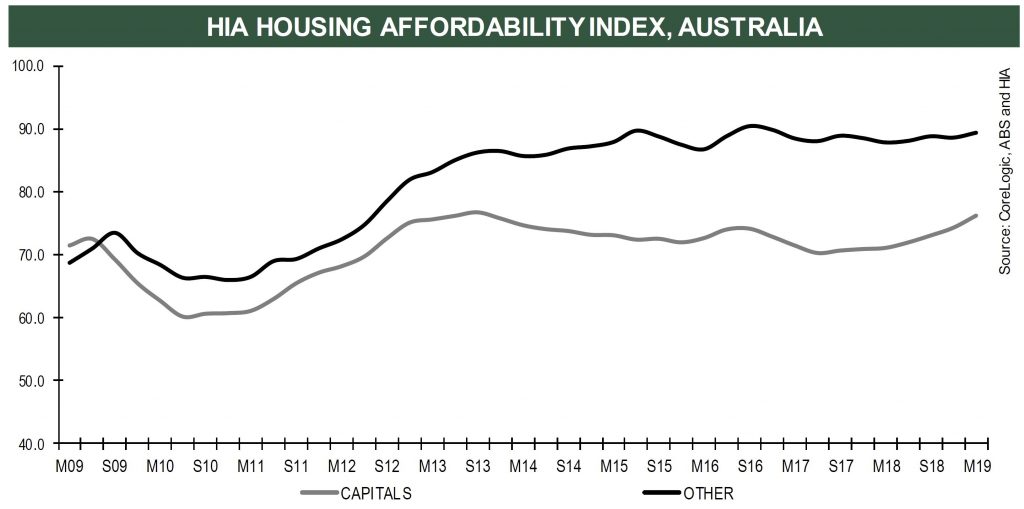

The HIA reported today that there was been a 10% improvement in affordability in a year. They attribute this to – wait for it, more building and wage rises – but do not mention the elephant in the room, the home price falls, which are continuing – at more than 10% in Sydney and Melbourne! No surprise, as home prices fall, affordability improves…

Five of the eight capital cities saw improved affordability over the year to March 2019. Sydney continues to be home to the greatest improvements, its index is up by 12.4 per cent. This was followed by Melbourne (+9.6 per cent), Perth (+7.7 per cent), Darwin (+5.9 per cent) and Brisbane (+2.5 per cent). Affordability deteriorated in Hobart (-5.1 per cent), Canberra (-5.1 per cent) and Adelaide (-1.1 per cent).

HIA’s Affordability Index is calculated for each of the eight capital cities and regional areas on a quarterly basis and takes into account the latest dwelling prices, mortgage interest rates and wage developments.

“The HIA Affordability Index rose by 2.2 per cent in the March 2019 quarter to post the most significant improvement in affordability since September 2013,” said Tim Reardon, HIA Chief Economist.

“The improvement in housing affordability has been experienced across the country, with the exception only of Tasmania and the ACT, where ongoing house price growth has seen affordability remain static,” added Mr Reardon.

“The boom in home building of the past five years is a key factor behind the improvement in housing affordability. With completions of new homes remaining at elevated levels, affordability is poised to continue to improve.

“Wage growth also contributed to the improvement in affordability.

“The improvement in affordability is most significant in east coast capital cities. Affordability in Sydney deteriorated to an extent that in June 2017 it required two average Sydney incomes to be able to afford repayments on an average Sydney home. In just over a year this has improved to only requiring 1.8 standard incomes to purchase the same home.

“Similarly, in Melbourne the Affordability Index has improved by almost 10 per cent in a year,” concluded Mr Reardon.

The Tasmanian Government announced yesterday that they have extended their first home builders grant.

The Hodgman Liberal Government is a strong supporter of our building and construction industry, and we want to boost dwelling construction so more Tasmanians can be in a position to own their own home.

The Hodgman Liberal Government will extend the first home builders grant in the upcoming budget so more young Tasmanians can realise the dream of building their first home.

The extension comes after we doubled the first home builders grant to $20,000 in the 2016-17 Budget.

We understand that there is high demand for new housing, and the first home builders grant is one part of our multi-pronged approach to address housing stress in Tasmania.

According to the latest ABS figures, Tasmania continues to lead the nation in the annual growth in building approvals.

The number of dwelling approvals grew 24.1 per cent in March 2019 compared to March 2018, with Tasmania one of only two jurisdictions to record growth. This is in stark contrast to the sharp fall in National approvals, which was down by 22.4 per cent over the same period.

