Bank of Ireland has caved in to public pressure following a public outcry over its plans to heavily restrict cash transactions in its branches, via Irish Independent.

The bank came in for sustained criticism

after the Irish Independent revealed yesterday that it plans to restrict

over-the-counter cash withdrawals to a minimum of €700 and cash

lodgements to a minimum of €3,000 in an effort to push customers towards

using ATMs and self-service machines.

However, after criticism from Finance

Minister Michael Noonan, as well as groups representing consumers,

farmers, older people, rural dwellers and bank workers, the bank

conceded that what it called “vulnerable” customers could continue to

get cash and make withdrawals of smaller amounts of money at branch

counters.

The changes prompted fears of a renewed

bout of bank branch closures and staff lay-offs in the wake of the

bank’s move to severely restrict counter-based cash transactions.

Mr Noonan described the changes as

“surprising and unnecessary”, adding that he expects the bank to “fully

honour” its commitment to “vulnerable customers”.

Bank of Ireland said it would continue to

allow older customers and those unfamiliar with technology to make cash

transactions over the counter.

“Bank of Ireland would like to confirm

that vulnerable customers, together with those elderly customers who are

not comfortable using self-service channels or other technology

solutions, will be assisted by branch staff to use the available

in-branch services.”

However, other banks are now expected to

follow the lead of Bank of Ireland by moving to set strict limits on

over-the-counter cash handling.

It comes after around 200 bank branches

were closed, mainly in rural areas, during the financial collapse, with

at least 10,000 retail bank staff laid-off.

Banks including Bank of Scotland, Danske, ACC and Irish Nationwide have already closed, limiting banking options for customers.

Now there are concerns that the move by

Bank of Ireland to effectively become a cashless bank will prompt more

branch shut-downs and redundancies.

Deputy chairman of the Consumers

Association Michael Kilcoyne said other banks were set to mirror Bank of

Ireland and discourage customers from withdrawing and lodging cash over

the counter.

This would make branches in rural areas less viable, he warned.

“The implications of the Bank of Ireland

move are very severe. If it gets away with this it will get rid of more

staff and close branches.

“This will be a further blow for rural Ireland,” he said.

Mr Kilcoyne predicted that AIB, Ulster Bank and Permanent TSB would make similar moves to curtail cash handling.

And banking union IBOA said it is seeking a

meeting with Bank of Ireland boss Richie Boucher over concerns the

changes would mean more job losses.

The Irish Farmers’ Association said the

changes would cause great difficulty for some farmers who are not

familiar with the bank’s online system.

Age Action accused the bank of ignoring the needs of older people by setting high limits on over-the-counter transactions.

Governor Lowe spoke at the Australian Payments Network Summityesterday. He discussed the rise of electronic transactions, especially though the New Payments Platform, the high relative costs of international retail payments, and the need for, and potential of a Strong Digital Identity System. He also highlighted the decline in cash transactions which now accounts for just around a quarter of day-to-day payments.

A recurring theme across these summits has been the need to improve customer outcomes. I am very pleased to see that this focus has been continued at this year’s summit. The focus on customer outcomes aligns very closely with the focus of the Payments System Board. The Board wants to see a payments system that is innovative, dynamic, secure, competitive, and that serves the needs of all Australians.

Increasingly, this means that the payments system needs to support Australia’s digital economy.

With the digital economy being an important key to Australia’s future economic prosperity, we need

a payments system that is fit for purpose. We will only fully capitalise on the fantastic opportunities

out there if we have a payments system that works for the digital economy. The positive news is that we

have made some substantial progress in this direction over recent years and in some areas,

Australia’s payments system is world class. However, in the fast-moving world of payments, things

don’t stand still and there are some important areas we need to work on.

In my remarks today, I would like to do three things.

The first is to talk about some of the progress that has been made over recent years.

The second is to highlight a few areas where we would like to see more progress, particularly around

payments and the digital economy.

And third, I will highlight some of the questions we will explore in next year’s review of retail

payments regulation in Australia.

Progress Is Being Made

Over recent years there have been significant changes in the way that we make payments. We now have

greater choice than ever before and payments are faster and more flexible than they used to be.

The launch of the New Payments Platform – the NPP – in early 2018 has been an important

part of this journey. This new payments infrastructure allows consumers and businesses to make

real-time, 24/7 payments with richer data and simple addressing using

PayIDs.

After the NPP was launched, it got off to a slow start, but it is now hitting its stride. Monthly

transaction values and volumes have both tripled over the past year (Graph 1). In November, the

platform processed an average of 1.1 million payments each day, worth about $1.1 billion. The

rate of take-up of fast retail payments in Australia is a little quicker than that in most other

countries that have also introduced fast payments (Graph 2).

