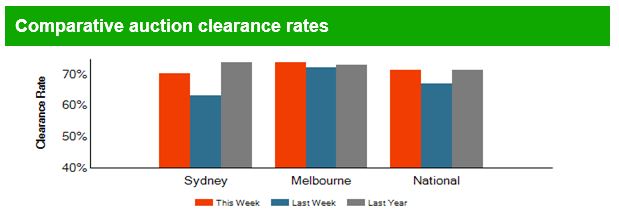

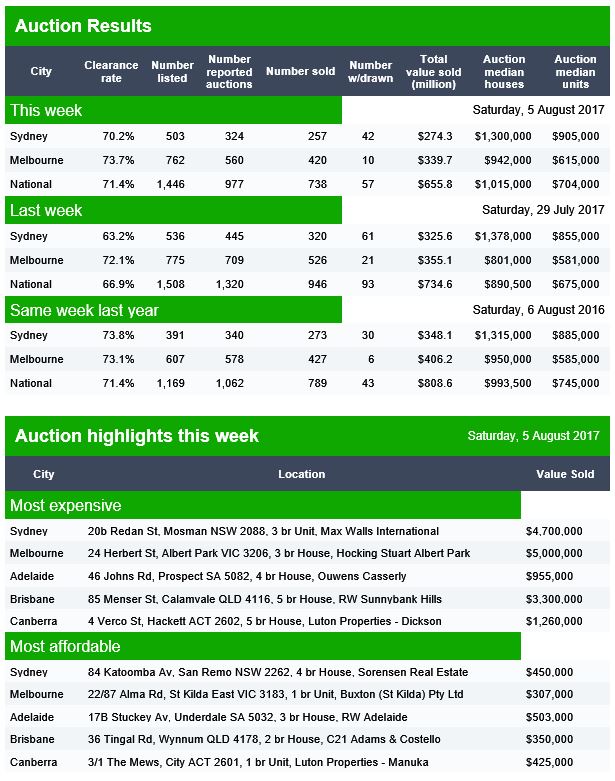

Demand for housing credit remains firm, which explains the ongoing high auction clearance rates. So has the property market further to run and what is the RBA likely to do?

Welcome to the Property Imperative weekly to 12th August 2017, our weekly digest of the latest finance and property news.

Welcome to the Property Imperative weekly to 12th August 2017, our weekly digest of the latest finance and property news.

Company results released this week included the full-year outcomes from the CBA, half year from AMP, and 3rd Quarter results from NAB. There was a common theme through them all. Mortgage loan growth has continued, and thanks to loan and deposit repricing, net interest margins have improved in recent months. This was also helped by more benign conditions in the international capital markets. In addition, overall provisions for bad loans were reduced, despite higher delinquency rates in the troubled Western Australia market. We think the banks, overall, will continue to churn out larger profits as they use repricing to cover the extra regulatory costs and bank taxes. In fact savers are taking a lot of the pain, especially on term deposits, as rates fall even lower, this gets less focus compared with all the commentary is on mortgage interest rates.

Mortgage Brokers were in the news again, this week, with NAB suggesting that changes do need to be made to “improve the trust and confidence that consumers can have in brokers”. UBS put out a research note suggesting that broker commissions will be trimmed soon, whilst CBA reported a fall in the volume of new mortgages sourced via brokers, compared with their branch channels. We are beginning to see significantly differentiated distribution strategies, with some suggesting a migration to digital will reduce the importance of the branch, whilst other lenders, like CBA are investing in new, smaller, outlets with the expectation of driving more business generation through them. On the other hand, CBA, as a result of John Symond exercising his put option, is also buying the remaining 20% interest rest of Aussie Home Loans. Interesting timing!

RBA Governor Philip Lowe’s Opening Statement to the House of Representatives Standing Committee on Economics today contained a few gems.

Globally monetary policy stimulus may be reducing, whilst low wage growth is linked to a complex range of global factors, from technology, competition and lack of security. Locally, business investment is still sluggish, and the RBA says, household are adjusting to lower wage growth plus rising power prices and the burden of household debt. They still back 3% growth in the years ahead. The next move in the cash rate will be up, but not for some time yet.

Ten years ago this week, French bank BNP Paribas wrote a warning of the risks in the US securitised mortgage system. Later, UK lender Northern Rock saw customers queuing to get their money from the bank, a reminder of what happens when confidence fails. Later still, Lehmann Brothers crashed. In the ensuing mayhem, as banks fell from grace and were either left to die, or were bailed out – mostly with public funds – and as mortgage arrears rocketed away in many northern hemisphere centres.

