatherings of 500 or more people.

The Fed’s announcement was unprecedented:

The Open Market Trading Desk (the

Desk) at the Federal Reserve Bank of New York has released a new

monthly schedule of Treasury securities operations and has updated the

current monthly schedule of repurchase agreement (repo) operations.

Pursuant to instruction from the Chair in consultation with the FOMC,

adjustments have been made to these schedules to address temporary

disruptions in Treasury financing markets. The Treasury securities

operation schedule includes a change in the maturity composition of

purchases to support functioning in the market for U.S. Treasury

securities. Term repo operations in large size have been added to

enhance functioning of secured U.S. dollar funding markets.

As a part of its $60 billion reserve

management purchases for the monthly period beginning March 13, 2020

and continuing through April 13, 2020, the Desk will conduct purchases

across a range of maturities to roughly match the maturity composition

of Treasury securities outstanding. Specifically, the Desk plans to

distribute reserve management purchases across eleven sectors,

including nominal coupons, bills, Treasury Inflation-Protected

Securities, and Floating Rate Notes. The distribution of purchases

across sectors will be the same distribution as the Desk uses to

reinvest principal payments from the Federal Reserve’s holdings of

agency debt and agency MBS in Treasury securities. The first such

purchases will begin tomorrow, March 13, 2020.

Today, March 12, 2020, the Desk will

offer $500 billion in a three-month repo operation at 1:30 pm ET that

will settle on March 13, 2020. Tomorrow, the Desk will further offer

$500 billion in a three-month repo operation and $500 billion in a

one-month repo operation for same day settlement. Three-month and

one-month repo operations for $500 billion will be offered on a weekly

basis for the remainder of the monthly schedule. The Desk will

continue to offer at least $175 billion in daily overnight repo

operations and at least $45 billion in two-week term repo operations

twice per week over this period.

These changes are being made to address highly unusual disruptions in Treasury financing markets associated with the coronavirus outbreak. Reserve management purchases into the second quarter will continue to be conducted with this maturity allocation. The terms of operations will be adjusted as needed to foster smooth Treasury market functioning and efficient and effective policy implementation.

Detailed information on the schedule of Treasury purchases is provided on the Treasury Securities Operational Details page.

Detailed information on the schedule and parameters of term and

overnight repo operations are provided on the Repurchase Agreement

Operational Details page.

The Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York has released the repurchase agreement (repo) operational schedule for the upcoming period.

Beginning Thursday, March 12, 2020 and

continuing through Monday, April 13, 2020, the Desk will offer at least

$175 billion in daily overnight repo operations and at least $45

billion in two-week term repo operations twice per week over this

period. In addition, the Desk will also offer three one-month term

repo operations, with the first operation occurring on Thursday, March

12, 2020. The amount offered for each of these three operations will

be at least $50 billion.

Consistent with the FOMC directive

to the Desk, these operations are intended to ensure that the supply of

reserves remains ample and to mitigate the risk of money market

pressures that could adversely affect policy implementation. They

should help support smooth functioning of funding markets as market

participants implement business resiliency plans in response to the

coronavirus. The Desk will continue to adjust repo operations as

needed to foster efficient and effective policy implementation

consistent with the FOMC directive.

Detailed information on the schedule and parameters of term and overnight repo operations are provided on the Repurchase Agreement Operational Details page.