Graph 1

Graph 2

I expect that we will see a further pickup in usage once the CBA has delivered on core NPP

functionality for all its customers. The slow implementation has been disappointing and we expect the

required functionality to be available soon.

There are now 86 entities connected to the NPP, including 74 that are indirectly connected

via a direct NPP participant. There are at least six non-ADI fintechs that are using the NPP’s

capabilities to innovate and provide new services to customers. All up, approximately 66 million

Australian bank accounts are now able to make and receive NPP payments.

Use of the PayID service has also been growing, with around 3.8 million PayIDs having been

registered to date. If you have not already got a PayID, I encourage you to get one. I also encourage

you to ask for other people’s PayIDs when making payments, as an alternative to asking for their

BSB and account number. It is much easier and faster.

One specific example of where the NPP is bringing direct benefits to people is its use by the

Australian Government, supported by the banking arm of the RBA, to make emergency payments. During the

current bushfires, the government has been able to use the NPP to make immediate payments to people at a

time when they are most in need, whether that be on the weekend or after their bank has shut for the

night.

One other area of the payments system where we have seen significant change is the take-up of

‘tap-and-go’ payments. Around 80 per cent of point-of-sale transactions are now

‘tap-and-go’, which is a much higher share than in most other countries. This growth has

been made possible by the acquirers rolling out new technology in their terminals and by the willingness

of Australians to try something different. There has also been rapid take-up of mobile payments,

including through wearable devices.

Progress has also been made on improving the safety of electronic payments, particularly in relation to

fraud in card-not-present transactions. The rate of fraud is still too high, but it has come down

recently (Graph 3). I would like to acknowledge the work that AusPayNet has done here to develop a

new framework to tackle fraud. This framework strengthens the authentication requirements for certain

types of transactions, including through the use of multi-factor authentication.[1] This will

help reduce card-not-present fraud and support the continued growth in online commerce.

Graph 3

As our electronic payments system continues to improve, we are seeing a further shift away from cash

and cheques. The RBA recently undertook the latest wave of our three-yearly consumer payments survey. We

are still processing the results, but ahead of publishing them early next year, I thought I would show

you the latest estimate on the use of cash (Graph 4). As expected, there has been a further trend

decline in the use of cash, with cash now accounting for just around a quarter of day-to-day

transactions, and most of these are for small-value payments. Given the other innovations that I just

spoke about, I expect that this trend will continue.

Graph 4

Further Progress Needed

The progress across these various fronts means that there is a positive story to be told about

innovation in Australia’s payments system.

At the same time, though, there are still some significant gaps and areas in our payments system that

need addressing and where progress would support the digital economy in Australia. I would like to talk

about four of these.

NPP

The first of these is further industry work to realise the full potential of the NPP, including its

data-rich capabilities.

The NPP infrastructure can help make electronic invoicing commonplace and help invoices be paid on

time. It can also support significant improvement in business processes, as more data moves with the

payment. Real-time settlement and posting of funds also enables some types of delivery-versus-payment,

so that the seller can confirm receipt of funds and be confident in delivering goods or services to the

buyer.

The layered architecture of the system was designed to promote competition and innovation in the

development of new overlay services. Notwithstanding this, one of the consequences of the

slower-than-promised rollout of the NPP by some of the major banks is that there has been less effort

than expected on developing innovative functionality. Payment systems are networks, and participants

need to know that others will be ready to receive payments and use the network. Some banks have been

reluctant to commit time and funding to support the development of new functionality given that others

have been slow to roll out their ‘day 1’ functionality. The slow rollout has also reduced

the incentive for fintechs and others to develop new ideas. So we have not yet benefited from the full

network effects.

The Payments System Board considered this issue as part of its industry consultation on NPP access and

functionality, conducted with the ACCC earlier this year. As part of that review we recommended that

NPPA – the industry-owned company formed to establish and operate the NPP – publish a

roadmap and timeline for the additional functionality that it has agreed to develop. The inaugural

roadmap was published in October and NPPA also introduced a ‘mandatory compliance

framework’. Under this compliance framework, NPPA can designate core capabilities that NPP

participants must support within a specified period of time, with penalties for non-compliance. This is

a welcome development.

One important element of the roadmap is the development of a ‘mandated payments service’

to support recurring and ‘debit-like’ payments. This new service will allow

account-holders to establish and manage standing authorisations (or consents) for payments to be

initiated from their account by third parties. This will provide convenience, transparency and security

for recurring or subscription-type payments and a range of other payments.

Another element of the roadmap that has the potential to promote the digital economy is the development

of NPP message standards for payroll, tax, superannuation and e-invoicing payments. The standards will

define the specific data elements that must be included with these payment types, which will support

automation and straight-through processing. We would expect financial institutions to be competing with

each other to enable their customers to make and receive these data-rich payments.