This initiative will give Tasmanians a greater opportunity to build and own their own home, adding to supply, and complementing the action the Government is taking through our Affordable Housing Strategy.

The extension of the grant will have positive flow-on effects for Tasmania’s booming building and construction industry, creating more work, and more jobs.

Tasmanian prices are still rising, as MyStateBank media release from 9th May reveals.

Median house prices are falling across most parts of the country, yet Hobart is bucking the national trend. Dwelling values in Hobart grew by 3.8% in the year ending April 2019, the highest of all other capital cities and one of only three capital cities to experience growth. Nationally, house price growth fell 7.2% over the same period.

“Australian homeowners see the appeal of selling up in markets like Sydney and Melbourne and buying in Tasmania, where it is more likely they’ll be able to afford a bigger property for a much cheaper price. The state’s strong economic conditions and attractiveness as a lifestyle choice are also big drawcards for residents on mainland Australia, fuelling housing demand,”

“A tightening in credit supply is also driving prospective buyers out of larger property markets like Melbourne and Sydney where demand from investors and owner occupiers has dampened.”

In fact, Tasmania is the only state to have experienced an increase in mortgage applications (+1.5%) over the year to December 2018. Mortgage applications in Victoria and New South Wales fell over the same period by 15.4% and 19.1% respectively.

Pressure on Tasmanian rental market unlikely to continue in the long term.

“Population growth and lack of new housing supply is putting considerable pressure on the Tasmanian rental market.”

MyState’s analysis shows Hobart’s strong rental yield position has increased to 5.2% in the year to April, the highest in the country. The median weekly house rent is $450 – now $10 more than Melbourne.

However, the issue of a lack of housing supply is unlikely to be a long-term one, with the state recording nation leading growth in the number of residential building approvals at 24% from March 2018 to March 2019.

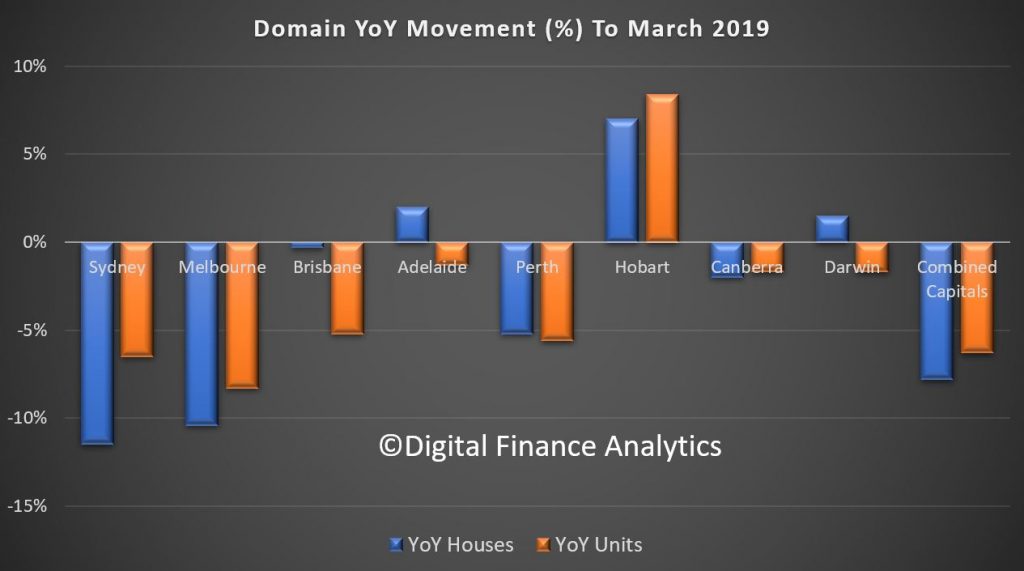

Domain has released their March quarter 2019 house price data. Sydney, Melbourne and Perth are bearing the brunt of the falls, alongside units in Brisbane, according to their statistics. Hobart remains the most buoyant but buyer interest appears to have passed its peak . And of course remember these are average figures which mask local changes.

They says that Sydney’s current property downturn is the sharpest in more than two decades. It is yet to surpass the duration of the 2004-06 slump but it is coming close to being the longest. Sydney house prices have fallen 14.3 per cent from the mid-2017 peak. If the pace of quarterly decline remains, prices are likely to dip below $1 million in the coming quarter. A six-figure median house price has not been recorded in four years. Sydney unit prices have fallen 9.9 per cent from the mid-2017 peak. For the first time in three years unit prices are below $700,000.