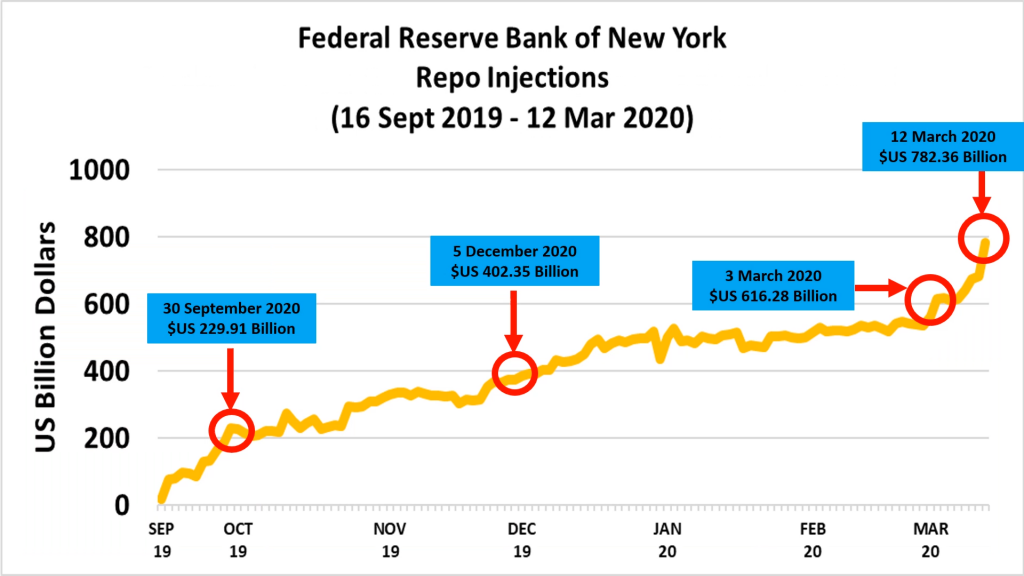

We are headed to $800 billion extra liquidity, which clearly is more than a temporary problem in the banking system. John Adams and I discussed this in a recent post.

The BIS has released their quarterly update. It comprises a review of market developments over the past quarter, and special features that analyse topical economic and financial issues.

Overall, they say that easing trade tensions in mid-October triggered a risk-on phase in global financial markets. Equity prices rallied, reaching new highs in the United States in November. At the same time, credit spreads tightened, and yields on safe sovereign bonds edged higher. Nevertheless, the economic outlook remained tepid and inflation low, leading central banks to ease further.

The renewed risk appetite, coupled with loose financial conditions, sparked questions about the sustainability of asset valuations. Investors’ compensation for bearing risk seems to hinge on the term premium; to the extent that the premium is unusually low, it may flatter valuations.

Claudio Borio, Head of the BIS Monetary

and Economic Department, commented: “Rather stretched asset valuations,

high risk-taking and hard-to-read changes in the financial system: the

mixture points to certain vulnerabilities in financial markets that

merit close attention on the part of market participants and central

banks alike.”

They offer specific analysis of the US Repo problem, and highlight a significant structural change as some US major banks become net providers of liquidity.

The mid-September tensions in the US dollar market for repurchase agreements (repos) were highly unusual. Repo rates typically fluctuate in an intraday range of 10 basis points, or at most 20 basis points. On 17 September, the secured overnight funding rate (SOFR) – the new, repo market-based, US dollar overnight reference rate – more than doubled, and the intraday range jumped to about 700 basis points. Intraday volatility in the federal funds rate was also unusually high. The reasons for this dislocation have been extensively debated; explanations include a due date for US corporate taxes and a large settlement of US Treasury securities. Yet none of these temporary factors can fully explain the exceptional jump in repo rates.

This box focuses on the distribution of liquid assets in the US banking system and how it became an underlying structural factor that could have amplified the repo rate reaction. US repo markets currently rely heavily on four banks as marginal lenders. As the composition of their liquid assets became more skewed towards US Treasuries, their ability to supply funding at short notice in repo markets was diminished. At the same time, increased demand for funding from leveraged financial institutions (eg hedge funds) via Treasury repos appears to have compounded the strains of the temporary factors. Finally, the stress may have been amplified in part by hysteresis effects brought about by a long period of abundant reserves, owing to the Federal Reserve’s large-scale asset purchases.

A repo transaction is a short-term

(usually overnight) collateralised loan, in which the borrower (of cash)

sells a security (typically government bonds as collateral) to the

lender, with a commitment to buy it back later at the same price plus

interest. Repo markets redistribute liquidity between financial

institutions: not only banks (as is the case with the federal funds

market), but also insurance companies, asset managers, money market

funds and other institutional investors. In so doing, they help other

financial markets to function smoothly. Thus, any sustained disruption

in this market, with daily turnover in the US market of about $1

trillion, could quickly ripple through the financial system. The

freezing-up of repo markets in late 2008 was one of the most damaging

aspects of the Great Financial Crisis (GFC).