Less positively, there is still uncertainty about the future of the two remaining services that were

expected to be part of the initial suite of Osko overlay services. These are the

‘request-to-pay’ and ‘payment with document’ services. We understand there

are still challenges in securing committed project funding and priority from NPP participants to move

ahead, even though BPAY has indicated it is ready to complete the rollout. The RBA strongly supports the

development of these additional NPP capabilities, which are likely to deliver significant value for

businesses and the broader community.

Digital identity

A second area where the Payments System Board would like to see further progress is the provision of

portable digital identity services that allow Australians to securely prove who they are in the digital

environment.

Today, our digital identity system is fragmented and siloed, which has resulted in a proliferation of

identity credentials and passwords. This gives rise to security vulnerabilities and creates significant

inconvenience and inefficiencies, which can undermine development of the digital economy. These generate

compliance risks and other costs for financial institutions, so it is strongly in their interests to

make progress here. It is fair to say that a number of other countries are well ahead of us in this

area.

The Australian Payments Council has recognised the importance of this issue and has developed the

‘TrustID’ framework. The Government’s Digital Transformation Agency has also been

working on a complementary framework (the Trusted Digital Identity Framework), which specifies how

digital identity services will be used to access online government services. The challenge now is to

build on these frameworks and develop a strong digital identity ecosystem in Australia with competing

but interoperable digital identity services.

The rollout of open banking and the consumer data right should bring additional competition among

financial services providers, and digital identity is likely to reduce the scope for identity fraud,

while providing convenient authentication, as part of an open banking regime.

A strong digital identity system would also open up new areas of digital commerce and help reduce

online payments fraud. It will also help build trust in a wide range of online interactions. Building

this trust is increasingly important as people spend more of their time and money online. So we would

like to see some concrete solutions developed and adopted here.

Cross-border retail payments

A third area where we would like to see more progress is on reducing the cost of cross-border

payments.

For many people, the costs here are still too high and the payments are still too hard to make. It is

important that we address this. It is an issue not just for Australians, but for our neighbours as well.

I recently chaired a meeting of the Governors from the South Pacific central banks, where I heard

first-hand about the problems caused by the high cost of cross-border payments.

Analysis by the World Bank indicates that the price of sending money from Australia has been

consistently higher than the average price across the G20 countries (Graph 5). And a recent

ACCC inquiry found that prices for cross-border retail payment services are opaque. Customers are not

always aware of how the ‘retail’ exchange rate they are being quoted compares with the

wholesale exchange rate they see on the news, or of the final amount that will be received in foreign

currency.[2] There are also sometimes add-on fees.[3]

Graph 5

As part of the RBA’s monitoring of the marketplace, our staff recently conducted a form of online

shadow shopping exercise, exploring the pricing of international money transfer services by both banks

and some of the new non-bank digital money transfer operators (MTOs).

This exercise showed that there is a very wide range of prices across providers and highlighted the

importance of shopping around.

The main results are summarised in this graph (Graph 6). In nearly every case, the major banks are

more expensive than the digital MTOs. For the major banks, the average mark-up over the wholesale

exchange rate is around 5½ per cent, versus about 1 per cent for the digital

MTOs.

Graph 6

The graph illustrates why the cost of cross-border payments is such an issue for the South Pacific

countries. These costs are noticeably higher than for payments to most other countries. This is a

particular problem as many people in the South Pacific rely on receiving remittances from family and

friends in Australia and New Zealand. In many cases, low-income people are paying very high fees and it

is important that we address this where we can. As is evident from the graph, most digital MTOs do not

service the smaller South Pacific economies, which limits customers’ choice of providers.

In part, the high costs – and slow speed – of international money transfers is the result

of inefficiencies in the traditional correspondent banking process. It is understandable why some large

tech firms operating across borders see an opportunity here. Where people are being served poorly by

existing arrangements, new solutions are likely to emerge with new technologies. This represents a

challenge to the traditional financial institutions to offer better service at a lower cost to their

customers, while still meeting their AML/CTF requirements.

Central banks have a role to play here too, and there is an increased focus globally on what we can do

to reduce the cost of cross-border payments. One example of this is the promotion of standardised and

richer payment messaging globally through the adoption of the ISO20022 standard. The RBA is also working

closely with the Reserve Bank of New Zealand, AUSTRAC and other South Pacific central banks to develop a

regional framework to address the Know-Your-Customer concerns that have limited competition and kept

prices high.

Operational resilience

A fourth area where we would like to see more progress is improving the operational resilience of the

electronic payments system.[4]

Disruptions to retail payments hurt both consumers and businesses. Given that many people now carry

little or no cash, the reliability of electronic payment services has become critical to the smooth

functioning of our economy.