Despite further price deterioration to house and unit prices over the quarter, the rate of decline has eased from the quarterly falls recorded last year. House prices are now back to early 2016 and units back to mid-2015. However, house prices are 30.2 per cent higher and unit prices 20.7 per cent higher than five years ago, providing many homeowners with substantial equity gain.

Melbourne is currently facing its steepest downturn in more than two

decades. House prices have fallen for five consecutive quarters, down 11

per cent from the peak reached at the end of 2017. Unit prices have

held firmer, with price falls shorter and less severe relative to

houses. Unit prices have deteriorated for four consecutive quarters,

pulling prices back 8.3 per cent from the peak notched a year ago.

The Melbourne property market started 2019 better than 2018 ended, with auction clearance rates nudging higher (admittedly from lower volumes), views per listing rising marginally, and banks now actively seeking new business. The rate of house price declines have eased over the latest quarter.

Greater Brisbane house prices have stalled following six years of

continuous annual growth, with prices flatlining over the year.

Homeowners may not be reaping equity gain but flat house prices is a

better outcome than a fall, which is what’s playing out across most

capital cities.

The housing market remains fragmented with houses outperforming units. This has been a trend since mid-2012. Unit prices are 9.6 per cent below the mid-2016 peak, with buyers now able to reap the benefits of purchasing at 2013 prices. Significant supply numbers have weighed heavily on unit prices. Although listing volumes are shrinking, it has not been enough to translate into price growth yet.

House prices in Adelaide have bucked the national downward trend and

became one of only three capital cities to rise over the year.

Homeowners have reaped the benefit of almost six years of steady annual

house price growth. House prices may have flatlined over the quarter,

but it is the second best outcome of all the capital cities, behind

Hobart. The sustainable pace of annual growth has slowed to a

five-and-a-half year low. This weakness provides further evidence that

credit access is having an impact on markets that would otherwise have

steady growth.

Adelaide is now the third most affordable city to purchase a house, surpassing Perth’s median house price for the first time since 1993. House prices currently remain higher than Hobart, but galloping Hobart prices mean the price gap is at a 12-year low. Adelaide’s unit prices have marginally fallen from the record high achieved last quarter, but remain the most affordable of all the capital cities.

Early indicators previously displayed some encouraging signs of a

recovery in Perth’s housing market. However, over the first quarter of

this year, house and unit price falls have gathered pace. House prices

are now 14 per cent and unit prices 16.6 per cent below the 2014 peak.

Buyers continue to have the upper hand. Improved affordability is providing the ultimate silver lining for prospective homeowners, allowing a purchase to be made at 2011 prices. Perth’s recovery is being hindered by a more restrictive lending environment at a time when local confidence is subdued under weak economic conditions. A sluggish economy is being dragged down by high unemployment, a tight consumer purse, and weak population growth.

Hobart bucked the national downward trend, and remains the best

performing city for capital growth. It became the only city to record

growth over the quarter and year for both houses and units. Despite

this, the pace of house price growth has slowed to half of that recorded

over the same period in 2018, providing homeowners the lowest annual

growth since mid-2016. In the space of a year-and-a-half, Hobart has

gone from the most affordable city to purchase a unit, to more expensive

than Adelaide, Darwin and Perth. If the pace of growth continues,

Hobart unit prices are likely to overtake Brisbane’s in the coming

months.

Hobart became a hotspot for investors, a destination for interstate buyers seeking the ultimate lifestyle location, and tourism flourished helping to drive economic growth and place pressure on housing demand. Buyer interest appears to have passed its peak, with Domain recording a slip in the number of views per listing over the past two months. It is likely that capital gains will be more subdued than the double-digit growth recorded last year.

Canberra’s housing market has shown the first signs of price weakness

since 2012. House prices had their steepest annual fall in a decade,

following a stint of continuous growth that spanned roughly six years.

Despite this, the nation’s capital has a tendency to be the quiet

achiever, providing homeowners with steady equity growth. Historically,

any pullback in house prices tend to be short and relatively minor,

apart from the 1995-97 downturn. Current market conditions are likely to

be the same, a short period of softening rather than the correction

currently unravelling in Sydney and Melbourne.

Unit prices continue to slide over the quarter and year, with the market failing to produce a steady period of price growth since 2009-10. The outlook for apartment prices has been mixed, providing only subdued capital growth over the past five years, up by 4.5 per cent. Equity growth in houses has been superior at 25.8 per cent.

The peak of Darwin’s housing market is in the rear-view mirror – with

prices hitting a high during 2013-14. House and unit prices continue to

be impacted from the weak economic conditions that have ensued post the

mining boom, with a soft employment sector and lack of migration

weighing on the demand for housing. A recovery in Darwin’s housing

market largely hinges on the government’s attempts at boosting the

population, jobs growth and an improvement in the availability of

housing credit.