Whilst much has changed, and banks now hold more capital, we still think there are risks in the financial system. In fact, if the RBA does raise rates here, there is a risk we could have our own version of the GFC. It was the sharp move up in mortgage rates which finally triggered the crash a decade ago. We have very high household debt, high home prices, flat income, rising living costs and ultra-low, but rising mortgage rates. We also have a construction boom, with a large supply of new (speculative) property, and banks that have around 60% of their assets in residential property. Arguably lending standards are still too lose despite recent tightening (which note, had to be imposed on the lenders by the regulators!). So the RBA will need to lift rates carefully to avoid a crash.

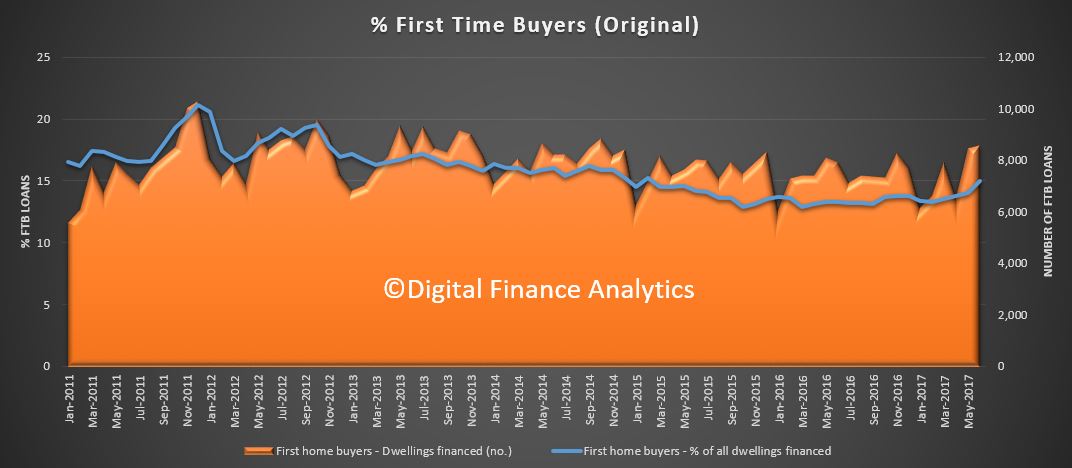

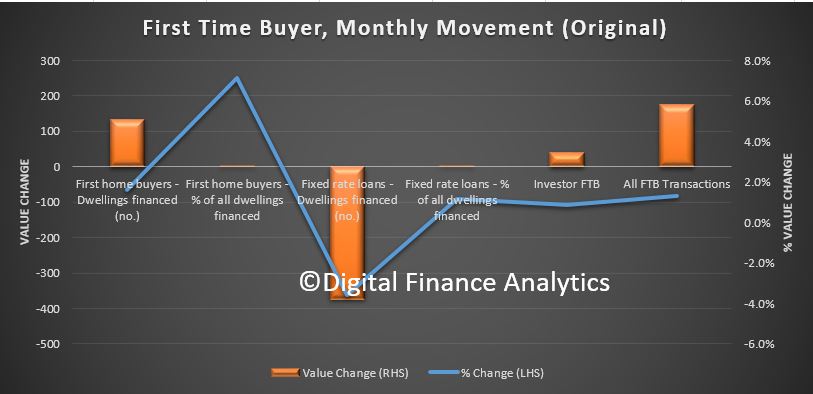

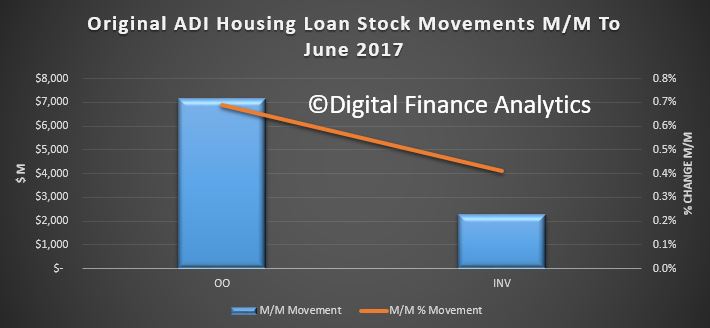

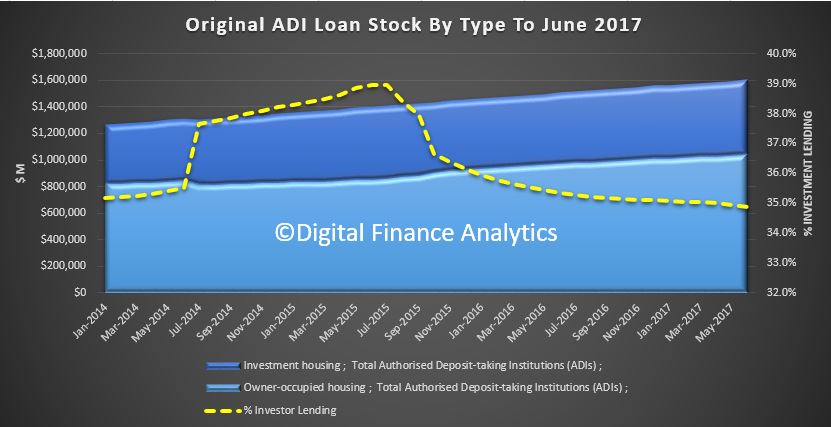

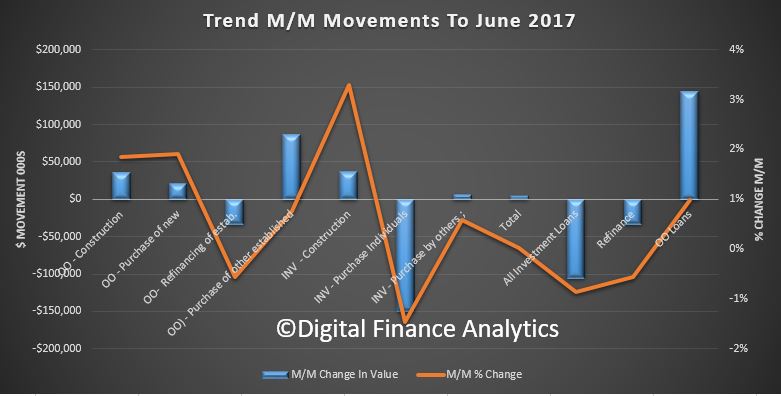

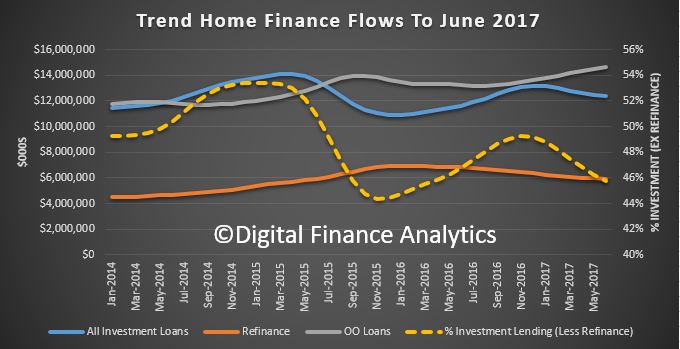

Lending data from the ABS showed owner occupied housing lending rose 0.5% in trend terms in the past month – or around 6% annually, well ahead of inflation. Lending for new construction rose. But lending for investment housing fell 0.85% month on month, despite ongoing strong demand from investors in Sydney and Melbourne. First time buyers were more active in June, they made up 15.0% of transactions, compared with 14.0% in May. Property demand is actually stronger than a couple of months ago as confirmed by the still strong auction clearance rates. Other personal finance fell 1.8%.

The trend series for the value of commercial finance commitments rose 1.8%. Non housing fixed lending rose 3% and revolving credit rose 1.8%. So, perhaps, finally, we see lending by business beginning to gain momentum! This is needed for sustainable growth. The ANZ Job ads were also stronger in July, and the NAB business confidence indicators were also higher. All pointing to strong business investment, perhaps.