We understand that, given the complexity of IT systems, some level of payments incidents and outages to

services is inevitable. But it is apparent from the data we have that the frequency and duration of

retail payments outages have risen sharply in recent years. In response, the RBA has begun working with

APRA and the industry to enhance the data on retail payment service outages and to introduce a suitable

disclosure framework for these data. These measures will provide greater transparency around the

reliability of services and allow institutions to better benchmark their operational performance.

The 2020 Review of Retail Payments Regulation

The third and final issue I would like to touch on is the Payments System Board’s review of retail

payments regulation next year.

The review is intended to be wide-ranging and to cover all aspects of the retail payments landscape,

not just the RBA’s existing cards regulation. As the first step in the process, we released an

Issues Paper a couple of weeks ago and have asked for submissions by 31 January.[5] There will

also be opportunities to meet with RBA staff conducting the review.

The review will cover a lot of ground, including hopefully some of the issues that I just mentioned.

There are, though, a few other questions I would like to highlight.

The first is what can be done to reduce further the cost of electronic payments?

Both the Productivity Commission and the Black Economy Taskforce have called for us to examine this

question. It is understandable why. As we move to a predominantly electronic world, the cost of

electronic payments becomes a bigger issue. The Payments System Board’s regulation of interchange

fees and the surcharging framework, as well as its efforts to promote competition and encourage

least-cost routing, have all helped lower payment costs.

At issue is how we make further progress: what combination of regulation and market forces will best

deliver this? Relevant questions here include: whether interchange fees should be lowered further; how

best to ensure that merchants can choose the payment rails that give them the best value for money; and

whether restrictions relating to no-surcharge rules should be applied to other arrangements, including

the buy-now-pay-later schemes.

A second issue is what is the future of the cheque system?

Cheque use in Australia has been in sharp decline for some time. Over the past year, the number of

cheques written has fallen by another 19 per cent and the value of cheques written has fallen

by more than 30 per cent, as the real estate industry has continued to shift to electronic

property settlements (Graph 7). At some point it will be appropriate to wind up the cheque system,

and that point is getting closer. Before this happens, though, it is important that alternative payment

methods are available for those who rely on cheques. Using the NPP infrastructure for new payment

solutions is likely to help here.

Graph 7

Third, is there a case for some rationalisation of Australia’s three domestically focused payment

schemes, namely BPAY, eftpos and NPPA? A number of industry participants have indicated to us that they

face significant and sometimes conflicting investment demands from the three different entities. This

raises the question of whether some consolidation or some form of coordination of investment priorities

might be in the public interest.

Fourth, and finally, what are the implications for the regulatory framework of technology changes, new

entrants and new business models?

The world of payments is moving quickly, with new technologies and new players offering solutions to

longstanding problems. At the same time, expectations regarding security, resilience, functionality and

privacy are continually rising. Meeting these expectations can be challenging, but doing so is critical

to building and maintaining the trust that lies at the heart of effective payment systems. The entry of

non-financial firms into the payments market also raises new regulatory issues. As part of the review,

it would be good to hear how the regulatory system can best encourage a dynamic and innovative payments

system in Australia that fully serves the needs of its customers.

As the country continues its inexorable march towards a cashless society, it’s important to remember the downsides. Via The Adviser.

Australia

has been just a few years away from being a cashless society for a

couple of decades now, but it will eventually get there. Legislation

currently before the Senate aims to ban transactions over $10,000 in a

bid to hinder the black economy. From there, it’s not difficult to

imagine that the ubiquity of digital payment systems – and efforts the

by government – will see hard cash disappear at some point in the

future.

One of the supposed benefits of a cashless society is

that it cuts down on crime, the logic being that if there’s less cash to

steal, less cash is stolen. Laundering dirty money is also harder, as

every transaction is logged in some form or another.

But a cashless society comes with a number of negatives that might well outweigh the positives.

“As

payments move online, there would be an increased risk of crimes such

as identity theft, account takeover, fraudulent transactions and data

breaches, due to the higher volume of cashless transactions and more

points of exposure for the average consumer,” Dr Richard Harmon,

managing director of financial services at Cloudera, told Investor

Daily.

“Hackers

and other criminals now have new ways to get access to accounts and to

potentially set up synthetic accounts to facilitate more sophisticated

money laundering activities.”

And that’s just the risk posed by hackers. According to the UK’s access to cash report, a cashless society could heighten the risks of financial abuse. Elderly people, who might lack understanding of digital technology, would be particularly vulnerable. Couples with joint bank accounts are also at risk – money can be tracked and controlled by one person. These issues are already of great concern, but they’d be even worse in a cashless society.

That’s

not to mention that digital systems rely on topnotch digital

infrastructure, something that Australia doesn’t exactly have in spades.

That infrastructure also has to be more or less impervious to cyber

attacks, which may be carried out by state-sponsored actors with an

interest in crippling a country’s entire financial system. In the face

of that existential threat to the economy, a little bit of money

laundering doesn’t seem so bad.