Drawing from his direct experience in the market, mortgage broker and financial adviser Chris Bates and I discuss the latest issues and consider the impact of negative gearing reform.

Chris can be found at www.wealthful.com.au & www.theelephantintheroom.com.au plus via LinkedIn: https://www.linkedin.com/in/christopherbates

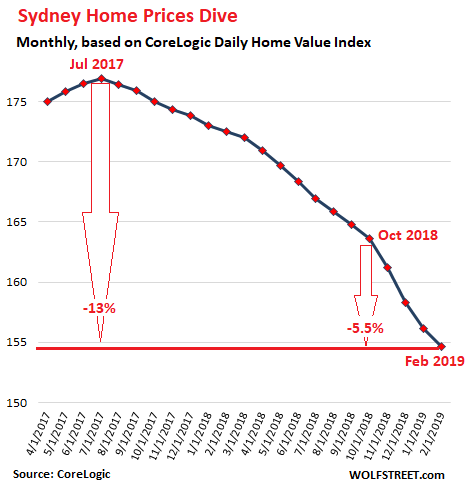

Across the metro area of Sydney, prices of all types of homes combined, according to CoreLogic’s Home Value Index,

fell 1.0% in February from January, 10.4% from a year ago, and nearly

13% from its peak in July 2017. Just over the past four months, the

index has dropped 5.5%:

The volume of closed sales recorded in Sydney in February plunged

20.6% from the already weak sales in February last year, according to

CoreLogic’s report.

Units, generally the lower end of the market, is where first-time buyers are thought to have a chance, and they were considered the saving grace in this market. But prices continue to drop, and the industry’s hope that first time buyers would bail out this market is now fading.

House prices dropped 1.1% in February and 11.5% year-over-year.

Unit prices dropped 0.8% in February and 8.8% year-over-year.

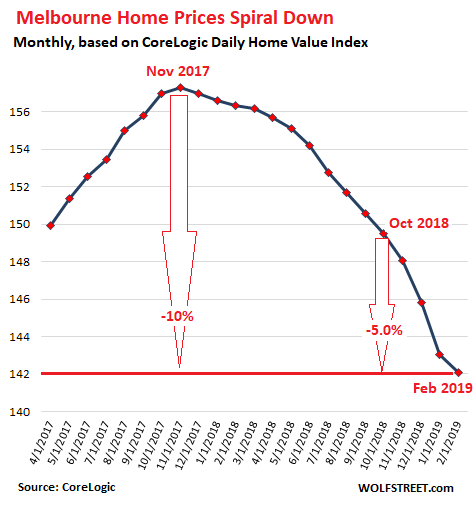

In the Melbourne metro, the second largest market in Australia,

prices of all types of homes fell 1% for the month and 9.1%

year-over-year, according to the CoreLogic Home Value Index. The index

is now down nearly 10% from the peak in November 2017. Over just the

past four months, the index for Melbourne dropped 5.0%:

House prices in Melbourne dropped 1.2% for the month and 11.5%

year-over-year. Condo prices dropped 0.6% for the months and 3.7%

year-over year. CoreLogic estimates that closed sales in Melbourne

plunged 22.1% in February from the already weak sales a year ago.

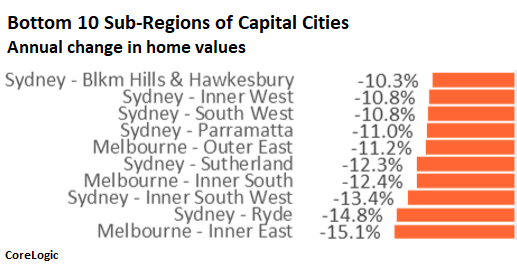

Of the bottom 10 sub-regions of Australia’s capital cities seven were

in the Sydney metro and three were in Melbourne (chart via CoreLogic):

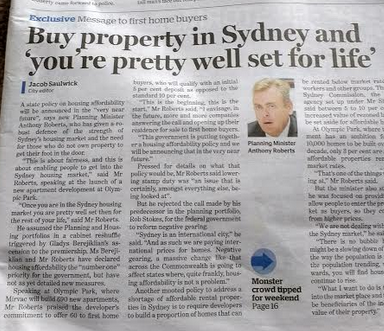

As Wolf Street highlights, there is a bitter irony to all this. In February 2017, just months before the market in Sydney peaked, Anthony Roberts, New South Wales Minister for Planning and Housing, was promoting the launch of a 690-unit apartment development at Olympic Park, a suburb of Sydney, heaping praise on the developer for having reserved 60 units for first-time buyers.