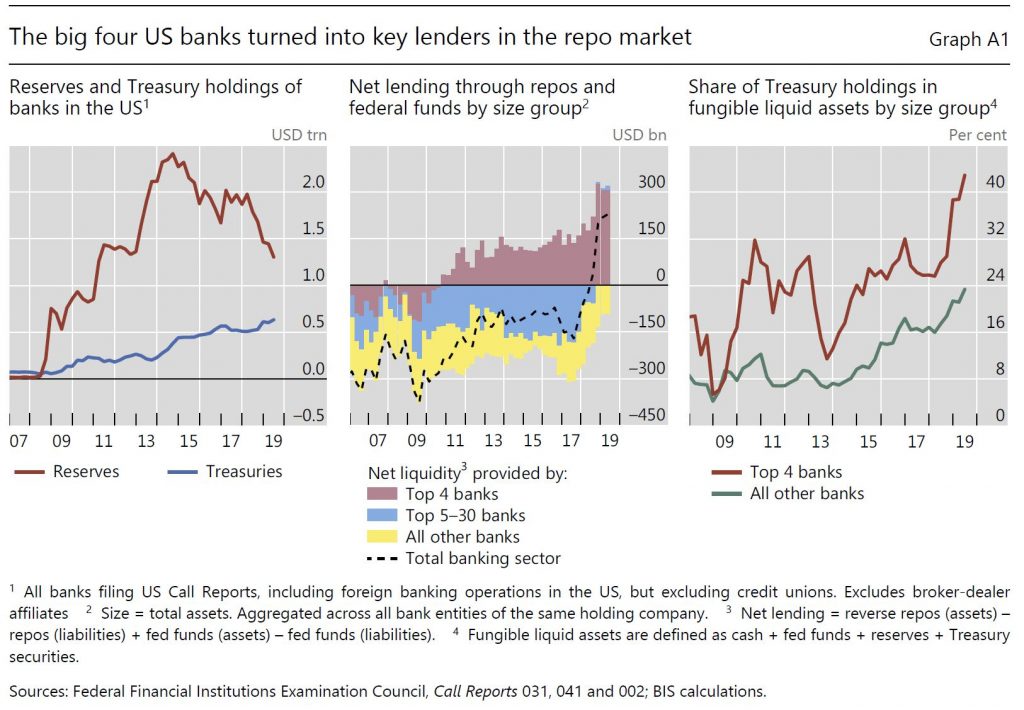

The liquid asset holdings of US banks and

their composition have changed significantly since the GFC. Successive

rounds of large-scale asset purchases reduced the free float of

long-dated US Treasuries available to the market between the end of 2008

and October 2014. On the flip side, banks accumulated large amounts of

reserve balances remunerated at the Fed’s interest on excess reserves

(IOER) (Graph A.1,

left-hand panel, red line). After the Federal Reserve started to run

down its balance sheet in October 2017, reserves contracted, quickly but

in an orderly way as intended. Alongside, banks’ holdings of US

Treasuries increased, almost trebling between end-2013 and the second

quarter of 2019 (blue line).

As repo rates started to increase above

the IOER from mid-2018 owing to the large issuance of Treasuries, a

remarkable shift took place: the US banking system as a whole, hitherto a

net provider of collateral, became a net provider of funds to repo

markets. The four largest US banks specifically turned into key players:

their net lending position (reverse repo assets minus repo liabilities)

increased quickly, reaching about $300 billion at end-June 2019 (Graph A.1,

centre panel, red bars). At the same time, the next largest 25 banks

reduced their demand for repo funding, turning the net repo position of

the banking sector positive (centre panel, dashed line). The big four

banks appear to have turned into the marginal lender, possibly as other

banks do not have the scale and non-bank cash suppliers such as money

market funds (MMFs) hit exposure limits (see below).