A cashless society could also

make things worse for workers and the most vulnerable. It’s only a short

jump from cashless to “cashier-less”, and a cashless society would have

to deal with an explosion of unemployed low-skill individuals.

Meanwhile, those who lack access to banks – or prefer not to use them – are also at risk.

“Let

me highlight that one of the concerns about becoming a cashless society

– at least as we transition into this state – is the ability for the

underbanked or unbanked to have sufficient access to function properly

as they would within a cash-based system,” Dr Harmon said.

“This would be a key concern from a societal perspective.”

The

idea of a cashless society is promising. But hidden in that promise are

a number of caveats that any country – let alone Australia – would be

foolish to ignore.

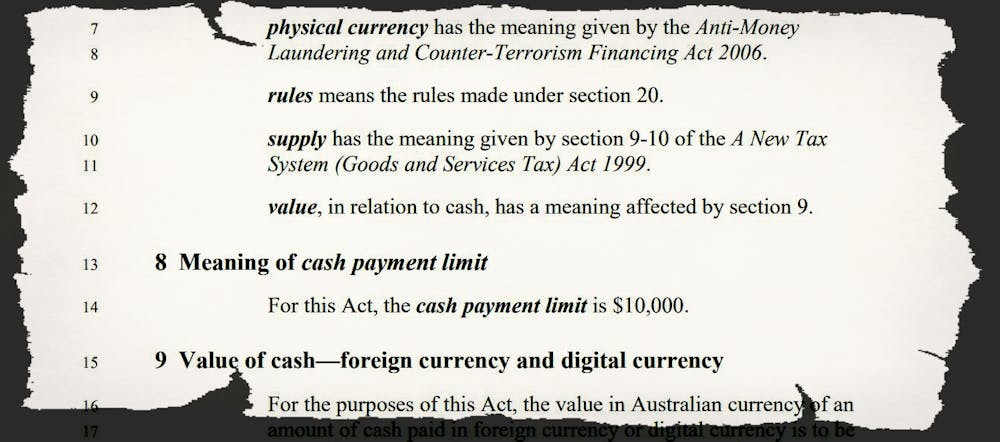

This Act places restrictions on the use of cash or cash-like products

within the Australian economy. The Act imposes criminal offences if an

entity makes or accepts cash payments in circumstances that breach the

restrictions.

The proposed limit is A$10,000. Section 8 would make it an offence to make or accept cash payments of $10,000 occurring either as one-offs or in a linked sequence.

In parliament the minister said the $10,000 limit would not apply to

person-to-person transactions, such as private sales of cars.

But these exceptions are not included in the the Bill. What is

included is the phrase “specified by the rules”. Section 20 puts those

rules in the minister’s hands. Future ministers may narrow exceptions

and change rules.

It would remain legal to withdraw and hold more than $10,000. The stated intent of this Bill is to modify the use of cash, not the holding of cash.

All Australians will continue to be able to deposit and withdraw cash

in excess of $10,000 into and from their accounts, and to store more

than $10,000 of their money outside a bank.

Cash overboard

What’s proposed would limit competition (Visa, Mastercard, and PayPal would face a lesser competitor, for example) and limit long-held rights.

Everyday behaviour at present protected by the law would be criminalised.

In some cases, and perhaps many, the onus of proof would be reversed, with an “evidential burden” imposed on cash-using defendants.

Each partner in a partnership, each committee member of an

incorporated association and each trustee of a trust or superannuation

fund might become individually culpable for their entity’s use of cash.

Oddly, “bodies corporate and bodies politic” are treated differently

(Part 3), and the government itself cannot be prosecuted, an uneven

application of the law which has attracted little attention.

In my submission to the Senate inquiry (Submission 146) I argue the provisions would, among other things:

undercut the ability of banks to head off a banking crisis by providing a trusted and useful form of money

funnel more financial traffic through the equivalent of private toll roads

remove a guaranteed and always available fallback from electronic transactions

increase societal ill-ease and polarisation as citizens realise

their rights have been eroded for not particularly compelling stated

reasons.

Each point and many presented in other submissions need serious consideration, including in public Senate hearings.

The rationale presented

The speech to parliament introducing the bill was built around the hardly-new observation that cash payments can be “anonymous and untraceable”.

The government’s Black Economy Taskforce produced no detailed analysis but recommended the ban as a means of fighting tax avoidance, to:

make it more difficult to under-report income or charge lower prices and not remit good and services tax.

The speech also asserted that “more crucially”

the ban

would fight organised crime syndicates, although organised crime was not

mentioned in the part of the taskforce report that dealt with the

problem the limit was meant to address.