Roberts was hyping new incentives for first-time buyers, including a

reduction of the down-payment to 5%, to lure them into the Sydney

housing market:

“This is about fairness, and this is about enabling people to get

into the Sydney housing market. Once you are in the Sydney housing

market, you’re pretty well set then for the rest of your life.”

The metros of Sydney and Melbourne, due to their enormous size and

high prices, dominate the national home values, but weakness is now

spreading to other capital cities, with only Hobart and Canberra still

showing year-over-year gains (in parenthesis, CoreLogic’s measure of

“median value”):

Sydney: -10.4% (A$789K)

Melbourne: -9.1% (A$629K)

Brisbane: -0.5% (A$491K)

Adelaide: -1.0% ($433K)

Perth: -6.9% (A$439K)

Hobart +7.2% (A$457K)

Darwin: -5.3% (A$398K)

Canberra +3.4% (A$594K)

On a national basis, the CoreLogic Home Value Index dropped 6.3%

year-over-year and 6.8% from its peak in October 2017. It’s now back

where it had been in September 2016. CoreLogic’s report

points out that, despite the decline, the index remains 18% higher than

it had been five years ago, “highlighting that most home owners remain

in a strong equity position.” Only recent buyers are underwater.

That’s a calming thought, even for the Reserve Bank of Australia, according to the minutes

for its Monetary Policy Meeting on February 5, 2019, when it decided to

maintain its policy rate at the record low level of 1.5%:

From a longer-run perspective, members assessed that,

following such large increases in housing prices, the effect of the

recent price falls on overall economic activity was expected to be

relatively small.

From a financial stability perspective, tighter lending standards, an

improving labor market and low interest rates were all likely to

support households’ capacity to service their debt.

Few households were in negative equity positions despite the falls in

housing prices, implying that banks’ losses would be limited even if

household financial stress were to become more widespread.

The IMF was less sanguine in its assessment

of Australia. It found that “the financial sector faces continued

vulnerabilities from high household debt, still-stretched real estate

valuations, and banks’ ongoing dependence on funding from global

markets.”

The assessment “recommended further steps to bolster financial

supervision as well as to reinforce financial crisis management,” which

might be a good idea.

We look at the latest real estate data from the US, where sales volumes are falling and home price growth is stalling.

And we read across to the local scene, where despite the hype about auction clearance rates, home price falls are accelerating. Indeed, we expect more ahead.

Welcome to the

Property Imperative weekly to the 23rd of February 2019 – our digest of the

latest finance and property news with a distinctively Australian flavour.

Watch the video, listen to the podcast or read the transcript.

The gap between the real data on housing and finance and the narrative offered by the RBA continues to wide, plus more on banking separation, which is now running on a new set of legs, and the markets are backing the end of the Trade Wars just as China turns off the tap to some Australia coal exports. But people are claiming its just a little local difficulty.

And by the way, if you value the content we produce, please do consider supporting our efforts. You can make a one off donation via PayPal here is the link, or consider joining our Patreon programme. We really appreciate your support to help us continue to make great content.

Governor Lowe appeared before the House Standing Committee On Economics

which took place on Friday. The session was streamed in audio only (a poor show

that they were unable to arrange a web show, as its was hard to follow who was

talking) and a

transcript has been released. He said that the RBA’s central scenario for

this year is for growth of around three per cent, inflation of around two per

cent and unemployment of around five per cent. The economy is benefiting from

increased spending on infrastructure and a pick-up in private investment as

capacity utilisation has tightened. The strong growth in jobs is also

supporting spending, as is the sustained low level of interest rates. Looking

beyond income growth, developments in the housing market can also affect

overall spending in the economy. Lower

turnover means less of the spending that occurs when people move homes. Declining housing prices also make some

people feel less wealthy, so they spend less, although this effect doesn’t look

to be particularly large. Lower housing

prices are also associated with less construction activity in the economy, so

these are the areas that we’re keeping a close watch on. This adjustment in the

housing market is

not expected to

derail our economy. It will put

our housing markets on more sustainable footings, and it will allow more people

to purchase their own home.