On the other hand, the July DFA household finance confidence index was lower with the average score at 99.3, down from 99.8 last month and below the neutral setting. However, the average score masks significant differences across the dimensions of the survey results. For example, younger households are considerably more negative, compared with older groups. This is strongly linked with property owning status, with those renting well below the neutral setting (and more younger households rent these days), whilst owner occupied home owners are significantly more positive. We also see a fall in the confidence of property investors, relative to owner occupied owners. Across the states, we see a small decline in confidence in NSW from a strong starting point, whilst VIC households were more confident in July.

The driver scorecard shows little change in job security expectations, but lower interest rates on deposits continue to hit savings. Households are more concerned about the level of debt held, as interest rate rises bite home. The impact of flat or falling incomes registers strongly, with more households saying, in real terms they are worse off. Costs of living are rising fast, with the changes in energy prices, child care costs and council rates all hitting hard. That said, the continued rises in home prices, especially in the eastern states meant that net worth for households in these states rose again, which was not the case in WA, NT or SA.

Sentiment in the property sector is clearly a major influence on how households are feeling about their finances, but the real dampening force is falling real incomes and rising costs. As a result, we still expect to see the index fall further as we move into spring, as more price hikes come through. In addition, the raft of investor mortgage rate repricing will hit, whilst rental returns remain muted.

So, overall, we see a mixed and complex picture, with demand for property remaining firm, lending still rising, incomes still under pressure and lenders able to buttress their profits thanks to lifting margins. This puts pressure on the RBA, who continues to warn of the risks to households but then cannot lift rates very far. This tension will all play out, not just in the next few months, but over the next two or three years.

And that’s the Property Imperative to 12th August 2017. If you found this useful, do subscribe to get future updates, and check back for the latest installment.