The guarantee dishonoured

Every pound note and then every dollar note issued by the

Commonwealth Bank and then Reserve Bank of Australia bears this

unconditional promise signed by the head of the bank and the head of the

treasury:

This Australian note is legal tender throughout Australia and its territories.

The bank’s website suggests the promise is ongoing:

All previous issues of Australian banknotes retain their legal tender status.

Its note printing arm was mortified earlier this year at the apparently accidental omission of the last letter “i” from the word “responsibility” on the new more secure $50 note.

The Bill before the Senate contains many and much more serious errors.

Cash has been one of the few things we can absolutely rely on,

whatever our status, situation or access to other payment means.

Removing (and dishonouring) that guarantee, while criminalising

reliance on it, should not be done lightly in a mad rush to an arbitrary

date.

Until now public debate about the proposal has been light, but concern is growing, even among quiet Australians.

Each Senator should ensure that last “i” in responsibility isn’t missing here either.

Author: Mark McGovern, Visiting Fellow, QUT Business School, Economics and Finance, Queensland University of Technology

The Victorian Liberal Party held their state council meeting in Ballarat where a motion was put forward calling on the Government to abandon their $10,000 cash transaction ban policy.

We discuss the implications of this move, with Steve Holland who is a member of the Victorian Liberal Party and who moved the motion at the State Council Meeting.

Afterpay breached money laundering law because of incorrect legal advice, according to an auditor. Via InvestorDaily.

The

buy-now, pay-later giant was the subject of an AUSTRAC probe over

allegations it breached the Anti-Money Laundering and Counter-Terrorism

Financing Act (AML/CTF).

But an independent auditor contracted by Afterpay has discovered that the breaches occurred because of incorrect legal advice.

“In

reaching these findings I have established that Afterpay’s compliance

with its AML/CTF obligations was, from the outset and over time, based

upon legal advice from top tier Australian law firms,” wrote Neil Jeans,

an anti-money laundering consultant who conducted the audit.

“I am of the opinion this initial legal advice was incorrect.”

The

unnamed law firms decided Afterpay was not providing loans to consumers

but instead providing factoring services to merchants. This advice “did

not reflect Afterpay’s business model” and led to the company focusing

its AML/CTF controls upon merchants rather than consumers.

“Despite

Afterpay having a compliance-focused culture, the consequences of being

provided with incorrect legal advice has resulted in historic

non-compliance with the AML/CTF Act and Rules,” Mr Jeans wrote in the

report.

However, the audit noted that Afterpay’s transaction

monitoring system is now “effective, efficient and intelligent” as a

result of greater resource allocation.

Mr Jeans also decided that

the nature of Afterpay’s service mitigates some money laundering and

terrorism financing risks, and noted that the company’s AML/CTF

compliance had “evolved and matured over time”.

Afterpay was quick to seize on the opportunities of the report in light of Westpac’s recent breaches of the same laws.

“Afterpay

reaffirms that it has not identified any money laundering or terrorism

financing activity via our systems to date,” the company said in a

statement accompanying the report.

But the ball is now in AUSTRAC’s court. The regulator will consider the report and decide whether to take further action.

Afterpay has pledged to continue its co-operation with AUSTRAC.

Currency (Restrictions on the Use of

Cash) Bill 2019

I have carefully reviewed the latest iteration of this legislation

and am gratified that the Senate has chosen to review the proposals, which I strongly

oppose.

Not only is the bill significantly eroding our civil

liberties, but the conduct of Treasury needs to be called out by suggesting

that 3,400 of the 3,500 submission they received during their brief 2 week

exposure review submission period were part of a campaign “by the CEC, a

political party”. While there was indeed a campaign to oppose the draft

legislation, I have evidence that submissions were made by many concerned

individuals and businesses with no links to the CEC. Indeed, my own submission,

some of the contents I am using here again, is based on my own independent

research and analysis. I have no

financial or political association with said CEC. I believe Treasury tried to

play down the considerable opposition which exists within the community. This

bill is, in my view toxic.

Digital Finance Analytics is a boutique research and analysis firm specialising in the financial service sector. We undertake primary research through our surveys, as well as deep research from the global literature relating to financial services. We publish regularly via our online channels at Digital Finance Analytics[1] as well as preparing reports on a range of related subject matters for our clients, and we collaborate with a number of academics.

My objections are centred around the following points.

Civil Liberties Are Being Eroded. Further public debate on these measures are warranted as they are fundamentally restricting personal freedoms. Today I can use and hold cash as I please. If passed, my freedom will be eroded. This is one in a series of measures which have been taken (including media freedoms) which are curtailing the hard-won freedoms Australians used to enjoy. Public hearings should be held by the Senate to judge community reactions to the bill as part of the current review.