There are some wealth effects from declining housing prices, but they’re

relatively small. We’ve got to remember that in Sydney and Melbourne prices are

still up 70 or

80 per cent

over a decade,

so most people

are sitting on

very substantial capital

gains. People who purchased in

the last year or 18 months are not, but most people are sitting on substantial

capital gains, so there are still positive

wealth effects coming

from that. It’s largely the income

story which doesn’t

get talked about enough, because the media love talking

about property prices, but year after year of weak income growth finally weighs

on our spending plans, so both the pick-up in wage growth and the tax cuts will

boost disposable-income growth.

There were three points to take away. First the RBA is holding to its

view that eventually wages will start to rise, despite the results reported by

the ABS this week. The trend Wage Price Index (WPI) rose 0.5 per cent in

December quarter 2018 and 2.3 per cent through the year, according to figures from

the Australian Bureau of Statistics. Growth remains anaemic. The trend

quarterly rise of 0.5 per cent continues an extended period of moderate hourly

wage growth. Annually, private sector wages rose 2.3 per cent and public sector

wages grew 2.5 per cent.

Second, Lowe played down the home price falls, and argued this had

little to do with APRA tightening lending standards as banks are still lending,

and offering discounted rates for new loans.

Third, the RBA will use monetary policy to trim the economic sails,

including expected tax cuts and even a lower US dollar, but accepted that QE

could be used in certain scenarios, if required. Dr Lowe said “I would

very much hope

that we don’t

have to go

down that route.

If the economy were

to slow significantly, there

are multiple margins

of adjustment—things that

could be done.

We could lower interest rates further; of course, there could be a

fiscal stimulus; and the exchange rate would adjust. So all those margins of

adjustment could take place before we would need to consider this, but in

extremis there are scenarios where that would have to be seriously considered.

And by the way, they played down the potential impact on asset prices if

QE were to be activated.

So I came away with a view that the RBA’s perspective continues to be

rosy, perhaps too rosy and the impact of tighter credit, the easing credit

impulse and lower loan to income multiples seem unimportant. I found this predictable. But remember they have said recently they are

not sure what level of debt would be too much, implying we are not there yet.

Given the high household debt ratios in Australia, this is lack of focus on

debt is disgraceful.

The Bank of England this week in a blog

on Bank Underground “What goes up must come down: modelling the mortgage cycle”

– said “it is critical for economists and policymakers to understand the

drivers of the mortgage credit cycle. On the one hand, it is important for

policymakers to know how the housing cycle and mortgage structure affect the

transmission of monetary policy. On the other hand, spotting the signs of a

potential mortgage market slowdown early on might help to avoid some of the

detrimental impacts from future events similar to those that took place a

decade ago”.

We agree, and I must question whether the RBA does. And I have to say, I felt the Governor had a

very easy time in the committee, other than the QE discussion. The rest was all

puff.

In contrast we ran our live show this week, taking questions from our

audience of more that 600 real-time viewers. We updated our property scenarios to

take account of a range of new data, and the latest input from our household

surveys. A peak to trough home price fall of 20-30% over 2-3 years remains our

base case, but with risks to the downside. On the other hand, the RBA’s base

case gets only a 1% probability now.

The factors we have considered include: Lower inflation and growth rates

ahead according to the RBA, Fed future rate hikes on hold, Potential for more

QE (Euro Zone, Japan, others), Recent home price falls in Australia driven by

weaker credit impulse, Underemployment still a significant issue and wages flat.

We also have used updated households’ intention to transaction data, mortgage

stress and affordability metrics. In passing it’s worth noting that ANZ

revealed their mortgage underwriting standards are now ~20% tighter, though

they are focussing more on investor lending ahead. Other Banks are even

tighter. “Mortgage Power” has been significantly curtailed. Here are the

results from our Core Market Model, with a probability rating and here is a

summary of the scenarios.

Business As Usual: RBA driven scenario

Things Can Only Get Better: Economy is weaker, as wages continue to grow

only slowly, costs rise, and RBA cuts later in the year. Some Government tax stimulation

either before or after the election, or both. Some easing of credit rules so

lending growth accelerates.

Not Yet Doomsday: A locally driven downturn, as wages are flat, despite

some mortgage rate repricing. RBA cuts significantly. Employment rises, and one

Bank requires assistance. Fiscal stimulus does not have significant impact as

household consumption falls.

Ireland 2.0: International crisis overlaid on scenario 2, with QE and

lower rates, in response. May be from Europe (Brexit), China, or US, or some

combination as global growth falls. In response cash rate is cut hard to zero

bounds, QE in Australia commences, and banks are rescued/restructured via bail

in and bail out.

Iceland 2.0: As above, but no bank rescues, so banks fail. RBA moves to

negative interest rates (see Japan).