Concurrent with the growing role of the

largest four banks in the repo market, their liquid asset holdings have

become increasingly skewed towards US Treasuries, much more so than for

the other, smaller banks (Graph A.1,

right-hand panel). As of the second quarter of 2019, the big four banks

alone accounted for more than 50% of the total Treasury securities held

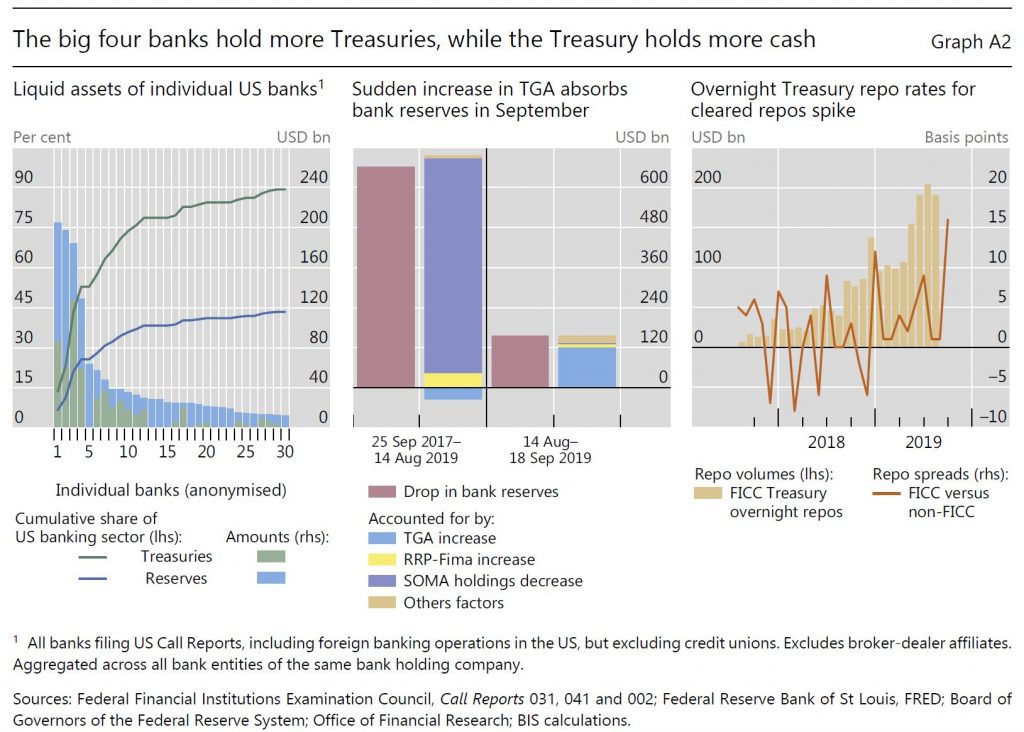

by banks in the United States – the largest 30 banks held about 90% (Graph A.2,

left-hand panel). At the same time, the four largest banks held only

about 25% of reserves (ie funding that they could supply at short notice

in repo markets).

Cash balances held by the US Treasury in

its Federal Reserve account (the Treasury General Account, TGA) grew in

size and became more volatile, especially after 2015. The resulting

drain and swings in reserves are likely to have reduced the cash buffers

of the big four banks and their willingness to lend into the repo

market. After the debt ceiling was suspended in early August 2019, the

US Treasury quickly set out to rebuild its dwindling cash balances,

draining more than $120 billion of reserves in the 30 days between 14

August and 17 September alone, and half of this amount in the last week

of that period. By comparison, while the Federal Reserve runoff removed

about five times this amount, it did so over almost two years (Graph A.2, centre panel).

Besides these shifts in market structure

and balance sheet composition, other factors may help to explain why

banks did not lend into the repo market, despite attractive profit

opportunities.

A reduction in money market activity is a natural by-product of central

bank balance sheet expansion. If it persists for a prolonged period, it

may result in hysteresis effects that hamper market functioning. For

instance, the internal processes and knowledge that banks need to ensure

prompt and smooth market operations may start to decay. This could take

the form of staff inexperience and fewer market-makers, slowing

internal processes.

Moreover, for regulatory requirements – the liquidity coverage ratio –

reserves and Treasuries are high-quality liquid assets (HQLA) of

equivalent standing. But in practice, especially when managing internal

intraday liquidity needs, banks prefer to keep reserves for their

superior availability.

Shifts in repo borrowing and lending by

non-bank participants may have also played a role in the repo rate

spike. Market commentary suggests that, in preceding quarters, leveraged

players (eg hedge funds) were increasing their demand for Treasury

repos to fund arbitrage trades between cash bonds and derivatives. Since

2017, MMFs have been lending to a broader range of repo counterparties,

including hedge funds, potentially obtaining higher returns.

These transactions are cleared by the Fixed Income Clearing Corporation

(FICC), with a dealer sponsor (usually a bank or broker-dealer) taking

on the credit risk. The resulting remarkable rise in FICC-cleared repos

indirectly connected these players. During September, however,

quantities dropped and rates rose, suggesting a reluctance, also on the

part of MMFs, to lend into these markets (Graph A.2,

right-hand panel). Market intelligence suggests MMFs were concerned by

potential large redemptions given strong prior inflows. Counterparty

exposure limits may have contributed to the drop in quantities, as these

repos now account for almost 20% of the total provided by MMFs.

Since 17 September, the Federal Reserve has taken various measures to supply more reserves and alleviate repo market pressures. These operations were expanded in scope to term repos (of two to six weeks) and increased in size and time horizon (at least through January 2020). The Federal Reserve further announced on 11 October the purchase of Treasury bills at an initial pace of $60 billion per month to offset the increase in non-reserve liabilities (eg the TGA). These ongoing operations have calmed markets.

But, I would observe, that structural change remains…

Blog")