There Is No Cost Benefit. The stated objective of the bill is to close tax avoidance and money laundering loopholes. But there is no quantification of the potential “savings” – and this is also true of the earlier Black Economy Taskforce report. It appears that simply stating these desired objectives is seen as sufficient to justify the bill. What is the cost benefit of such a measure, bearing in mind that transactions which fall outside the exemptions would need to be tracked and examined?

Increased Surveillance Will Be Required.

In some form, monitoring of offending transactions would be required if the

Bill were passed. This is not explained,

nor how it would be policed. Who would police them, at what cost? Further, the bill proposed a draconian set of

penalties designed to deter. Treasury admitted this in their FOI’d response.

Existing Laws Are Not Enforced. The true

size of the black economy is much in dispute, but indications are that it is

already falling. In addition, much of the tax leakage and avoidance would be

covered by existing legalisation if it were being policed effectively. We

support the view, recently aired by Andrew Wilkie in the debate on the floor of

the house, that:

“There’s already a requirement

to report transactions over $10,000. The problem is that those laws are not

being implemented and enforced[2].”

There are other more pressing areas of tax

leakage and AML risk. According to the OECD report “Implementing The OECD

Anti-Bribery Convention” released as part of the OECD Working Group on Bribery,

Real Estate is identified as at “significant risk” of being used for money

laundering. Among a raft of recommendations, is one saying Australia should be

“Taking urgent steps to address the risk that the proceeds of foreign bribery

could be laundered through the Australian real estate sector. These should

include specific measures to ensure that, in line with the FATF standards, the

Australian financial system is not the sole gatekeeper for such transactions”. To date these loopholes, remain open, as do those

relating the corporates and big business who, partly thanks to the assistance

of the large international accounting firms are responsible for the lions share

of tax leakage and AML activity. Our research suggests that Government, under

heavy corporate and business lobbying is deliberately letting this slide,

preferring to target in on a relatively inconsequential area of tax leakage

relating to cash transactions.

The Legislation Would Be Ineffective. Beyond

that, it is clear from our wider research of a range of sources that such a

proposed cash ban would have very little impact on hard core tax leakage. For example,

Professor Fredrich Schneider, a research fellow at the Institute of Labor

Economics at the University of Linz, Austria, a leading international expert on

the black economy has stated that there is a lack of empirical evidence that

cash transaction bans will help reduce the black economy. Schneider published a

paper in 2017[3] “Restricting or Abolishing Cash: An Effective

Instrument for Fighting the Shadow Economy, Crime and Terrorism” in which he

made this specific point.

There Is Another Agenda. In addition, while the Bill is silent on the connection to implementing negative interest rates as part of unconventional policy, the link was made clearly in the 2016 Geneva Report by the International Centre Monetary and Banking Studies (ICBM) titled: What else can Central Banks do?[4] This paper which was drafted by officials from international organisations such as the IMF/BIS and multiple central banks + commercial banks. In addition, within the original Black Economy Taskforce Report there was mention of the benefits of a cash transaction ban in relationship to monetary policy – yet this link was denied by Treasury in their recent FOI release.

The IMF Shows Why. The same thematic came through in recent IMF Blogs and working papers. In April 2019, the IMF published a new working paper on how deeply negative interest rates work. In previous papers, the IMF has suggested that nominal interest rates may have to go deeply negative, for example, -3% – 4%. First, they say “In summary, ten years after the crisis, it is clear that the zero-lower bound on interest rates has proved to be a serious obstacle for monetary policy. However, the zero lower bound is not a law of nature; it is a policy choice. We show that with readily available tools a central bank can enable deep negative rates whenever needed—thus maintaining the power of monetary policy in the future.” Next they declare “Our view is that, when needed, deep negative rates are likely to be worth the political cost. While the complete abolition of paper currency would indeed clear the way for deep negative interest rates whenever deep negative rates were called for, such proposals remain difficult to implement since they involve a drastic change in the way people transact.”

The Bill Is Connected to Negative Interest

Rates. The connection is obvious in that in a negative interest rate

environment households and businesses will be likely to withdraw funds from the

banking system and transact in cash. If enough cash is extracted, negative

interest rates will simply have no effect. We believe the measures proposed in

the current Bill are truly about enabling negative rates, yet this is not

mentioned within the Bill. This is misleading and deceptive. The true

motivations should be on the record. But it explains the short time frames.

Households and Businesses Would Be Trapped In The Banking System. If such a ban was introduced households and businesses would be forced to use the banking system, meaning that bank charges could not be avoided, which benefits banks, not their customers. In addition, we have seen recent system and power failures which have caused disruption to the electronic payments systems. If cash is less available and restricted, a failure would be even more significant and inconvenient and could damage the economy. Once in the banking system, funds can be monitored and controlled (seen by the Taskforce as a positive move – we disagree), but such control could limit access to cash and transactions in general in a crisis. And we note from our SME surveys that many businesses, especially in rural and regional Australia regularly use cash as electronic alternatives are not available. Finally, offering cash for a discount, which is part of legitimate everyday business (because bank charges are avoided) would be removed.