The AFR this week carried a story suggesting that over-valuation of

properties was widespread and were partly driven by real estate agents trying

to generate more revenue through advertising campaigns paid for by the vendor,

which then generate commissions and other incentives from advertising

companies. The higher the forecast price of a property the more is likely to be

spent on advertising. A lot of agents are losing money. The kickbacks help keep

their businesses running. This is something which our Property Insider Edwin

Almedia highlighted recently in our post “Breaking With Tradition”.

I was quoted in the article – “Martin North, principal of Digital

Finance Analytics, an independent consultancy, said discounts of more than 40

per cent were also being made in Victoria’s Red Hill, a leafy weekend retreat

about 82 kilometres south-east of Melbourne, and Sydney suburbs including Box

Hill and Agnes Banks. “Typically, in a downturn it’s the top end of the

market which dies first, and the decay in price spreads down the market like a

canker,” said Mr North. He estimated one-in-ten households were in

negative equity, where the value of the mortgage is bigger than the expected

realisable value of the property.

The AFR went on to say the falls are out-pacing predictions by major

lenders, such as Gareth Aird, senior economist for Commonwealth Bank of

Australia, the nation’s largest lender. Mr Aird said property prices will this

year fall by about 5 per cent in Sydney and 6 per cent in Melbourne. That would

take the fall in Sydney prices from their July 2017 peak to around 15 per cent

and 13 per cent in Melbourne. Mr Aird expects the national peak to trough falls

to be about 12 per cent. Good luck with that!

LF Economics report which we discussed in our post “Crisis – What Crisis?

The Latest On Home Prices” is more realistic, saying a

“bloodbath” is possible with falls this year in Melbourne and Sydney

– before allowing for inflation – of between 15 per cent and 20 per cent. This

could rise to 25 per cent if the finance and housing markets continue to

deteriorate. I discussed this on Seven

Sunrise and left Kochie all but speechless…. Its worth watching the video just for that!

And the IMF

reported on Australia this week.

Directors noted that although growth is expected to remain above trend

in the near term, a weaker global economic environment, high household debt,

and vulnerabilities in the housing sector could weigh on medium‑term growth.

Against this background, they highlighted the importance of maintaining

supportive macroeconomic policies to secure stronger demand momentum, address

macrofinancial risks, and boost long‑term productivity and potential growth.

Directors welcomed the authorities’ macroprudential interventions to

reduce credit risk and reinforce sound lending standards. They concurred that,

with high prices for residential real estate along with elevated household

debt, macroprudential policies should hold the course on the improved lending

standards and further strengthen bank resilience by refining the capital

adequacy framework. Directors also saw merit in expanding and strengthening the

macroprudential toolkit to allow for more flexible responses to financial

stability risks.

Directors underscored the need to remain vigilant about housing market

developments. They noted that while the housing market correction is helping

housing affordability, continued housing supply reforms remain critical for

broad affordability and to reduce macrofinancial vulnerabilities. Directors

generally encouraged the authorities to explore, where possible, alternative

and effective non‑discriminatory measures for buyers.

Or in other words, find ways to keep the housing bubble alive, despite

the risks. I see the hand of Treasury here! Also, it’s worth noting that the

Output Gap and Fiscal Balance for Australia is considerably worse that New

Zealand, with Australian net debt at 15%, worse than New Zealand, though better

than Canada or the UK. New Zealand has

generally had countercyclical fiscal policy, and this is reflected in the

evolution of its net debt to GDP ratio.

Australia is not dealing with either private debt or international debt,

though there is a little more attention on public debt. But this does not bode

well. All this in the context of rising global debt, which has reached another

new record.

And here is the killer slide. The

question to ask is why did prices take off around the year 2000. The answer is

stupid tax policy as Peter Costello halved the capital gains tax on property,

and with negative gearing led to a plain stupid rise as investors crowded into

the market. Of course the reverse will also be true, as investors are already

deserting the field, and Labor, if the win, trims the tax breaks, to get back

to a more normal housing market. Despite the pain, that would be a good thing,

but we still must deal with the legacy of debt. The words I quote before from the Bank of

England ring in my ears!

We have argued that the Royal Commission into Financial Services

Misconduct passed on the main reform area – structural separation. As Paul

Keeting, the architect of financial deregulation in the 1980’s said in the

Australian “The royal commissioner should have recommended — this conflict between

product and advice — be prohibited. This he monumentally failed to do. He

should have acted upon the examination and the evidence of these serious

conflicts of interest.”