The Structure Allows Change by Regulation Subsequently. The structure of the Bill enables parameters to be changed subsequently by regulation (not via Parliament). This opens the door to removing some of the concessions contained in the current drafting by agencies without full scrutiny. The bill is therefore open ended with regards to crypto, precious metals and other carveouts. In addition, we note surprisingly, government transactions, and cash transactions in Casinos are carved out, which again flags concerns about the structure and limitations of the bill.

A Reduced Limit Could Be Waived Through. Whilst we note that the $10,000 limit would require Parliamentary approval, in practice this could be made without full debate – as illustrated by the passage on the recent APRA bill, or as part of an omnibus “procedural” bill which masks the true intent. It is important to note that where cash transaction bans have been introduced, the value ceiling has been lowered. France has legally prohibited cash transactions above 1,000 euros, Spain has legally prohibited cash transactions above 2,500 euros, Italy has legally prohibited cash transactions above 3,000 euros, and the European Central Bank ended the production and issuance of its 500 euro note at the end of 2018.

In summary, my overriding concern is that Parliamentarians

will only consider the narrow tax efficiency aspect of the Bill and vote it

through without grasping the true intent and consequences. Civil liberties are

being eroded, and the trap will be set to force households and businesses to

transact within the banking system, thus facilitating experimental monetary

policies, via the back door.

It would be nice if the “facts” being thrown around in the debate over the Cashless Debit Card were peer-reviewed, or even just evidence-based. Via The Conversation.

Instead, there are anecdotes. And it’s these that are being used to justify the government’s decision to spend A$128.8 million

over four years continuing the existing trial of the cashless debit

card in five sites in Western Australia, Queensland and South Australia

and extending it to Cape York and all of the Northern Territory.

The cashless card was recommended to Prime Minister Tony Abbott in a report from mining billionaire Andrew Forrest in 2014. He initially called it the “Healthy Welfare Card”.

It wasn’t a new idea. Some A$1 billion dollars had already been spent

on income management programs in the past, many of which had failed to meet their stated objectives.

The biggest was the Basics Card introduced as part of the 2007 Northern Territory Emergency Response (the “Intervention”) which was only made possible through the suspension of the Racial Discrimination Act.

Research published by the Australian Research Council funded Life Course Centre of Excellence found its introduction was correlated with negative impacts on children, including reductions in birth weight and school attendance.

It points to several possible explanations, including increased

stress on mothers, disrupted financial arrangements within households,

and confusion about how to access funds.

The government has not addressed these serious issues. Instead, it

now seeks to place those who have been left on the basics card for over

ten years now, on to the cashless debit card.

What was ‘Basics’ has become ‘Indue’

The 2016 Indue Cashless Debit Card.

indue.com.au

The “Indue” Cashless Debit Card trials underway since 2016 direct 80% of each payment to the card (Forrest asked for 100%)

where it can only be spent on things such as food, clothes, health

items and hygiene products. Purchases of alcohol and withdrawals of cash

are not permitted.

The trials are compulsorily for everyone living in the trial sites

receiving a disability, parenting, carer, unemployment or youth

allowance payment.

My own research in the East Kimberley found it makes those people’s lives harder.

Those targeted are a broad group needing support for a broad range of

reasons, yet all are treated as if they have issues with alcohol or

drugs or gambling.

Most of the people on it do indeed have a common problem: that is

trying to survive on meagre payments in remote environments with a

chronically low supply of jobs.

Of all the claims made for the card, the least believable is that it gets its users into jobs.

What it does do is limit access to cash needed for day to day-to-day

living. It makes it hard to buy second-hand goods, transport and (at

some outlets) food, and can make living more expensive.

For anyone actually struggling with addiction, it can’t substitute for treatment, a concern raised by medical specialists.

While the government says the trials have been community-led, in

reality consultation has been limited to a small group of people not

subject to the card.

When leaders in the East Kimberley who had agreed to the card withdrew their support, the government continued with the trial.

Profiting from the Cashless Debit Card has been Indue, a private company whose deputy chairman up until 2013 is now the present President of the National Party, Larry Anthony.

Indue’s involvement is helping to create a two tiered banking system

in which most people have a choice of financial providers, but those

subject to the card are restricted to one, which provides a very

different product to the others.

Indue is also not a member of the Australian Banking Association, and

so is not bound by the consumer protection provisions of its Banking Code of Practice.

The inquiry is due to report next week. Given the expensive and harmful consequences of the trial, it ought to find the extension is not justified. There are better ways to spend $128.8 million that would actually help vulnerable Australians.

Author: Elise Klein (OAM), Senior Lecturer in Development Studies, University of Melbourne