But the torch has been picked up in the Senate, and a 3 month inquiry is

now in train. This is a golden opportunity to push hard at getting a better

structure for the sector. I discussed this with CEC’s Robbie Barwick see “Another Swipe At

Banking Supervision”. There

is a chance now to make a submission to the Senate Inquiry, and I encourage you

to do this – via the online submission process. And to assist, I will be

releasing a video in a few days with some key points and a how to…. We can

really make a difference.

Another issue, Broker remuneration continues to flare, as the industry

attempts to push back on the idea of replacing broker commissions with a fee

paid for by prospective borrowers. Now both sides of politics have gone coy on

this, citing competition -related issues. And this week Labour came out with

the idea of a scaled fee of 1.1% being paid for by the banks for mortgage

applications. That misses the point, because it still means a bigger loan

translate to a bigger payment to a broker, so conflict of interest would still

exist. Perhaps the best option would be a flat fee, paid by the bank, as, after

all the bank is outsourcing an element of its loan processing to the broker. Labor

has lost the plot here, but at least they still support best interests and the

removal of trail commissions.

Finally, home prices fell again according to Corelogic, taking the fall

from peak in Sydney to 13% and in Melbourne to 9.5%, and in Perth its 17.4%.

Auction clearance rates were still slightly higher than before Christmas, at

51.2% on 1,259 auctions, well down on last year. Sydney ended at 54.6% and

Melbourne at 52.5%. I continue to see accelerated weakness in Melbourne.

Nothing here is signal signs of a bounce, despite the spruikers. As McGrath put

it in their results release”

Economic factors are contributing to a significant reduction in

transaction volumes with settled sales for the reals estate sector nationally

down 13.2% and across the eastern seaboard Sydney is down 20.3% and Melbourne

down 22.3% and Brisbane down 11.3% on the 12 months to January 2019. This is

shown in their share price which is down 36.9% over the past year.

IN the US markets, te S&P 500 posted its highest closing level since

Nov. 8 on Friday as investors clung to signs of progress in the ongoing trade

talks between the United States and China. Investors assessed a slew of

headlines on the talks, with top trade negotiators from the two countries

meeting to wrap up a week of discussions on some of the thorniest issues in

their trade war. If the two sides fail to reach a deal by midnight on March 1,

then their seven-month trade war could escalate.

Optimism on the trade front and dovish signals from the U.S. Federal

Reserve have driven the recent gains and left indexes well above their lows of

December, when the market swooned on fears of an economic slowdown.

U.S. President Donald Trump was reportedly set to meet with China’s top

trade negotiator, Chinese Vice Premier Liu He, as the world’s two largest

economies scramble to reach a trade deal before the U.S. increases tariffs on

around $200 billion in Chinese imports on the March 1 deadline.

Markets have been closely following the standoff between China and the

U.S. amid concerns of the negative impact on the global economy and the meeting

between Trump and Liu is taken as a sign of progress in reaching a deal.

The S&P 500 is now up about 19 percent since its late-December low.

The S&P 500 technology index was up 1.3 percent, leading gains among

the 11 major S&P sectors, while the trade-exposed industrials index climbed

0.6 percent.

The Dow Jones Industrial Average rose 181.18 points, or 0.7 percent, to

26,031.81, the S&P 500 gained 17.79 points, or 0.64 percent, to 2,792.67

and the Nasdaq Composite added 67.84 points, or 0.91 percent, to 7,527.55.

All three indexes registered gains for the week, with both the Dow and

Nasdaq posting a ninth week of increases.

Oil prices headed higher on Friday, on track for a second consecutive

weekly rise, as progress in U.S.-China trade talks adjusted expectations for

global demand higher in the hope of a deal. Evidence that trade tensions

between the world’s two largest economies may be thawing, together with

OPEC-led production cuts, have translated into a rally of more than 20% this

year, though concerns remain over surging U.S. production. The Energy

Information Administration reported Thursday that weekly production stateside

hit a record high of 12.0 million barrels per day.

European Union Trade Commissioner Cecilia Malmstrom said Friday that a

trans-Atlantic trade deal could be achieved before year-end, as the economic

bloc hopes to avoid the threat of U.S. automotive tariffs. The U.S. and Europe

ended a stand-off of several months last July, when Trump agreed to hold off on

car tariffs while the two sides looked to improve trade ties

So, the housing sector continues to look weak, and credit remains tight.

The Financial Crisis is so close now, you can almost smell it.

In fact you can get a

nice overview over at Nuggets News. I provided several comments to the show,

alongside Roger Montgomery, entitled “Australia A Coming Financial Crisis”. I will put a link in the comments. Here is a

flavour. It’s a good reflective piece,

Alex did a great job putting it together.